Private Debt

Becomes Mainstream

Buyout Debt

The global private debt market has hit new levels of mainstream acceptance as banks have become more cautious about lending into a downturn and rising interest rates increase the potential rewards for debt fund managers and investors alike. The reported $5.5bn private debt financing package being prepared for Carlyle Group’s planned purchase of a 50% stake in U.S. healthcare analytics company Cotiviti, valued in excess of $15bn, represents a potential new high-water mark for private lending, underscoring the scale and competitiveness of the strategy. Europe is seeing similar appetite which will drive ever-larger private debt packages for the region’s buyouts.

Private Lenders Step Into Financing Larger Buyouts

Market volatility in 2022 raised concerns about banks’ exposure to leveraged buyouts, as many struggled to syndicate large debt packages agreed during the surge in dealmaking in 2021. The dislocation opened the door for private debt funds, which typically hold debt to maturity and operate in small clubs, to increase their focus on larger buyouts.

Among the recent debt agreements, Sixth Street Partners agreed a $2.3bn package to back Advent International’s buyout of satellite operator Maxar Technologies in December1. Such funds have also taken a flexible approach to working with banks. Goldman Sachs’ private lending arm and Sixth Street joined forces in October to provide $2.3bn of private debt for Blackstone’s purchase of Emerson Electric’s climate technology business, alongside a loan from more traditional lenders and a portion of seller financing2.

Despite fewer large and mega-buyouts in Europe, there have been opportunities for private debt funds to participate in large financings. In June last year, Hg and TA Associates secured £3.5bn from a group of direct lenders for their reinvestment and refinancing of UK management software provider Access Group, including one of the largest ever unitranche packages at £2.3bn. The pair were reported to be seeking to add a further £500mn to the financing in February this year, tapping into continued private lending appetite3.

While banks can offer lower lending rates than funds on the senior debt portion, private debt providers tend to have greater flexibility to provide senior or unitranche loans to buyouts, or move down the capital structure to provide mezzanine debt or preferred equity.

Investors Target More Capital at Private Debt Funds

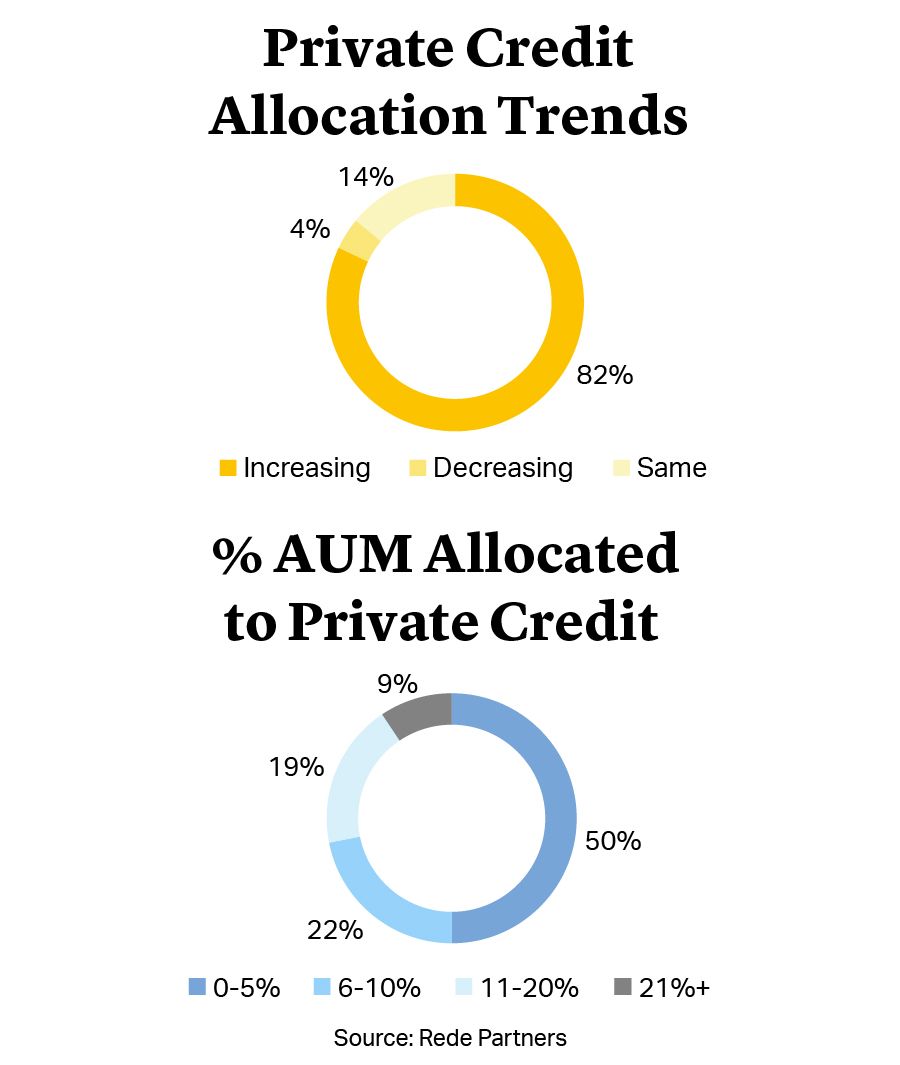

Behind the surge in private lending for buyouts is equally strong appetite from institutional investors for the asset class, which is seen to offer attractive risk-adjusted returns and interest-rate-hedging capabilities as loans are typically structured with a floating rate. According to a 2022 survey of large institutional investors by advisory firm Rede Partners, 82% expected to increase exposure to private debt funds in the coming year compared with just 4% who expected to reduce allocations4.

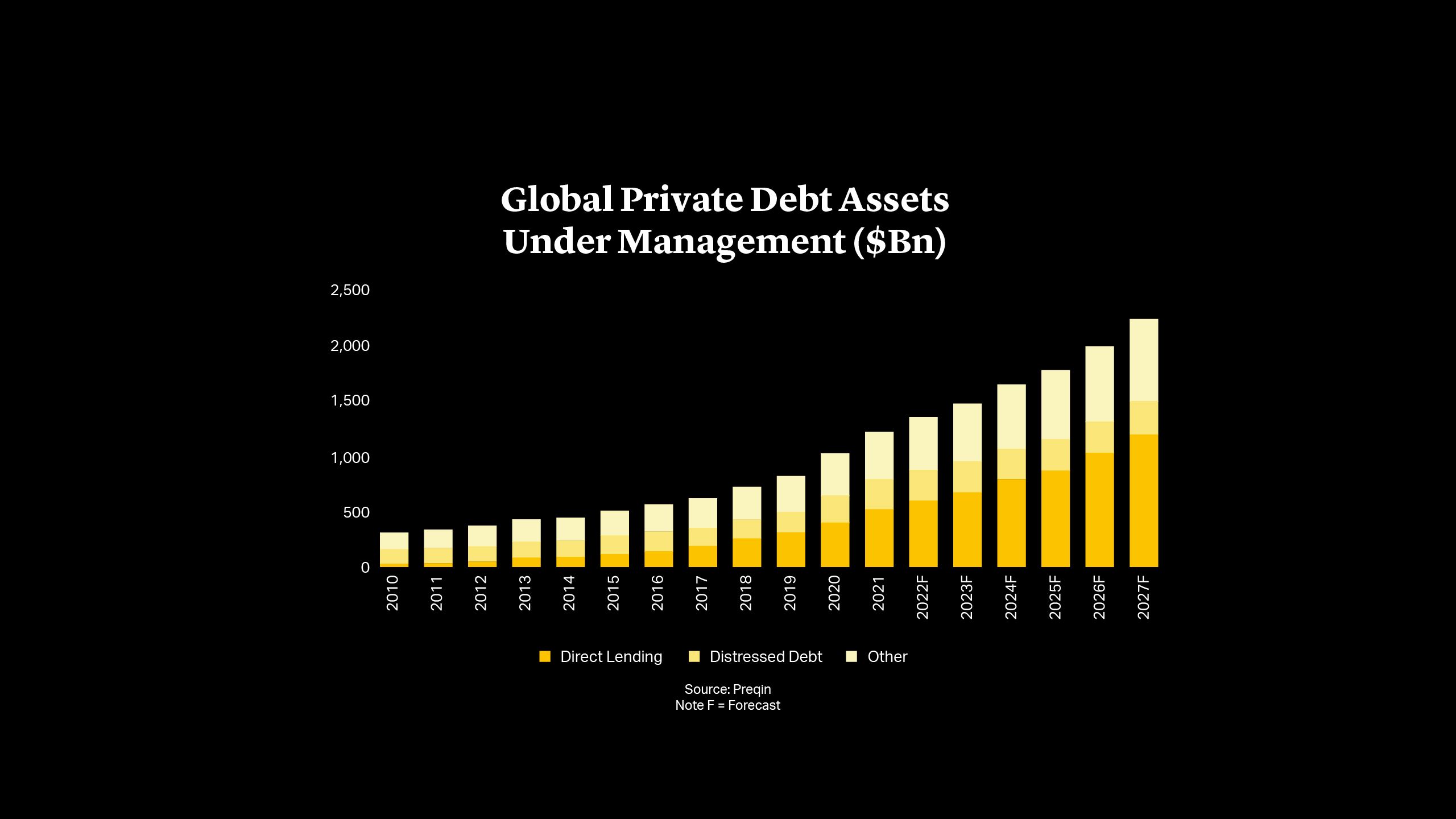

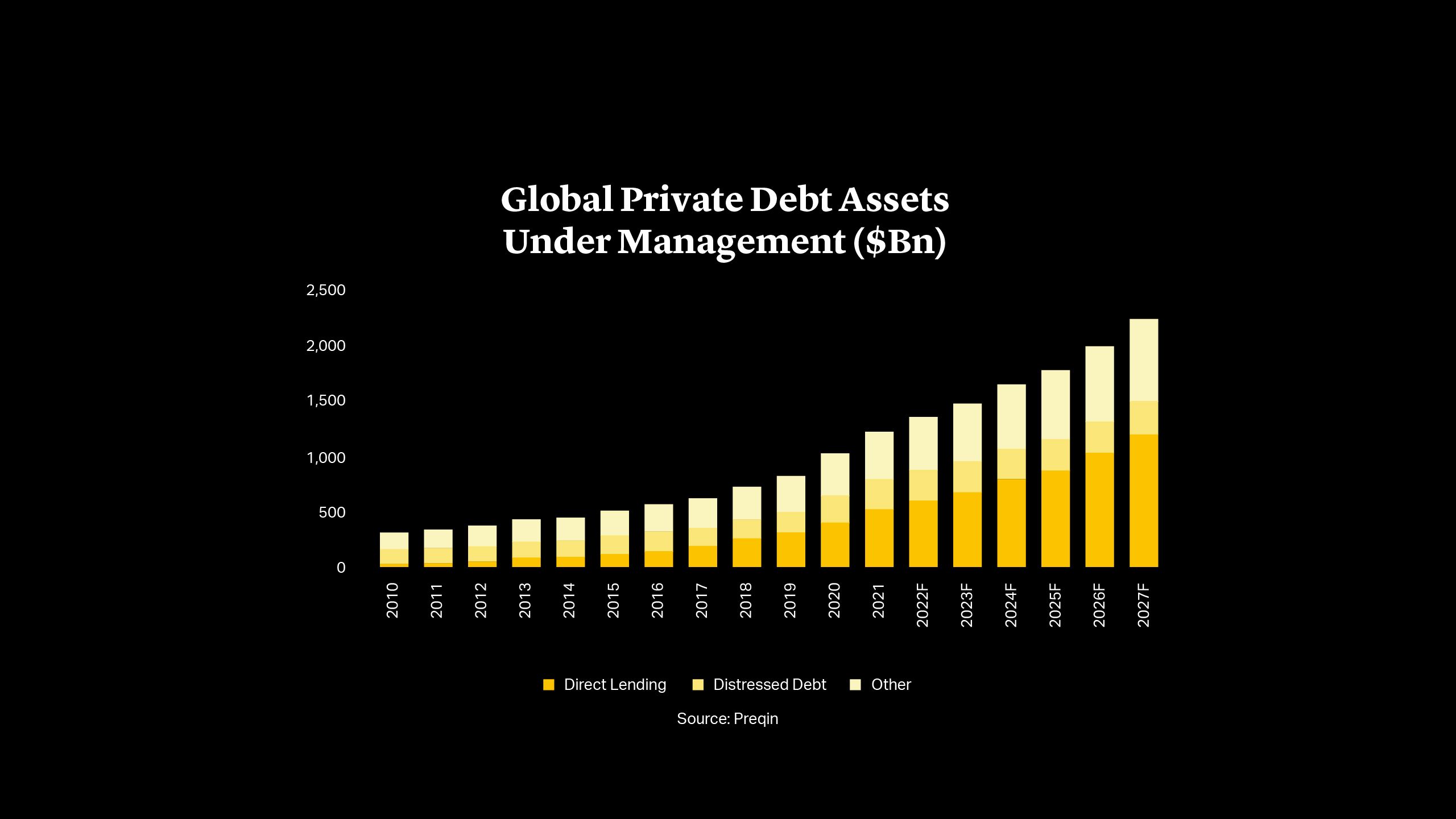

That demand is driving more capital into funds from existing players and encouraging new entrants into the space. CVC raised €6.3bn for its third European lending fund in December5, far above the €2bn it was reported to be targeting6. Meanwhile, Oaktree is said to be planning its entrance into the market, targeting a $10bn fund that could write cheques of $500mn or more for buyouts7. According to Preqin’s latest private debt report, fundraising for private debt hit $172bn by the end of the third quarter, comparing favorably to the asset class’s record 2021 when it raised $215bn. The overall market is expected to almost double to $2.3tn by 20278.

Investors Target More Capital at Private Debt Funds

Behind the surge in private lending for buyouts is equally strong appetite from institutional investors for the asset class, which is seen to offer attractive risk-adjusted returns and interest-rate-hedging capabilities as loans are typically structured with a floating rate. According to a 2022 survey of large institutional investors by advisory firm Rede Partners, 82% expected to increase exposure to private debt funds in the coming year compared with just 4% who expected to reduce allocations4.

That demand is driving more capital into funds from existing players and encouraging new entrants into the space. CVC raised €6.3bn for its third European lending fund in December5, far above the €2bn it was reported to be targeting6. Meanwhile, Oaktree is said to be planning its entrance into the market, targeting a $10bn fund that could write cheques of $500mn or more for buyouts7. According to Preqin’s latest private debt report, fundraising for private debt hit $172bn by the end of the third quarter, comparing favorably to the asset class’s record 2021 when it raised $215bn. The overall market is expected to almost double to $2.3tn by 20278.

Navigating Challenges and Conflicts in Private Debt

The growth in private debt means that large buyout firms are increasingly working with rival private capital firms on the lending side. In some instances, a firm may have interests in both the equity and debt side of the transaction. While this can create potential conflicts of interest in certain scenarios, for example in the event of a debt restructuring, these can be anticipated and managed in the deal terms.

Clear policies, planning and early agreement can head off any more difficult negotiations in incidences of restructuring, while increasing experience in the private debt industry is enabling funds to understand and avoid potential issues. That maturity is also leading to deeper relationships between debt funds and private equity firms, meaning that private debt will remain an attractive and flexible financing option for deals of all sizes even as more traditional lending recovers.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card