COP26 saw renewed calls for high-income countries to do more to finance the energy transitions of developing countries and particularly in Africa. Private partnerships, public-private partnerships and blended finance all have a part to play in funding and shaping the continent’s move to clean energy. Beyond financing, however, it is the task of wealthier nations to ensure Africa’s green transition is also a just transition.

The State of Play

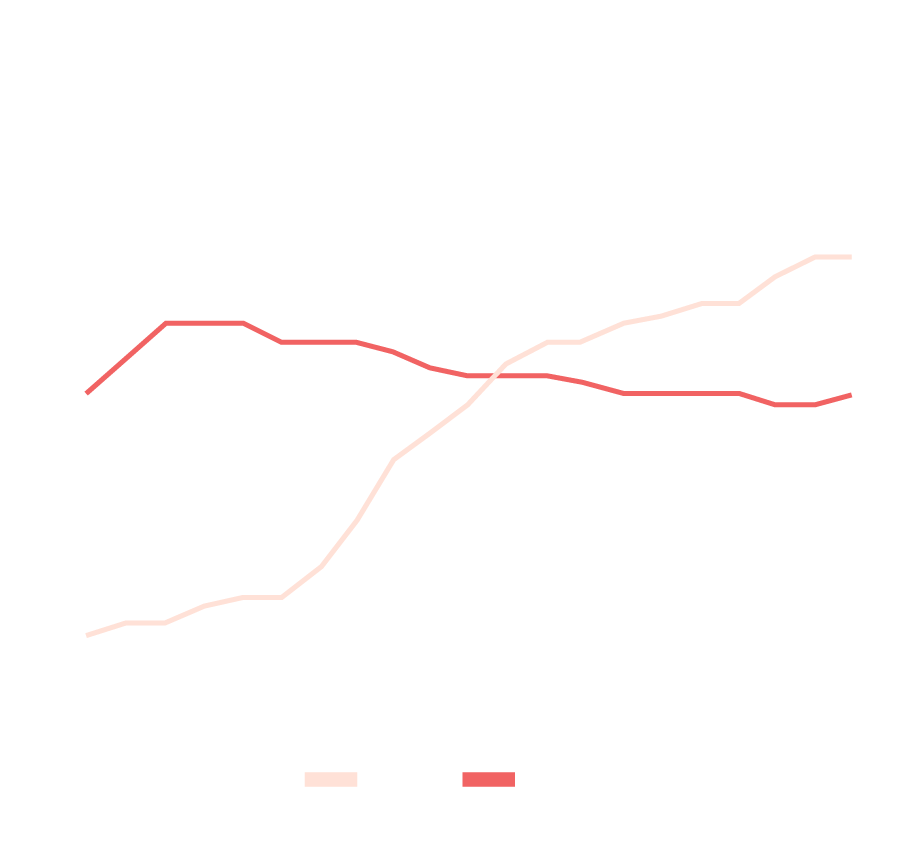

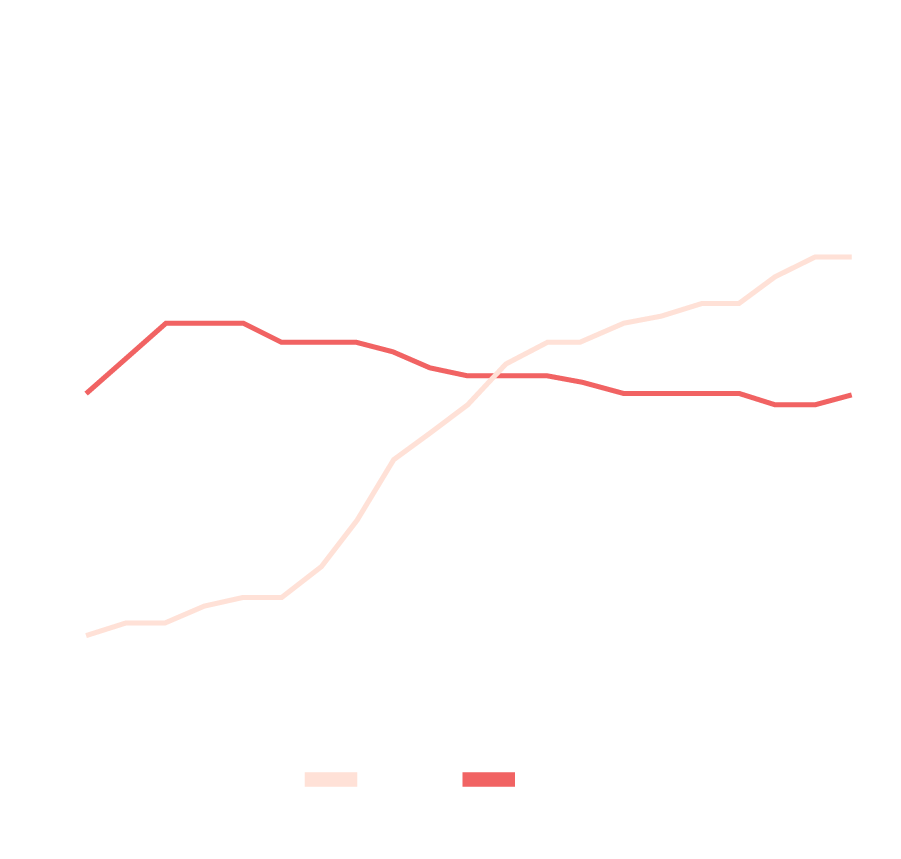

With 35 out of Africa’s 54 nations already committed to reaching net zero carbon emissions by 2050, an estimated $2.8tn is required just to convert the continent’s current energy base to clean energy sources1. Following COP26, the U.S., UK, EU, France, and Germany pledged $8.5bn to hasten South Africa’s transition from coal. There has also been growing momentum from a broad range of public and private investors. Renewable projects across Africa are increasing, with an annual growth rate of 21% between 2010 and 2020, according to PwC2.

Africa’s growth trajectory alone gives it a pivotal strategic role in the global energy transition. By 2050, it is predicted that one in four people on Earth will live in Africa. Already housing 17% of the global population, the continent generates less than 5% of global emissions3, while also suffering some of the worst effects of climate change.

The imbalance between population and global emissions has even led to debate about whether Africa’s net zero targets are fair and appropriate. At COP26, Rashid Abdallah, Executive Director of the African Energy Commission, argued the continent is essentially carbon neutral, given 600 million Africans have no electricity4. It is inequitable, Abdallah and others argue, to hold Africa to the same targets as high earning countries with much larger carbon footprints.

COP26 saw renewed calls for high-income countries to do more to finance the energy transitions of developing countries and particularly in Africa. Private partnerships, public-private partnerships and blended finance all have a part to play in funding and shaping the continent’s move to clean energy. Beyond financing, however, it is the task of wealthier nations to ensure Africa’s green transition is also a just transition.

The State of Play

With 35 out of Africa’s 54 nations already committed to reaching net zero carbon emissions by 2050, an estimated $2.8tn is required just to convert the continent’s current energy base to clean energy sources1. Following COP26, the U.S., UK, EU, France, and Germany pledged $8.5bn to hasten South Africa’s transition from coal. There has also been growing momentum from a broad range of public and private investors. Renewable projects across Africa are increasing, with an annual growth rate of 21% between 2010 and 2020, according to PwC2.

Africa’s growth trajectory alone gives it a pivotal strategic role in the global energy transition. By 2050, it is predicted that one in four people on Earth will live in Africa. Already housing 17% of the global population, the continent generates less than 5% of global emissions3, while also suffering some of the worst effects of climate change.

The imbalance between population and global emissions has even led to debate about whether Africa’s net zero targets are fair and appropriate. At COP26, Rashid Abdallah, Executive Director of the African Energy Commission, argued the continent is essentially carbon neutral, given 600 million Africans have no electricity4. It is inequitable, Abdallah and others argue, to hold Africa to the same targets as high earning countries with much larger carbon footprints.

Leapfrogging to a Green Industrialisation

Africa has huge potential for renewable energy – particularly solar and hydroelectric. A green energy revolution, if handled correctly, offers significant opportunities to unlock Africa’s social and economic potential. Moreover, its underdeveloped energy infrastructure is viewed by some as an opportunity to bypass fossil fuels entirely and move directly to clean energy – known as ‘leapfrogging’ or ‘green industrialisation’5. Renewable energy could create huge socio-economic opportunities for Africa – particularly in rural communities, where improved energy access through mini-grids and off-grid solutions, would boost economic activity.

Though this vision is appealing, however, it requires planning, funding, and international cooperation from developed countries, which has not been forthcoming. Many African governments also need to reform legislative frameworks to make them more attractive to private investors – something politics does not always allow. If the energy transition is to be handled equitably, funding should also include financial compensation for the stalling of Africa’s fossil fuel reserves, with an estimated worth of more than $15.2tn6.

The Fossil Fuel Dilemma

Studies suggest that limiting global warming to 1.5°C will require nearly 60% of current oil and gas reserves and nearly 90% of coal reserves to stay in the ground7. For Africa, this essentially means stranding assets worth trillions of dollars which could turbocharge its economies – just as coal did in Europe’s industrial revolution. More than a third of African economies already depend heavily on fossil fuels for state revenue. For example, income from oil and gas accounted in 2019 for 4.9% of Ghana’s total GDP, 8.4% in Nigeria (and fuels represent over 85% of the country’s exports8) and as much as 16.3% in Algeria (the world’s sixth-largest gas exporter9), 25.8% in Angola and 44.7% in Republic of Congo10.

However, many investors are moving away from fossil fuels on environmental grounds. While this logic is understandable, simply pulling investments in African fossil fuels without compensating some of the world’s poorest countries (also among the worst hit by COVID-19) is inequitable and counterproductive. Fossil fuel projects are pivotal to many African economies. Their governments will simply look elsewhere for investment and are likely to find it. This then removes the ability of developed countries and responsible investors to work with Africa in the wider strategic planning around an energy transition, which must happen in some form.

Mozambique and the Role of Gas in Africa’s Transition

Natural gas – North Africa’s most widely used energy – could have a significant role to play in Africa’s and the world’s shift towards a low carbon economy. It has a considerably lower carbon footprint than coal and is also required for fertiliser, which is essential to Africa’s future agricultural needs. The West African Power Pool masterplan estimates lack of electricity access in Nigeria alone costs over $30bn per year11. Gas, it argues, is the cheapest, most practical solution to Africa’s electricity shortfall, as many nations already have domestic gas resources.

The Mozambique LNG Project (Britain’s funding for which is currently under legal challenge by Friends of the Earth) could create tens of thousands of jobs and lift millions out of poverty. Nearly half of Mozambique’s population live below the poverty line and just over a third have access to electricity12. Accounting for just 0.02% of global carbon emissions, Mozambique also ranks among the nations most vulnerable to climate change13. Bringing electricity to the country’s rural areas would reduce both deforestation and emissions caused by burning firewood and charcoal.

Mozambique’s LNG reserves could also help lift neighbouring nations, such as Zimbabwe, out of energy poverty. It could even supply Asia’s growing LNG market, which includes China, India, and South Korea – three of the largest producers of carbon emissions – helping the shift away from coal. If China – responsible for 28% of global emissions and reliant on coal for 70% of its energy needs14 – pivots decisively towards gas, it could significantly lower its carbon footprint.

Mozambique and the Role of Gas in Africa’s Transition

Natural gas – North Africa’s most widely used energy – could have a significant role to play in Africa’s and the world’s shift towards a low carbon economy. It has a considerably lower carbon footprint than coal and is also required for fertiliser, which is essential to Africa’s future agricultural needs. The West African Power Pool masterplan estimates lack of electricity access in Nigeria alone costs over $30bn per year11. Gas, it argues, is the cheapest, most practical solution to Africa’s electricity shortfall, as many nations already have domestic gas resources.

The Mozambique LNG Project (Britain’s funding for which is currently under legal challenge by Friends of the Earth) could create tens of thousands of jobs and lift millions out of poverty. Nearly half of Mozambique’s population live below the poverty line and just over a third have access to electricity12. Accounting for just 0.02% of global carbon emissions, Mozambique also ranks among the nations most vulnerable to climate change13. Bringing electricity to the country’s rural areas would reduce both deforestation and emissions caused by burning firewood and charcoal.

Mozambique’s LNG reserves could also help lift neighbouring nations, such as Zimbabwe, out of energy poverty. It could even supply Asia’s growing LNG market, which includes China, India, and South Korea – three of the largest producers of carbon emissions – helping the shift away from coal. If China – responsible for 28% of global emissions and reliant on coal for 70% of its energy needs14 – pivots decisively towards gas, it could significantly lower its carbon footprint.

Conclusion

Africa must ultimately commit to net zero – to do otherwise, would mean falling behind global markets. While developing renewable energy must be a common objective, it is the duty of developed countries to help ensure the shape of this transition protects developing countries, including in Africa, from suffering dire human and economic costs in the process. This may mean pursuing a low carbon, rather than a net zero path, including by maintaining funding for advanced non-renewable energy projects – at least for the time being.