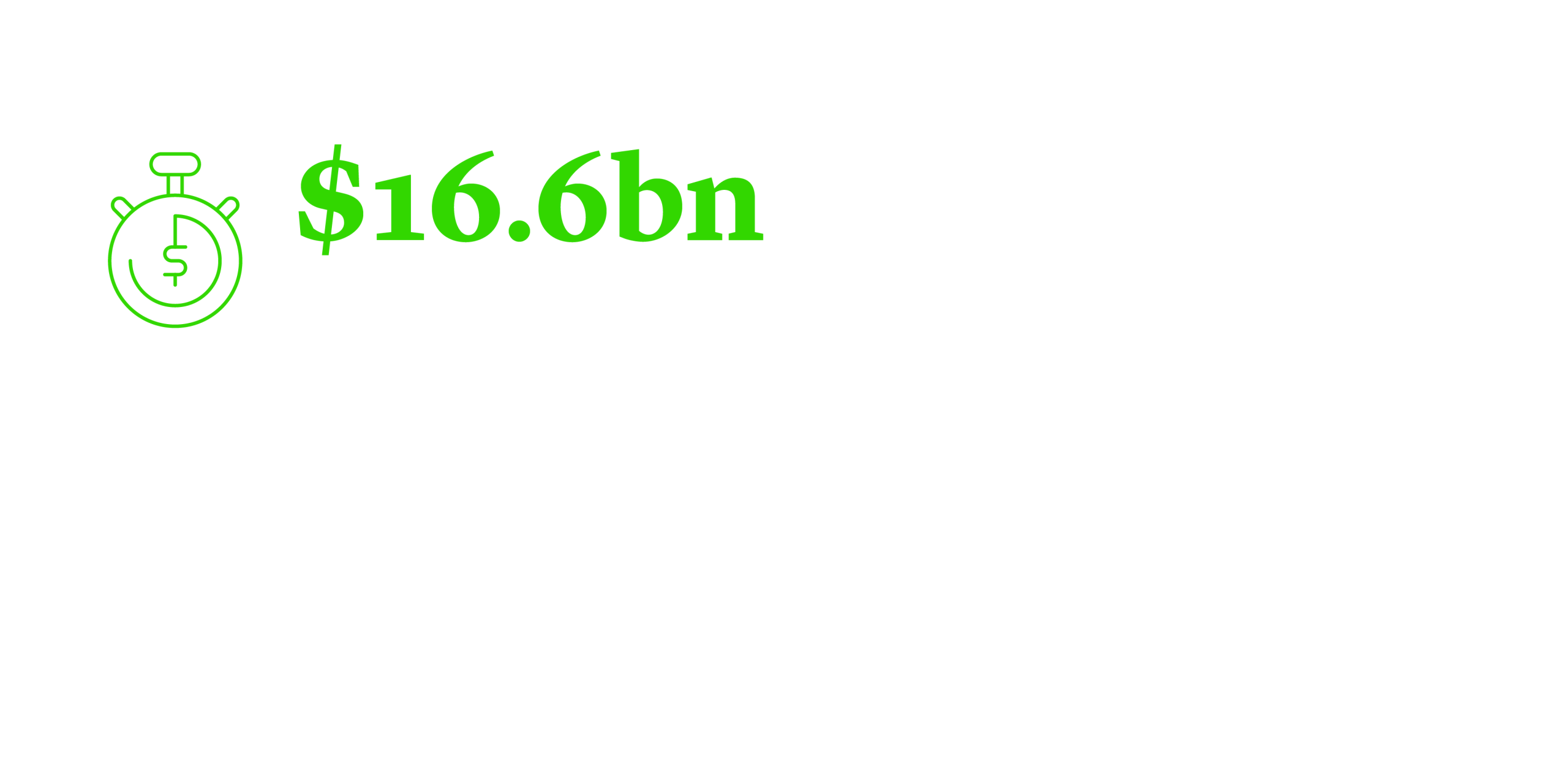

The last few years have seen an explosion in the issuing of green, social, and sustainability (GSS) bonds1 across Latin America. In 2019, the region attracted almost $6bn of investment in GSS bonds. This increased to just under $14bn by 2020 and, in the first four months of 2021 alone, Latin America has attracted $16.6bn of investment2.

Much of this new traction, in a region that has typically lagged behind much of the world on environmental, social and governance (ESG) initiatives, comes not from private sector issuers, but from sovereigns. The past two years have already seen ground-breaking activity by Chile and Mexico, and many more countries look to be waiting in the wings.

Governments across Latin America are struggling with financing needs intensified by the COVID-19 pandemic, at the same time that many also need significant energy and infrastructure funding and improvements on the ESG front. Given the continued demand for GSS bonds, sovereigns may be uniquely positioned to issue these instruments.

Latin America’s Green Bond Revolution

Chile became the first Latin American country to issue a GSS bond in 2019. By March 2021, Chile had issued approximately $7.7bn of GSS bonds, funding a broad range of projects from green buildings to public transport. Chile’s January 2021 issuance of $2.25bn in GSS bonds included the largest sustainability bond ever issued by a Latin American sovereign in foreign debt markets with the $1.5bn tranche.

In September 2020, Mexico became the first sovereign to issue bonds linked to the United Nations’ Sustainable Development Goals (SDGs). The eligible expenditures for this bond and for Mexico’s second SDG-linked bond issued in July 2021 are social projects aligned with selected target SDGs.

Colombia recently announced it had obtained senate approval to issue its inaugural sovereign GSS bonds, leading to speculation that the issuance could come later this year. Elsewhere, Peru, Costa Rica, and the Dominican Republic are all reportedly contemplating or preparing to issue GSS bonds in the near future.

GSS bonds are used to raised funds for specific projects, but corporates in Latin America have also started issuing sustainability-linked bonds, also referred to as key performance indicator (KPI) bonds.

Sustainability-linked bonds contain green or social targets that the issuer is seeking to achieve during the tenor of the bond. In the most common structure, if the target is not successfully hit, the issuer must pay a higher interest rate for the remaining life of the bond.

No sovereign, even outside of Latin America, has yet issued a sustainability-linked bond, but this financing structure provides another option for sovereigns looking to finance (or receive a financial benefit from) their environmental and social goals. For example, investors have been calling for a sustainability-linked bond from Brazil, with the KPI tied to protecting the Amazon rainforest.

Latin America’s Green Bond Revolution

Chile became the first Latin American country to issue a GSS bond in 2019. By March 2021, Chile had issued approximately $7.7bn of GSS bonds, funding a broad range of projects from green buildings to public transport. Chile’s January 2021 issuance of $2.25bn in GSS bonds included the largest sustainability bond ever issued by a Latin American sovereign in foreign debt markets with the $1.5bn tranche.

In September 2020, Mexico became the first sovereign to issue bonds linked to the United Nations’ Sustainable Development Goals (SDGs). The eligible expenditures for this bond and for Mexico’s second SDG-linked bond issued in July 2021 are social projects aligned with selected target SDGs.

Colombia recently announced it had obtained senate approval to issue its inaugural sovereign GSS bonds, leading to speculation that the issuance could come later this year. Elsewhere, Peru, Costa Rica, and the Dominican Republic are all reportedly contemplating or preparing to issue GSS bonds in the near future.

GSS bonds are used to raised funds for specific projects, but corporates in Latin America have also started issuing sustainability-linked bonds, also referred to as key performance indicator (KPI) bonds.

Sustainability-linked bonds contain green or social targets that the issuer is seeking to achieve during the tenor of the bond. In the most common structure, if the target is not successfully hit, the issuer must pay a higher interest rate for the remaining life of the bond.

No sovereign, even outside of Latin America, has yet issued a sustainability-linked bond, but this financing structure provides another option for sovereigns looking to finance (or receive a financial benefit from) their environmental and social goals. For example, investors have been calling for a sustainability-linked bond from Brazil, with the KPI tied to protecting the Amazon rainforest.

Green and Social Potential

There are many factors that make GSS bonds issued by Latin American sovereigns a highly attractive prospect to investors. With its wealth of biodiversity - which is coming under increasing threat - Latin America holds a huge pull, not only for green-minded investors, but also those who are interested in social improvements.

Many Latin American countries are in urgent need of widescale infrastructure overhaul, and the events of 2020 have predictably intensified this need. It is believed that 12 million more people will be left unemployed, and 30 million more people will be pushed into poverty in the region because of COVID-19 and its effects3.

In a recent UN publication, executive secretary Alicia Bárcena reported that of 72 statistical indicators describing how far Latin America is in meeting the SDGs, just four have been achieved, 15 are 'on the right track', 27 are stagnant, 21 need either 'more' or 'strong' government intervention, and five are in decline4.

A separate study estimates the public investment gap in Latin America, if current trends are followed, is expected to be 4.4% of GDP by 2030 - the year the UN would like to see SDG targets met. If measured strictly against the SDGs, this public investment gap could be as much as 12.4% of the region's GDP by 2030 - or $1.4tn5.

Funding SDG-related projects with GSS bonds rather than typical bond financings would lead to greater disclosure surrounding the projects and related goals, as well as ongoing reporting after issuance on the allocation of the proceeds to the projects.

With the right investment, it’s possible that Latin America’s combined water, wind, and solar capabilities mean it could become the first region to be entirely powered by renewable energy: Chile has the best solar conditions on Earth; Brazil’s electricity portfolio is one of the cleanest on Earth; and Chile and Costa Rica have committed to reaching net zero by 2050.

Last year, Latin America saw $16.4bn investment in renewable energy. In Brazil alone, green bond issuances by companies and the national development bank have raised $8bn since 2015. All of this carries huge promise for sovereign issuers entering the GSS bond market.

Facing Latin America’s Political Climate

One potential stumbling block for issuing sovereigns is the question of political instability. Fitch ratings ranks Latin America as having the second highest political risk after Sub-Saharan Africa. Though the situation varies widely from country to country, this could cause some investor hesitancy.

GSS bond issuers typically allocate the proceeds within a two-to-three-year window, so depending on the election cycle, there may not be a risk of political turnover and a shift in priorities. Requiring that the proceeds be ring-fenced for specific sustainability projects, if possible for the sovereign’s public finances, provides additional assurance. Even with these protections, certain projects could nonetheless be cancelled by a future administration.

Sustainability-linked bonds require an even longer time horizon, and the selected green or social targets are usually five, seven or even ten years after issuance. There is a real need to select targets that will be supported and pursued across administrations, and which can withstand political fluctuations.

On the other hand, the structure of a sustainability-linked bond may help mitigate concerns of long-term credibility and political fluctuations. In contrast to GSS bonds, sustainability-linked bonds provide for a financial consequence in the form of an interest rate increase, typically in the region of 25 basis points per year, if the issuer fails to meet its targets.

The benefit of both GSS bonds and sustainability-linked bonds is that there is some internal infrastructure created and a public commitment from the issuers with accompanying annual reporting, which could help to reduce the risk that a future administration will suddenly decide to reverse course.

A GSS Bubble?

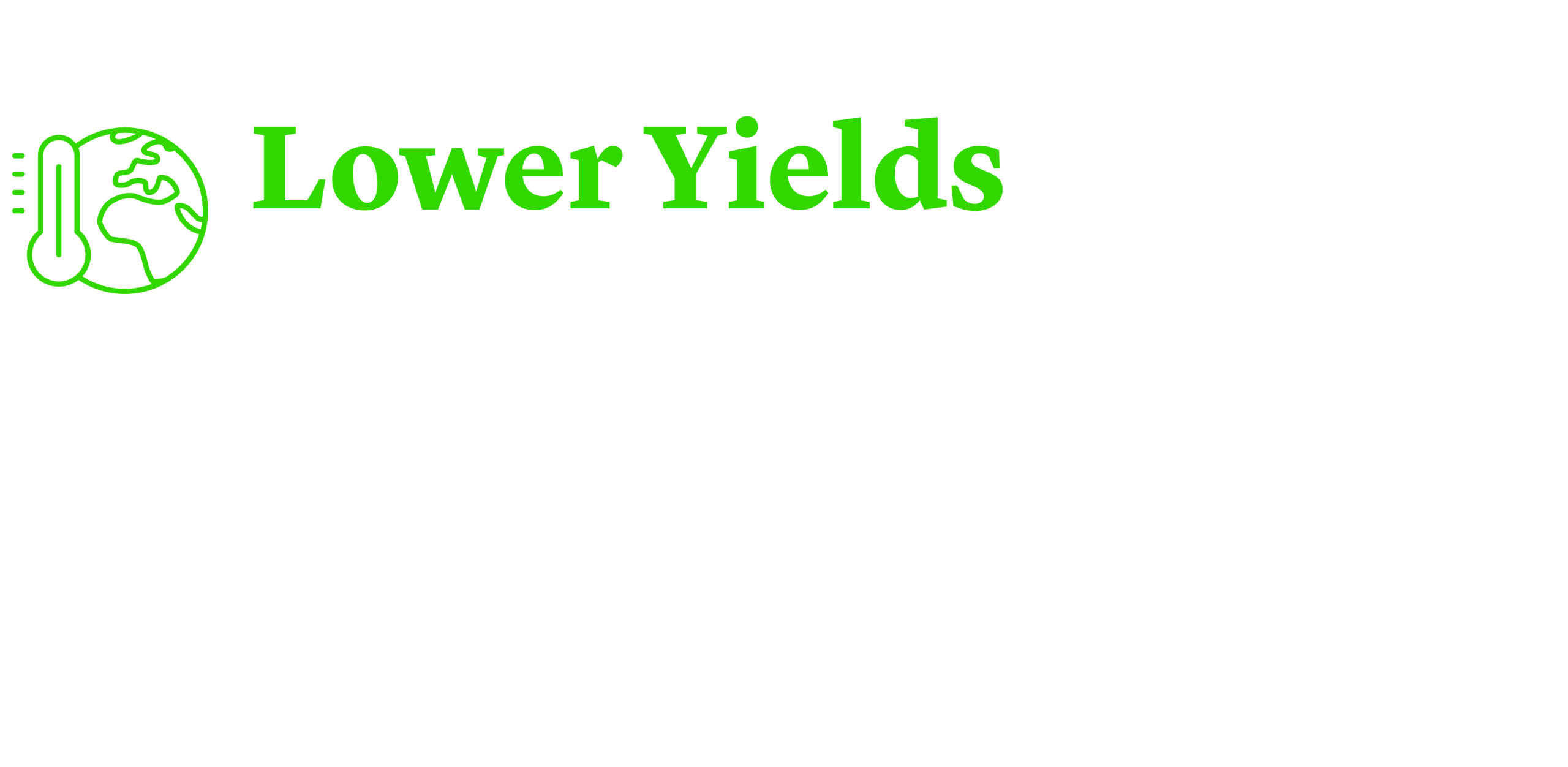

As GSS bonds sit at the top of a rapidly expanding global ESG debt market, there are growing signs that this high demand is resulting in lower borrowing costs for this type of debt. The Climate Bonds Initiative has found consistent signs of green bonds achieving lower yields than vanilla bonds.

In terms of sovereign debt, this so-called ‘greenium’ was highly visible in Germany’s inaugural green bond issuance, and, to a lesser extent, in Italy’s, which followed in March. This in itself could be seen as an incentive for Latin American sovereigns to start issuing GSS bonds (although, to date, it is unclear how far this ‘greenium’ extends beyond European debt markets).

Some analysts fear, however, that these bonds may be approaching ‘bubble’ territory, placing doubts over their future viability. Others contend that a ‘greenium’ simply reflects a market where demand far outpaces supply, and that pricing will settle down once a balance is found.

Given the future stake we all have in the green, social, and sustainability economy, it is difficult to imagine this type of debt will not hold up as a viable long-term investment.

Andrés de la Cruz

Partner

Buenos Aires

T: +54 11 5556 8901

New York

T: +1 212 225 2208

adelacruz@cgsh-arg.com

V-Card

Juan G. Giráldez

Partner

São Paulo

T: +55 11 2196 7202

jgiraldez@cgsh.com

V-Card

Jim Ho

Partner

London

T: +44 20 7614 2284

jho@cgsh.com

V-Card