Seven Things

to Know About

Private Credit Funds

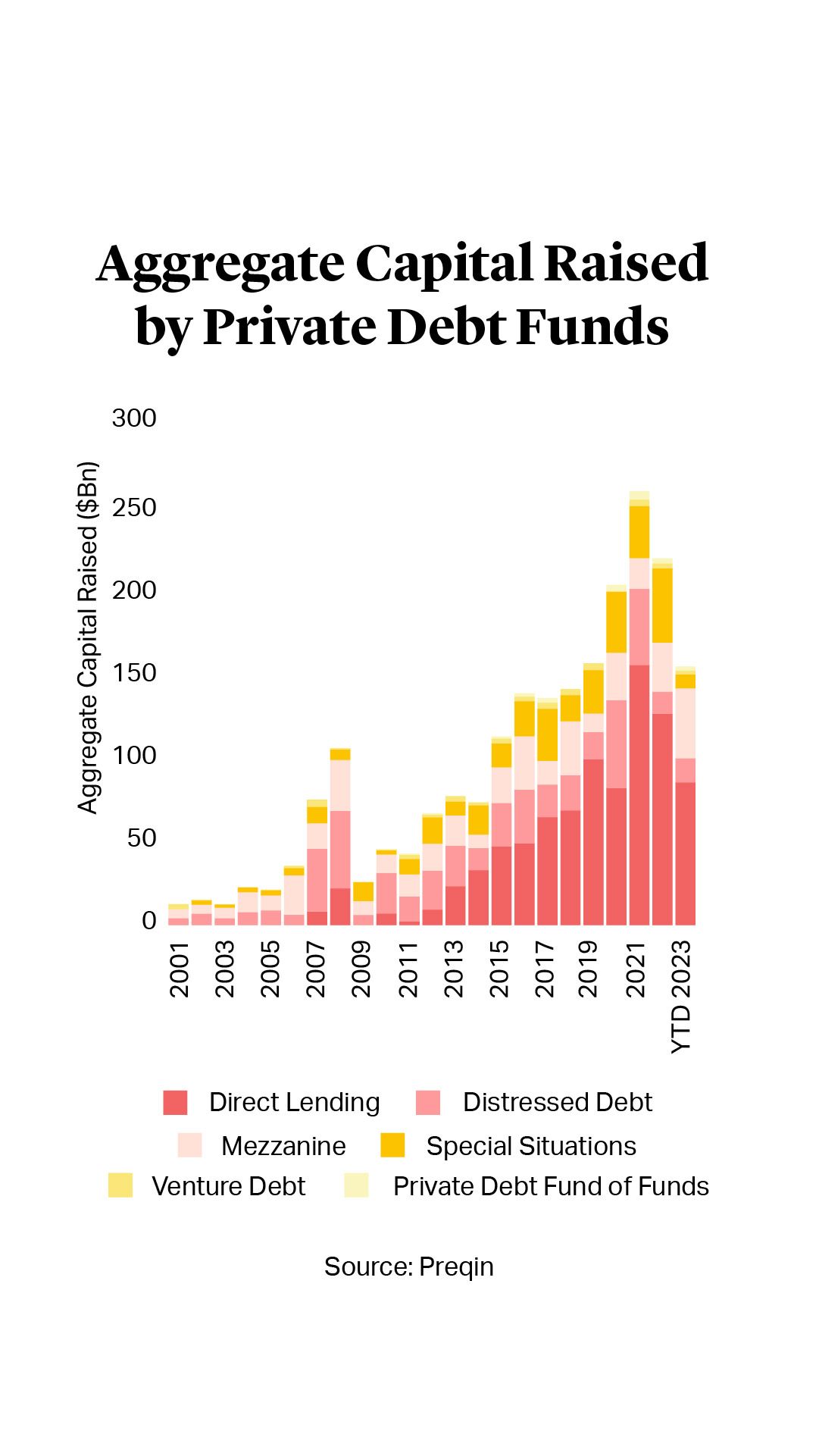

Private credit has been in growth mode since the 2008 global financial crisis. The industry has swelled from $280bn in assets under management (AUM) at that time to $1.5tn in 20221. Private credit has been further buoyed by the retreat of banks, which have tightened lending in recent years in the face of liquidity constraints, regulatory scrutiny, and higher cost structures.

Despite being subject to the same investor overallocation issues that have hampered other corners of the alternatives world, private credit has shown resiliency, raising over $200bn in an exceptionally challenging fundraising market last year2. Growth of the asset class appears well positioned to persist in 2024, with a recent study finding that just under 90% of investors plan to invest the same or more capital in the space over the next 12 months, while just over 90% said the asset class had met or exceeded performance benchmarks3.

Private credit has been in growth mode since the 2008 global financial crisis. The industry has swelled from $280bn in assets under management (AUM) at that time to $1.5tn in 20221. Private credit has been further buoyed by the retreat of banks, which have tightened lending in recent years in the face of liquidity constraints, regulatory scrutiny, and higher cost structures.

Despite being subject to the same investor overallocation issues that have hampered other corners of the alternatives world, private credit has shown resiliency, raising over $200bn in an exceptionally challenging fundraising market last year2. Growth of the asset class appears well positioned to persist in 2024, with a recent study finding that just under 90% of investors plan to invest the same or more capital in the space over the next 12 months, while just over 90% said the asset class had met or exceeded performance benchmarks3.

Investment advisers (GPs) looking to launch their first private credit product and investors looking to increase their private credit exposure should keep in mind the following features that distinguish these funds from private equity.

Attractive Across Market Cycles

The private credit universe is broad and increasingly diverse, including strategies that seek to capitalize on volatility and high interest rates. Private credit investments are typically floating rate investments, so when interest rates rise, the coupon on a private credit investment also rises, increasing the return profile for the fund.

Direct lending and mezzanine funds have surged in popularity due to traditional lending constraints and higher interest rates, and the trend of credit funds serving as a funding alternative to traditional banking is expected to continue in the foreseeable future. Opportunistic credit plays, designed to take advantage of market dislocation, are also seeing enhanced LP interest.

Private credit products have also shown resiliency compared to public debt markets. The historical default rate of private credit assets is approximately 2%, with recovery rates of between 60% and 70% for senior loans. This compares to default rates of close to 3.6% in the high-yield bond market, where recovery rates are around 45%4.

Attractive Across Market Cycles

The private credit universe is broad and increasingly diverse, including strategies that seek to capitalize on volatility and high interest rates. Private credit investments are typically floating rate investments, so when interest rates rise, the coupon on a private credit investment also rises, increasing the return profile for the fund.

Direct lending and mezzanine funds have surged in popularity due to traditional lending constraints and higher interest rates, and the trend of credit funds serving as a funding alternative to traditional banking is expected to continue in the foreseeable future. Opportunistic credit plays, designed to take advantage of market dislocation, are also seeing enhanced LP interest.

Private credit products have also shown resiliency compared to public debt markets. The historical default rate of private credit assets is approximately 2%, with recovery rates of between 60% and 70% for senior loans. This compares to default rates of close to 3.6% in the high-yield bond market, where recovery rates are around 45%4.

Operational Issues

GPs and LPs should be aware of some fundamental operational differences between traditional closed-end private credit funds and their equity counterparts, which arise as a result of the nature of the underlying investments. Given that a credit fund may have a greater number of investments and that credit investments may be more time sensitive than private equity, credit funds typically have greater flexibility to call capital without immediate deployment and without the capital being tied to a particular investment.

Similarly, it can be more operationally difficult to provide opt-out rights on a deal-by-deal basis in a credit fund. As a result, credit funds are more likely to hardwire opt-out rights to enable the fund to take advantage of investment opportunities on a shorter timeline.

Operational Issues

GPs and LPs should be aware of some fundamental operational differences between traditional closed-end private credit funds and their equity counterparts, which arise as a result of the nature of the underlying investments. Given that a credit fund may have a greater number of investments and that credit investments may be more time sensitive than private equity, credit funds typically have greater flexibility to call capital without immediate deployment and without the capital being tied to a particular investment.

Similarly, it can be more operationally difficult to provide opt-out rights on a deal-by-deal basis in a credit fund. As a result, credit funds are more likely to hardwire opt-out rights to enable the fund to take advantage of investment opportunities on a shorter timeline.

Recycling Terms

The nature of credit investments also has an impact on recycling provisions. Credit investments tend to have a shorter holding period, and therefore generate returns faster, than typical private equity investments. While some private credit funds have recycling provisions that mirror those of traditional buyout funds – for example, imposing a maximum percentage of committed capital that can be recycled, as well as a time limit that only permits recycling during the investment period and other more limiting restrictions – many credit funds have the ability to recycle amounts constituting both a return of capital and profits and to do so beyond the investment period.

Waterfall Inventions

As credit investments are typically more liquid than private equity investments, credit funds are more likely to have a European waterfall. Some credit funds targeting assets that regularly generate cash income, such as direct lending, are adopting a separate current income waterfall, similar to many business development companies.

There is, however, an increasing trend of more illiquid credit strategies, like special situations funds, utilizing an American waterfall structure, more like a typical buyout fund.

Waterfall Inventions

As credit investments are typically more liquid than private equity investments, credit funds are more likely to have a European waterfall. Some credit funds targeting assets that regularly generate cash income, such as direct lending, are adopting a separate current income waterfall, similar to many business development companies.

There is, however, an increasing trend of more illiquid credit strategies, like special situations funds, utilizing an American waterfall structure, more like a typical buyout fund.

Borrowing Provisions

Private credit funds are more likely than private equity to employ actual leverage in an attempt to maximize returns. As a result, private credit funds are less likely to have time limits on borrowing, as is common in private equity funds, and to have higher limits on borrowing amounts. There is also a trend towards credit funds offering both levered and unlevered sleeves to provide optionality for LPs seeking different risk/return profiles.

Investing in Different Tiers of the Capital Stack

Given the proliferation and specialization of the credit investing space, credit fund GPs are increasingly likely to have multiple fund products seeking to invest in different tiers of the capital stack of the same issuer, such as senior debt, subordinated debt, mezzanine debt, etc. Credit fund GPs need the flexibility to engage in such transactions, and as a result, investment allocation, investment restriction, and conflicted transaction provisions for credit funds are likely to be drafted to accommodate investments by multiple of the GP’s funds in the same issuer.

These dynamics pose unique conflicts of interest and heighten the need for fulsome conflicts disclosure, particularly to the extent that conflicted transactions do not require the approval of the fund’s limited partner advisory committee. They can also complicate any GP-led secondaries transactions with respect to credit fund assets. Please refer to our article on credit secondaries in the Summer 2023 edition of the Cleary Gottlieb Private Funds Bulletin for further analysis of those issues5.

Investing in Different Tiers of the Capital Stack

Given the proliferation and specialization of the credit investing space, credit fund GPs are increasingly likely to have multiple fund products seeking to invest in different tiers of the capital stack of the same issuer, such as senior debt, subordinated debt, mezzanine debt, etc. Credit fund GPs need the flexibility to engage in such transactions, and as a result, investment allocation, investment restriction, and conflicted transaction provisions for credit funds are likely to be drafted to accommodate investments by multiple of the GP’s funds in the same issuer.

These dynamics pose unique conflicts of interest and heighten the need for fulsome conflicts disclosure, particularly to the extent that conflicted transactions do not require the approval of the fund’s limited partner advisory committee. They can also complicate any GP-led secondaries transactions with respect to credit fund assets. Please refer to our article on credit secondaries in the Summer 2023 edition of the Cleary Gottlieb Private Funds Bulletin for further analysis of those issues5.

Flexible Structuring

LPs are now able to access private credit strategies through a greater variety of structures. Although illiquid credit strategies are likely to utilize a traditional closed-end structure, more liquid strategies are increasingly employing open-ended or hybrid structures. While some LPs may prefer the familiar closed-end structure, others may like the flexibility offered by open-end and hybrid structures.

In such hybrid and open-end structures, an LP can remain continuously exposed to a strategy for a longer period of time, and the periodic liquidity rights of such structures give an LP greater ease in managing its portfolio allocation. For the GP, these structures can provide a more permanent source of capital, while also providing efficiencies from a borrowing and operations perspective.

The enhanced liquidity can also make an open-end or hybrid credit fund more attractive to an increasingly important pool of capital – retail investors. For additional information on open-end and hybrid funds, please see our article on evergreen fund structures in the Winter 2022/2023 edition of the Cleary Gottlieb Private Funds Bulletin6.

Flexible Structuring

LPs are now able to access private credit strategies through a greater variety of structures. Although illiquid credit strategies are likely to utilize a traditional closed-end structure, more liquid strategies are increasingly employing open-ended or hybrid structures. While some LPs may prefer the familiar closed-end structure, others may like the flexibility offered by open-end and hybrid structures.

In such hybrid and open-end structures, an LP can remain continuously exposed to a strategy for a longer period of time, and the periodic liquidity rights of such structures give an LP greater ease in managing its portfolio allocation. For the GP, these structures can provide a more permanent source of capital, while also providing efficiencies from a borrowing and operations perspective.

The enhanced liquidity can also make an open-end or hybrid credit fund more attractive to an increasingly important pool of capital – retail investors. For additional information on open-end and hybrid funds, please see our article on evergreen fund structures in the Winter 2022/2023 edition of the Cleary Gottlieb Private Funds Bulletin6.

A Flourishing Future

As a floating-rate product, private credit has been one of the most resilient asset classes through this period of higher interest rates. Although commonly viewed as presenting a lower risk/return profile than a typical private equity fund, private credit returns exceeded private equity returns in both the second and third quarters of 20237.

As a result, appetite for private credit remains strong. A recent study found that LPs are more likely to increase their allocation to private credit than any other area of alternatives – with 44% saying they were likely to increase their allocation to private credit over the next year8.

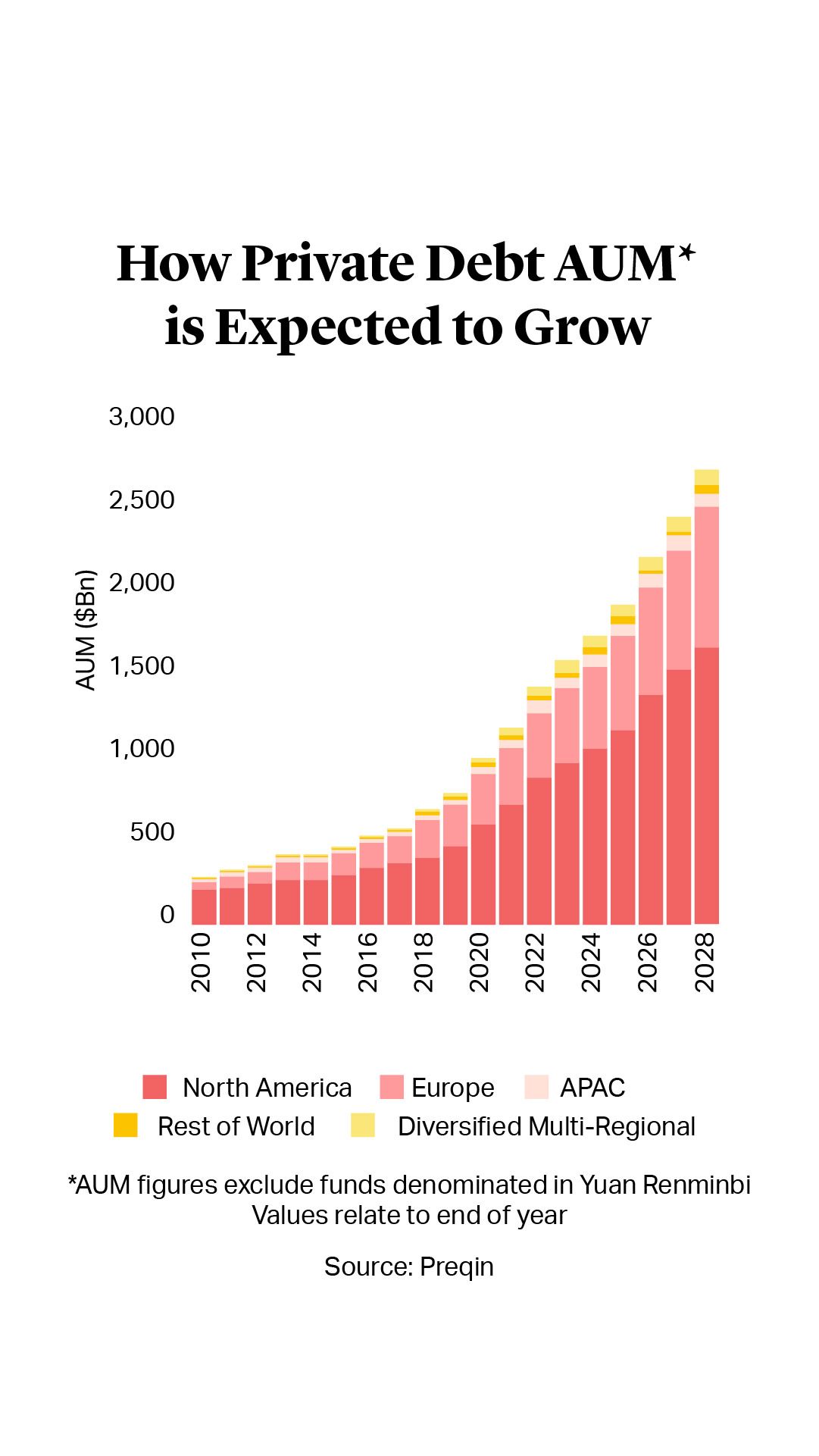

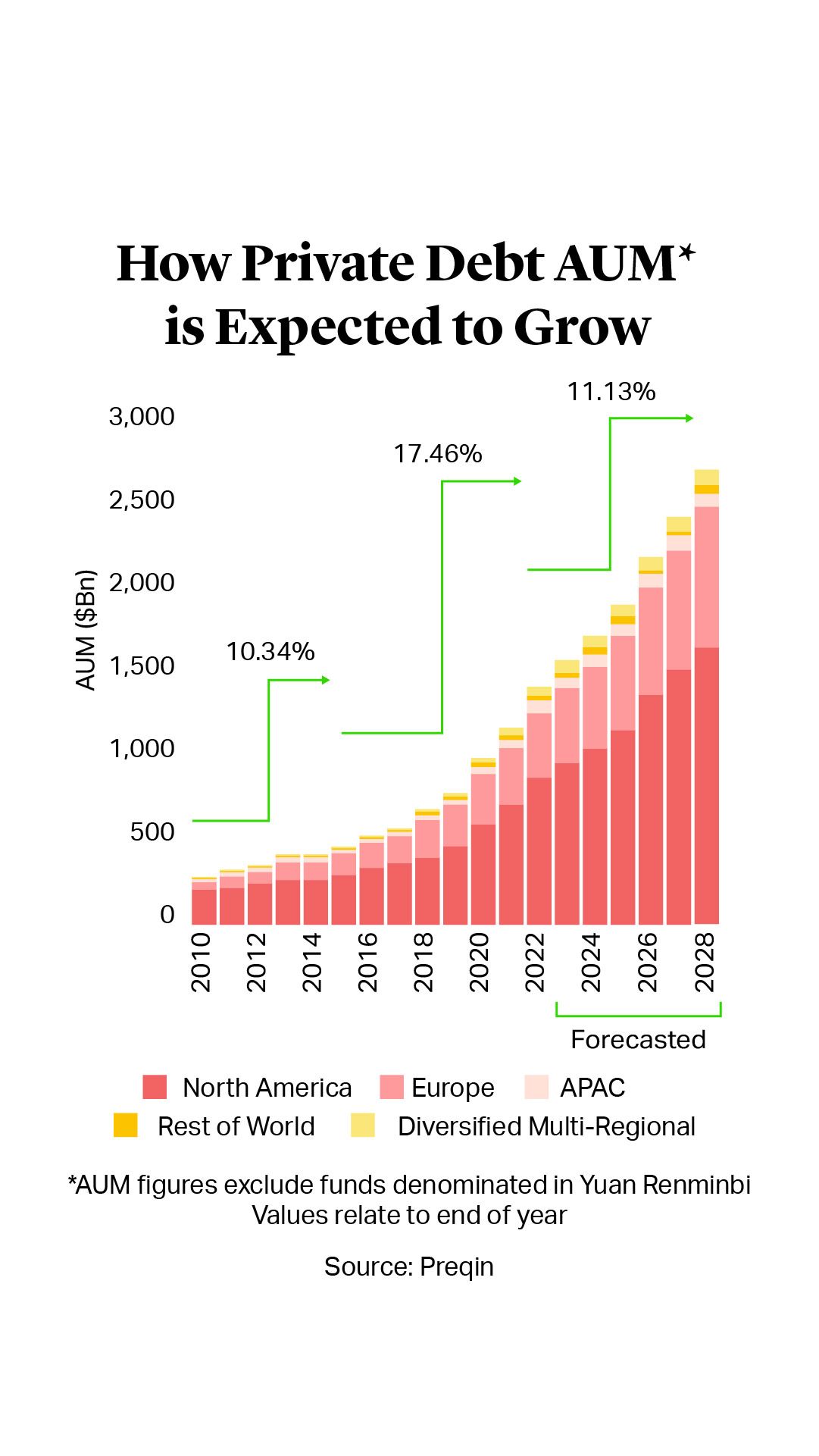

The private credit market is projected to almost double in size to $2.8tn by the end of 2028, based on investor sentiment9. With the potential for such a promising future, private credit is positioned to be a key player in the evolving alternatives landscape.

A Flourishing Future

As a floating-rate product, private credit has been one of the most resilient asset classes through this period of higher interest rates. Although commonly viewed as presenting a lower risk/return profile than a typical private equity fund, private credit returns exceeded private equity returns in both the second and third quarters of 20237.

As a result, appetite for private credit remains strong. A recent study found that LPs are more likely to increase their allocation to private credit than any other area of alternatives – with 44% saying they were likely to increase their allocation to private credit over the next year8.

The private credit market is projected to almost double in size to $2.8tn by the end of 2028, based on investor sentiment9. With the potential for such a promising future, private credit is positioned to be a key player in the evolving alternatives landscape.