2025: Heralding a New Regulatory

Era for Private Funds and Advisers

March 2025

There can be no doubt that 2024 marked a pronounced turning point in the regulation of private funds and their advisers after the first three years of Securities and Exchange Commission (“SEC”) Chair Gary Gensler’s tenure, during which he doggedly pursued an agenda of imposing a retail-like disclosure and restrictions framework on the private funds industry.

Indeed, a year that began with the SEC having implemented the most comprehensive set of proposed and final new rules and amendments since the Dodd-Frank Act of 2010 ended in conspicuous quiet.

The vacatur of the Private Fund Adviser Rules (PFAR) in June 2024 was, of course, a pivotal moment. The Fifth Circuit’s rebuke of the SEC’s statutory authority in the PFAR decision, combined with the presidential election and the nomination of new SEC Chair Paul Atkins, stalled final versions of many live proposals in the second half of 2024 and largely halted new rulemaking.

There can be no doubt that 2024 marked a pronounced turning point in the regulation of private funds and their advisers after the first three years of Securities and Exchange Commission (“SEC”) Chair Gary Gensler’s tenure, during which he doggedly pursued an agenda of imposing a retail-like disclosure and restrictions framework on the private funds industry.

Indeed, a year that began with the SEC having implemented the most comprehensive set of proposed and final new rules and amendments since the Dodd-Frank Act of 2010 ended in conspicuous quiet.

The vacatur of the Private Fund Adviser Rules (PFAR) in June 2024 was, of course, a pivotal moment. The Fifth Circuit’s rebuke of the SEC’s statutory authority in the PFAR decision, combined with the presidential election and the nomination of new SEC Chair Paul Atkins, stalled final versions of many live proposals in the second half of 2024 and largely halted new rulemaking.

Enforcement

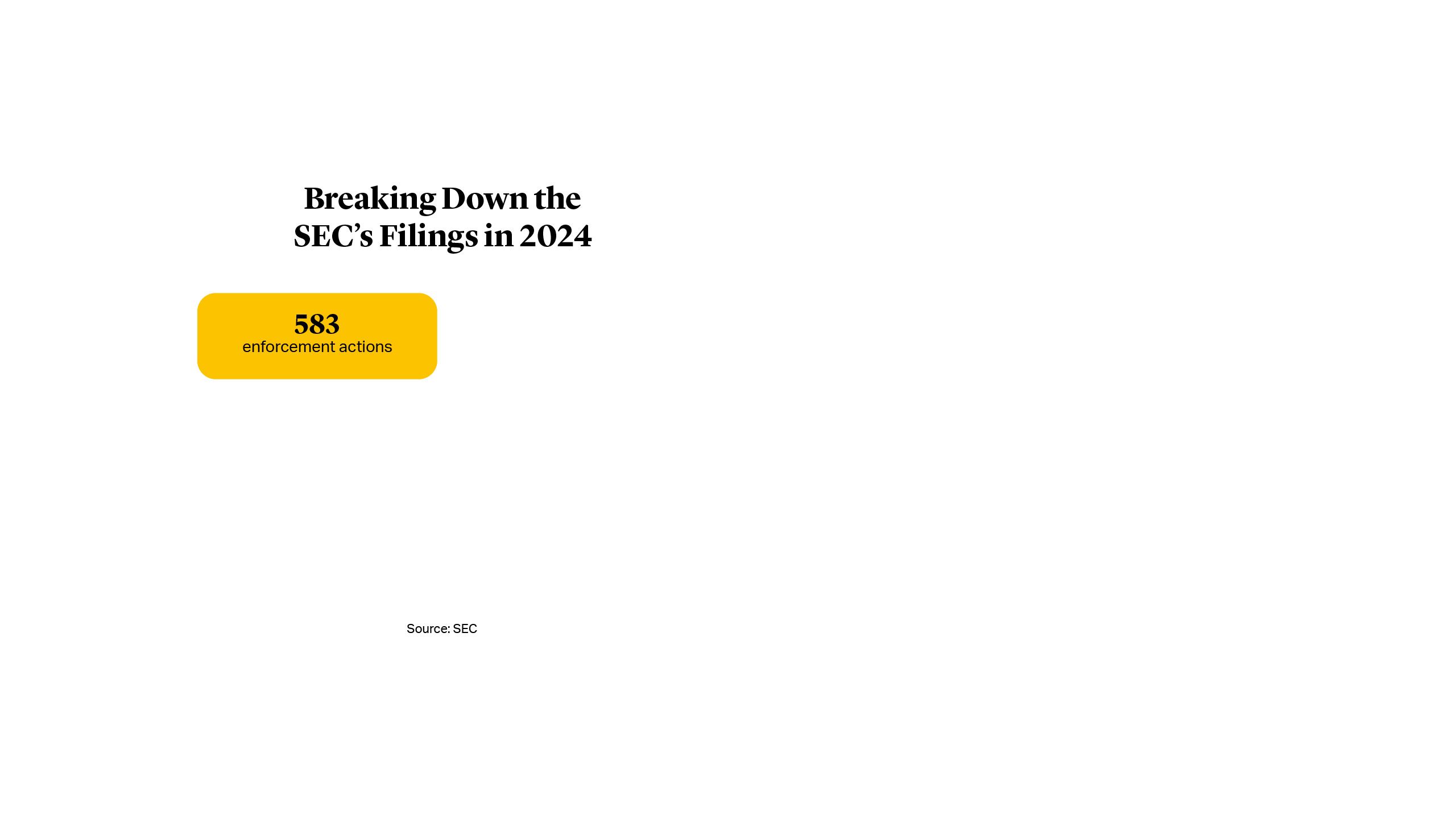

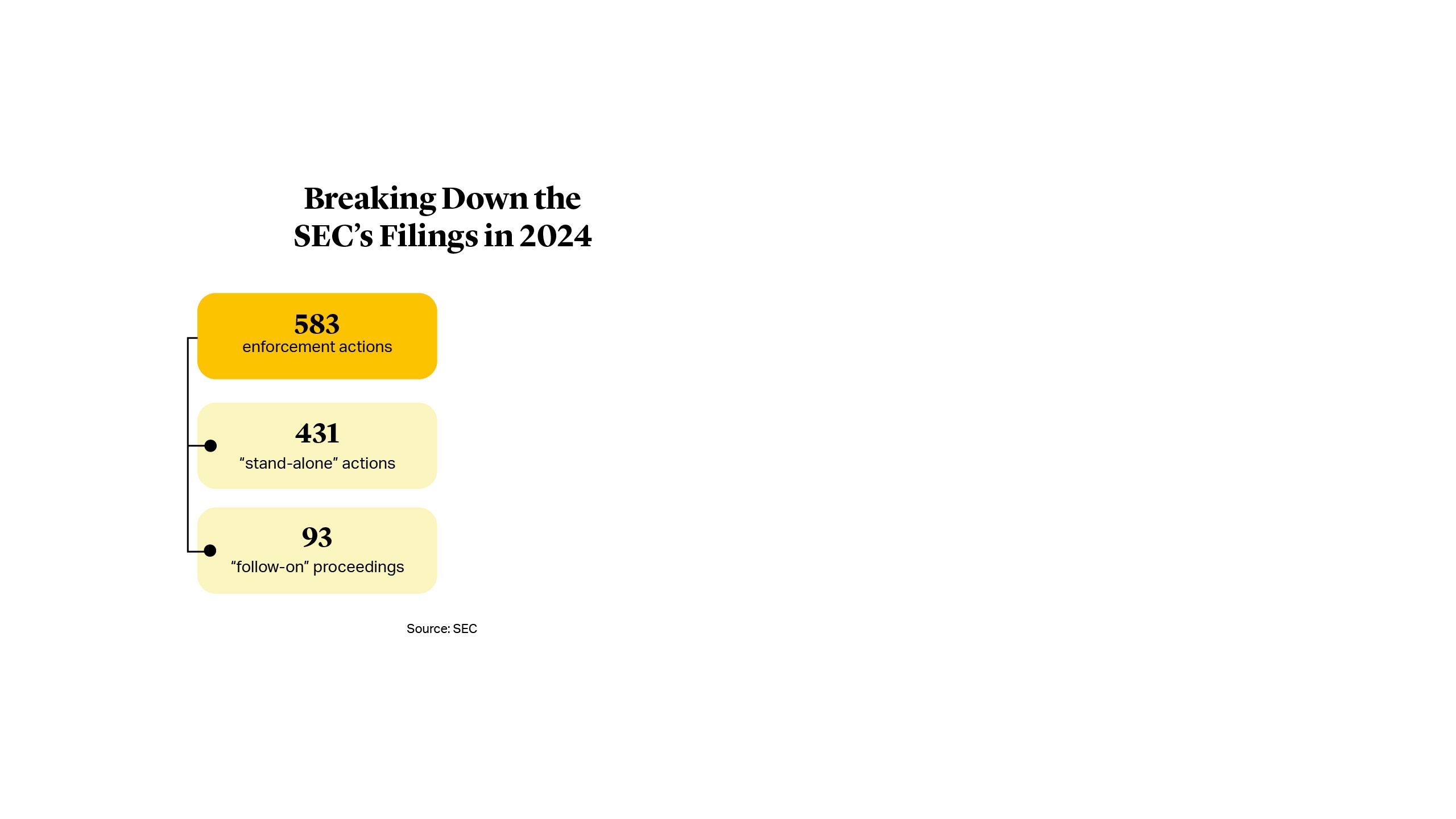

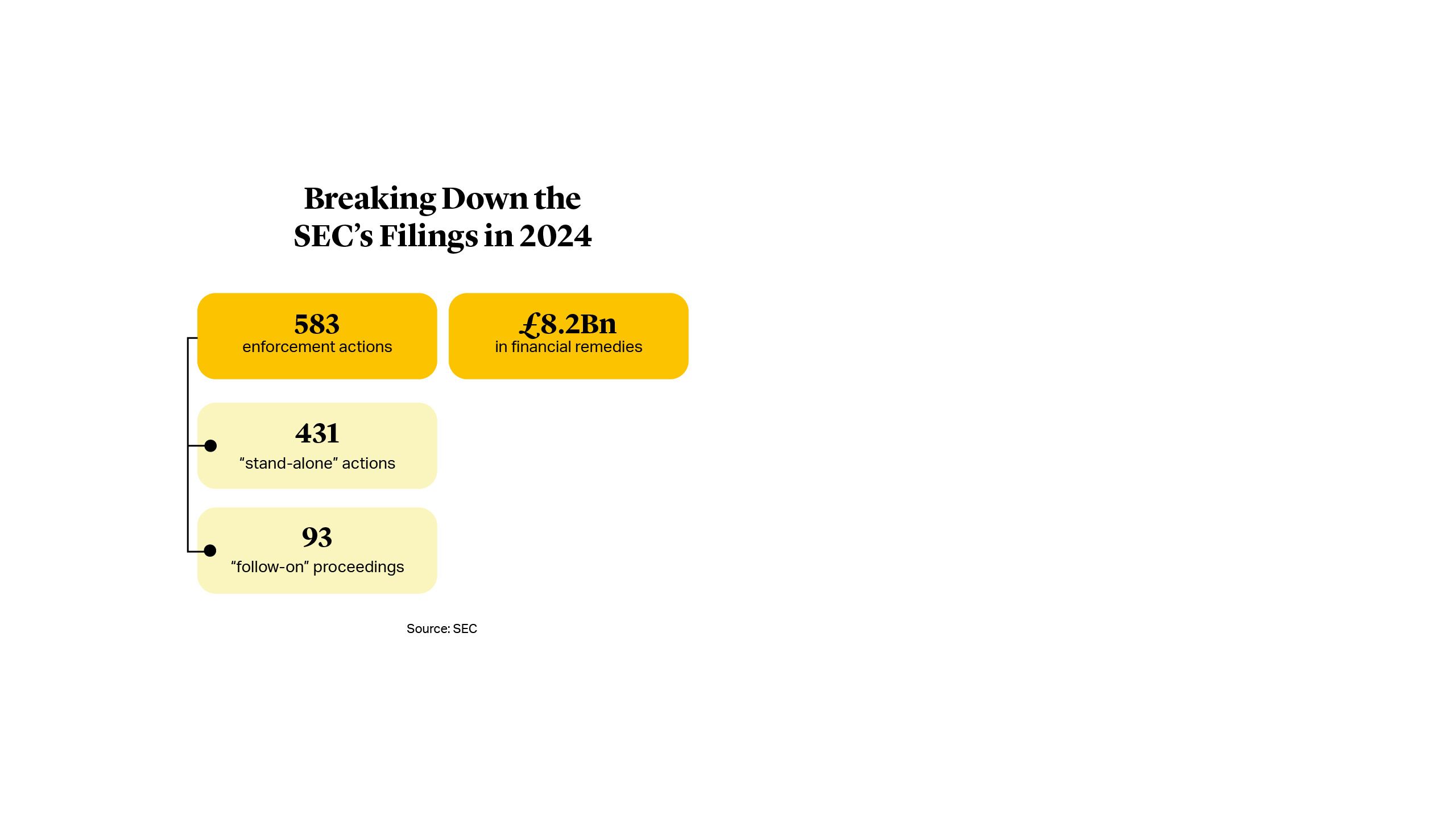

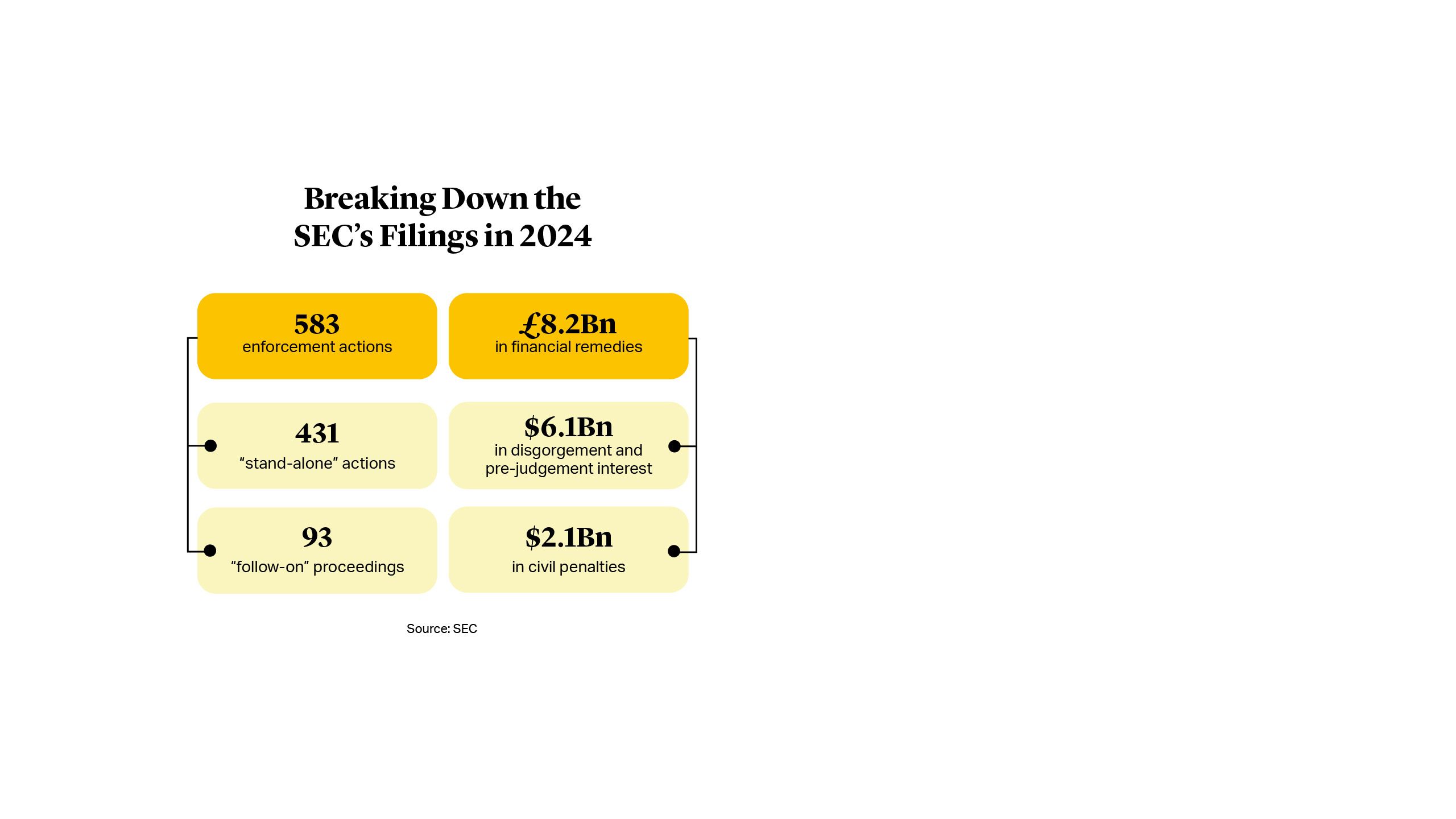

This is not to say that the SEC put its foot on the brake altogether. Enforcement activity, in stark contrast to rulemaking, continued at high speed even through the last day of the outgoing administration in January 2025. The SEC filed 583 enforcement actions in fiscal year 2024, obtaining orders for $8.2bn in financial remedies – the highest in the regulator’s history.

In the context of private fund advisers in particular, the SEC maintained its steadfast focus on post-commitment period management fee calculations, recordkeeping, and off-channel communications, as well as fees and expenses disclosures.

Material non-public information (MNPI) was also a clear area of interest, with enforcement actions relating not just to actual insider trading allegations but also to alleged deficiencies in advisers’ policies and procedures for preventing misuse of MNPI.

Meanwhile, the SEC conducted additional enforcement sweeps relating to the Marketing Rule and continued to focus on compliance with the Rule in examinations and related enforcement actions. This included charging advisers with violations such as advertising hypothetical performance without adequate policies and procedures and/or disclosure, making untrue or unsubstantiated statements of material fact, and using testimonials, endorsements, or third-party ratings without required disclosures.

SEC Enforcement Director Gurbir Grewal’s departure from the agency in October last year, followed by the resignation of Acting Director Sanjay Wadhwa, has set the stage for a meaningful shift in enforcement strategy in 2025.

Enforcement

This is not to say that the SEC put its foot on the brake altogether. Enforcement activity, in stark contrast to rulemaking, continued at high speed even through the last day of the outgoing administration in January 2025. The SEC filed 583 enforcement actions in fiscal year 2024, obtaining orders for $8.2bn in financial remedies – the highest in the regulator’s history.

In the context of private fund advisers in particular, the SEC maintained its steadfast focus on post-commitment period management fee calculations, recordkeeping, and off-channel communications, as well as fees and expenses disclosures.

Material non-public information (MNPI) was also a clear area of interest, with enforcement actions relating not just to actual insider trading allegations but also to alleged deficiencies in advisers’ policies and procedures for preventing misuse of MNPI.

Meanwhile, the SEC conducted additional enforcement sweeps relating to the Marketing Rule and continued to focus on compliance with the Rule in examinations and related enforcement actions. This included charging advisers with violations such as advertising hypothetical performance without adequate policies and procedures and/or disclosure, making untrue or unsubstantiated statements of material fact, and using testimonials, endorsements, or third-party ratings without required disclosures.

SEC Enforcement Director Gurbir Grewal’s departure from the agency in October last year, followed by the resignation of Acting Director Sanjay Wadhwa, has set the stage for a meaningful shift in enforcement strategy in 2025.

Breaking Down the SEC's Filings in 2024

Source: SEC

What Next?

With respect to enforcement, the general expectation is that under a new presidential administration, new SEC Chair, and new Director of Enforcement, there is likely to be a shift in focus back to violations of securities laws with the potential for market manipulation or other harm, such as insider trading or fraud, as opposed to deficiencies in policies and procedures or other more technical violations. Going forward, Enforcement staff may take a less expansive approach to materiality and engage in fewer practices that could be deemed “regulation by enforcement.” There may also be a shift back in focus towards the protection of retail investors, with the spotlight leaving private funds and advisers.

With respect to rules and regulations, the previous SEC leadership has left some unanswered questions but also opportunities. So, what possibilities may exist in the years ahead for the industry to work with the SEC on existing rules, and what new proposals may be on the horizon?

What Next?

With respect to enforcement, the general expectation is that under a new presidential administration, new SEC Chair, and new Director of Enforcement, there is likely to be a shift in focus back to violations of securities laws with the potential for market manipulation or other harm, such as insider trading or fraud, as opposed to deficiencies in policies and procedures or other more technical violations. Going forward, Enforcement staff may take a less expansive approach to materiality and engage in fewer practices that could be deemed “regulation by enforcement.” There may also be a shift back in focus towards the protection of retail investors, with the spotlight leaving private funds and advisers.

With respect to rules and regulations, the previous SEC leadership has left some unanswered questions but also opportunities. So, what possibilities may exist in the years ahead for the industry to work with the SEC on existing rules, and what new proposals may be on the horizon?

Artificial Intelligence and Emerging Regulatory Frameworks

Emerging regulatory frameworks concerning the use of artificial intelligence (AI) are likely to be a high priority.

The Predictive Data Analytics rules were proposed as the SEC’s significant step towards regulating how registered advisers and broker-dealers approach various deployments of AI-driven tools and management of associated conflicts of interest.

The 2023 proposal met with significant industry backlash and criticism. In June 2024, shortly following the Fifth Circuit’s PFAR decision, Gensler publicly stated that the SEC planned to re-propose the rules in a different form, rather than moving to the finalization phase.

Artificial Intelligence and Emerging Regulatory Frameworks

Emerging regulatory frameworks concerning the use of artificial intelligence (AI) are likely to be a high priority.

The Predictive Data Analytics rules were proposed as the SEC’s significant step towards regulating how registered advisers and broker-dealers approach various deployments of AI-driven tools and management of associated conflicts of interest.

The 2023 proposal met with significant industry backlash and criticism. In June 2024, shortly following the Fifth Circuit’s PFAR decision, Gensler publicly stated that the SEC planned to re-propose the rules in a different form, rather than moving to the finalization phase.

However, to date, the SEC has not offered a new proposal or made any further public statements. Gensler is widely viewed as a staunch champion of the Predictive Data Analytics rules and the notion of regulating advisers’ uses of AI generally. Under Gensler, the SEC also conducted AI-focused enforcement sweeps of registered advisers, seeking information on topics ranging from advisers’ AI-related policies and procedures, to mentions of AI in fund marketing materials, as well as deployments of AI in algorithms or other trading architecture.

It remains to be seen how the new SEC regime will address the topic, particularly in light of the expected desire to foster innovation. In December, the Commodities Futures Trading Commission (CFTC) issued a staff advisory on the use of AI in CFTC-regulated markets. The advisory reminded CFTC-regulated entities of their obligations under the Commodity Exchange Act and the CFTC’s regulations as these entities begin to implement AI. In it, the CFTC highlighted that its staff are closely tracking the development of AI technology and AI’s potential benefits and risks.

However, to date, the SEC has not offered a new proposal or made any further public statements. Gensler is widely viewed as a staunch champion of the Predictive Data Analytics rules and the notion of regulating advisers’ uses of AI generally. Under Gensler, the SEC also conducted AI-focused enforcement sweeps of registered advisers, seeking information on topics ranging from advisers’ AI-related policies and procedures, to mentions of AI in fund marketing materials, as well as deployments of AI in algorithms or other trading architecture.

It remains to be seen how the new SEC regime will address the topic, particularly in light of the expected desire to foster innovation. In December, the Commodities Futures Trading Commission (CFTC) issued a staff advisory on the use of AI in CFTC-regulated markets. The advisory reminded CFTC-regulated entities of their obligations under the Commodity Exchange Act and the CFTC’s regulations as these entities begin to implement AI. In it, the CFTC highlighted that its staff are closely tracking the development of AI technology and AI’s potential benefits and risks.

The Atkins Agenda

Attention is now turning to what President Trump’s nominee and expected new SEC Chair Paul Atkins may bring to the role.

Atkins is a former SEC Commissioner who served from 2002 until 2008, when he resigned after the collapse of Lehman Brothers. Most recently, however, he has worked with Securitize, a company providing tokenized exposure to private funds.

The Atkins Agenda

Attention is now turning to what President Trump’s nominee and expected new SEC Chair Paul Atkins may bring to the role.

Atkins is a former SEC Commissioner who served from 2002 until 2008, when he resigned after the collapse of Lehman Brothers. Most recently, however, he has worked with Securitize, a company providing tokenized exposure to private funds.

During Trump’s previous presidency, the SEC expanded its definition of “accredited investor” to include individuals who meet certain criteria beyond just net worth and income. Although further expansion of qualification criteria by the SEC is uncertain, there has also been recent Congressional interest in a legislative push to broaden such criteria; in addition, the nomination of Atkins, who in the past has voiced support for opening up access to alternative asset classes, would suggest increased opportunities for the so-called democratization of private markets.

Atkins is also expected to move away from regulation by enforcement and to favor public input on regulations. Throughout his time as SEC Commissioner, he consistently advocated for a collaborative approach to rulemaking, emphasizing cost-benefit analysis and adherence to statutory authority, with the aim of promoting market efficiency and innovation.

More generally, Atkins is known to believe that private funds were appropriately regulated under historical standards and that sophisticated investors in these funds are equipped to protect themselves from abusive practices, opening up the possibility of revisiting some more recent aspects of private markets regulation.

During Trump’s previous presidency, the SEC expanded its definition of “accredited investor” to include individuals who meet certain criteria beyond just net worth and income. Although further expansion of qualification criteria by the SEC is uncertain, there has also been recent Congressional interest in a legislative push to broaden such criteria; in addition, the nomination of Atkins, who in the past has voiced support for opening up access to alternative asset classes, would suggest increased opportunities for the so-called democratization of private markets.

Atkins is also expected to move away from regulation by enforcement and to favor public input on regulations. Throughout his time as SEC Commissioner, he consistently advocated for a collaborative approach to rulemaking, emphasizing cost-benefit analysis and adherence to statutory authority, with the aim of promoting market efficiency and innovation.

More generally, Atkins is known to believe that private funds were appropriately regulated under historical standards and that sophisticated investors in these funds are equipped to protect themselves from abusive practices, opening up the possibility of revisiting some more recent aspects of private markets regulation.

Opportunities for

Industry Advocacy

As the regulatory landscape transitions under new leadership, private fund advisers and industry groups have an opportunity to engage with the SEC and influence the direction of key policies.

Form PF

In December 2024, industry groups submitted a letter to the SEC in December requesting an extension of the compliance date for Form PF amendments. In January 2025, the SEC, together with the CFTC, extended the compliance deadline for the amendments to Form PF to June 12, 2025. This extension gives private fund advisers more time to prepare and seek guidance on the significant changes to the form.

The Marketing Rule

There may also be opportunities to engage with the new SEC regime on the Marketing Rule, which was originally intended to modernize the regulatory overlay of adviser marketing activity, but which has proved to be extremely cumbersome in practice and has been the source of multiple enforcement issues.

A reversion to a more principles-based approach that affords greater flexibility in the design of disclosures and marketing materials, would undoubtedly be welcomed by the industry, whether that comes in the form of FAQs or no action relief.

Opportunities for

Industry Advocacy

As the regulatory landscape transitions under new leadership, private fund advisers and industry groups have an opportunity to engage with the SEC and influence the direction of key policies.

Form PF

In December 2024, industry groups submitted a letter to the SEC in December requesting an extension of the compliance date for Form PF amendments. In January 2025, the SEC, together with the CFTC, extended the compliance deadline for the amendments to Form PF to June 12, 2025. This extension gives private fund advisers more time to prepare and seek guidance on the significant changes to the form.

The Marketing Rule

There may also be opportunities to engage with the new SEC regime on the Marketing Rule, which was originally intended to modernize the regulatory overlay of adviser marketing activity, but which has proved to be extremely cumbersome in practice and has been the source of multiple enforcement issues.

A reversion to a more principles-based approach that affords greater flexibility in the design of disclosures and marketing materials, would undoubtedly be welcomed by the industry, whether that comes in the form of FAQs or no action relief.

ESG

A second Trump administration is likely to mean that further federal laws driving ESG disclosure are stalled indefinitely and ESG is expected to be a low priority for federal regulators in terms of both rulemaking and enforcement activity. There may also be initiatives at the state level to advance anti-ESG regulations during what would be a more favorable political climate.

This is in direct contrast to many other parts of the world, most notably the EU, which is actively considering updates to its Sustainable Finance Disclosure Regime (SFDR). What may result is an increased disparity of sustainability-related regulatory regimes for private fund managers operating globally or with a global investor base.

ESG

A second Trump administration is likely to mean that further federal laws driving ESG disclosure are stalled indefinitely and ESG is expected to be a low priority for federal regulators in terms of both rulemaking and enforcement activity. There may also be initiatives at the state level to advance anti-ESG regulations during what would be a more favorable political climate.

This is in direct contrast to many other parts of the world, most notably the EU, which is actively considering updates to its Sustainable Finance Disclosure Regime (SFDR). What may result is an increased disparity of sustainability-related regulatory regimes for private fund managers operating globally or with a global investor base.

Looking Ahead

The private funds industry is emerging from a period during which it was the subject of intense regulatory scrutiny, with a proliferation of prescriptive proposals and aggressive enforcement action.

This year could herald potentially dramatic shifts in interpretations and enforcement approaches. Private fund advisers will need to stay abreast of, and be ready to act on, the latest changes.

However, 2025 may also be a year in which there will be opportunities to help shape a regulatory environment that is more responsive to, and supportive of, the private funds industry going forward.