Private Equity Market Snapshot

June 2023

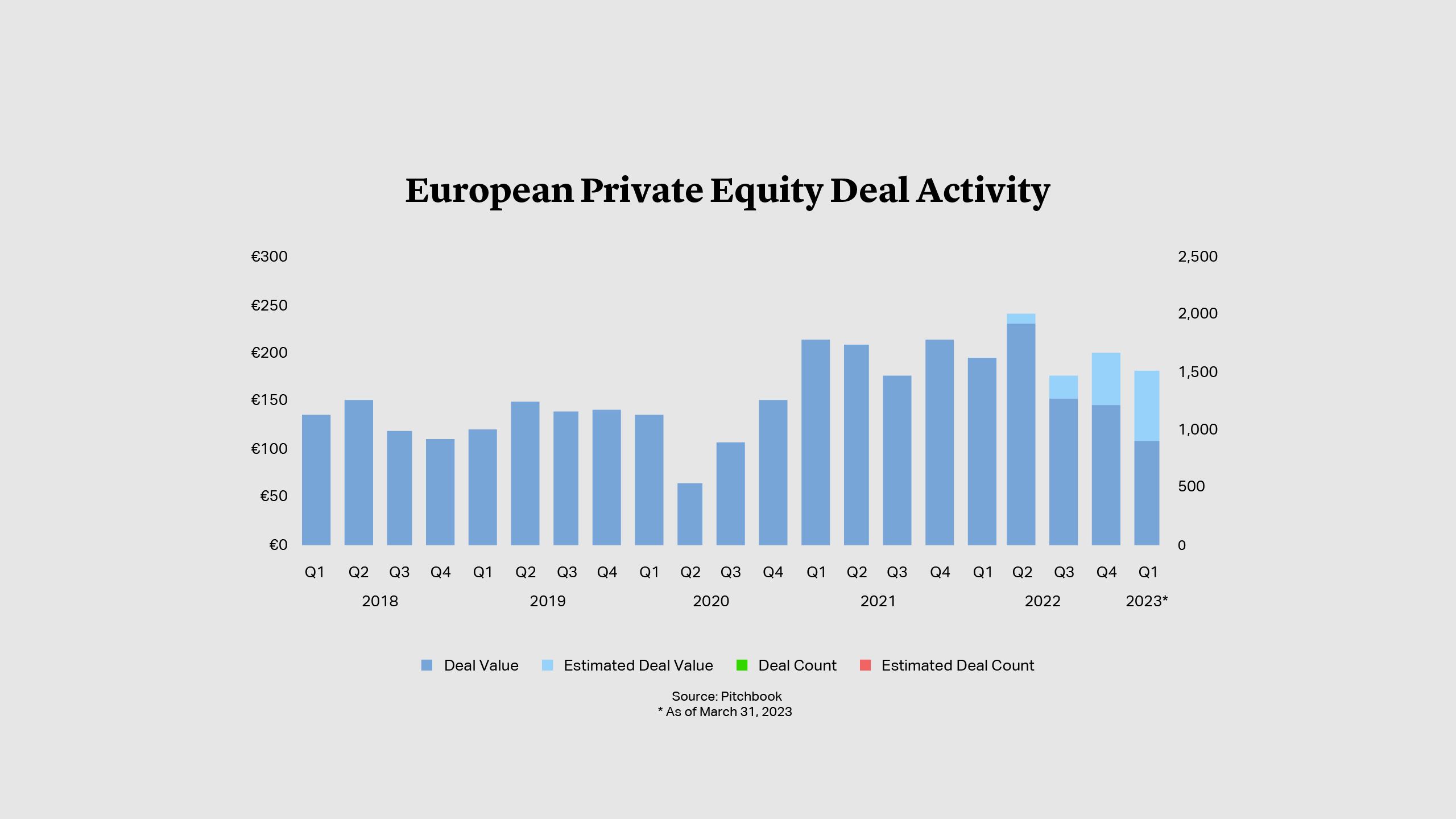

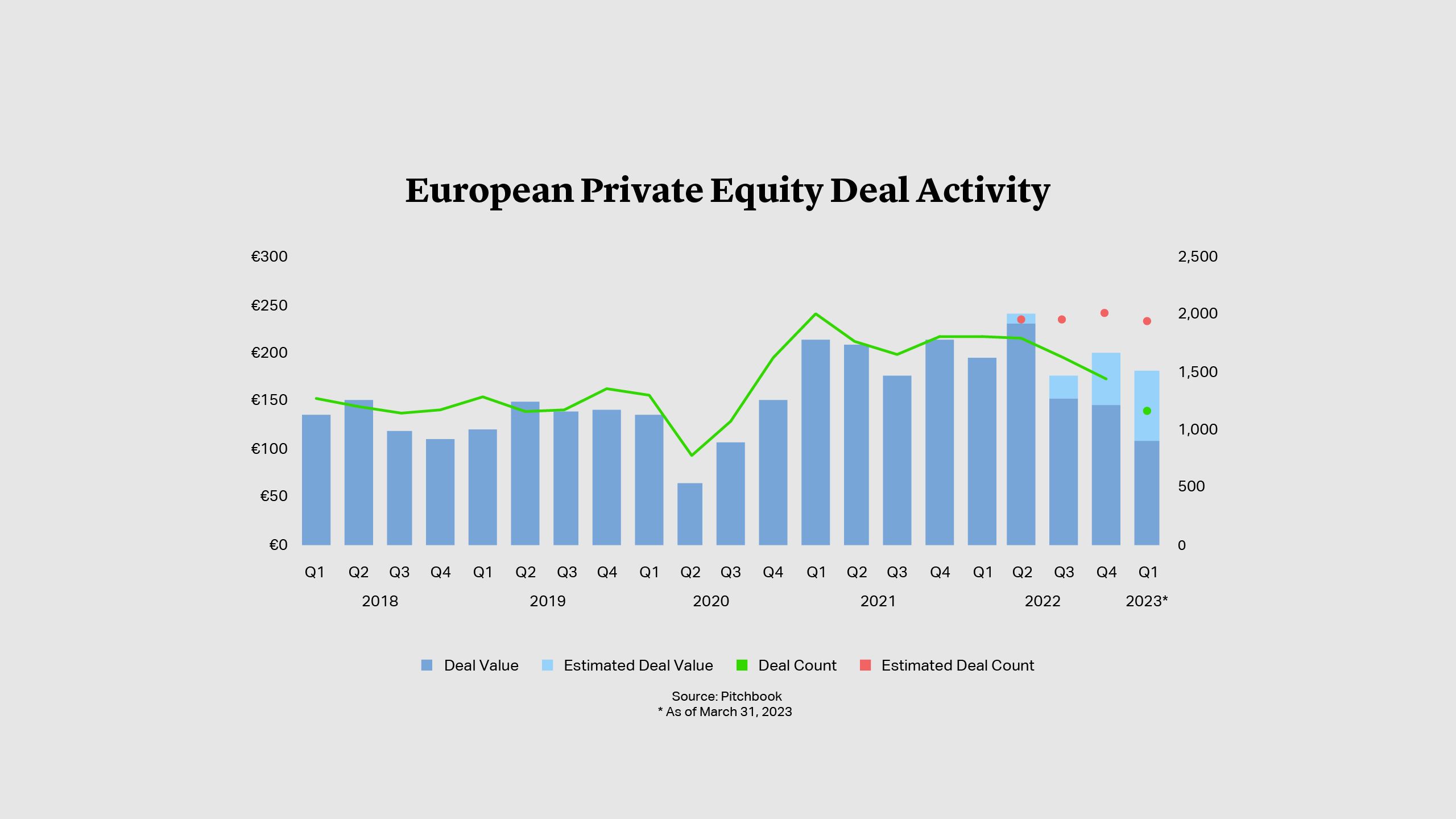

Market signals continue to be mixed. Data points to an ongoing slowdown in private equity activity. According to PitchBook, European private equity activity peaked in the second quarter of 2022 and was €182bn in the first quarter of 2023 – representing a 6.8% year-on-year decline1. Yet, at the same time, there are signs of improvement for high quality assets with some significant transactions agreed against a still-uncertain backdrop. On the upper end of the market, dealmaking was focused mostly on the tech/pharma sectors, where there was a smaller number of quality assets with strong pricing power2. In early June, an EQT-led consortium agreed an all-cash deal for listed veterinary pharma group Dechra at an enterprise value of £4.9bn, the UK’s largest buyout of the year so far3.

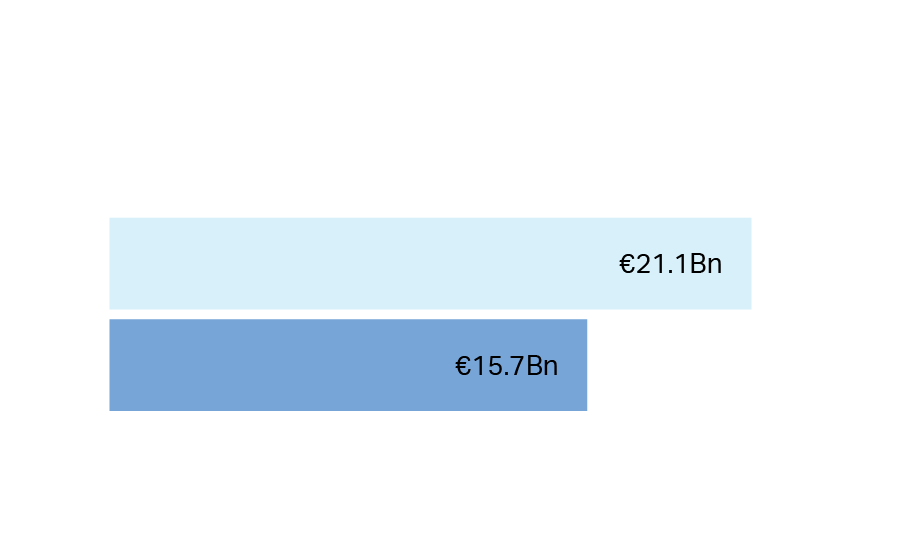

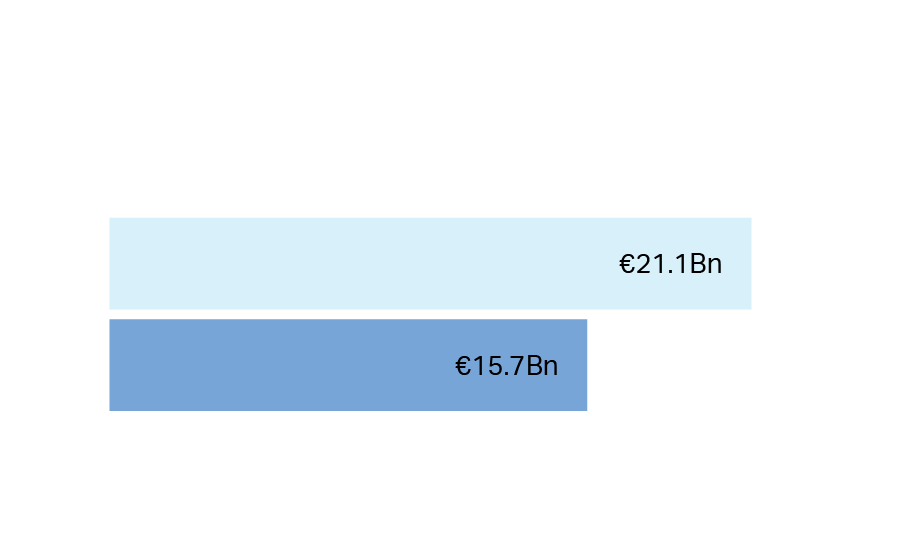

The cloud caused by the collapse of Silicon Valley Bank is dispersing, and investors are regaining a more positive outlook. However, there remain some hurdles to overcome, not least of all the availability and cost of financing. European leveraged loan issuance totaled €15.7bn in the first quarter, a 26% decline on the same period last year, according to Fitch Ratings research, with issuance related mainly to refinancing, as opposed to new buyouts4.

The cloud caused by the collapse of Silicon Valley Bank is dispersing, and investors are regaining a more positive outlook. However, there remain some hurdles to overcome, not least of all the availability and cost of financing. European leveraged loan issuance totaled €15.7bn in the first quarter, a 26% decline on the same period last year, according to Fitch Ratings research, with issuance related mainly to refinancing, as opposed to new buyouts4.

Sellers Begin to Accept Reduced Multiples

Persistent inflation across the UK and Europe increases the prospect of further interest rate rises, as well as rates staying higher for longer, squeezing the financing model for buyouts and, by extension, target returns. As conditions appear to be more entrenched, there is greater pressure for sellers to rein in their price expectations.

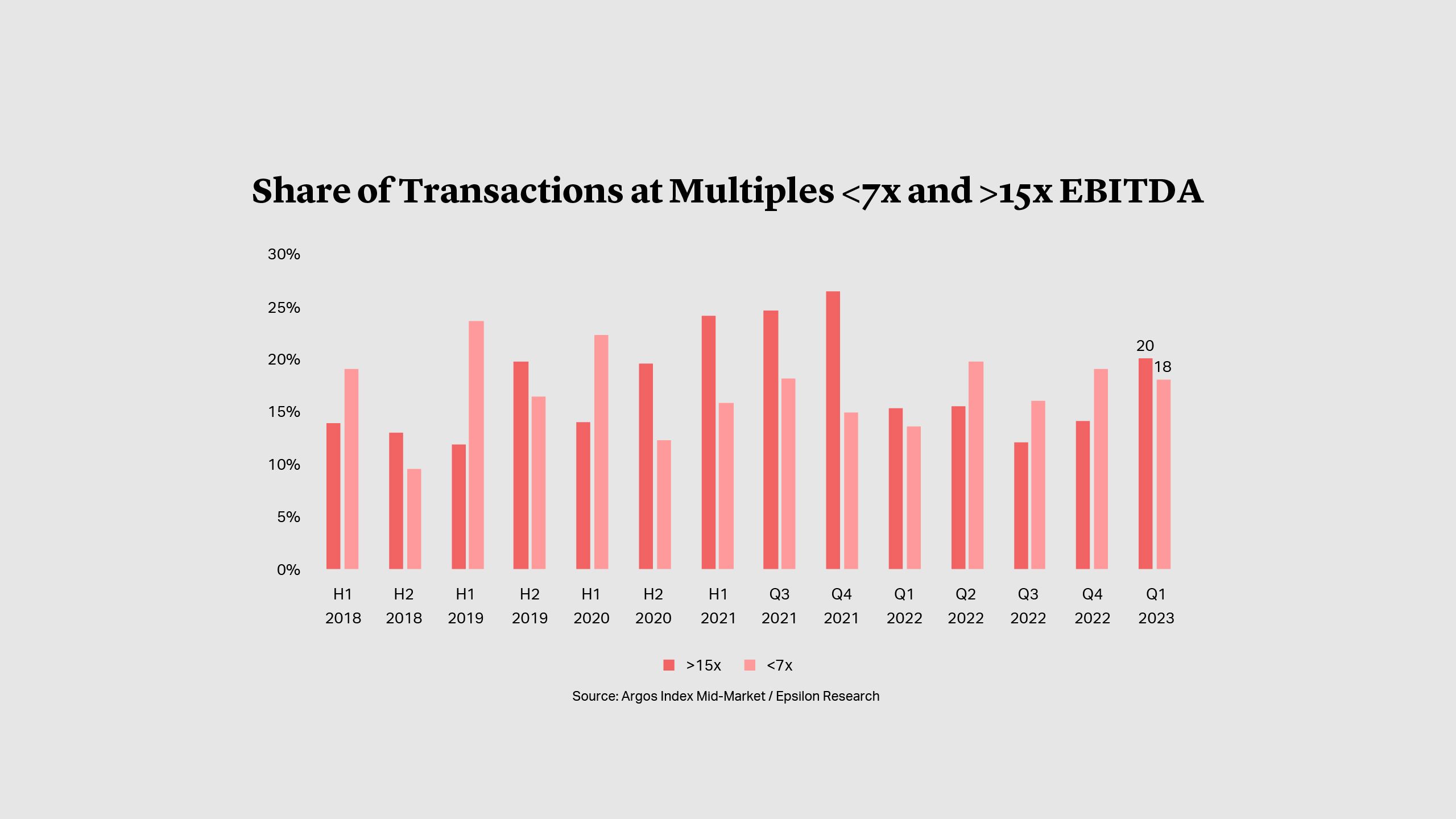

Rolling four-quarter purchase price multiples in Europe fell back from 14.6x EBITDA in the first quarter of 2022 to 11.2x in the fourth quarter of the year, according to the latest PitchBook data, marking a clear disconnect from U.S. pricing which remained more elevated5. The trend is clearly continuing in 2023, with lower pricing seen for smaller companies. Argos Wityu research shows that mid-market multiples dipped below 10x for the first time since 2020, reaching 9.7x EBITDA in the first quarter. That figure masks a wide divergence in pricing – perhaps consistent with the bifurcation in market activity between high quality assets and those with more mundane characteristics – with the market getting ever more polarized and the proportion of deals concluded at both less than 7x and more than 15x EBITDA increasing to represent to 38% of total investments6.

Take-Private Activity Decelerates Amid Persistent Inflation

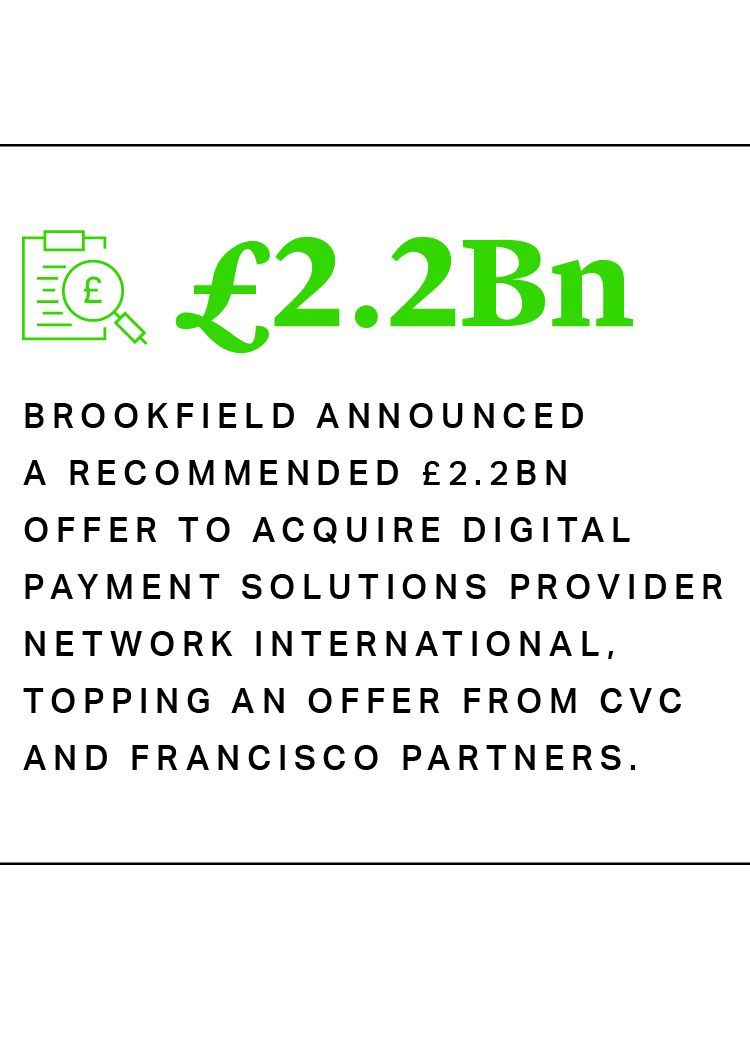

The disconnect between U.S. valuations and those in Europe – particularly the UK – has helped fuel a strong rekindling of appetite for take-private deals. U.S. firms Providence Equity and Searchlight Capital completed their acquisition of events management group Hyve in early June after having increased their offer price in the face of resistance from shareholders. In contrast, an EQT-led consortium's agreed offer for Dechra was pitched at a lower level than initially indicated, following a profit warning from the UK-listed company. Most recently, Brookfield announced a recommended £2.2bn offer to acquire digital payment solutions provider Network International, topping an offer from CVC and Francisco Partners.

Not all parties are able to reach agreement on price, however. After multiple approaches succeeded in opening the door to negotiations, Apollo ultimately walked away from engineering services company Wood Group in mid-May. The U.S. firm’s talks with online retail firm THG also ended after it was unable to meet the valuation expectations of the company7. Research from broker Peel Hunt showed that private equity firms started just six new offer periods in May, down from 13 in April, with inflation being a key factor among the concerns for prospective buyers8.

Take-Private Activity Decelerates Amid Persistent Inflation

The disconnect between U.S. valuations and those in Europe – particularly the UK – has helped fuel a strong rekindling of appetite for take-private deals. U.S. firms Providence Equity and Searchlight Capital completed their acquisition of events management group Hyve in early June after having increased their offer price in the face of resistance from shareholders. In contrast, an EQT-led consortium's agreed offer for Dechra was pitched at a lower level than initially indicated, following a profit warning from the UK-listed company. Most recently, Brookfield announced a recommended £2.2bn offer to acquire digital payment solutions provider Network International, topping an offer from CVC and Francisco Partners.

Not all parties are able to reach agreement on price, however. After multiple approaches succeeded in opening the door to negotiations, Apollo ultimately walked away from engineering services company Wood Group in mid-May. The U.S. firm’s talks with online retail firm THG also ended after it was unable to meet the valuation expectations of the company7. Research from broker Peel Hunt showed that private equity firms started just six new offer periods in May, down from 13 in April, with inflation being a key factor among the concerns for prospective buyers8.

High-Profile Sports Brands Remain Attractive but Hard to Pursue

Sports investments have remained high on private equity’s radar throughout the turbulence, with sponsors eyeing potential new revenue streams from big-name leagues and clubs. However, processes have illustrated the challenges of deals involving large numbers of interested parties, often with conflicting points of view. In May, a minority of German football clubs blocked a potential private equity investment for a 12.5% stake in the commercial and marketing rights for the Bundesliga, the second time such a deal has been tabled and rejected9.

Private equity parties also face fierce competition for the biggest brands from the world’s wealthiest individuals, as well as unconventional and protracted processes. Carlyle emerged as a suitor for Manchester United in April, reportedly offering to buy a minority stake in the football club from the U.S. Glazer family, whilst interest from British billionaire Jim Ratcliffe, founder of chemicals producer INEOS, was also in contention. However, in June Qatari royal Sheikh Jassim bin Hamad Al Thani was reported to have put forward a fifth and final offer, some eight months after the sale started. The offer, said to be pitched at no more than £6bn, was the only one for outright ownership of the club and also promised to pay off some £1bn of debt10.

Investing in ESG and Energy Transition

Private equity firms are also increasingly positioning themselves for even greater investment in the energy transition sector. Earlier this year, EQT set the hard cap for its sixth infrastructure fund at €21bn, and in late May announced the appointment of former Enel CEO Francesco Starace as partner. In his time as CEO of the Italian utility, Starace oversaw the company’s efforts to exit fossil-fuel energy production and focus on renewable energy production11.

We also see strong appetite for life sciences investments, and continued development in Europe as a hub for the sector. Following the sale of its cell and gene therapy solutions business Polyplus in April at a record return of 300x12, French firm ArchiMed announced the closing of its MED Platform II fund for €3.5bn at the start of June, far ahead of its €2bn target.

After a year of false dawns and ongoing uncertainty, it continues to be difficult to predict private equity deal activity in the second half of 2023. There does seem to be a slight improvement in sentiment but whether that translates into a genuinely brighter outlook in the near-term, particularly in the face of headwinds around core inflation and the continued monetary policy response, remains to be seen. Deal activity seems likely to show some positive momentum - but that activity may well be dominated by high quality assets, with deal volumes more generally remaining thinner than hoped.

Ian Shawyer

Partner

London

T: +44 20 7614 2242

ishawyer@cgsh.com

V-Card

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card

Ed Aldred

Partner

London

T: +44 20 7614 2302

ealdred@cgsh.com

V-Card