Private Equity Market Snapshot: Silicon Valley Bank Focus

April 2023

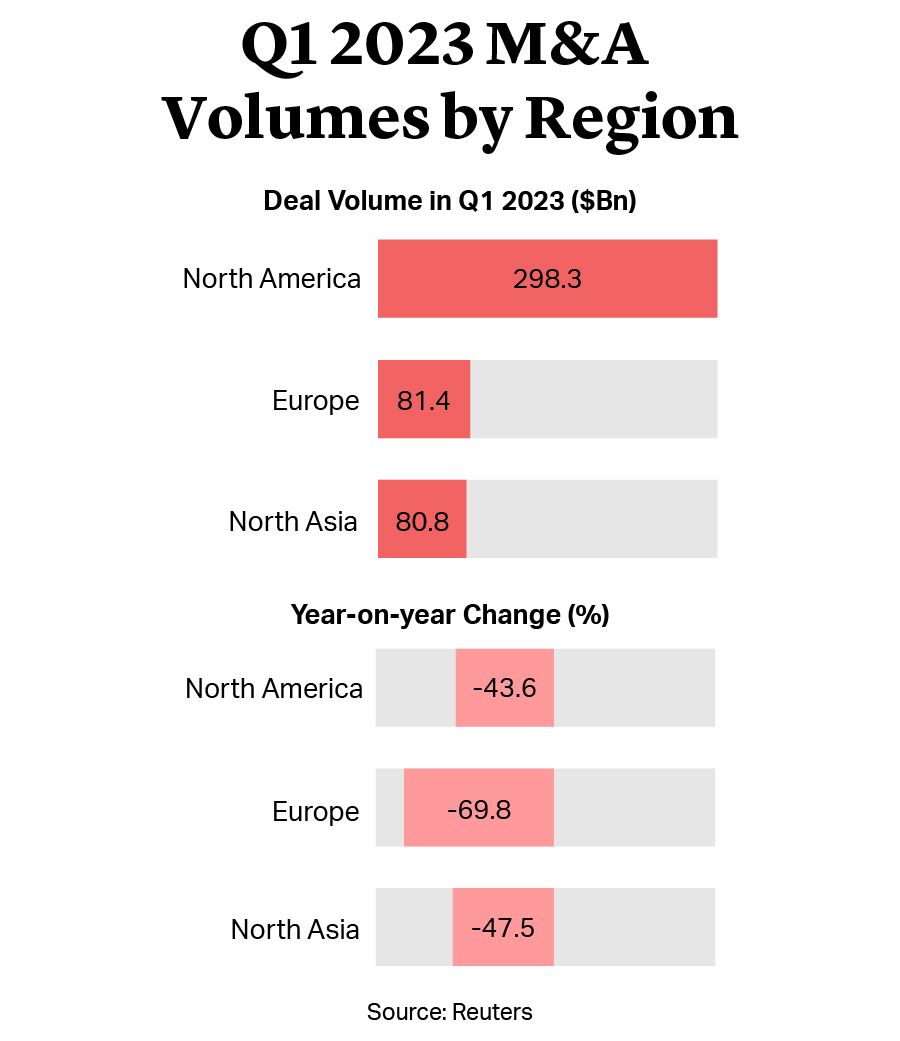

M&A activity slowed across the board in the first quarter of 2023 after the collapse of Silicon Valley Bank shook the banking sector and knocked already-fragile confidence. Dealogic data reported by Reuters showed that global deal volumes – including strategic M&A and private equity takeovers – fell by 48% to $575bn in the first quarter, the lowest level in over a decade. European M&A fell at an even sharper rate, contracting by almost 70% to $81bn1.

Despite the downturn, there were bright spots as private equity firms pursued new investments and secured exits by adapting to the financing conditions. Cinven agreed a deal to buy the concrete admixtures business of Germany’s Sika for an undisclosed amount, and was reported to have funded the purchase with equity only2. Sika had previously planned to sell the building materials business to Ineos but the deal was reported to have faced concerns from UK regulators.

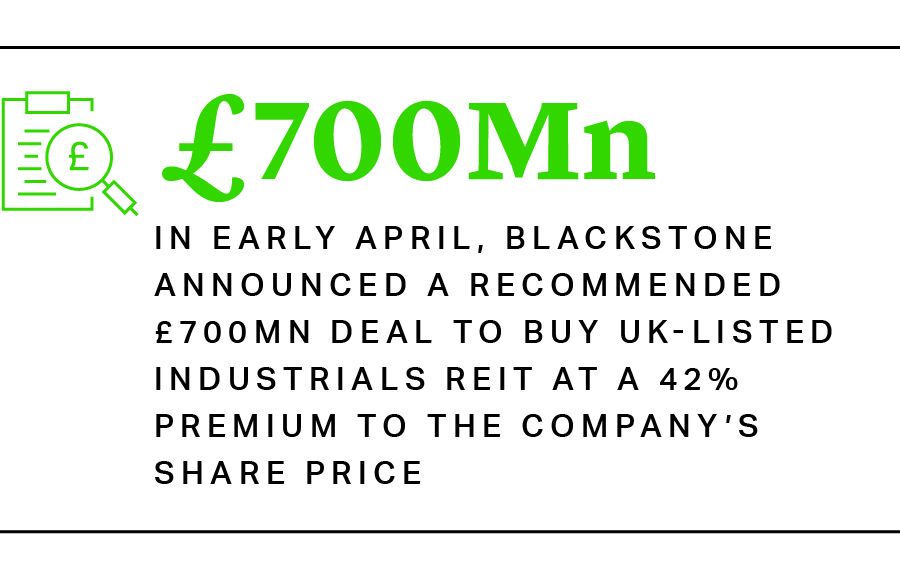

Private equity also continued to hunt for undervalued investments on public markets. In early April, Blackstone announced a recommended £700mn deal to buy UK-listed Industrials REIT at a 42% premium to the company’s share price3. This was closely followed by Dechra Pharmaceuticals’ confirmation of a possible £4.6 billion cash bid from EQT, backed by a leading UAE sovereign wealth fund4. However, the increasingly activist approach of public market investors was also on display. M&G Investments said it would vote against Providence Equity Partners’ planned £481mn takeover of London-listed events group Hyve on the grounds that it significantly undervalued the company5. Providence struck a deal at 108 pence per share in March, well below that company’s pre-pandemic high in excess of 600 pence.

M&A activity slowed across the board in the first quarter of 2023 after the collapse of Silicon Valley Bank shook the banking sector and knocked already-fragile confidence. Dealogic data reported by Reuters showed that global deal volumes – including strategic M&A and private equity takeovers – fell by 48% to $575bn in the first quarter, the lowest level in over a decade. European M&A fell at an even sharper rate, contracting by almost 70% to $81bn1.

Despite the downturn, there were bright spots as private equity firms pursued new investments and secured exits by adapting to the financing conditions. Cinven agreed a deal to buy the concrete admixtures business of Germany’s Sika for an undisclosed amount, and was reported to have funded the purchase with equity only2. Sika had previously planned to sell the building materials business to Ineos but the deal was reported to have faced concerns from UK regulators.

Private equity also continued to hunt for undervalued investments on public markets. In early April, Blackstone announced a recommended £700mn deal to buy UK-listed Industrials REIT at a 42% premium to the company’s share price3. This was closely followed by Dechra Pharmaceuticals’ confirmation of a possible £4.6 billion cash bid from EQT, backed by a leading UAE sovereign wealth fund4. However, the increasingly activist approach of public market investors was also on display. M&G Investments said it would vote against Providence Equity Partners’ planned £481mn takeover of London-listed events group Hyve on the grounds that it significantly undervalued the company5. Providence struck a deal at 108 pence per share in March, well below that company’s pre-pandemic high in excess of 600 pence.

Silicon Valley Bank Collapse Adds to Market Uncertainty

The collapse of Silicon Valley Bank in early March hit recovering market sentiment and raised concerns about a new banking crisis. Fears swept across Europe, highlighting banks with the weakest balance sheets and the highest potential for bad assets. After the merger of Credit Suisse and UBS, investors briefly alighted on Deutsche Bank, before German Chancellor Olaf Scholz sought to soothe markets6. While the European Stoxx 600 largely regained its pre-SVB levels, the FTSE 100 was almost 4% lower at the end of March, reflecting broader concerns about the economy and the ongoing impact of interest rate rises.

The UK authorities were quick to broker a takeover of SVB UK by HSBC in the weekend following the bank’s collapse. With just £6.7bn of deposits and around £5.5bn of loans as of 10 March7, SVB UK is a small but nonetheless well-connected player in the UK venture capital and start-up space. The deal boosts HSBC’s capacity in the tech and biotech market, however, start-ups may not benefit from the kind of personalized service that they received from SVB. Despite only costing HSBC £1 in consideration, the bank met stiff criticism from shareholders in Hong Kong who were concerned that it was acting under the control of the UK government8.

Investment Banking Fallout Weighs on Private Equity

The collapse of SVB and the merger of Credit Suisse and UBS have added to the challenges facing private equity and venture capital in Europe. The volatility is likely to push out the recovery of investment activity, which many in the market had expected to pick up in the second quarter of 2023. In the face of uncertainty, private equity firms will be more inclined to postpone planned investments and disposals until the outlook is clearer. Large corporates are also more likely to hold onto cash and delay any capital expenditure plans, although deals that were already in the pipeline have continued. At the end of March, German pharma group Sartorius announced the €2.4bn takeover of French gene-therapy technology company Polyplus from investors including healthcare private equity firm Archimed9.

There will be practical near-term implications for private equity in Europe also. The high profile shocks to hit the banking sector in recent months are expected to lead to tens of thousands of job losses worldwide including many in London where investment banking and advisory personnel numbers are strong10. The result is likely to impact the flow of financing as well relationships governing capital markets activities, including fundraising and secondaries advisory in which both banks have a strong presence.

Banking Disruption Also Unearths New Opportunities

At the same time as it has created disruption, the banking crisis has also shone a light on new opportunities. First Citizens' purchase of SVB’s U.S. deposits and loans does not include investment banking assets or SVB Capital, the investment division with some $9.5bn of holdings in VC funds including Sequoia, Andreessen Horowitz and Index, which is expected to draw the attention of asset managers and secondaries players11.

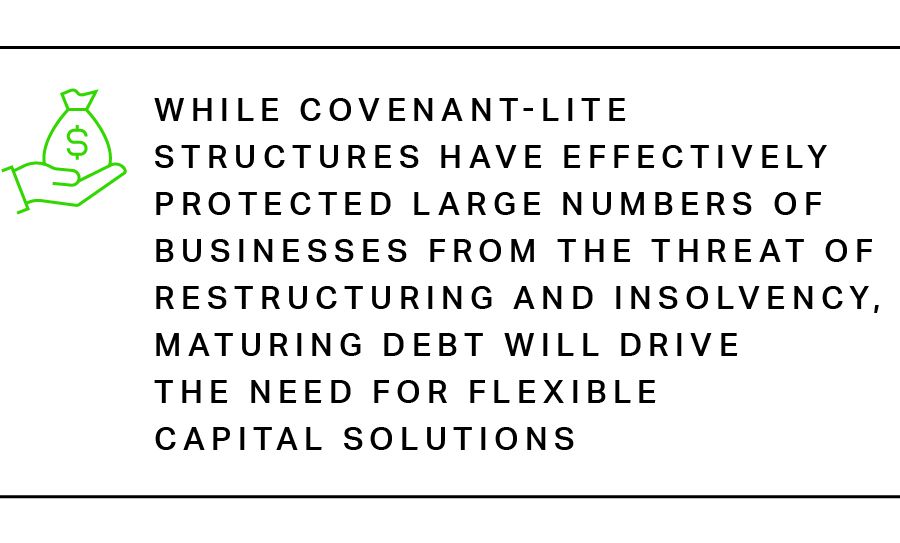

With access to financing tightening further amid the banking disruption, there will be more opportunities for private equity to provide refinancing for small and medium-sized companies that find themselves under increased financial stress. While covenant-lite structures have effectively protected large numbers of businesses from the threat of restructuring and insolvency, maturing debt will drive the need for flexible capital solutions. That will create opportunities for distressed debt investors, as well as private equity firms in a position to provide hybrid financing, such as preferred equity or mezzanine debt with warrants.

Private Equity Returns Soften but Outperform Public Markets

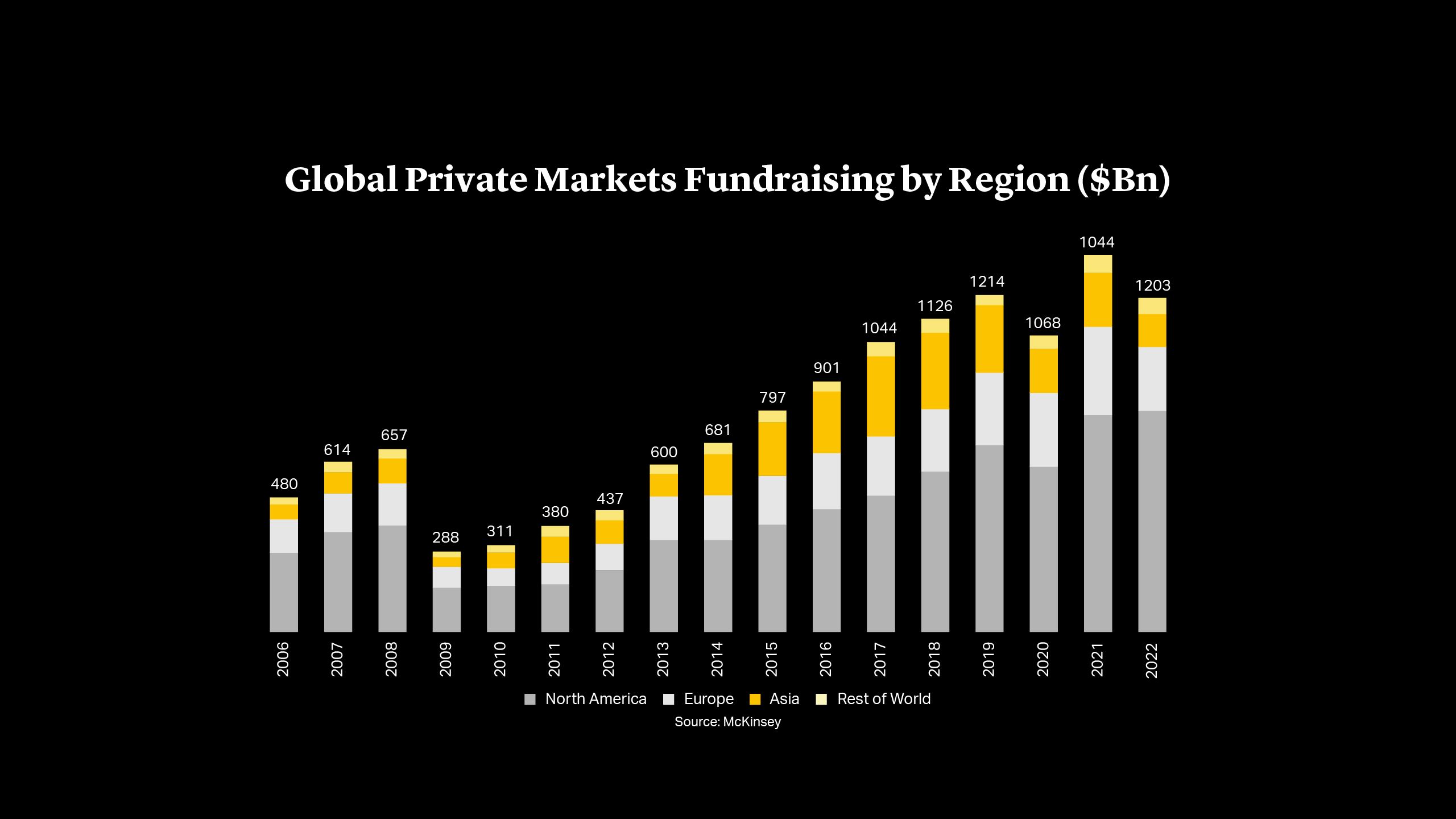

Having avoided the sharp slump in valuations recorded in public markets in the first half 2022, declining returns have begun to catch up with the private equity industry. According to data from McKinsey, the industry recorded a -9% return for the 12 months to September 202212. While it marks the first negative performance since 2008, the return still compares favorably with the almost 18% decline in the S&P 500 and the 14% fall in the Stoxx 600 over the same period. Pressure on valuations may yet crystalize as a result of the persistence of high interest rates and difficult financing conditions, however. In its annual report on the industry, private equity investor and advisor Hamilton Lane claimed that most private equity assets are conservatively valued and should maintain their value13.

Private Equity Returns Soften but Outperform Public Markets

Having avoided the sharp slump in valuations recorded in public markets in the first half 2022, declining returns have begun to catch up with the private equity industry. According to data from McKinsey, the industry recorded a -9% return for the 12 months to September 202212. While it marks the first negative performance since 2008, the return still compares favorably with the almost 18% decline in the S&P 500 and the 14% fall in the Stoxx 600 over the same period. Pressure on valuations may yet crystalize as a result of the persistence of high interest rates and difficult financing conditions, however. In its annual report on the industry, private equity investor and advisor Hamilton Lane claimed that most private equity assets are conservatively valued and should maintain their value13.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card