Private Equity

Market Snapshot

March 2023

Private equity has been cautious through the first quarter of 2023, as the world continues to navigate uncertain conditions. Stronger than expected economic performance has raised the likelihood of continued interest rate rises to combat persistent high inflation. Even the UK, the weakest of the G7 economies, appears to be defying the worst expectations so far, and inflation surprisingly ticked up in late March. Both the Bank of England and the Office for Budget Responsibility have forecast a five-quarter-long recession starting in the first three months of 2023, but official figures showed GDP growth of 0.3% in January1.

Against this uncertainty, the deal pipeline is filling slowly, and buyers and sellers are moving with care, testing the valuation gaps between them. However, sponsors are also happy to be opportunistic and move quickly when value is identified. Prospective pockets include sections of the venture and growth capital space, companies seeking alternative liquidity solutions, opportunities created by corporate spin-outs and also the public markets. The UK is not the only market where private equity investors are hunting for listed companies though. Northern Europe-focused Triton and Bain Capital have been engaged in a bidding war for Finnish listed building maintenance services provider Caverion, with Triton’s latest offer valuing the group at some €1.2bn2.

Optimism and Expectations Build for H2 2023

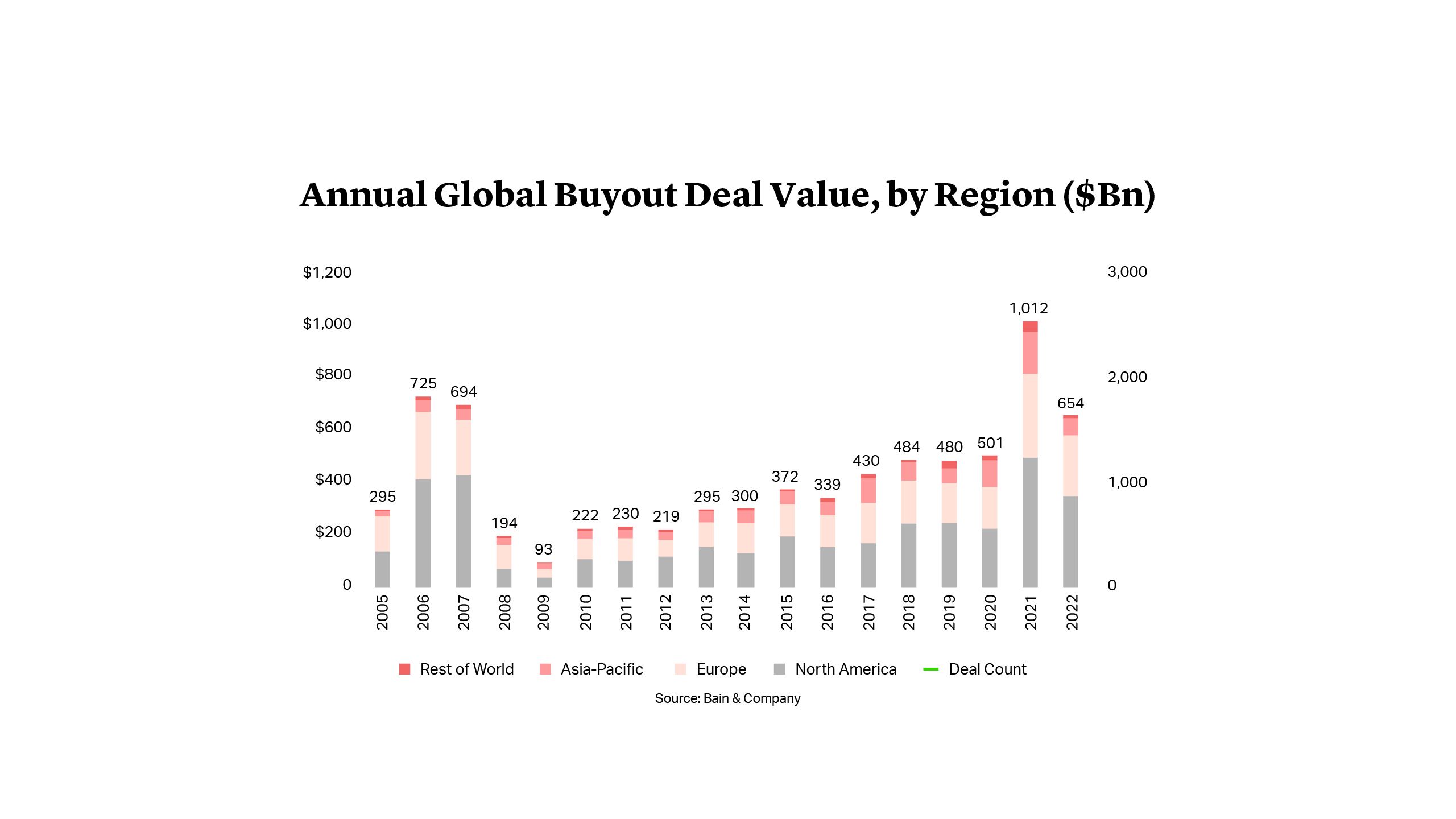

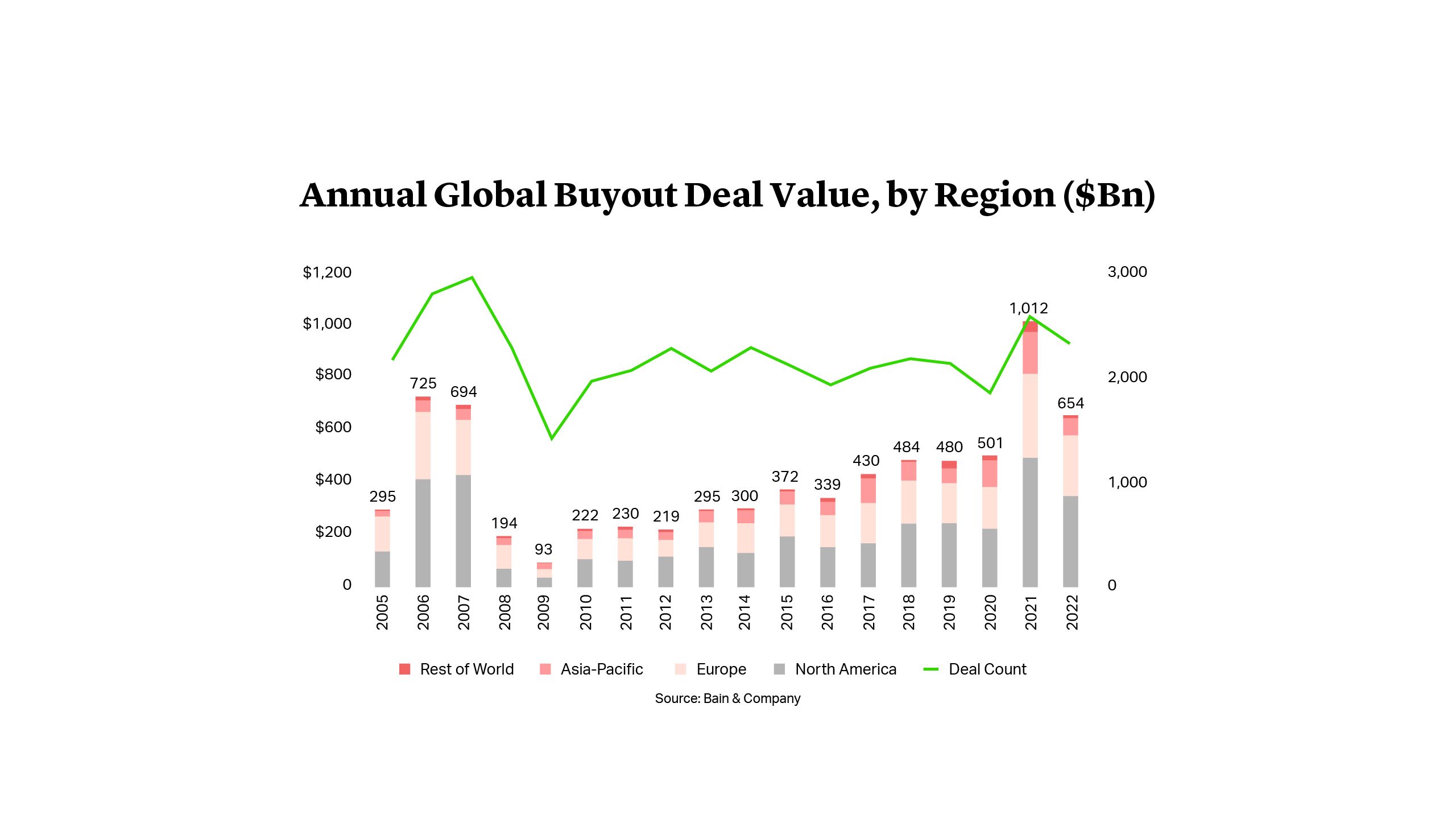

New data and research show what a year of contrasts 2022 was for private equity. Total buyout value (excluding the large and accelerating trend to bolt-on deals) was $654bn in 2022, a 35% decline from 2021, according to Bain & Co’s Global Private Equity Report 2023. Nevertheless, that ranked as the second-best calendar year on record for private equity, indicating the relentless momentum of 2021 that carried into the first half of 20223. In Europe, investment fell particularly precipitously in the second half of 2022, as concerns about the outlook for the UK and continental economies darkened, inflation jumped and banks sharply reduced lending.

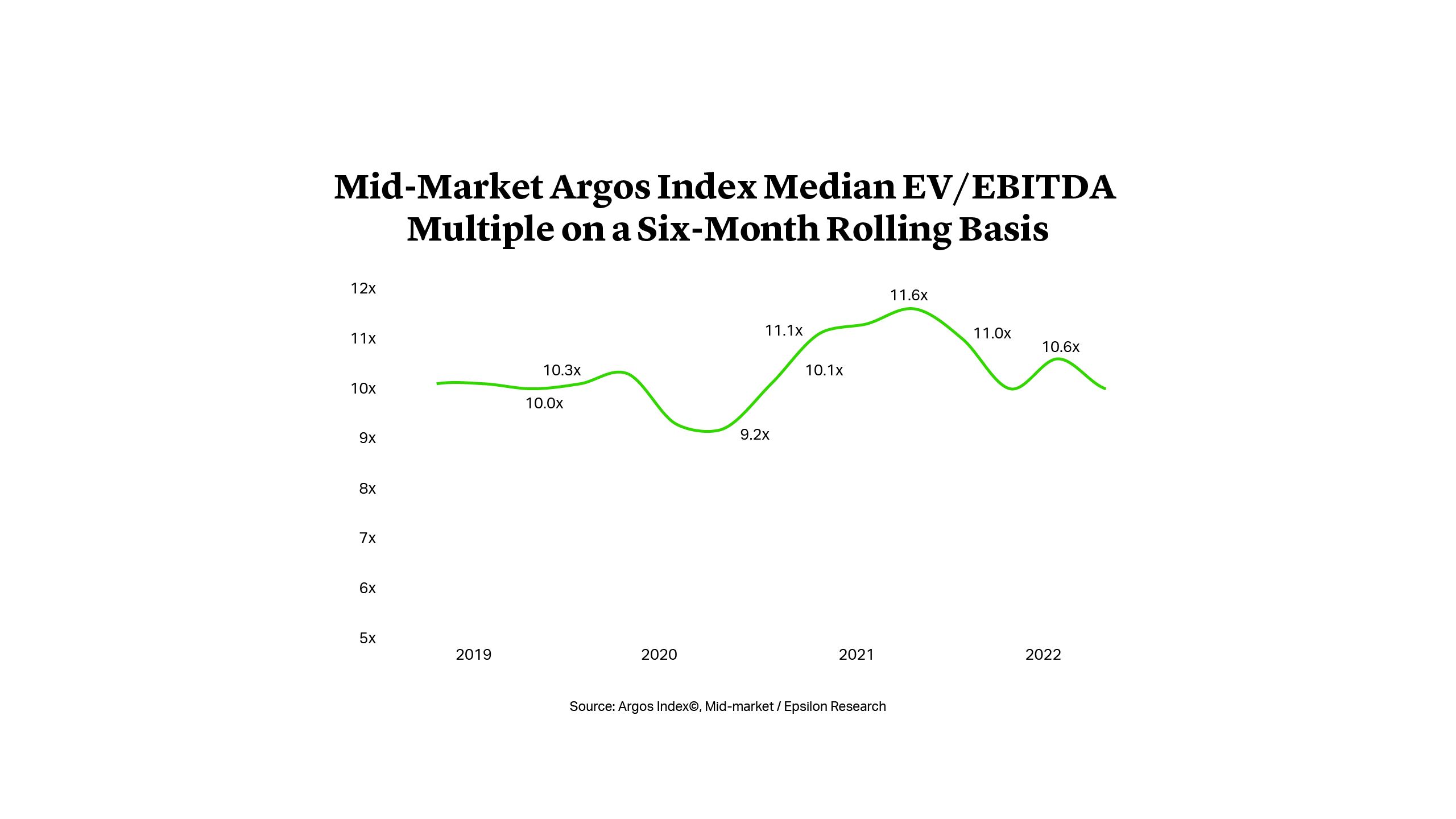

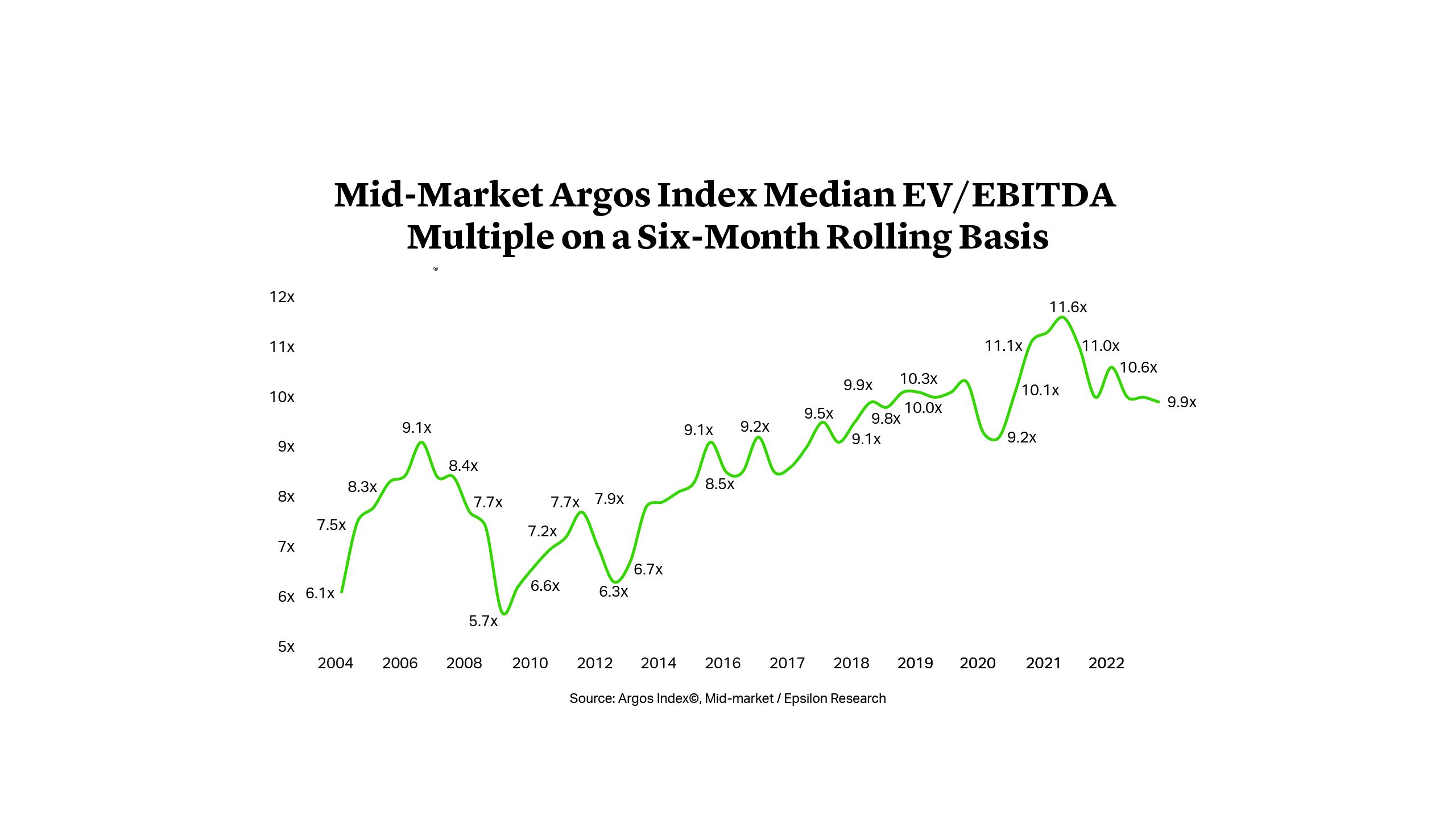

There are signals of a correction that could provide an impetus for a recovery in deal activity. Bain & Co data shows that investment multiples contracted to 10.7x EBITDA in 2022, taking them back to pre-COVID levels. For mid-market investments, prices are lower still, with the Argos Wityu index dropping to 9.9x – similarly bringing assets back in line with 2018 and 2019 pricing4.

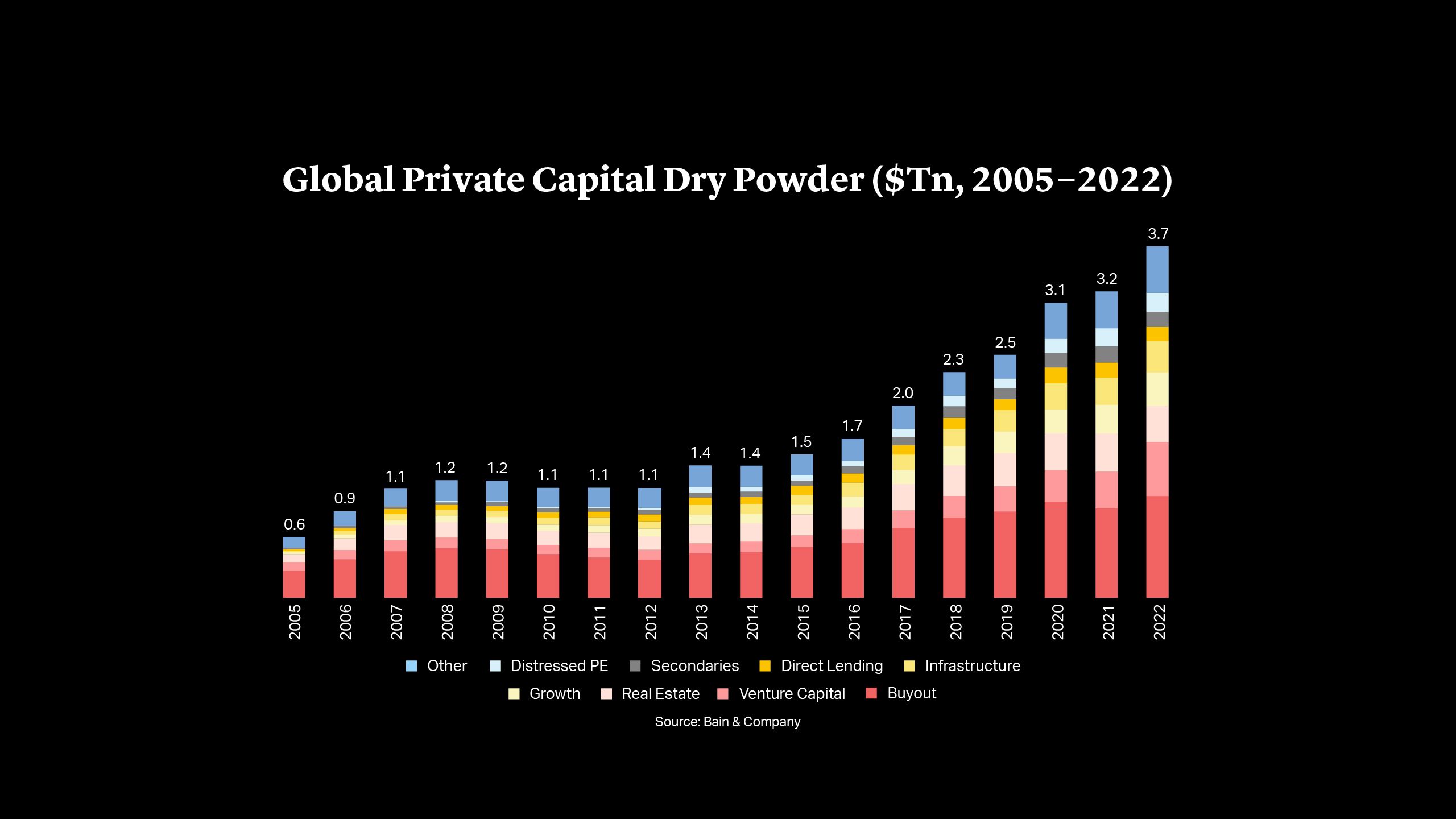

Expectations of a sharper contraction in multiples appear relatively unlikely, however. In a recent report, private equity investment firm Hamilton Lane opined that holding valuations remained broadly fair, given earnings growth at many private companies that exceeded public peers, relatively conservative existing valuation levels, and the potential for follow-on equity to support companies5. Consistently high levels of dry powder are also helping keep a floor under prices, particularly for the best performing companies in resilient sectors such as technology or healthcare. Bain & Co put total private capital dry powder at $3.7tn at the end of 2022, a new record, with buyout funds accounting for 20% of the total. Direct lenders are also increasingly active, providing some of the capacity withdrawn by traditional banks.

Much of the complexity and uncertainty that marked the second half of 2022 remains. We see many private equity firms remaining cautious in the current environment, while expecting – and preparing for – a broader recovery in activity in the second half of 2023.

Markets Watch for Silicon Valley Bank Fallout

The collapse of Silicon Valley Bank in mid-March has potentially wide-reaching repercussions for venture capital firms and the companies they back across Europe. UK Chancellor Jeremy Hunt spoke of a serious risk to the tech industry, while founders warned of the threat of not being able to pay wages and bills in the short term6. To avert an escalating crisis, the UK government helped broker a sale of Silicon Valley Bank’s UK arm to HSBC, giving immediate security to start-ups and other depositors that have some £6.7bn of deposits with the bank.

While companies will be able to access their deposits for essential business purposes, the failure will likely lead to some reshaping of start-up finances, as well as those of fund managers, many of whom also accessed fund financing and other services at the bank. The full impact of the collapse and risk of contagion to other financial services firms will take time to unfold, and UBS’ acquisition of Credit Suisse is a reminder that events of such significance rarely happen in isolation. A reinvestigation of banking regulation and oversight in Europe or even globally may yet follow.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card