GPs Stick to Fundraising Terms in Challenging Markets

Private equity firms, investors and their advisers gathered in Berlin in early June to take the industry’s pulse and discuss the outlook. As on many occasions in the past, the mood was mixed, and the fundraising environment was high on the agenda. Gabriel Caillaux, Head of EMEA for General Atlantic, said the industry was enduring the toughest fundraising conditions in a decade, while EQT CEO Christian Sinding warned that consolidation could be on the horizon for alternatives managers, in part due to the challenges GPs face in raising capital.

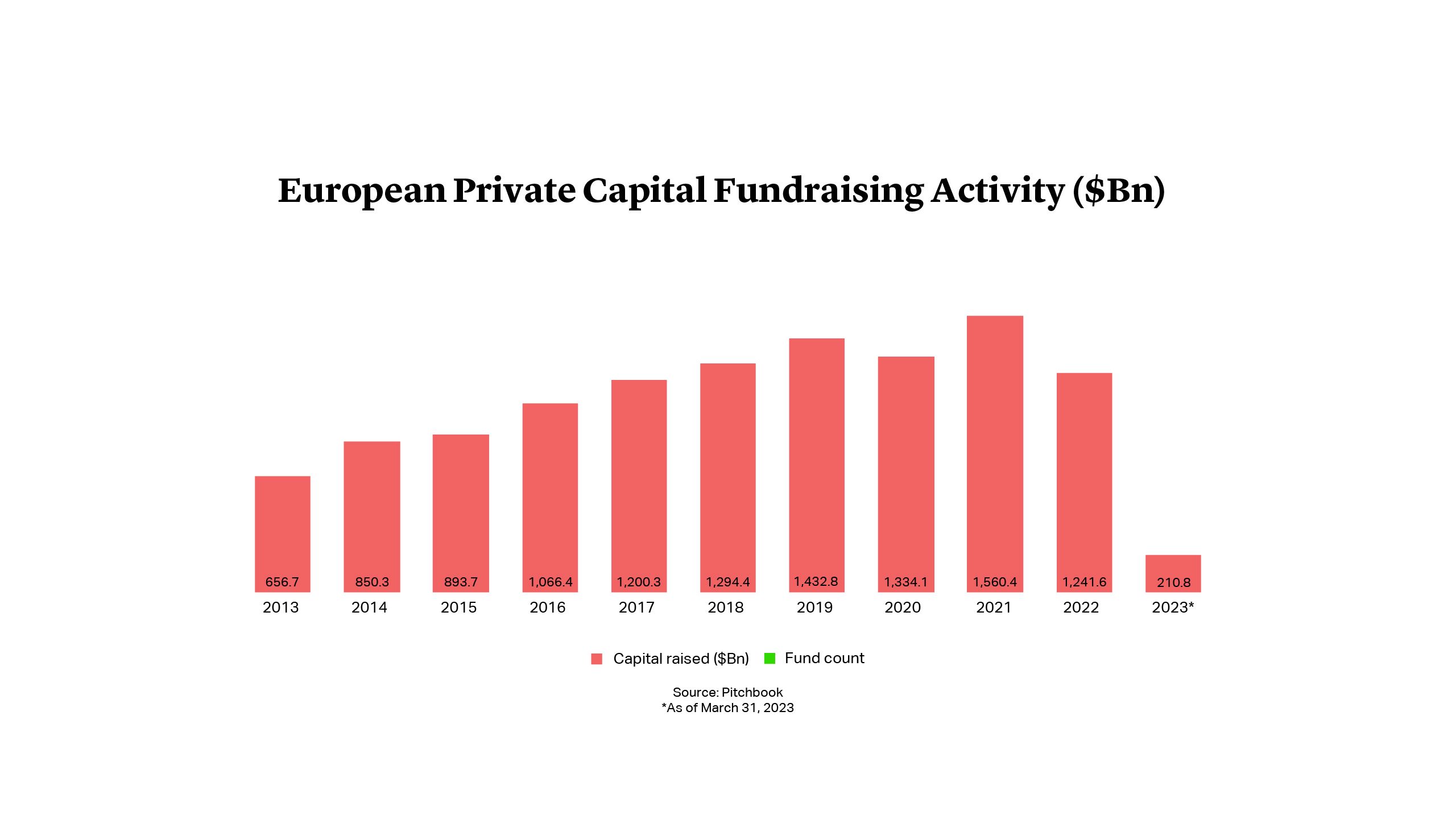

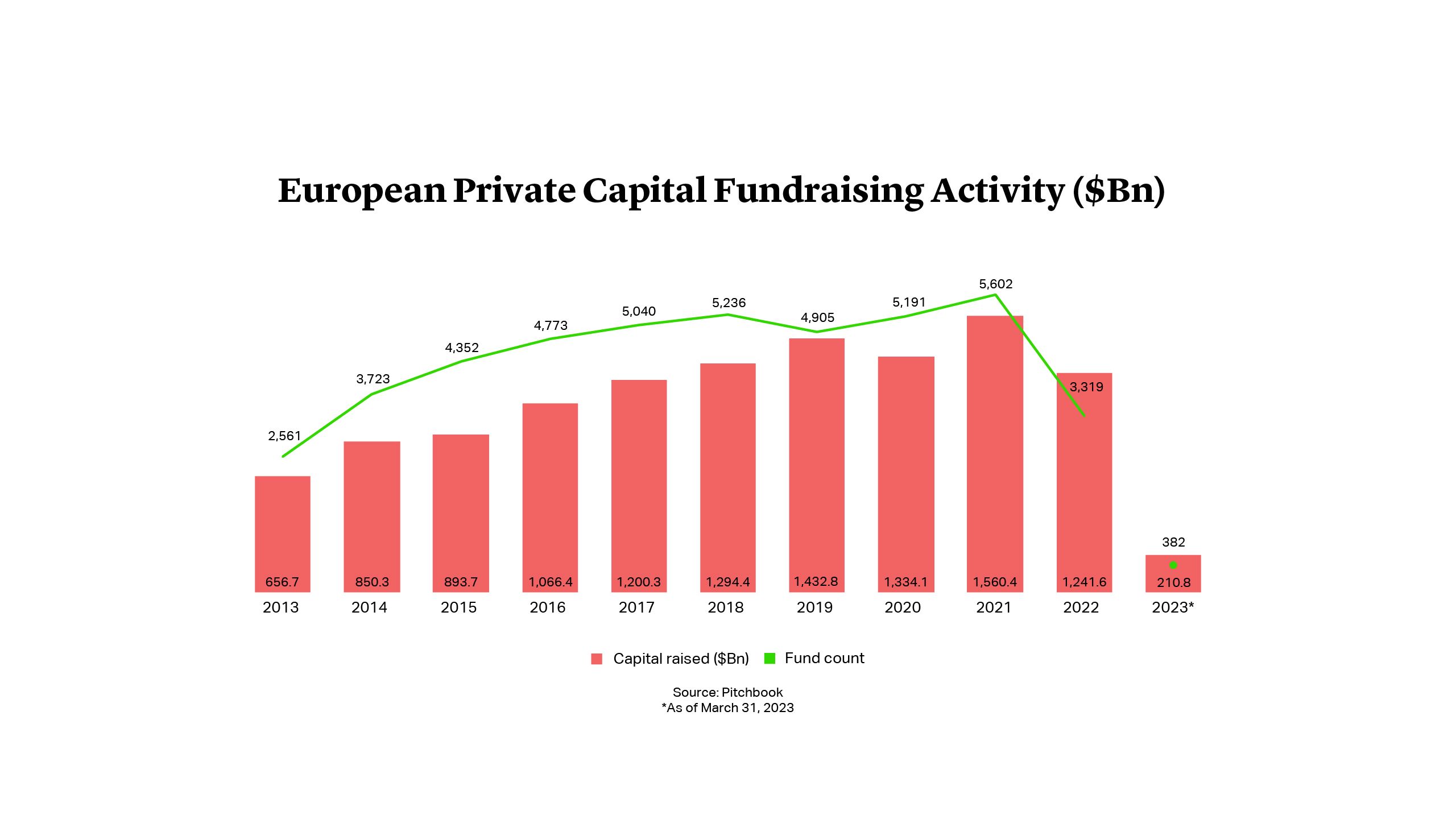

Weakness in the fundraising environment has prompted some to speculate that it has led to a shift in the balance of power between GPs and LPs, with investors in the ascendancy. Yet not all data points to a fundraising crunch for firms. According to Invest Europe, all private equity fundraising on an incremental basis (as opposed to final closes) reached a new record at €170bn in 2022, some 30% above the prior record of 20211.

The reality is more complex than the data suggests with a bifurcation in conditions. Top-tier firms and those with long track records continue to raise capital and maintain robust terms. However, newer managers, or in certain managers, raising new capital as part of a diversification of strategies are facing hard-to-resist pressure, and seeing a shift in fund terms.

Private equity firms, investors and their advisers gathered in Berlin in early June to take the industry’s pulse and discuss the outlook. As on many occasions in the past, the mood was mixed, and the fundraising environment was high on the agenda. Gabriel Caillaux, Head of EMEA for General Atlantic, said the industry was enduring the toughest fundraising conditions in a decade, while EQT CEO Christian Sinding warned that consolidation could be on the horizon for alternatives managers, in part due to the challenges GPs face in raising capital.

Weakness in the fundraising environment has prompted some to speculate that it has led to a shift in the balance of power between GPs and LPs, with investors in the ascendancy. Yet not all data points to a fundraising crunch for firms. According to Invest Europe, all private equity fundraising on an incremental basis (as opposed to final closes) reached a new record at €170bn in 2022, some 30% above the prior record of 20211.

The reality is more complex than the data suggests with a bifurcation in conditions. Top-tier firms and those with long track records continue to raise capital and maintain robust terms. However, newer managers, or in certain managers, raising new capital as part of a diversification of strategies are facing hard-to-resist pressure, and seeing a shift in fund terms.

Top-Tier Private Equity Firms Hit Hard Caps

The weakening in fundraising has been noted by some of the largest and longest-standing in the industry. Carlyle Group and Apollo have been among the names to warn of a slowdown in fundraising, resulting in lower targets, and/or prolonged fundraising periods2. However, many firms – including those with a focus on Europe – have continued not only to reach targets, but also hard caps.

In January, Dutch firm Waterland announced the final close on its ninth flagship fund at €3.5bn, and also unveiled a €500mn fund to take minority stakes in subsequently-exited Waterland companies3. Similarly, the following month, Boston-based Summit Partners announced that its oversubscribed fourth European growth fund achieved its hard cap at €1.4bn4.

The CEO of the Institutional Limited Partners Association, Jennifer Choi, commented to Institutional Investor that there has not been a “wholesale shift in favor of the LP in any notable way in terms of any specific terms”5.

From our experience, neither fund terms nor fees have shifted materially towards investors. Indeed, large or top-tier funds appear to be holding their positions in LP negotiations, which has been in part responsible for their recent fundraising hiatus.

Top-Tier Private Equity Firms Hit Hard Caps

The weakening in fundraising has been noted by some of the largest and longest-standing in the industry. Carlyle Group and Apollo have been among the names to warn of a slowdown in fundraising, resulting in lower targets, and/or prolonged fundraising periods2. However, many firms – including those with a focus on Europe – have continued not only to reach targets, but also hard caps.

In January, Dutch firm Waterland announced the final close on its ninth flagship fund at €3.5bn, and also unveiled a €500mn fund to take minority stakes in subsequently-exited Waterland companies3. Similarly, the following month, Boston-based Summit Partners announced that its oversubscribed fourth European growth fund achieved its hard cap at €1.4bn4.

The CEO of the Institutional Limited Partners Association, Jennifer Choi, commented to Institutional Investor that there has not been a “wholesale shift in favor of the LP in any notable way in terms of any specific terms”5.

From our experience, neither fund terms nor fees have shifted materially towards investors. Indeed, large or top-tier funds appear to be holding their positions in LP negotiations, which has been in part responsible for their recent fundraising hiatus.

Pressure on Emerging Managers Intensifies

First-time managers or those raising capital around new or ancillary strategies have seen a certain amount of pushback from LPs, with large institutional investors looking to dictate the terms on which they are prepared to invest. In addition to the usual fee pressure, we have been seeing a step-up in demands for enhanced measures to remove underperforming managers:

No-Fault Removal

In certain cases, investors have succeeded in lowering the threshold to remove managers without cause, a step that typically requires the agreement of at least 75% of LPs. Some terms also include the ability to appoint new managers alongside the existing managers.

For-Cause Events

Historically reserved for the most serious events, such as fraud, in some instances such clauses have been extended to include the removal of managers for more minor issues, including any breach of LPA terms or side letters.

Such terms, even if not resulting in the removal of managers, can have severe financial implications for sponsors, leading to carried interest haircuts, or the return of carry and management fees to investors.

The leverage of LPs is most prevalent when they appear aligned around certain issues. While negotiations are bilateral and confidential, in practice a number of institutional investors in any fundraise are increasingly focused on the same key issues and can create overwhelming commercial pressure.

Signs of Improvement on the Horizon for Fundraising Market

Pressure among LPs to deploy capital and strong returns in private markets have been significant drivers for renewed investment appetite. Neuberger Berman analysis suggests that buyout valuations may already be rebounding from a shallow downturn6.

We see signs of the challenges in the PE fund raising market easing (particularly for GPs with scale investing funds with a very clear focus and a long track record of high performance), with a number of managers aiming to hold first and interim closes on capital that has been recently committed. This demand could receive a further boost as the denominator effect eases thanks to a rebound in listed equity valuations – the S&P 500 is up almost 11% since March, while the Stoxx 600 has added some 5.5% over the same period.

Any improvement in conditions could help break the deadlock between GPs and LPs on stalled fundraisings. While investor pressure will continue on a case-by-case issue, industry-wide terms are unlikely to shift far from the current status quo.

Ian Shawyer

Partner

London

T: +44 20 7614 2242

ishawyer@cgsh.com

V-Card

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card

Ed Aldred

Partner

London

T: +44 20 7614 2302

ealdred@cgsh.com

V-Card