GPs and LPs Lean

Into Co-Investment

Although global private equity deal volume has declined in recent years1, demand for LP co-investment opportunities is booming. And a challenging fundraising environment, coupled with increased cost of debt, means GPs are relying on LP support more than ever to get deals done.

LPs continue to seek out co-investment opportunities in large part because of their preferential economics. Co-investments also give LPs greater control over their deployment pace and their exposure to particular GPs, geographies, and sectors. According to a recent survey, 67% of LPs plan to participate in private equity co-investment opportunities in the next 12 months2.

Many GPs are also happy to offer co-investment for a variety of reasons. They are continuing to leverage co-investment opportunities in connection with LP investments in new funds, as fundraising continues to be constrained by LP allocation issues. Co-investments can also help right-size equity checks, enabling the GP to make an investment without running into concentration and other investment restriction problems – an issue that may be particularly relevant for smaller funds. GPs are also increasingly turning to co-investment as a result of the current borrowing environment. Higher interest rates and pullback by traditional lenders has resulted in many recent private equity deals with a higher equity-to-debt ratio than they may have had previously.

Below we provide a summary of some of the trends we are seeing in the co-investment space.

Co-investments can help right-size equity checks, enabling the GP to make an investment without running into concentration and other investment restriction problems

Co-investments can help right-size equity checks, enabling the GP to make an investment without running into concentration and other investment restriction problems

Single-Investor Vehicles

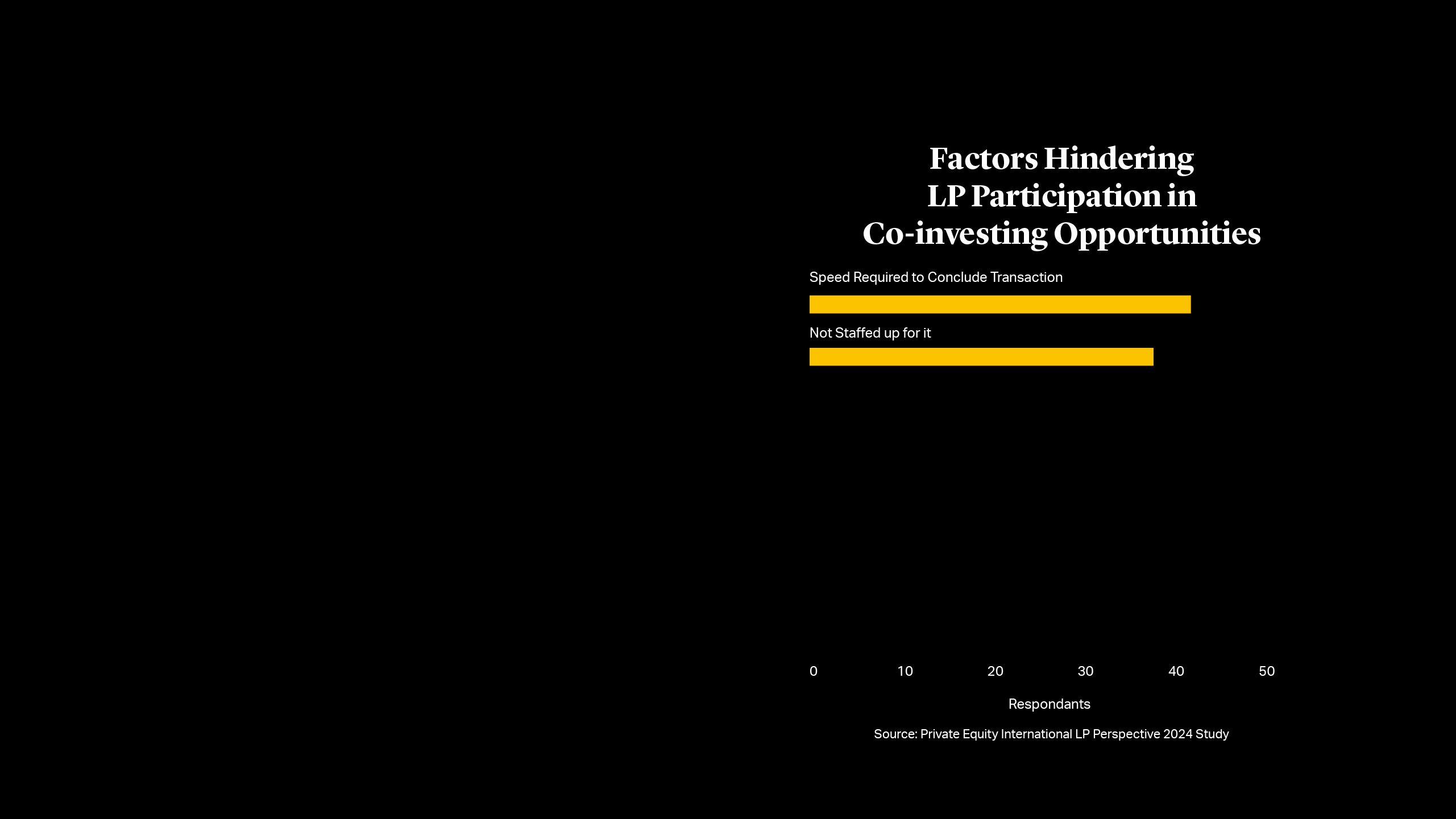

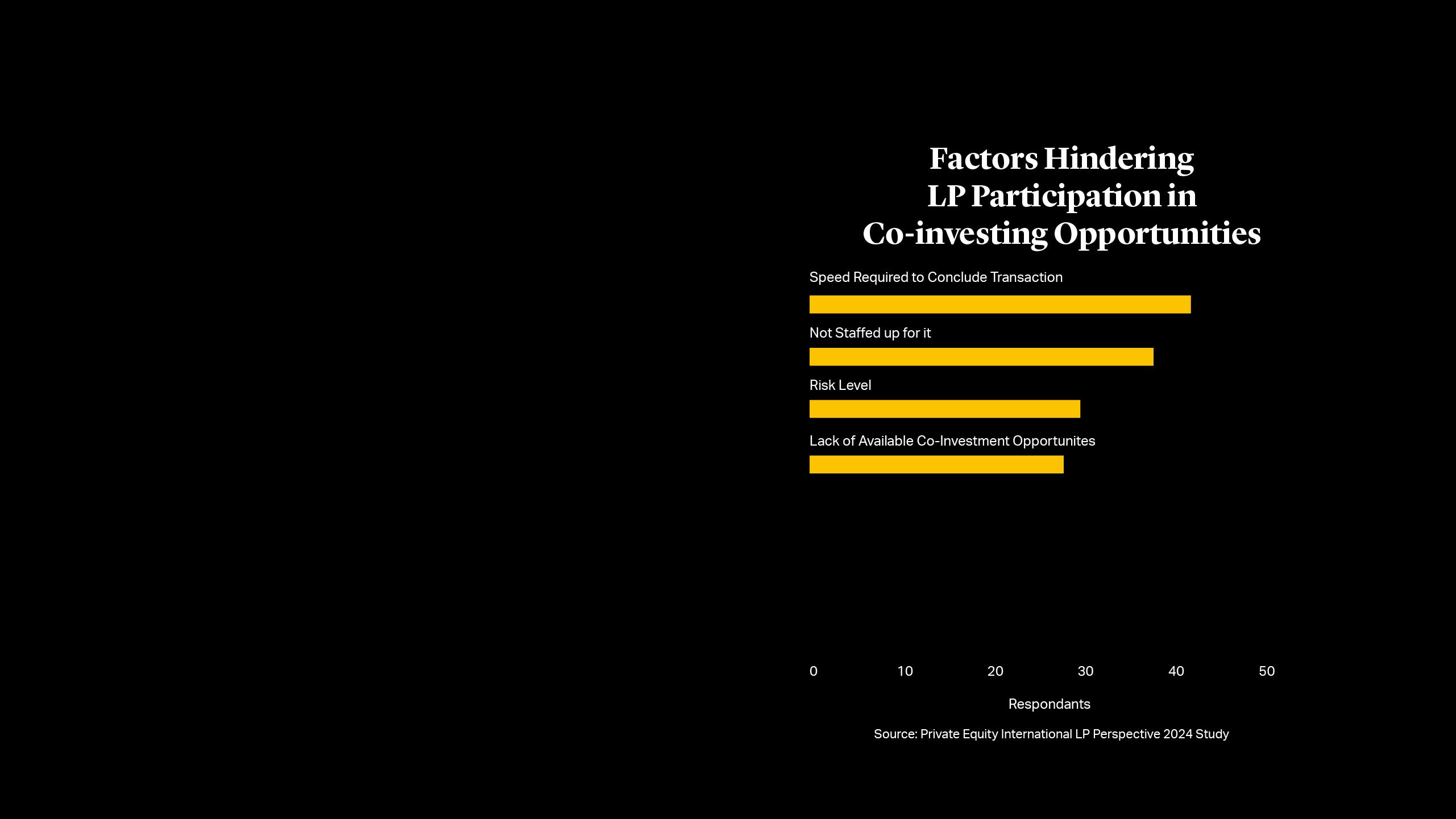

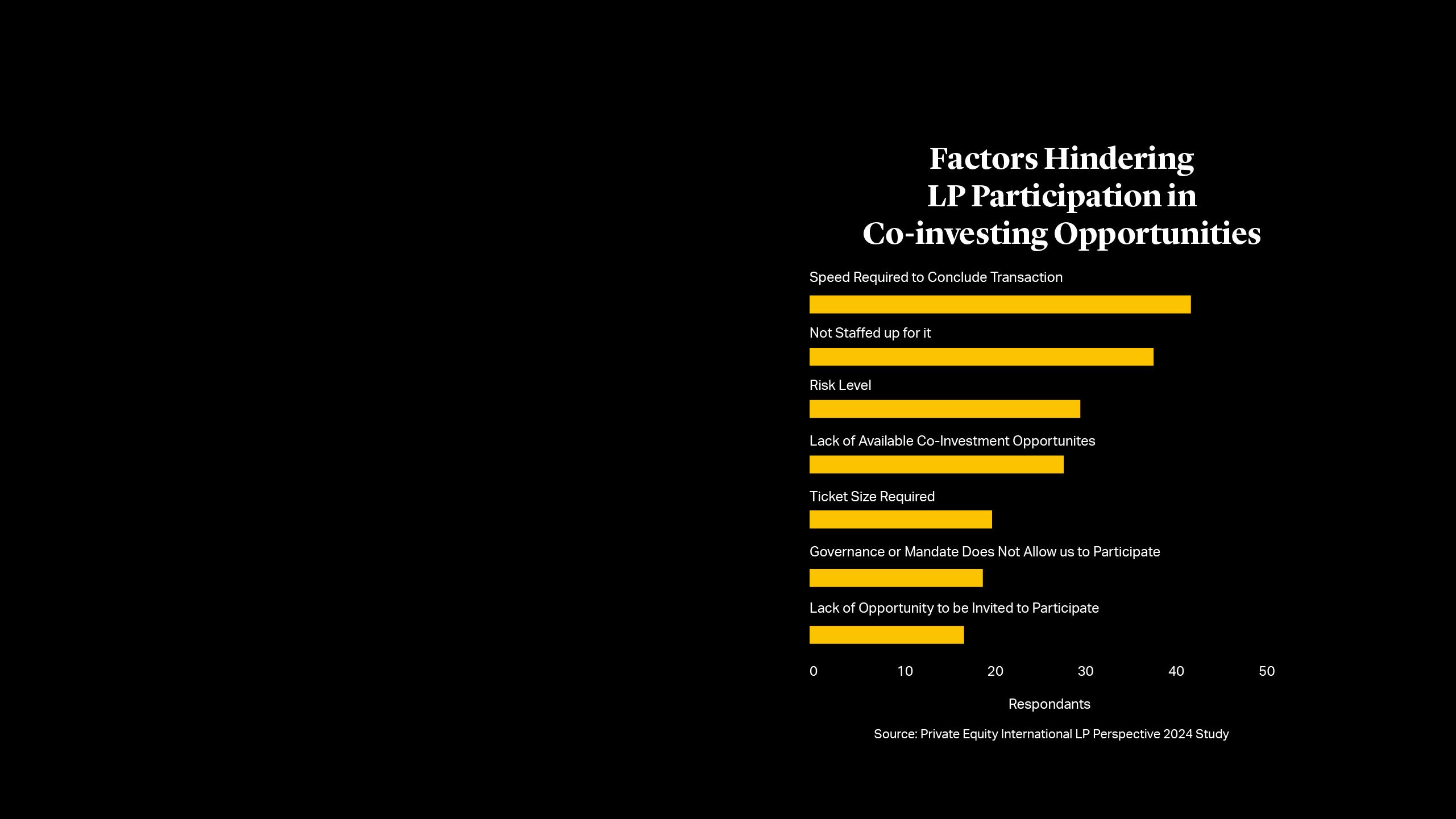

Despite significant LP appetite for co-investment, execution continues to be a challenge for many. According to a recent study, the speed required to evaluate transactions and a lack of internal staffing were the two factors most likely to hinder LP participation in co-investment3.

As a result, we are increasingly seeing GPs and LPs taking a programmatic approach to co-investing. With such an approach, an LP can outline its investment capacity and preferred parameters at the outset, including particular strategies and types of deals it would like to participate in, thereby alleviating the pressure to make rapid decisions. These arrangements are commonly facilitated by the use of a standing, single investor co-investment vehicle that can be used for multiple deals with a quick action “opt-in” or “opt-out” mechanic for LPs to utilize when presented with a deal. The negotiation of these co-investment arrangements typically dovetails with fundraising conversations and are viewed by many GPs as a way to strengthen LP relationships, with establishment of programmatic co-investment vehicles increasingly being offered concurrently with the main fund.

Single-Investor Vehicles

Despite significant LP appetite for co-investment, execution continues to be a challenge for many. According to a recent study, the speed required to evaluate transactions and a lack of internal staffing were the two factors most likely to hinder LP participation in co-investment3.

As a result, we are increasingly seeing GPs and LPs taking a programmatic approach to co-investing. With such an approach, an LP can outline its investment capacity and preferred parameters at the outset, including particular strategies and types of deals it would like to participate in, thereby alleviating the pressure to make rapid decisions. These arrangements are commonly facilitated by the use of a standing, single investor co-investment vehicle that can be used for multiple deals with a quick action “opt-in” or “opt-out” mechanic for LPs to utilize when presented with a deal. The negotiation of these co-investment arrangements typically dovetails with fundraising conversations and are viewed by many GPs as a way to strengthen LP relationships, with establishment of programmatic co-investment vehicles increasingly being offered concurrently with the main fund.

Co-Investments in Follow Ons

In addition to seeking co-investment to support new deals, GPs are also turning to co-investors for follow-on capital. Co-investments may be used to provide additional equity to support the continued expansion of a high-growth company, for example, or to facilitate a transformative acquisition.

Alignment around valuation and duration needs to be carefully considered in these situations, as do existing fund LPAC and other LPA provisions. But as long as the dynamics of the transaction are fully understood and LPA terms are complied with, these situations can be advantageous for both existing and co-investing LPs.

Co-Investments in Follow Ons

In addition to seeking co-investment to support new deals, GPs are also turning to co-investors for follow-on capital. Co-investments may be used to provide additional equity to support the continued expansion of a high-growth company, for example, or to facilitate a transformative acquisition.

Alignment around valuation and duration needs to be carefully considered in these situations, as do existing fund LPAC and other LPA provisions. But as long as the dynamics of the transaction are fully understood and LPA terms are complied with, these situations can be advantageous for both existing and co-investing LPs.

Increased Co-Investor Engagement

Although co-investors have traditionally taken a passive role with respect to co-investments, similar to their role in a typical fund, we are seeing an uptick in LPs that are seeking to become more actively involved in the co-investments in which they participate. This is often motivated in part by an LP’s desire to develop or enhance their internal direct investing capabilities. LPs in some instances have requested terms such as enhanced transparency, board observer seats and input on investment decisions.

In our experience, GPs are typically thoughtful when LPs request these rights, balancing LP desires with the broader investment dynamics, and often must politely decline these rights based on deal dynamics. Control and governance rights may pose a variety of deal issues, including ensuring the GP feels adequately in control of the main fund’s investment, sensitivity with counterparties, and regulatory considerations. For example, these rights could trigger issues under U.S. and non-U.S. foreign direct investment regimes, depending on the scope of the rights and the particular LP.

Increased Co-Investor Engagement

Although co-investors have traditionally taken a passive role with respect to co-investments, similar to their role in a typical fund, we are seeing an uptick in LPs that are seeking to become more actively involved in the co-investments in which they participate. This is often motivated in part by an LP’s desire to develop or enhance their internal direct investing capabilities. LPs in some instances have requested terms such as enhanced transparency, board observer seats and input on investment decisions.

In our experience, GPs are typically thoughtful when LPs request these rights, balancing LP desires with the broader investment dynamics, and often must politely decline these rights based on deal dynamics. Control and governance rights may pose a variety of deal issues, including ensuring the GP feels adequately in control of the main fund’s investment, sensitivity with counterparties, and regulatory considerations. For example, these rights could trigger issues under U.S. and non-U.S. foreign direct investment regimes, depending on the scope of the rights and the particular LP.

Economics & Monetization

Co-investment terms have remained relatively stable and consistent in recent years. As in private funds generally, we have seen an increase in LP requests for enhanced transparency and reporting with respect to co-investments, particularly in the ESG/impact space.

Monetizing co-investments, whether through a management fee, administrative fee, placement fee, or carried interest arrangement is a perennial topic of conversation among GPs. While some LPs may be accustomed to co-investing without fees or carry, deal dynamics, asset class, and access to opportunities can drive fees in certain scenarios.

Economics & Monetization

Co-investment terms have remained relatively stable and consistent in recent years. As in private funds generally, we have seen an increase in LP requests for enhanced transparency and reporting with respect to co-investments, particularly in the ESG/impact space.

Monetizing co-investments, whether through a management fee, administrative fee, placement fee, or carried interest arrangement is a perennial topic of conversation among GPs. While some LPs may be accustomed to co-investing without fees or carry, deal dynamics, asset class, and access to opportunities can drive fees in certain scenarios.

Co-Investment and Continuation Vehicles

The rapid growth of GP-led secondaries transactions over the past few years has led to questions about the implications of such transactions for co-investors. In a GP-led secondary transaction, where one or more of a fund’s assets are transferred to a continuation vehicle, fund LPs are typically given the option to roll their interest in such assets into the continuation vehicle or to receive a cash distribution for their interest in such assets. An LP that elects to roll its interest into the continuation vehicle will retain its exposure to any future upside in the assets, but will also be subject to the terms of the continuation vehicle, which may provide that an LP retains the key terms that applied to its investment in the original fund (i.e., a “status quo” option) or which may have terms that differ from those of the original fund.

GPs and LPs typically seek alignment between the fund and co-investors with respect to any liquidity event – often via tag and drag rights with respect to asset dispositions to ensure that the fund and co-investors are generally exiting at the same time and on the same terms. There may, however, be a carveout from such rights in certain instances.

A common point of discussion in new co-investment arrangements is express language regarding how a GP-led secondary transaction should be treated and whether and on what terms co-investors should be able or required to roll their interest into the continuation vehicle. Co-investors who are interested in rolling into the continuation vehicle may be particularly concerned about the ability to do so on a “status quo” basis, in order to preserve their preferential economic terms.

Co-Investment and Continuation Vehicles

The rapid growth of GP-led secondaries transactions over the past few years has led to questions about the implications of such transactions for co-investors. In a GP-led secondary transaction, where one or more of a fund’s assets are transferred to a continuation vehicle, fund LPs are typically given the option to roll their interest in such assets into the continuation vehicle or to receive a cash distribution for their interest in such assets. An LP that elects to roll its interest into the continuation vehicle will retain its exposure to any future upside in the assets, but will also be subject to the terms of the continuation vehicle, which may provide that an LP retains the key terms that applied to its investment in the original fund (i.e., a “status quo” option) or which may have terms that differ from those of the original fund.

GPs and LPs typically seek alignment between the fund and co-investors with respect to any liquidity event – often via tag and drag rights with respect to asset dispositions to ensure that the fund and co-investors are generally exiting at the same time and on the same terms. There may, however, be a carveout from such rights in certain instances.

A common point of discussion in new co-investment arrangements is express language regarding how a GP-led secondary transaction should be treated and whether and on what terms co-investors should be able or required to roll their interest into the continuation vehicle. Co-investors who are interested in rolling into the continuation vehicle may be particularly concerned about the ability to do so on a “status quo” basis, in order to preserve their preferential economic terms.

SEC’s Private Fund Adviser Rules

On August 23, 2023, the SEC adopted the new private fund adviser rules, which radically alter the regulation of private funds and pose many interpretative questions. The compliance dates for the new rules are generally September 14, 2024, and March 14, 2025, depending on the rule and the size of the GP. The rules are subject to ongoing litigation initiated by industry organizations against the SEC in the U.S. Court of Appeals for the Fifth Circuit, where the petitioners have requested a decision by May 31, 2024. Once the court issues its opinion, a non-prevailing party can ask the Fifth Circuit to rehear the case “en banc” and/or can petition the U.S. Supreme Court to hear the case.

The future of the private fund adviser rules and the scope of their application to co-investments is currently unclear. At this time, we are not seeing GPs and LPs significantly change their approach to co-investments and co-investing terms in light of the private fund adviser rules, although that could change depending on the Fifth Circuit’s decision.

SEC’s Private Fund Adviser Rules

On August 23, 2023, the SEC adopted the new private fund adviser rules, which radically alter the regulation of private funds and pose many interpretative questions. The compliance dates for the new rules are generally September 14, 2024, and March 14, 2025, depending on the rule and the size of the GP. The rules are subject to ongoing litigation initiated by industry organizations against the SEC in the U.S. Court of Appeals for the Fifth Circuit, where the petitioners have requested a decision by May 31, 2024. Once the court issues its opinion, a non-prevailing party can ask the Fifth Circuit to rehear the case “en banc” and/or can petition the U.S. Supreme Court to hear the case.

The future of the private fund adviser rules and the scope of their application to co-investments is currently unclear. At this time, we are not seeing GPs and LPs significantly change their approach to co-investments and co-investing terms in light of the private fund adviser rules, although that could change depending on the Fifth Circuit’s decision.

For more information on the private fund adviser rules, please see Cleary Gottlieb's in-depth client alert.

Market dynamics continue to drive demand for co-investments, which we expect to play a growing role in private equity dealmaking and fundraising in 2024 and beyond.