As climate change injects greater uncertainty into financial markets, nature is increasingly being harnessed as part of the solution. In this article we present a few examples in which nature and finance intertwine. Given that we have already described ESG bonds and sustainability-linked bonds in prior pieces (see buttons below), this article will focus on Debt Conversion for Nature (DCFN) financing arrangements, which address sovereign debt relief while simultaneously protecting biodiversity. We will also look at Natural Disaster Clauses (NDC) and Catastrophe Bonds (CAT Bonds), which can offer climate resilience by providing greater certainty and faster relief following nature related events.

Debt Conversion for Nature

As the worsening global economic outlook increasingly pushes emerging market countries into situations where their debt burdens are economically unsustainable, climate and nature conservation policies are often the first place where funding is cut. Debt-for-nature swaps offer a solution to both problems by freeing fiscal space (or in some cases forgiving portions of a country’s debt) in exchange for commitments to invest in nature conservation.

While debt swaps are not new (Conservation International entered into an agreement with Bolivia in 1987 to retire a portion of the country’s debt in exchange for a promise to preserve four million acres of Amazonian tropical rain forest), the idea has generated renewed interest in recent years in light of the urgency of the climate crisis and the rise of ESG investment. An IMF working paper, released in August 20221, backed DCFN transactions as part of a broader debt restructuring program. The Green Climate Fund has expressed an interest in facilitating further DCFN transactions, and the African Development Bank is finalizing a feasibility study on scaling up debt-for-climate and nature swaps in Africa2. Cabo Verde, Eswatini and Kenya are among the African nations openly looking into such potential swaps3, and in South America, Ecuador, Argentina and Colombia have also all called for DCFNs.

Debt Conversion for Nature

As the worsening global economic outlook increasingly pushes emerging market countries into situations where their debt burdens are economically unsustainable, climate and nature conservation policies are often the first place where funding is cut. Debt-for-nature swaps offer a solution to both problems by freeing fiscal space (or in some cases forgiving portions of a country’s debt) in exchange for commitments to invest in nature conservation.

While debt swaps are not new (Conservation International entered into an agreement with Bolivia in 1987 to retire a portion of the country’s debt in exchange for a promise to preserve four million acres of Amazonian tropical rain forest), the idea has generated renewed interest in recent years in light of the urgency of the climate crisis and the rise of ESG investment. An IMF working paper, released in August 20221, backed DCFN transactions as part of a broader debt restructuring program. The Green Climate Fund has expressed an interest in facilitating further DCFN transactions, and the African Development Bank is finalizing a feasibility study on scaling up debt-for-climate and nature swaps in Africa2. Cabo Verde, Eswatini and Kenya are among the African nations openly looking into such potential swaps3, and in South America, Ecuador, Argentina and Colombia have also all called for DCFNs.

The Seychelles, 2018

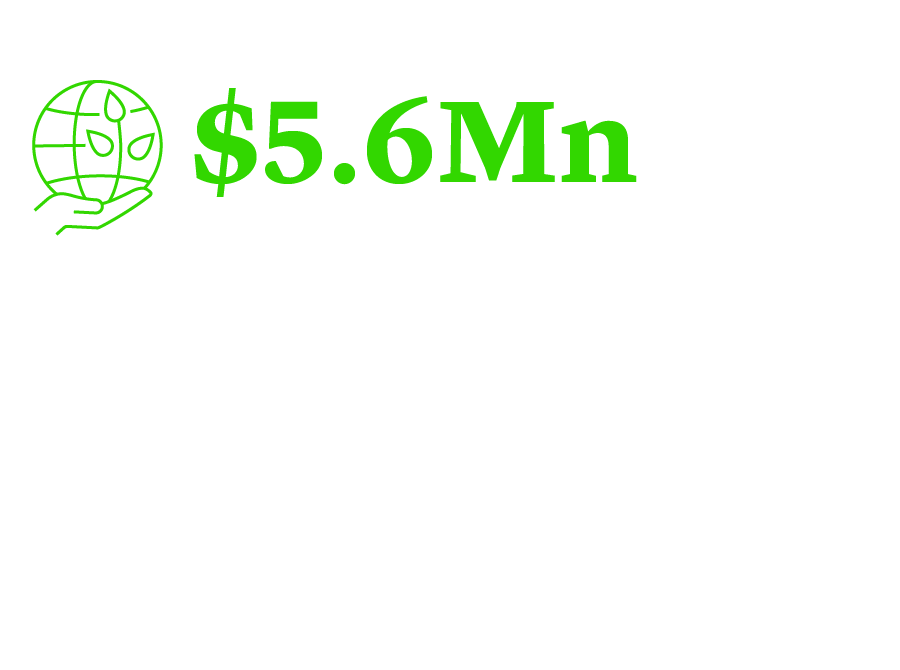

The Seychelles’ 2018 DCFN restructuring was a global first, both for the financial markets and biodiversity. It was the first debt conversion to focus on marine conservation and the first to contain a policy commitment. In return for $21.6mn debt forgiveness, facilitated by the UN and The Nature Conservancy, the Seychelles protected a third of its ocean territory – an area almost the size of Germany. The sovereign used private philanthropic funding, $15.2mn loan capital raised by TNC and $5mn in grants to buy back $21.6mn of its sovereign debt at a discount4. It is repaying these loans into a specially created local trust, the Seychelles Conservation and Climate Adaptation Trust (SeyCCAT), which will repay the $15.2mn loan capital over 10 years. Over a 20-year period, SeyCCAT will go as far as to provide $5.6mn of funding for marine conservation and climate adaptation activities and give $3mn to an endowment fund for further activities beyond this5. There are questions as to how replicable and scalable the Seychelles transaction would be, given that the transaction targeted the country’s Paris Club debt as opposed to commercial debt and the structure was reliant on donor funding in order to make the economics work.

Belize, 2021

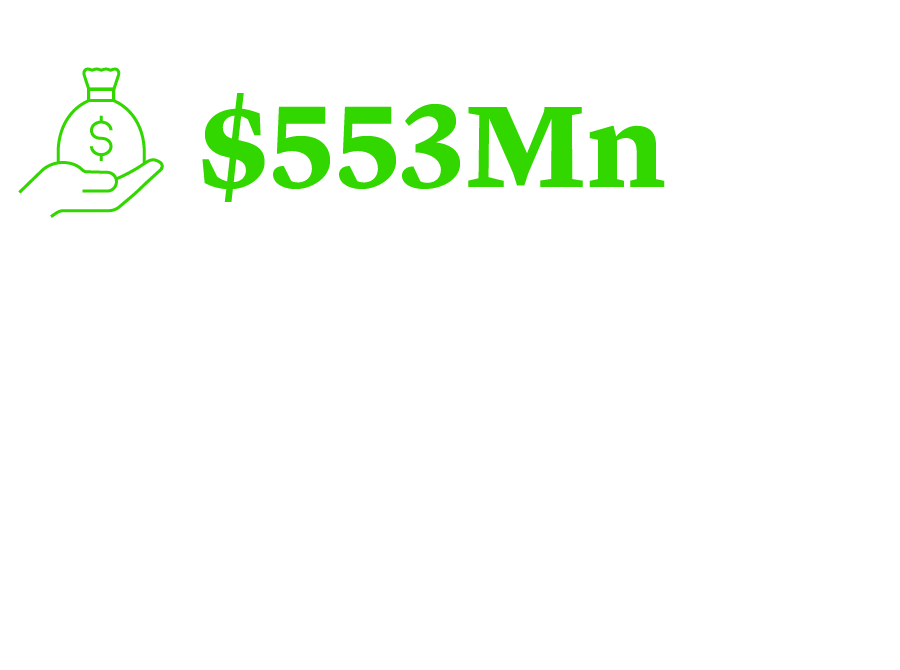

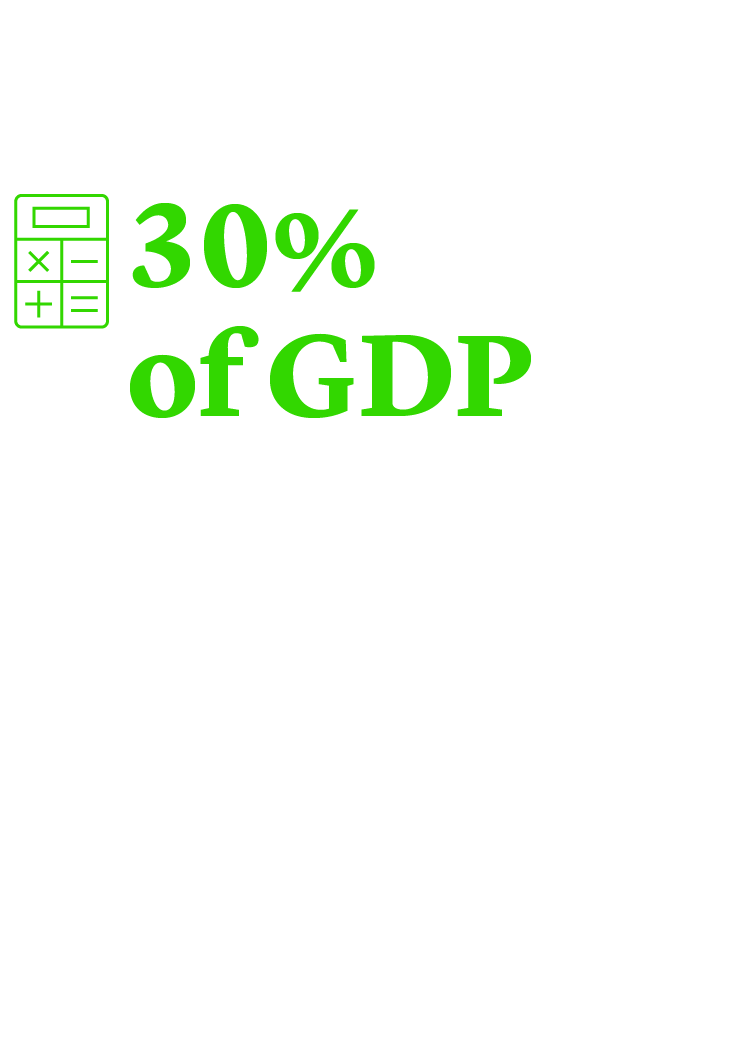

Belize’s 2021 agreement with The Nature Conservancy reduced the country’s GDP by 10%, through a $553mn “superbond”, representing the sovereign’s entire commercial debt stock (worth 30% of its GDP). Unlike the Seychelles, the Belize transaction targeted the country’s commercial debt.

This transaction was funded, in part, by a $364mn blue bond issuance arranged and underwritten by Credit Suisse. Political risk insurance from the U.S. International Development Finance Corporation (DFC) also contributed to a more attractive cost of financing. Belize, in return, agreed to spend $4mn annually on marine conservation until 2041, doubling its Biodiversity Protection Zones from 15.9% to 30% of its ocean territory. Using DFC insurance also secured a strong investment-grade credit rating for the blue bonds, giving investors the confidence to lend to a sovereign with a poor credit history, albeit in the context of a restructuring transaction.

Barbados, 2022

Most recently Barbados conducted an innovative DCFN transaction that will provide savings to support environmental and sustainable development objectives for the blue economy . Barbados entered into a $146.5mn-equivalent dual currency “blue” term loan, with guarantees provided by the Inter-American Development Bank and The Nature Conservancy of up to $100mn and $50mn respectively. In return, Barbados agreed to apply the proceeds of the blue loan in a concurrent buyback of a portion of Barbados’s existing Eurobonds and domestic bonds. The conversion of this outstanding debt stock is expected to generate savings of $50mn over the next 15 years 6.

Under the terms of certain conservation agreements entered into with The Nature Conservancy, Barbados will direct these savings into the Barbados Environmental Sustainability Fund (BESF), which will oversee and fund marine conservation and other environmental and sustainable development projects in Barbados, as well as into an endowment trust to fund long-term marine conservation efforts in Barbados. In addition to its commitment to fund the BESF and the endowment trust, Barbados committed to a number of conservation commitments and milestones, including the protection and management of up to 30% of Barbados’s Exclusive Economic Zone and Territorial Sea — an area of more than 55,000 square kilometers.

Unlike the Seychelles, the Barbados transaction targeted private debt. Unlike Belize, this transaction was done outside the context of a restructuring. This provides a blueprint for other sovereigns looking to utilize similar structures for new money or ordinary course (re)financing transactions. This could be especially attractive to governments with limited fiscal space who would like to free up funding for nature conservation and climate-related expenditure.

The Seychelles, 2018

The Seychelles’ 2018 DCFN restructuring was a global first, both for the financial markets and biodiversity. It was the first debt conversion to focus on marine conservation and the first to contain a policy commitment. In return for $21.6mn debt forgiveness, facilitated by the UN and The Nature Conservancy, the Seychelles protected a third of its ocean territory – an area almost the size of Germany. The sovereign used private philanthropic funding, $15.2mn loan capital raised by TNC and $5mn in grants to buy back $21.6mn of its sovereign debt at a discount4. It is repaying these loans into a specially created local trust, the Seychelles Conservation and Climate Adaptation Trust (SeyCCAT), which will repay the $15.2mn loan capital over 10 years. Over a 20-year period, SeyCCAT will go as far as to provide $5.6mn of funding for marine conservation and climate adaptation activities and give $3mn to an endowment fund for further activities beyond this5. There are questions as to how replicable and scalable the Seychelles transaction would be, given that the transaction targeted the country’s Paris Club debt as opposed to commercial debt and the structure was reliant on donor funding in order to make the economics work.

Belize, 2021

Belize’s 2021 agreement with The Nature Conservancy reduced the country’s GDP by 10%, through a $553mn “superbond”, representing the sovereign’s entire commercial debt stock (worth 30% of its GDP). Unlike the Seychelles, the Belize transaction targeted the country’s commercial debt.

This transaction was funded, in part, by a $364mn blue bond issuance arranged and underwritten by Credit Suisse. Political risk insurance from the U.S. International Development Finance Corporation (DFC) also contributed to a more attractive cost of financing. Belize, in return, agreed to spend $4mn annually on marine conservation until 2041, doubling its Biodiversity Protection Zones from 15.9% to 30% of its ocean territory. Using DFC insurance also secured a strong investment-grade credit rating for the blue bonds, giving investors the confidence to lend to a sovereign with a poor credit history, albeit in the context of a restructuring transaction.

Barbados, 2022

Most recently Barbados conducted an innovative DCFN transaction that will provide savings to support environmental and sustainable development objectives for the blue economy . Barbados entered into a $146.5mn-equivalent dual currency “blue” term loan, with guarantees provided by the Inter-American Development Bank and The Nature Conservancy of up to $100mn and $50mn respectively. In return, Barbados agreed to apply the proceeds of the blue loan in a concurrent buyback of a portion of Barbados’s existing Eurobonds and domestic bonds. The conversion of this outstanding debt stock is expected to generate savings of $50mn over the next 15 years 6.

Under the terms of certain conservation agreements entered into with The Nature Conservancy, Barbados will direct these savings into the Barbados Environmental Sustainability Fund (BESF), which will oversee and fund marine conservation and other environmental and sustainable development projects in Barbados, as well as into an endowment trust to fund long-term marine conservation efforts in Barbados. In addition to its commitment to fund the BESF and the endowment trust, Barbados committed to a number of conservation commitments and milestones, including the protection and management of up to 30% of Barbados’s Exclusive Economic Zone and Territorial Sea — an area of more than 55,000 square kilometers.

Unlike the Seychelles, the Barbados transaction targeted private debt. Unlike Belize, this transaction was done outside the context of a restructuring. This provides a blueprint for other sovereigns looking to utilize similar structures for new money or ordinary course (re)financing transactions. This could be especially attractive to governments with limited fiscal space who would like to free up funding for nature conservation and climate-related expenditure.

Natural Disaster Clauses

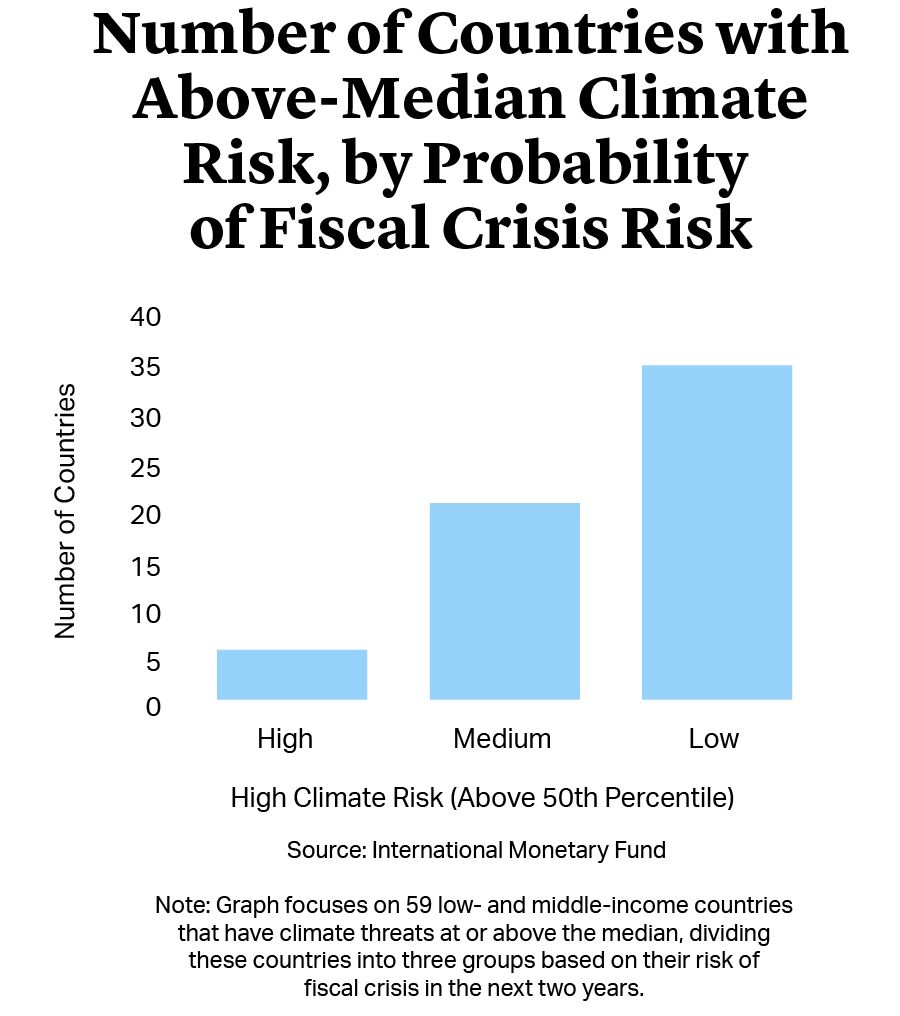

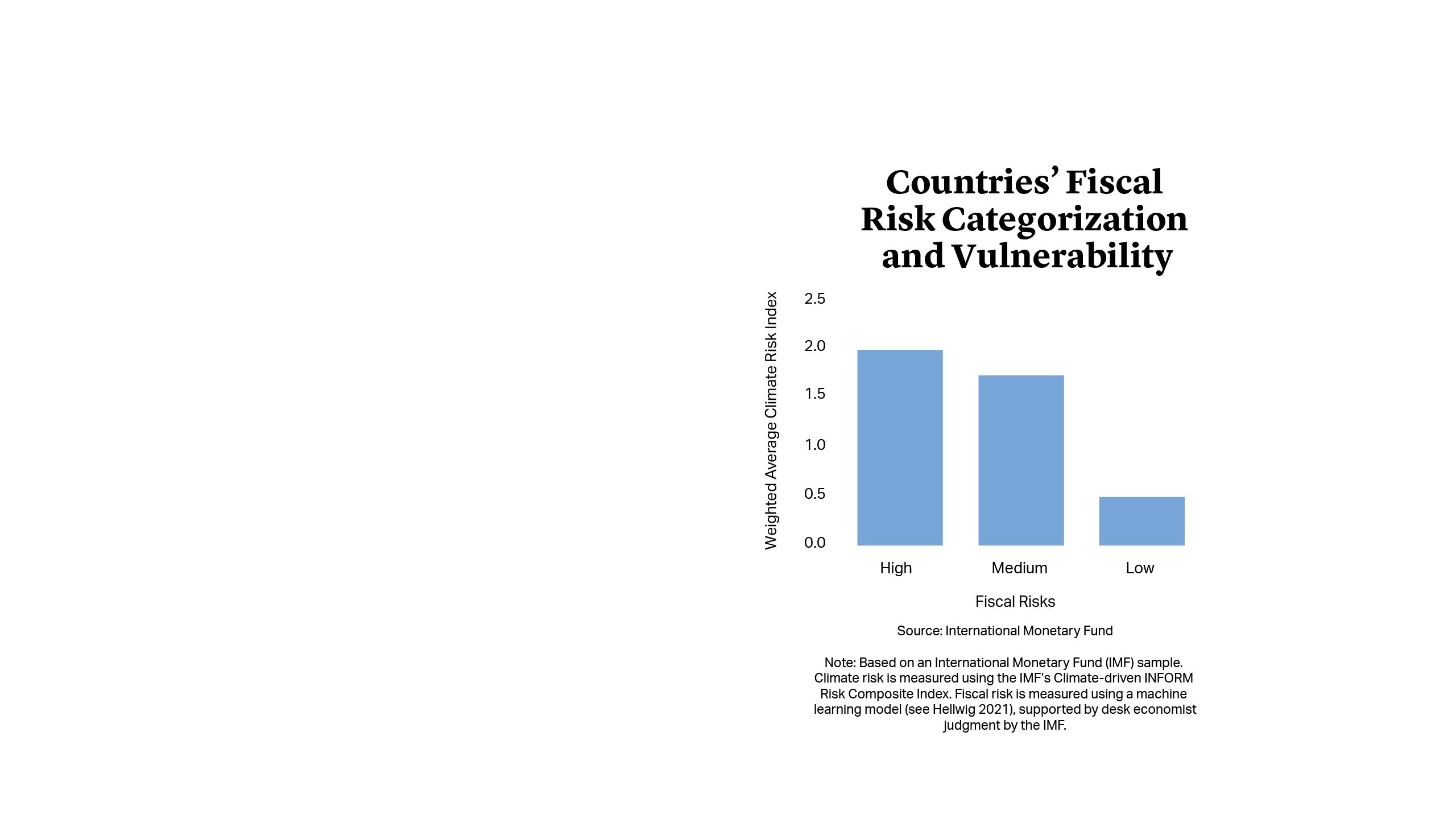

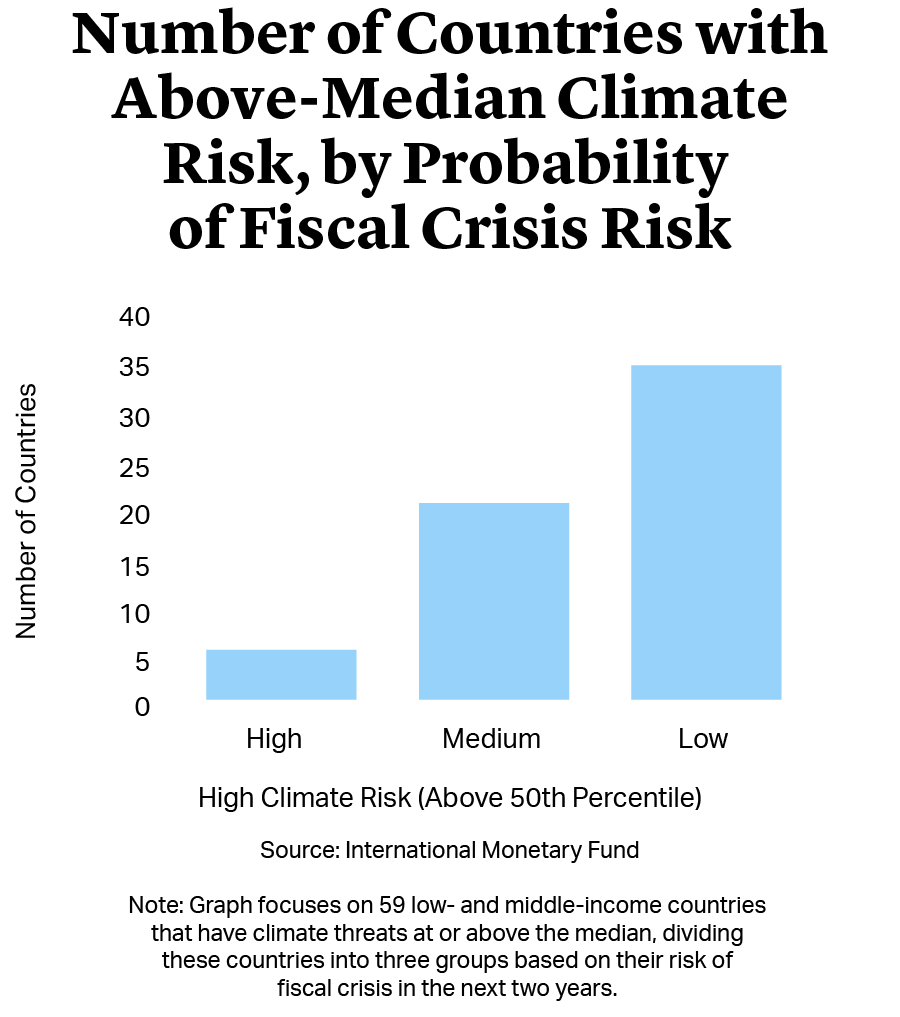

As climate change makes natural disasters more common, it is smaller island nations that are the most vulnerable. According to the IMF, one in 10 natural disasters that hit small countries causes damage equal to more than 30% of GDP7. The Natural Disaster Clause (NDC), or ‘Hurricane Clause’ enables a sovereign bond issuer to defer payments of both interest and principal sum, should a qualifying natural disaster occur. For a sovereign suddenly facing disaster, NDCs can provide immediate relief and certainty – placing far greater control into the sovereign’s hands. They also reduce the risks of natural disasters triggering a disorderly default or costly formal restructuring, precisely at a time when the sovereign needs to deal with the fallout of the natural disaster on its population and economy.

Natural Disaster Clauses

As climate change makes natural disasters more common, it is smaller island nations that are the most vulnerable. According to the IMF, one in 10 natural disasters that hit small countries causes damage equal to more than 30% of GDP7. The Natural Disaster Clause (NDC), or ‘Hurricane Clause’ enables a sovereign bond issuer to defer payments of both interest and principal sum, should a qualifying natural disaster occur. For a sovereign suddenly facing disaster, NDCs can provide immediate relief and certainty – placing far greater control into the sovereign’s hands. They also reduce the risks of natural disasters triggering a disorderly default or costly formal restructuring, precisely at a time when the sovereign needs to deal with the fallout of the natural disaster on its population and economy.

Grenada, 2015

Grenada incorporated the first NDC into a debt restructuring caused by a natural disaster. When Hurricane Ivan hit 10 years earlier, Grenada suffered total damage worth 200% of its GDP, setting it into a spiral of economic difficulty, which eventually made formal restructuring inevitable.

The clause allows Grenada to defer two years of principal and interest payments due in the event of a tropical cyclone causing $15mn to $30mn or more in losses.

Definitions of tropical storms and loss calculation are tied to the Caribbean Catastrophe Risk Insurance Facility (CCRIF) – a risk pool covering hurricanes, earthquakes, and excess rainfall in the Caribbean and Central America – creating greater certainty for all parties. If the CCRIF pays out more than $15mn, Grenada can defer payment. The country can trigger the NDC up to three times.

Barbados, 2018, 2019 and 2022

The NDC in the first of Barbados’s two-stage restructuring expanded trigger events to include earthquakes and excess rainfall, as well as tropical cyclones. It also lowered the loss threshold to a baseline of $5mn. Like Grenada, Barbados could elect to defer interest and principal payments for two years and is limited to deferring three times. We describe the evolution of the NDC from Grenada to Barbados in further detail in our previous piece:

The second restructuring stage in 2019 and 2020 made three further changes:

- the loss threshold was changed to $5mn for earthquakes and floods and $7.5mn for hurricanes;

- Barbados cannot make a deferral in the final two years before the final payment date, so the clause will not extend the bond’s final maturity;

- a new blocking clause enables holders of 50% of the principal amount to block the deferral within a 15-day notice period, which helps to assuage bondholders’ concerns regarding the potential abuse of the NDC.

In the event of a qualifying natural disaster (which results in the CCRIF insurance payout), these two NDCs could free as much as $700mn, or almost 15% of Barbados’s economy, across its debt stock for disaster relief. As a result, Barbados is now considered the only country in the world with a climate-resilient public debt stock.

In response to the COVID-19 pandemic and the recognition of the potential impact of future pandemics on government expenditures and revenues, Barbados’s 2022 DCFN transaction incorporated a new variant of the NDC which included a “pandemic event” as a qualifying trigger event. This is the first ever use of a “pandemic event” trigger in an NDC and adds an additional layer of pandemic-resilience to Barbados’s climate-resilient debt stock. Barbados’s 2022 DCFN transaction also saw the inclusion of the NDC (and the pandemic clause) for the first time in a new money transaction outside of a restructuring.

ICMA Model Clause, 2018

Like the Grenada and Barbados NDCs, the model clause allows the issuer to defer principal and interest payments, linking the qualifying event and damage value to CCIF insurance. Following Barbados’s model, it opens up the possibility of including earthquakes and excess rainfall events as triggers.

However, unlike Grenada and Barbados, it does not specify a loss threshold and the clause pushes all payments back by three years, instead of two. There is also no limit to the number of deferrals made – which is particularly good news for sovereigns prone to repeated natural disasters.

Catastrophe Bonds

Another way in which sovereigns are using capital markets to finance the impact of natural events are CAT Bonds. These financial instruments allow a sovereign exposed to hurricanes, earthquakes or other kinds of natural disasters to transfer a portion of the risk associated to such events to investors. Unlike NDCs, which provide breathing room for a sovereign hit by a natural disaster (or pandemic), CAT Bonds directly provide funds for the sovereign to recover from such disasters.

CAT Bonds originated in the private sphere to increase available capital to the natural-disaster-related insurance market following Hurricane Andrew striking Florida in 1992, which increased the demand for insurance beyond what the existing insurance companies could provide in the context of systemic natural catastrophes. Most recently, the World Bank included CAT Bonds as part of its Capital-at-Risk Notes program, providing sovereigns with a source of disaster-related insurance.

Catastrophe Bonds

Another way in which sovereigns are using capital markets to finance the impact of natural events are CAT Bonds. These financial instruments allow a sovereign exposed to hurricanes, earthquakes or other kinds of natural disasters to transfer a portion of the risk associated to such events to investors. Unlike NDCs, which provide breathing room for a sovereign hit by a natural disaster (or pandemic), CAT Bonds directly provide funds for the sovereign to recover from such disasters.

CAT Bonds originated in the private sphere to increase available capital to the natural-disaster-related insurance market following Hurricane Andrew striking Florida in 1992, which increased the demand for insurance beyond what the existing insurance companies could provide in the context of systemic natural catastrophes. Most recently, the World Bank included CAT Bonds as part of its Capital-at-Risk Notes program, providing sovereigns with a source of disaster-related insurance.

Under the auspices of the World Bank program, sovereigns commonly enter into an insurance agreement with the World Bank at the same time that the World Bank issues CAT Bonds in the market. Pursuant to such insurance agreement, the sovereign pays an insurance premium to protect itself from the realization of a predefined natural disaster. In turn, the World Bank issues the CAT Bonds into the market and invests the net proceeds safely. With the proceeds of such investment and the premium paid by the sovereign, the World Bank pays interest to bondholders and extracts its commission. The terms of CAT Bonds include clauses providing that if the qualifying natural disaster occurs during the life of the CAT Bond, bondholders forfeit their right to the payment of principal. Such clauses are paralleled in the insurance agreements providing that upon such events, the World Bank pays the sovereign.

CAT Bonds offer investors the possibility of tapping a market with risks that are uncorrelated with the returns of other financial market instruments. Given that the proceeds of the CAT Bonds are invested safely, counterparty risks are minimized – in addition to the fact that the counterparty is the World Bank and not the sovereign. Investors’ risk lies almost entirely in the realization of the pre-defined event.

Under the auspices of the World Bank program, sovereigns commonly enter into an insurance agreement with the World Bank at the same time that the World Bank issues CAT Bonds in the market. Pursuant to such insurance agreement, the sovereign pays an insurance premium to protect itself from the realization of a predefined natural disaster. In turn, the World Bank issues the CAT Bonds into the market and invests the net proceeds safely. With the proceeds of such investment and the premium paid by the sovereign, the World Bank pays interest to bondholders and extracts its commission. The terms of CAT Bonds include clauses providing that if the qualifying natural disaster occurs during the life of the CAT Bond, bondholders forfeit their right to the payment of principal. Such clauses are paralleled in the insurance agreements providing that upon such events, the World Bank pays the sovereign.

CAT Bonds offer investors the possibility of tapping a market with risks that are uncorrelated with the returns of other financial market instruments. Given that the proceeds of the CAT Bonds are invested safely, counterparty risks are minimized – in addition to the fact that the counterparty is the World Bank and not the sovereign. Investors’ risk lies almost entirely in the realization of the pre-defined event.

Conclusion

As the natural world injects escalating uncertainty into financial markets, sovereigns most affected by climate change and/or unsustainable debt will need to find further creative approaches to debt. The market is developing to provide more alternatives for sovereigns to take action to mitigate climate change and minimize the economic impact of nature related events. Countries have been increasingly taking advantages of these alternatives, a trend that we expect to continue.

Juan G. Giráldez

Partner

São Paulo

T: +55 11 2196 7202

jgiraldez@cgsh.com

V-Card

Jim Ho

Partner

London

T: +44 20 7614 2284

jho@cgsh.com

V-Card

Ignacio Lagos

Associate

New York

T: +1 212 225 2852

ilagos@cgsh.com

V-Card