Private Equity Focuses on New Opportunities in Healthcare

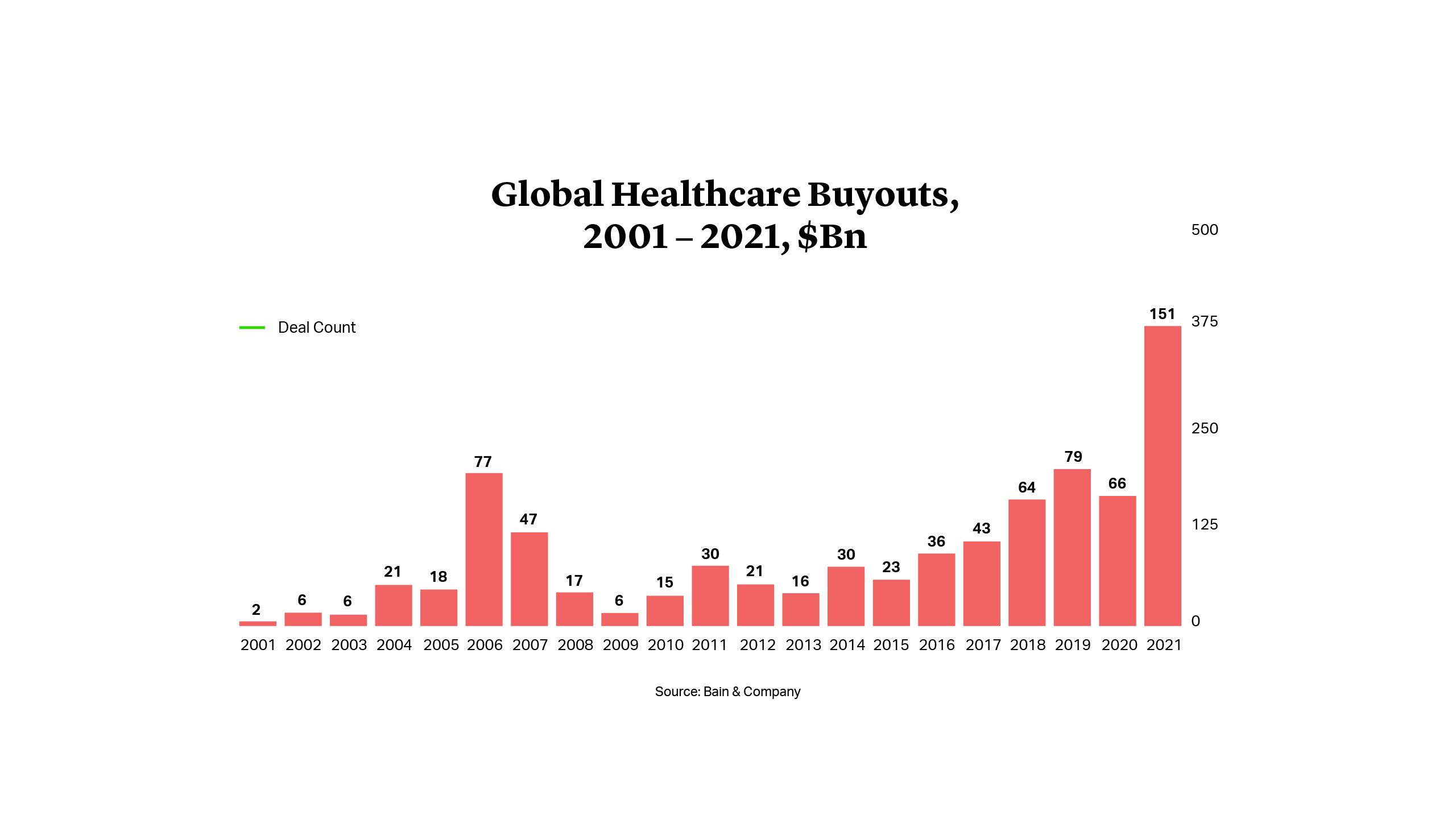

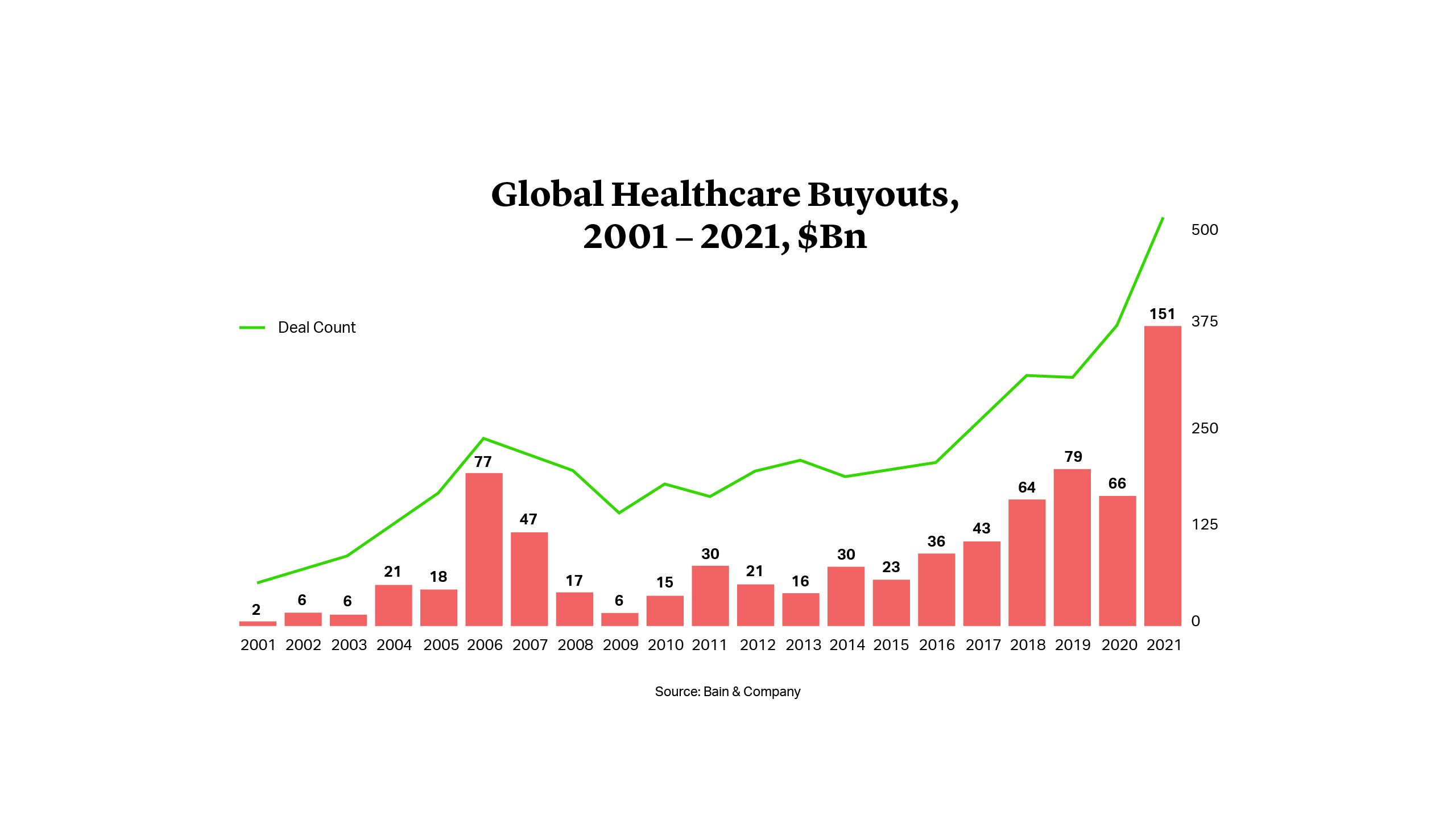

In the recovery from COVID-19, private equity investment in healthcare rebounded strongly as firms anticipated increased global focus and spending in the sector, as well as increased demand for procedures and treatments put off during the years of social distancing. According to Bain & Co data, global investment in the sector more than doubled from $66bn in 2020 to $151bn in 2021, while the number of deals increased by 36%1. In Europe, deal value surged by 86% to €24bn in 20212.

The big drivers of investment were megadeals, as private equity firms teamed up to buy U.S. groups Medline and Athenahealth, two of the largest buyouts of the year. Europe also hosted some of the largest deals in the sector, including the EQT-led buyout of Cerba HealthCare, valued at over $5bn.

Despite the contraction in large buyouts and the constraints on debt financing in 2022, the healthcare sector continued to deliver opportunities for private equity, including Triton’s £1.3bn take-private of UK pharmaceutical services business Clinigen Group. When final figures are tallied for 2022, Bain & Co expects capital deployment to be close to $100bn3 - a decline on 2021 levels but nonetheless the second-best year on record for healthcare investment. With the dealmaking environment remaining complicated in 2023, we see private equity firms exploring different avenues to access opportunities in what continues to be an attractive and resilient sector.

Pivot to Late-Stage Biotech Investment

High-profile success for companies including Germany’s BioNTech, one of the first to develop an approved vaccine against COVID-19, fueled a surge of investment into European biotech in 2021 as the sector attracted some $15bn4, according to BioWorld figures. While that investment cooled in 2022 amid the broader slowdown in venture capital for startups, the long-term opportunity has led some private equity firms to focus more effort and investment on Europe’s biotech and biopharma industry.

In 2022, Apollo acquired a minority stake in life sciences investment specialist Sofinnova, and The Carlyle Group bought control of Abingworth, giving them each an investment platform with deep expertise in the European life sciences space. They followed other large firms including Blackstone, which has already raised a dedicated global biotech fund.

To avoid risks associated with early-stage drug development, private equity often targets treatments that are in the later phases of clinical trials5. Blackstone’s €300mn investment alongside Sanofi in multiple myeloma drug Sarclisa last year enabled the pharma group to secure funding for costly development and testing in return for royalties from future sales of any marketed product6.

Activists Keep Up Pressure on European Healthcare Corporates

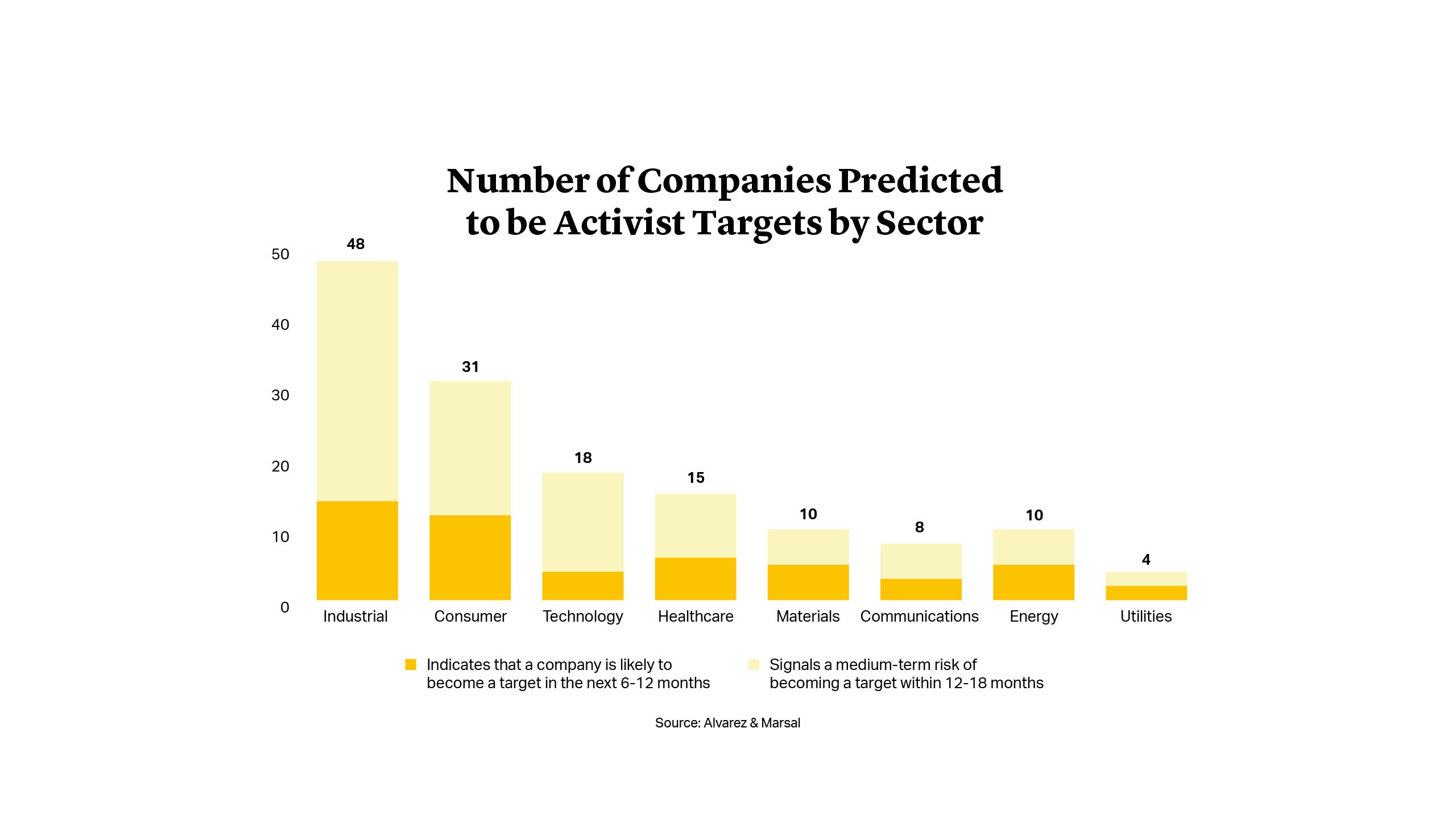

Pressure on corporates is expected to increase as Europe’s economic downturn continues. Advisory firm Alvarez & Marsal has identified a total of 144 companies at risk of activist attacks in the next 18 months7, which includes 15 in the healthcare sector. While that number represents a fall on previous levels, the industry remains under threat from weak returns on capital and cash generation8.

A number of companies, including Germany’s Fresenius and the UK’s GSK, have been the target of activist investors. Such agitation can often lead to disposals of underperforming or non-core units9. According to Bain & Co, the combined percentage of U.S. healthcare corporate carveouts and public-to-private transactions increased from 14% of all deals over $250mn in 2021 to 46% of such investments in the first three quarters of 202210, a trend being replicated in Europe.

Smaller companies can also use the strategic sale of business units to generate investment for their core businesses. In August, Dutch group Sanquin Health Solutions, which focuses on blood products and services, sold its reagents business – which had a turnover of roughly €25mn – to private equity group Gilde Healthcare11.

Long-Term Healthcare Returns Outperform

While the healthcare sector has not escaped market volatility, it has proved its ability to outperform for private equity investors over the long-term. Between 2010 and 2021, private equity healthcare investments delivered a median IRR of 27% compared with 21% for the broader private equity investment universe12.

That resilience was also evident in the exit market in 2022, with private equity firms able to secure sizeable exits to corporate buyers. In fact, there were 35 exits in excess of $500mn by the end of the third quarter, including Nordic Capital’s sale of British diagnostics company The Binding Site to U.S. group Thermo Fisher Scientific for about $2.6bn13.

We expect ongoing strong appetite in the European healthcare sector, combined with flexibility and creativity towards deal structuring, as sponsors look to gain exposure to companies that are developing healthcare solutions with long-term potential, including in the fields of gene therapy, diagnostics and specialist treatments (such as oncology, ophthalmology and dermatology), but also in primary care.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card