Private Equity

Market Snapshot

January 2023

Final data for 2022 revealed, as expected, a year that was significantly down on 2021 levels, but still one of the best for private equity investment on record. Global private equity backed buyouts decreased by 36% in 2022, according to Refinitiv data, but nonetheless totaled $785bn and accounted for a record 20% of M&A activity for the year1.

The final quarter saw a flurry of activity as firms aimed to complete investments and exits by the end of the year. Among them, French group Ardian agreed a $2.1bn partnership to invest in a portfolio of U.S. and European assets owned by Mubadala Capital, the asset management arm of the Abu Dhabi investment fund2. There were also sizeable exits, with Hg sealing the disposal of German cloud-based logistics services group Transporeon to U.S. listed software firm Trimble for €1.88bn3.

However, as we enter 2023 private equity is being pushed and pulled by contrasting forces.

Private Equity Investors Face Asset Allocation Dichotomy

Private equity firms have substantial reserves of dry powder to invest across Europe in the expectation that investments in dislocated markets can yield good long-term returns. Yet, the impact of rising interest rates and inflation, combined with a worsening economic outlook for businesses, is leading to some expectations that markets and companies have further to fall.

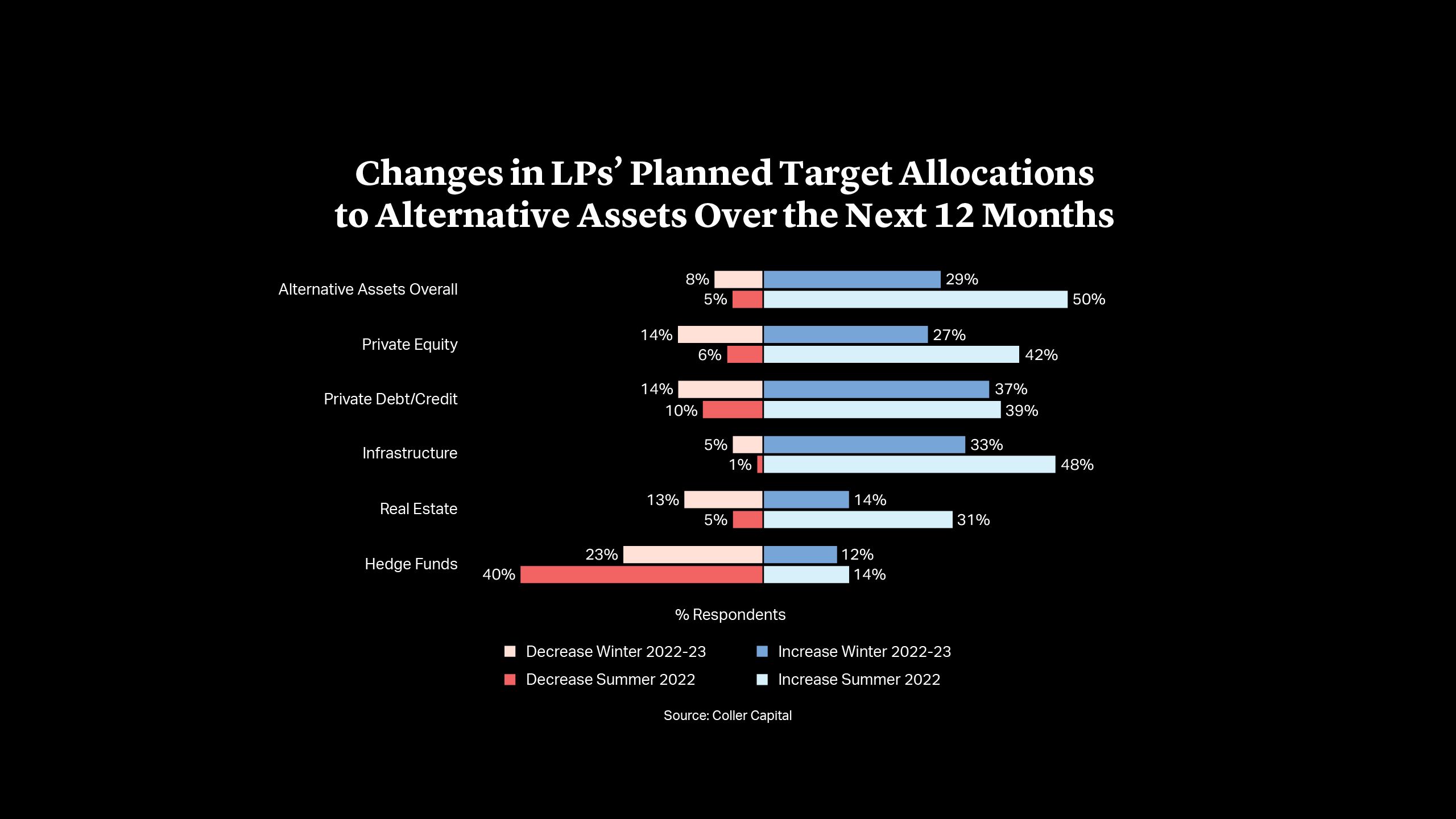

Those forces are evident in investors’ assessments and expectations for the asset class. A significant minority of LPs believe that the current market conditions have made private equity a more attractive proposition than public markets, according to Coller Capital’s Winter Barometer 2022-23. However, at the same time, the vast majority believe that macroeconomic conditions and inflation pose a significant risk to private equity returns over the next two to three years. As a result, the number planning to increase exposure to alternative assets has fallen to 29% from 50% in the middle of 20224.

Fundraising for Private Equity Slows

The liquidity and allocation pressures on investors are beginning to curtail commitments to private equity, with some of the largest and most-established fund managers noting challenges in raising funds. Carlyle is reported to have asked investors for more time as it continues to seek $22bn for its latest and largest buyout fund5. Others including Apollo have also said they will take longer to raise funds.

Not only are large flagship funds taking longer to raise, but the volume of capital flowing into private equity is contracting. Preqin estimated that fundraising will have contracted by over 20% when the 2022 results are tallied, with figures expected to remain below 2021 levels for 2023 as well6.

Next Level of Sustainability Regulation Comes Into Force

In addition to macro and capital raising challenges, private equity has higher regulatory requirements to meet in Europe. The second phase of the EU’s Sustainable Finance Disclosure Regulation (SFDR) came into force on 1 January 2023, bringing in mandatory sustainability reporting for financial market participants.

The regulatory technical standards (RTS) lay out in detail the standards that asset managers must meet and the templates they must use for ESG disclosures of their “light green” (Article 8) and “dark green” (Article 9) funds. Compared to the SFDR’s base requirements, these standards and templates revealed a number of additional issues for managers, such as committing upfront to a minimum percentage of sustainable investments and separately measuring allocations towards environmental or social factors.

In parallel to the approval of the RTS, the Commission released several sets of FAQs which added numerous additional rules to the mix “by way of interpretation”. The most widely discussed relates to the minimum “100% sustainable investments” hurdle that, in the Commission’s view, should apply to Article 9 funds – subject to limited exceptions. Following the release of this interpretation, several leading EU asset managers downgraded their funds from Article 9 funds to Article 8 in the run-up to January 2023, lamenting the lack of regulatory clarity.

Fund managers face further ESG disclosure standards and challenges from around the globe. Other jurisdictions – including the U.S., the UK and UAE – have announced plans to unroll their own ESG disclosure rules for funds from 2023. Fund managers that raise capital across these jurisdictions may now find themselves having to categorize their ‘green’ and impact funds under different – and sometimes competing – rules.

Next Level of Sustainability Regulation Comes Into Force

In addition to macro and capital raising challenges, private equity has higher regulatory requirements to meet in Europe. The second phase of the EU’s Sustainable Finance Disclosure Regulation (SFDR) came into force on 1 January 2023, bringing in mandatory sustainability reporting for financial market participants.

The regulatory technical standards (RTS) lay out in detail the standards that asset managers must meet and the templates they must use for ESG disclosures of their “light green” (Article 8) and “dark green” (Article 9) funds. Compared to the SFDR’s base requirements, these standards and templates revealed a number of additional issues for managers, such as committing upfront to a minimum percentage of sustainable investments and separately measuring allocations towards environmental or social factors.

In parallel to the approval of the RTS, the Commission released several sets of FAQs which added numerous additional rules to the mix “by way of interpretation”. The most widely discussed relates to the minimum “100% sustainable investments” hurdle that, in the Commission’s view, should apply to Article 9 funds – subject to limited exceptions. Following the release of this interpretation, several leading EU asset managers downgraded their funds from Article 9 funds to Article 8 in the run-up to January 2023, lamenting the lack of regulatory clarity.

Fund managers face further ESG disclosure standards and challenges from around the globe. Other jurisdictions – including the U.S., the UK and UAE – have announced plans to unroll their own ESG disclosure rules for funds from 2023. Fund managers that raise capital across these jurisdictions may now find themselves having to categorize their ‘green’ and impact funds under different – and sometimes competing – rules.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card