From Industrials to Cleantech, Germany Offers Private Equity Opportunities

Germany’s industrial strength has provided private equity with a rich seam of carve-outs and big buyouts down the years. The sale of ThyssenKrupp’s elevators division to a consortium led by Advent International and Cinven for €17.2bn, agreed just before the first COVID-19 lockdowns of 2020, was one Europe’s largest ever deals and highlighted the scale of opportunity for global private equity firms. While manufacturing and industrials continue to provide potential large and mid-market buyouts, the country’s pivot to green energy and climate tech – accelerated by the impact of war in Ukraine on energy prices and security – is creating a new wave of deals focused on growth and innovation.

German Corporates Yield Large Buyout Potential

Following the high water mark set by the ThyssenKrupp deal, deal activitiy continued strongly in the investment rebound of 2021, driven by the potential for recovery in Europe’s largest economy. After initially competing for pet food retailer Zooplus, Hellman & Friedman and EQT teamed up to offer €3.7bn for the company’s shares, representing an 85% premium for the Frankfurt-listed company. Investment has also homed in on international businesses based in Germany, including Vantage Towers, the wireless telecoms carrier for Vodafone which spans 10 countries across Europe. In November 2022, the German-headquartered business agreed a €16bn joint venture with KKR and GIP, backed by Saudi Arabia’s Public Investment Fund, giving the investors access to a portfolio of stable and cash-generative assets, while enabling Vodafone to cut its debt.

High interest rates and inflation are likely to create rising pressure on German companies, and could contribute to more disposals. Furthermore, the conditions could narrow the disconnect between buyer and seller price expectations, providing further impetus for deal activity.

German pharma and chemicals giant Merck is reported to be preparing the sale of its pigments business, which could be worth over €1bn1, while state-backed railroad operator Deutsche Bahn is said to be preparing the sale of its logistics assets with a valuation of up to €20bn2. Both transactions are expected to draw interest from international private equity firms, as well as major strategic buyers.

New German Mittelstand Investments Emerge in the Mid-Market

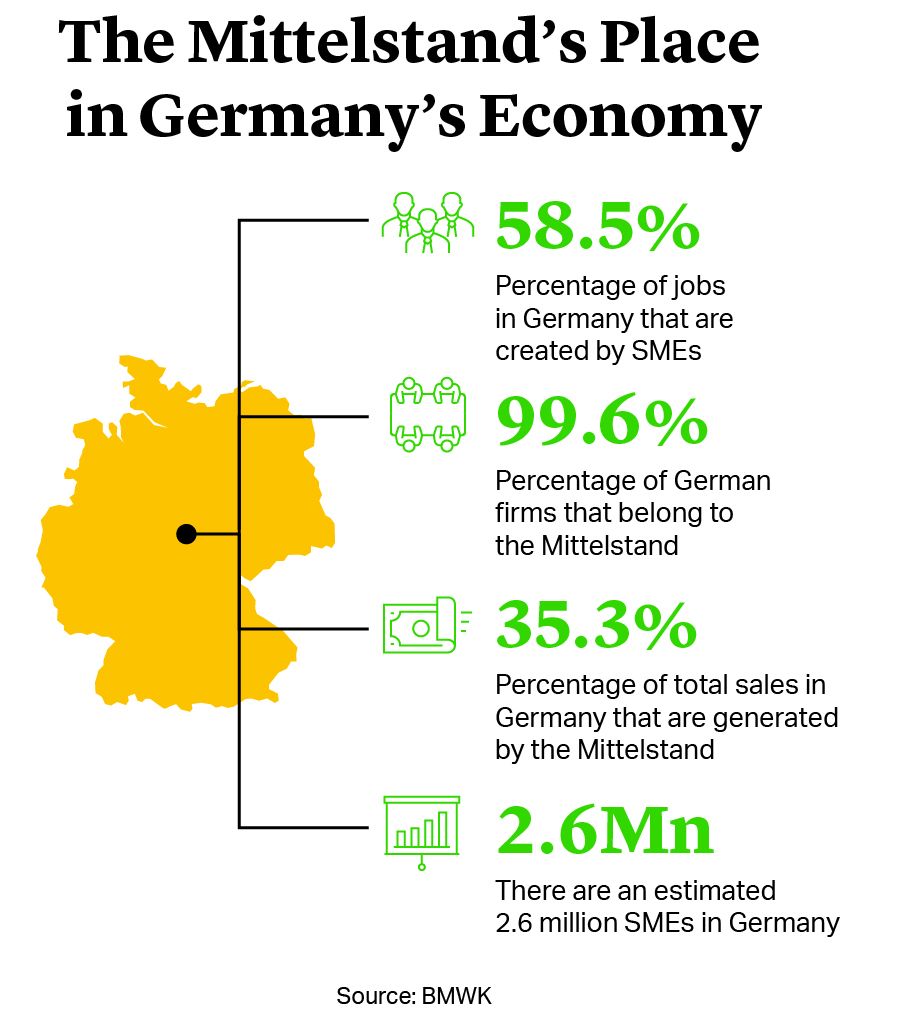

While large carve-outs grab the headlines in Germany, the country’s economic force continues to be its “Mittelstand” – the wealth of small and medium-sized enterprises (SMEs) that employ millions and drive job creation. There are an estimated 2.6mn SMEs in Germany3, accounting for over 99% of all companies across the country, and 58.5% of jobs created4, national statistics show.

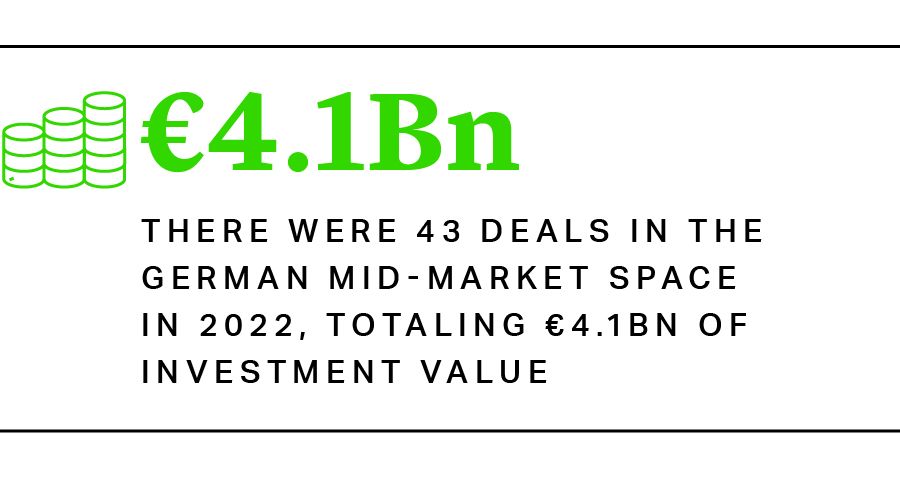

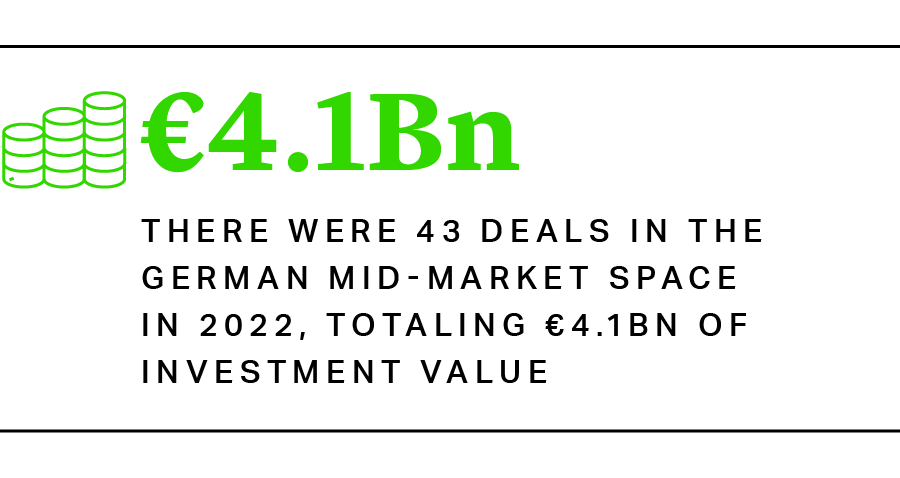

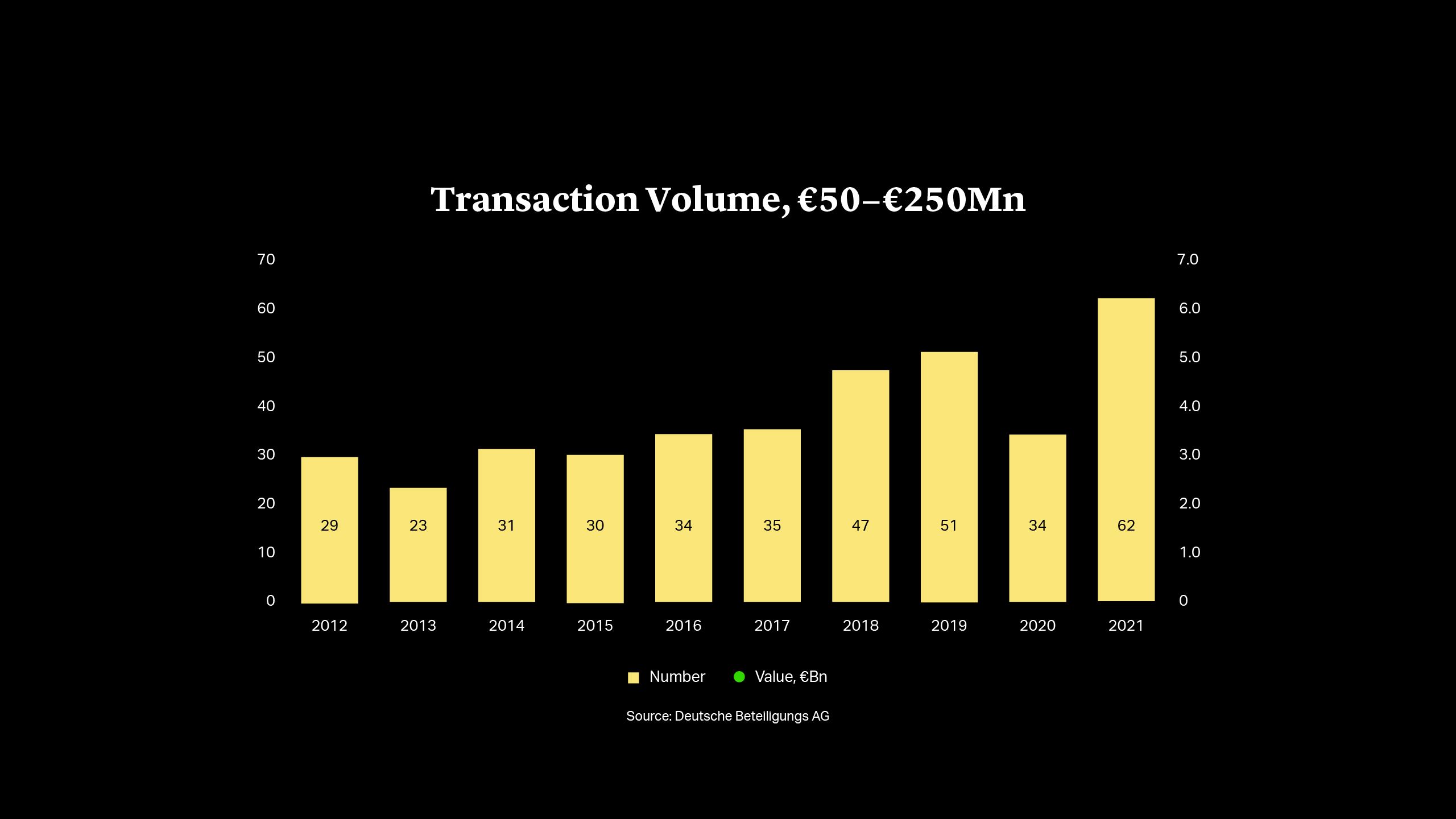

Many SMEs are below the scale of mid-market private equity appetite, but increasing numbers of family and privately owned businesses are warming to private equity as a means of funding future growth and managing succession challenges. According to research from German listed private equity group Deutsche Beteiligungs, there were 62 buyouts worth €6.6bn led by financial investors in the mid-market space in 2021, more than double the number and volume achieved in 2015. While the number dipped sharply in 2022 amid the global slowdown in private equity activity, the 43 deals and €4.1bn of investment value remained well above long-term averages5. The figures included 16 transactions in the software and IT services space, over a third of the total, while the majority were primary deals in companies that had never received private equity investment before.

That expansion in Germany’s tech space is leading to the development of more domestically founded and focused firms, such as Flex Capital, which in January raised a €300mn second fund to roll up SMEs in the DACH region and fuel their expansion internationally6.

New German Mittelstand Investments Emerge in the Mid-Market

While large carve-outs grab the headlines in Germany, the country’s economic force continues to be its “Mittelstand” – the wealth of small and medium-sized enterprises (SMEs) that employ millions and drive job creation. There are an estimated 2.6mn SMEs in Germany3, accounting for over 99% of all companies across the country, and 58.5% of jobs created4, national statistics show.

Many SMEs are below the scale of mid-market private equity appetite, but increasing numbers of family and privately owned businesses are warming to private equity as a means of funding future growth and managing succession challenges. According to research from German listed private equity group Deutsche Beteiligungs, there were 62 buyouts worth €6.6bn led by financial investors in the mid-market space in 2021, more than double the number and volume achieved in 2015. While the number dipped sharply in 2022 amid the global slowdown in private equity activity, the 43 deals and €4.1bn of investment value remained well above long-term averages5. The figures included 16 transactions in the software and IT services space, over a third of the total, while the majority were primary deals in companies that had never received private equity investment before.

That expansion in Germany’s tech space is leading to the development of more domestically founded and focused firms, such as Flex Capital, which in January raised a €300mn second fund to roll up SMEs in the DACH region and fuel their expansion internationally6.

Energy Pivot Fuels Energy and Cleantech Investment

Despite the impact of the energy crisis in 2022, Germany has maintained some of the most ambitious energy transition targets in Europe. The government closed the remaining nuclear powerplants in April and continued decommissioning ageing sites across the country. The use of coal-fired power generation did pick up during recent energy shortages, but is scheduled to be phased out by 2038, with some regions, such as North Rhine Westphalia, hoping to exit coal production and use by 20307. The government is also clamping down on domestic consumption of fossil fuels and aims to ban new oil and gas boilers from 2024.

That change in focus is already leading to funding for cleantech start-ups that is bucking the broader growth and venture investment slowdown. German solar panel group Enpal raised $215mn in January from a consortium led by TPG Rise, which saw the company nearly double its valuation to $2.4bn8.

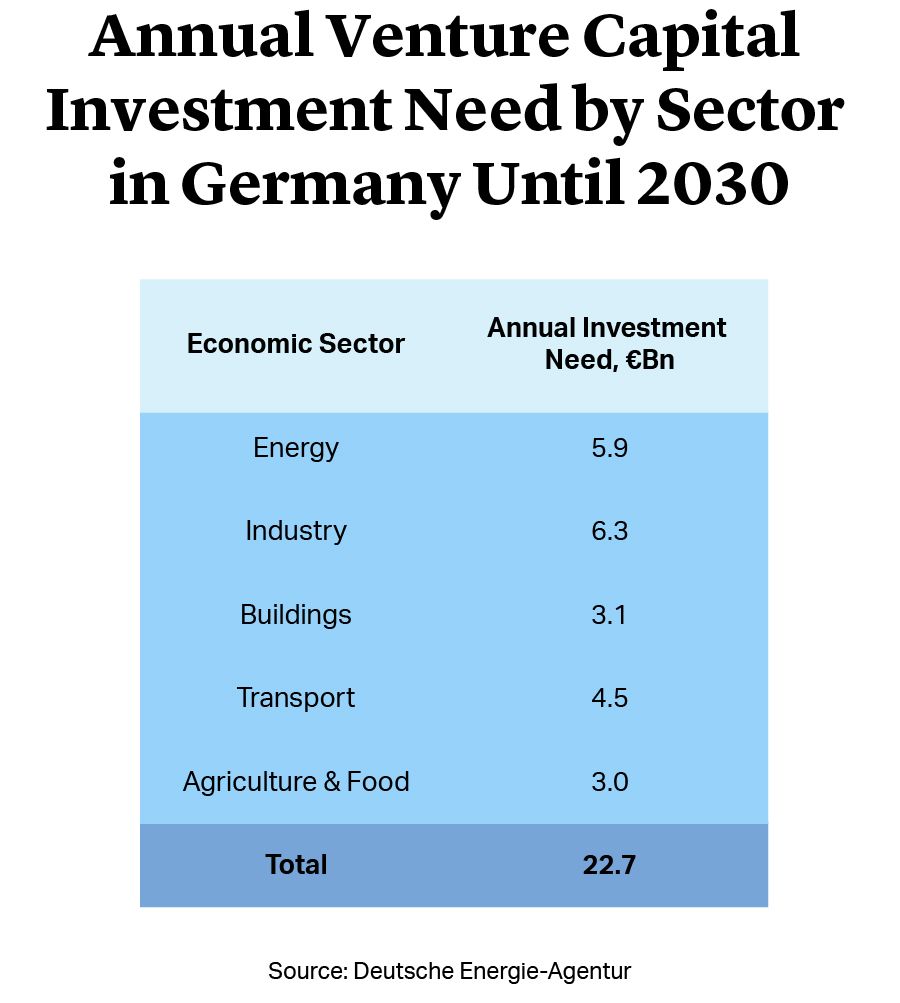

At the same time, the government has been committing new investment and support to renewables and green technology. In February, it created the €1bn DeepTech & Climate Fonds vehicle to invest alongside private investors to boost promising green start-ups and SMEs9. The possibilities could be much greater, however. The Tech for Net Zero Alliance estimated that the climate tech financing opportunity in Germany could represent almost €23bn a year until 2030 – some €200bn in total – and span sectors from energy and industry to transport and food10, providing widespread potential for private equity to participate in the green transition in Europe’s largest market.

Energy Pivot Fuels Energy and Cleantech Investment

Despite the impact of the energy crisis in 2022, Germany has maintained some of the most ambitious energy transition targets in Europe. The government closed the remaining nuclear powerplants in April and continued decommissioning ageing sites across the country. The use of coal-fired power generation did pick up during recent energy shortages, but is scheduled to be phased out by 2038, with some regions, such as North Rhine Westphalia, hoping to exit coal production and use by 20307. The government is also clamping down on domestic consumption of fossil fuels and aims to ban new oil and gas boilers from 2024.

That change in focus is already leading to funding for cleantech start-ups that is bucking the broader growth and venture investment slowdown. German solar panel group Enpal raised $215mn in January from a consortium led by TPG Rise, which saw the company nearly double its valuation to $2.4bn8.

At the same time, the government has been committing new investment and support to renewables and green technology. In February, it created the €1bn DeepTech & Climate Fonds vehicle to invest alongside private investors to boost promising green start-ups and SMEs9. The possibilities could be much greater, however. The Tech for Net Zero Alliance estimated that the climate tech financing opportunity in Germany could represent almost €23bn a year until 2030 – some €200bn in total – and span sectors from energy and industry to transport and food10, providing widespread potential for private equity to participate in the green transition in Europe’s largest market.

Nico Abel

Partner

Frankfurt

T: +49 69 97103 190

nabel@cgsh.com

V-Card

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card