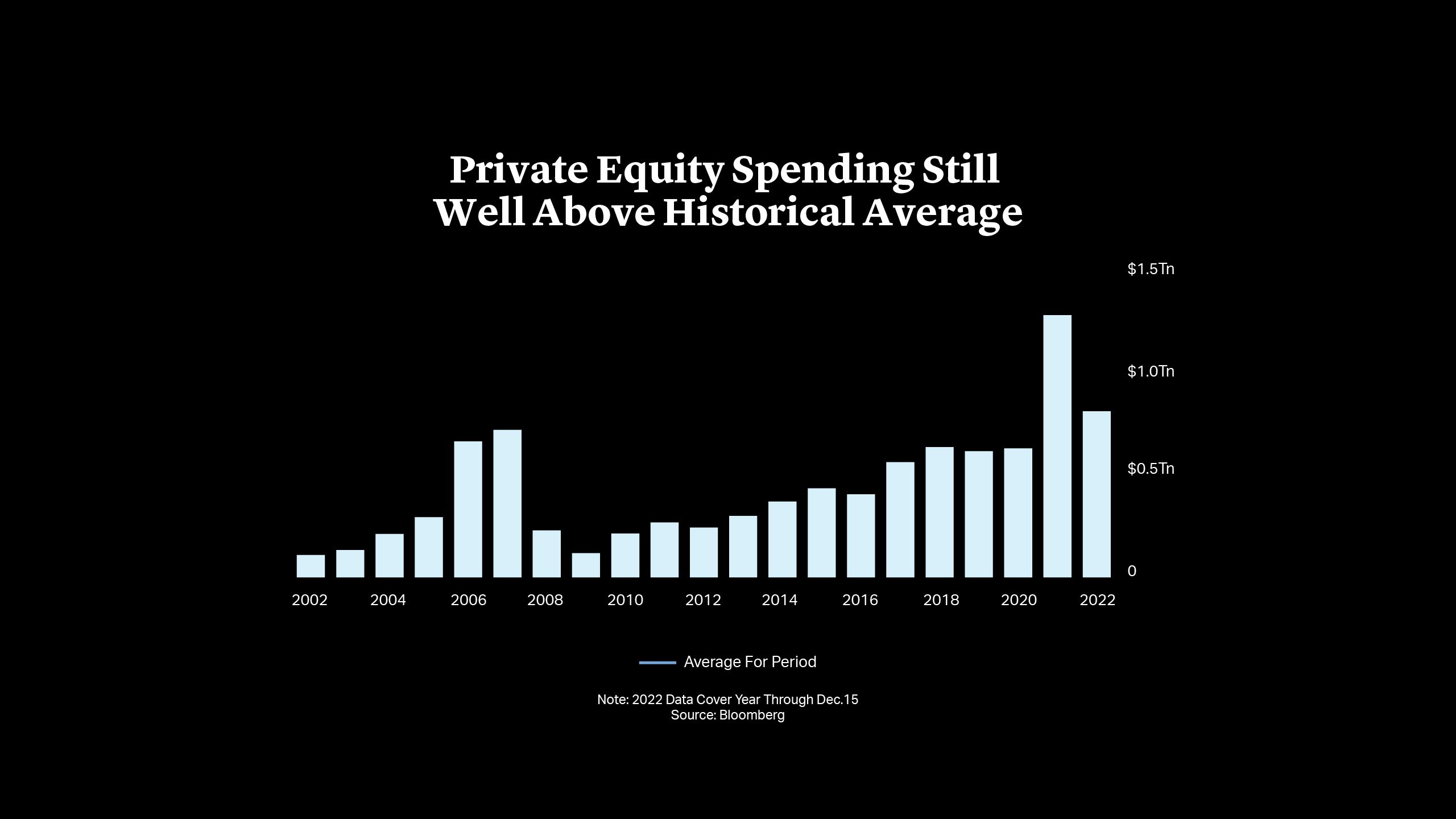

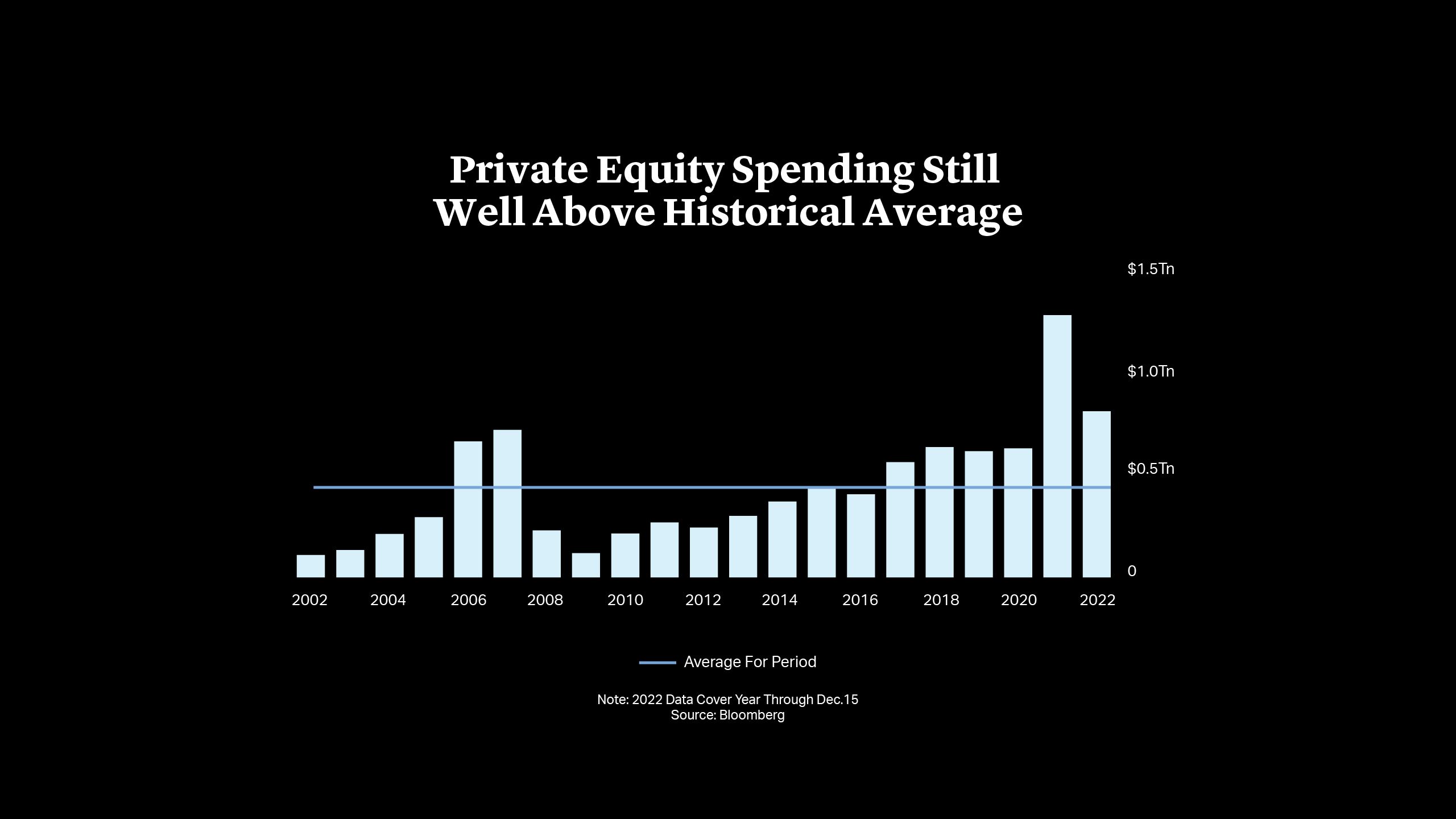

Private Equity Seeks Ways Through

Dealmaking Uncertainty

Global markets are at an inflection point. After the rapid increase in interest rates throughout 2022, investors are wondering whether central banks have done enough to tame inflation – or perhaps if they have gone too far. In Europe, the European Central Bank has indicated further interest rate rises stretching into 2023 and predicted persistent cost-push inflation1. While a soft economic landing in the U.S. remains a possibility, the EU is predicting recession across many member states2. In the UK, economists at KPMG anticipate recession lasting until the end of 20233.

European Financing Markets to Remain Subdued in H1

Against the volatile European economic backdrop, there is uncertainty around private equity investment strategy, with many sponsors waiting for stronger signals of a turnaround, or at least that the bottom has been reached. On top of macroeconomic challenges is the availability of debt, with EQT’s CEO Christian Sinding not expecting banks to return to financing in force before the second half of 20234.

In that context, private equity firms that have already raised sizeable funds are likely to continue to execute deals using larger equity cheques, in the hope of leveraging their deals in the future. KKR’s acquisition of a majority stake in French insurer April Group, valued at €2.3bn, was reported to be an all-cash transaction5. Co-CEO Scott Nuthall said on an earnings call in November that the industry “may lean a bit more on the private credit market” in the current environment, as well as some portable capital structures. Private lending is already well established in Europe. According to Permira’s Head of Private Credit, David Hirschmann, private debt-backed transactions now account for the majority of European mid-market private equity deal financing6.

Private lenders are also increasingly moving into larger investments. In December, Sixth Street led financing packages for Thoma Bravo’s purchase of U.S. software firm Coupa, and Advent International’s buy of satellite operator Maxar Technologies7. We expect to see this trend followed in Europe.

European Financing Markets to Remain Subdued in H1

Against the volatile European economic backdrop, there is uncertainty around private equity investment strategy, with many sponsors waiting for stronger signals of a turnaround, or at least that the bottom has been reached. On top of macroeconomic challenges is the availability of debt, with EQT’s CEO Christian Sinding not expecting banks to return to financing in force before the second half of 20234.

In that context, private equity firms that have already raised sizeable funds are likely to continue to execute deals using larger equity cheques, in the hope of leveraging their deals in the future. KKR’s acquisition of a majority stake in French insurer April Group, valued at €2.3bn, was reported to be an all-cash transaction5. Co-CEO Scott Nuthall said on an earnings call in November that the industry “may lean a bit more on the private credit market” in the current environment, as well as some portable capital structures. Private lending is already well established in Europe. According to Permira’s Head of Private Credit, David Hirschmann, private debt-backed transactions now account for the majority of European mid-market private equity deal financing6.

Private lenders are also increasingly moving into larger investments. In December, Sixth Street led financing packages for Thoma Bravo’s purchase of U.S. software firm Coupa, and Advent International’s buy of satellite operator Maxar Technologies7. We expect to see this trend followed in Europe.

Deal Structures for Potential Downturns

In addition to more reliance on private lenders, private equity firms in Europe are turning to alternative investment techniques. The disconnect between buyer and seller price expectations, as well as caution around company performance, is also encouraging deal terms and products that can help bridge the valuation gap and give added protection to buyers.

As we noted in November’s Private Equity Market Wrap8, we are seeing more club deals as private equity firms look to de-risk investments and reduce capital outlay by sharing even relatively modest equity cheques with other sponsors or large sovereign investment funds. Other approaches are likely to include:

Distressed Investing Expected to Rise in 2023

The quick rebound from the post-pandemic recession, fueled by fiscal stimulus and various forms of government support, curtailed expected distressed investing opportunities in 2020. 2023 looks more perilous. Today’s combination of rising interest rates, persistent inflation and the removal of COVID-19 financial support while banks are retreating from debt markets, are feeding expectations of a protracted downturn in Europe which will push more companies into distress. Fitch Ratings is forecasting a material increase in European high-yield bond defaults in 2023 and 2024 and has increased its base-case loan default rate to 4.5% for 2023, with a cumulative rate of 9.8% for 2022-249.

Dislocation in credit markets is creating other opportunities. In its October update, Oaktree estimated that U.S. banks held some $70bn of “hung” bridge loans and bonds stemming from recent M&A activity, with meaningful volume also present in Europe10. Reports of banks being forced to hold onto billions in debt for the buyout of Twitter adds to pressure in financing markets, leading to expectations that banks may be willing to sell some hung securities at discounts.

Firms have been raising capital for the forecast opportunities. In August, European mid-market special situations investor Zetland Capital raised over €620mn for its second fund – targeting U.S. as well as European investments – representing a roughly 66% increase in size on its first vehicle11.

Distressed Investing Expected to Rise in 2023

The quick rebound from the post-pandemic recession, fueled by fiscal stimulus and various forms of government support, curtailed expected distressed investing opportunities in 2020. 2023 looks more perilous. Today’s combination of rising interest rates, persistent inflation and the removal of COVID-19 financial support while banks are retreating from debt markets, are feeding expectations of a protracted downturn in Europe which will push more companies into distress. Fitch Ratings is forecasting a material increase in European high-yield bond defaults in 2023 and 2024 and has increased its base-case loan default rate to 4.5% for 2023, with a cumulative rate of 9.8% for 2022-249.

Dislocation in credit markets is creating other opportunities. In its October update, Oaktree estimated that U.S. banks held some $70bn of “hung” bridge loans and bonds stemming from recent M&A activity, with meaningful volume also present in Europe10. Reports of banks being forced to hold onto billions in debt for the buyout of Twitter adds to pressure in financing markets, leading to expectations that banks may be willing to sell some hung securities at discounts.

Firms have been raising capital for the forecast opportunities. In August, European mid-market special situations investor Zetland Capital raised over €620mn for its second fund – targeting U.S. as well as European investments – representing a roughly 66% increase in size on its first vehicle11.

Buy-And-Build Investments Increase

Deteriorating conditions for businesses and a fall in valuation levels are leading to an increase in bolt-on and buy-and-build transactions as private equity firms bet on it being a good time to scale up, increase efficiency and expand market share. Among recent deals, Brookfield’s UK infrastructure services company Modulaire Group bought Mobile Mini UK, a supplier of steel storage and accommodation units, to boost its portable storage business12.

Such deals are also happening to help expansion across borders. In Q4, U.S. component supplier Infinite Electronics, owned by Warburg Pincus, signed deals to acquire Netherlands-headquartered Cable Connectivity from Torqx Capital Partners and TKH Group and UK-headquartered Bulgin from Equistone, giving it well established brands and access to a wide range of end markets, including in Europe and China13. Bolt-on deals have the advantage of typically being smaller than primary or secondary buyouts, with new financing easier to raise as a result of that scale and lower leverage levels at platform companies following buy-and-build strategies. We see more bolt-on transactions working their way through the pipeline as firms pivot to deals that are easier to execute and enable them to keep deploying capital in volatile markets.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card