Private Equity

Market Snapshot

February 2023

M&A markets continued their tentative thaw in early 2023, albeit with prospective buyers’ eyes firmly fixed on the uncertain economic outlook ahead.

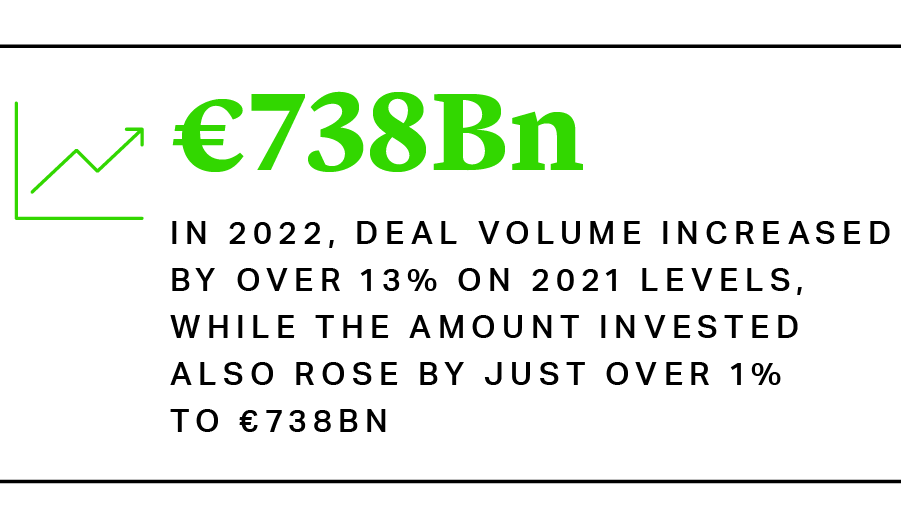

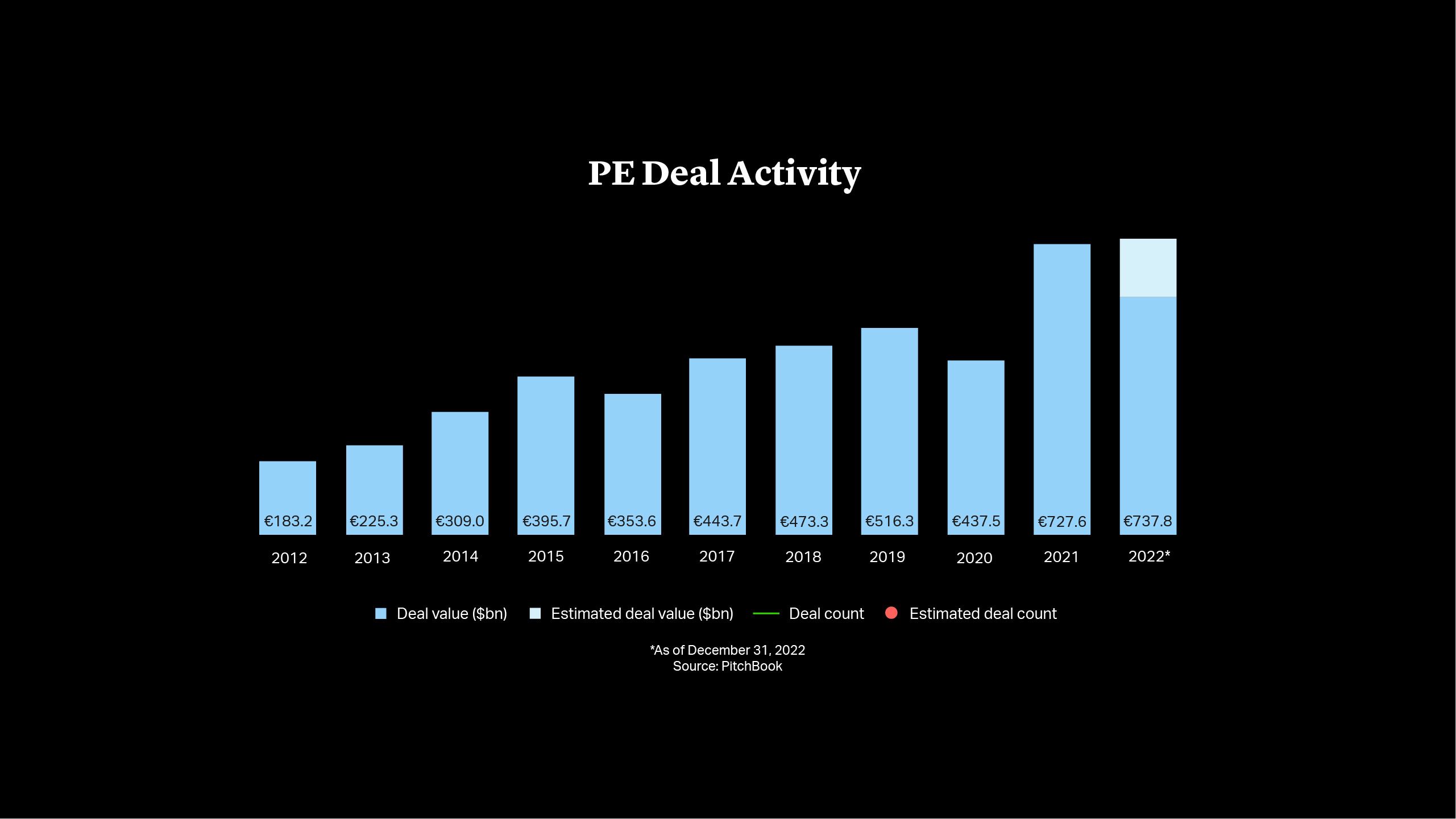

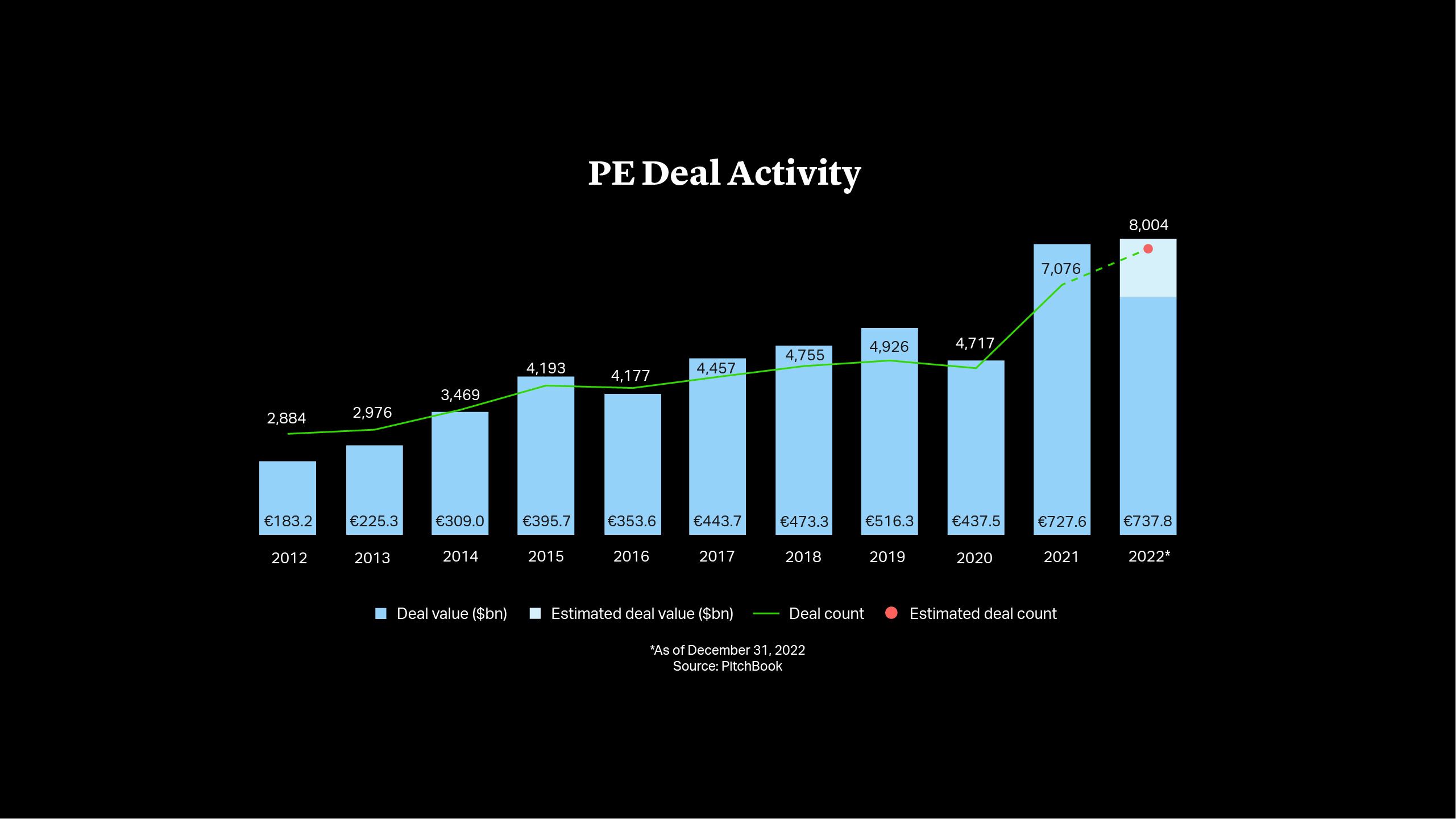

Data shows that private equity investment in Europe for 2022 was far more positive than many had expected. Deal volume increased by over 13% on 2021 levels, while the amount invested also rose by just over 1% to €738bn, a new record, according to PitchBook data1. However, the headline figures do mask signs of slowdown in primary buyout activity as around two thirds of the capital went into bolt-on investments, while mega buyout transactions (defined as those larger than €1bn) more than halved.

Markets Watch for

Recovery Signals

The deceleration in U.S. interest rate rises at the start of February is leading to expectations that other regions, notably the Eurozone and the UK, could follow suit. Although the region’s central banks have lagged their U.S. peer in tightening monetary policy, inflation shows similar signs of coming under control, resulting in a degree of renewed buoyancy across markets.

GDP data showed that the Eurozone grew modestly in the fourth quarter of 2022, despite a moderate contraction in Germany and Italy. The UK is lagging its neighbors in growth terms, but nonetheless saw the FTSE 100 hit an all-time high in early February. Many investors appear to believe that economic weakness is already reflected in share prices, while the index’s concentration of global companies focused on energy, mining or financials may mean it is poised to outperform2.

Other global factors are giving confidence a boost, notably signs of strength in the U.S. economy and the reopening of China following the relaxation of its zero-COVID policy, a move with potential positive repercussions for supply chains, demand and global growth.

Debt Market Constrictions Ease

Financing for mega buyouts remains difficult in Europe. Presenting the firm’s 2022 results, EQT CEO Christian Sinding warned of “substantially slower” investment3, but he did point to a recovery in debt markets that could facilitate financing for deals of up to €3bn, while also noting growing appetite for IPOs4.

According to reports, European banks have reduced the volume of unsold loans on their books to €5bn from around €15bn in the third quarter of 20225. This, combined with a greater degree of confidence in the interest rate outlook and overall economic conditions, may lead to a recovery in activity, particularly in the second half of 2023.

In the meantime, private equity firms continue to explore alternative strategies to side step uncertainty in debt markets. Among them are “portable capital structures,” which allow sponsors to acquire large stakes in targets, or even make full buyouts, without the need to pay off and refinance existing debt6. Other deals are being structured to avoid triggering change of control clauses in existing financial packages as sponsors bring in peers to buy minority stakes in a business.

UK Public-to-Privates

Remain in Focus

As noted above, UK-listed company share prices have surged to new highs in the face of macro data that points to deteriorating economic conditions. Sterling has also staged a recovery against the dollar, rising more than 10% since September 2022 lows.

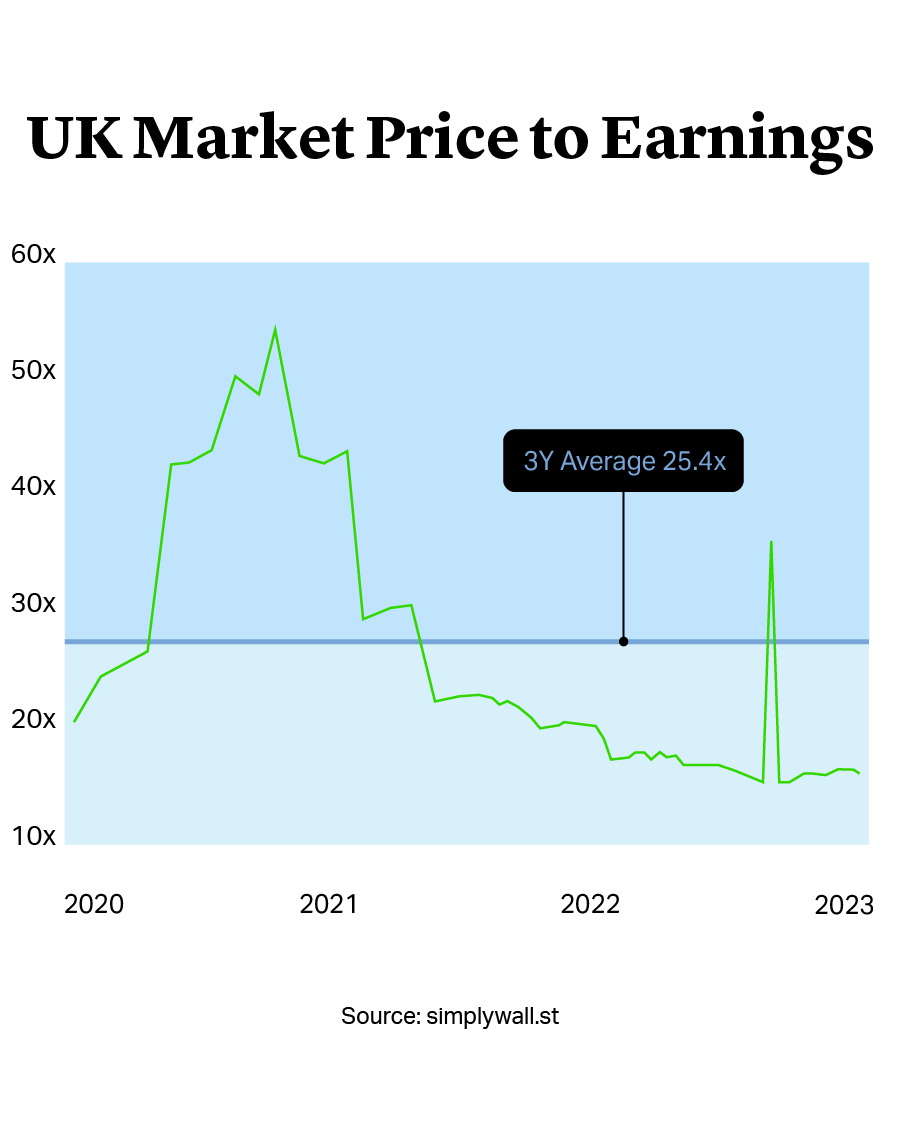

However, potential investors still see significant value in the UK market. Equities analysts highlight price-to-earnings ratios that are significantly lower than for companies in other geographies, in addition to being well below historical averages7. At the same time, prospective buyers are identifying UK-based companies that are less susceptible to the domestic economy and more exposed to diversified international demand, across sectors including healthcare, technology and industrials.

The continuing thaw in debt markets is likely to release renewed interest in public-to-private transactions in the UK and across Europe. Following its attempt to take over Italy’s Telecom Italia last year, KKR is continuing to court the indebted telecoms group and in February made an offer to carve out and take over its fixed-line business8. The approach also highlights potential opportunities to execute more complex transactions that stem from rising company stress and distress in the rising interest rate environment.

ESG Driving and Defining Deals

Rising regulatory and investor focus on ESG is having an ever more important impact on private equity and venture capital deals. Some 80% of fund managers see questions on ESG incorporated into due diligence questionnaires for portfolio company exits, according to a survey from consultancy KEY ESG, reflecting ever greater interest in ESG performance from both corporates and private equity buyers9.

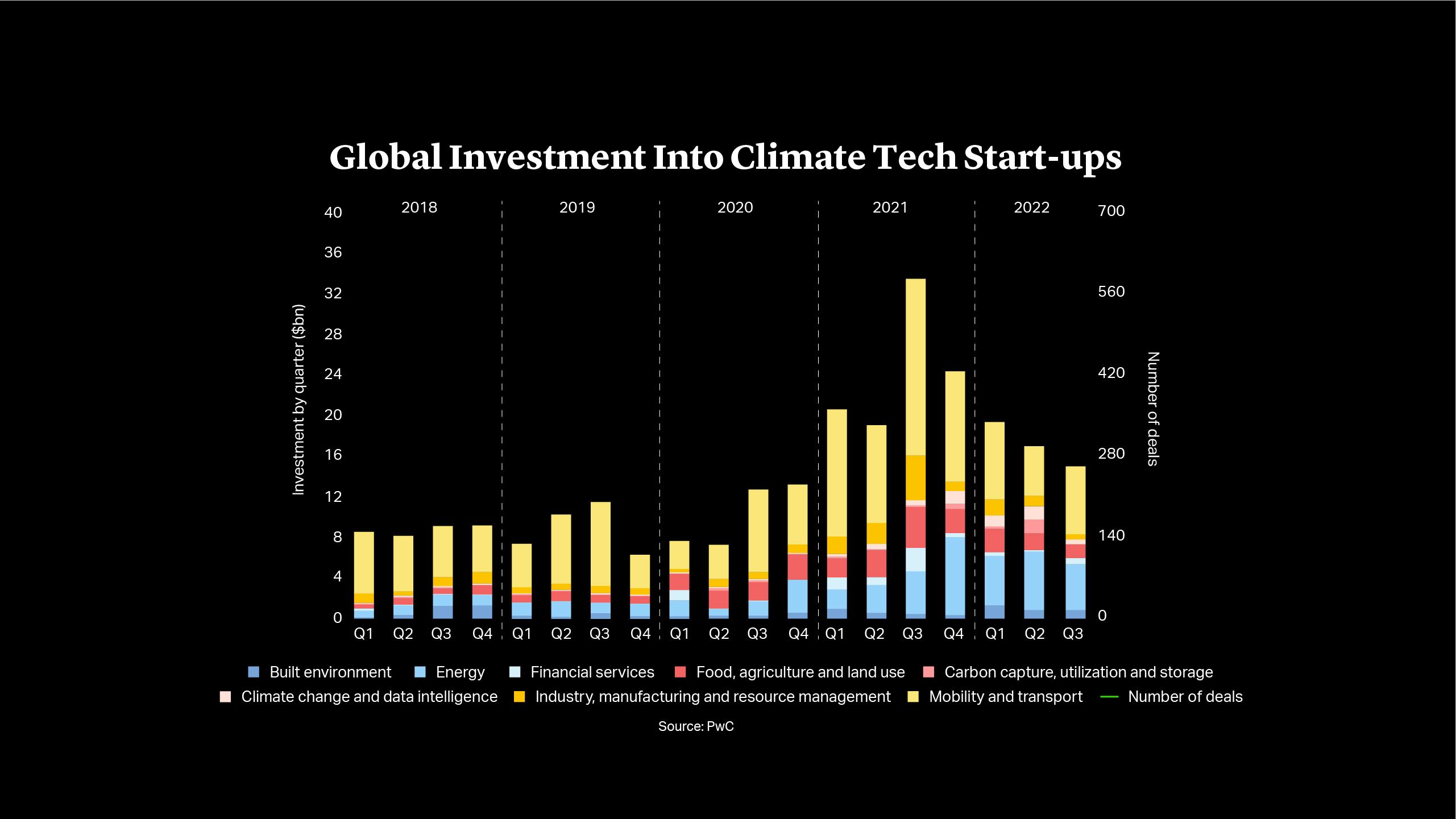

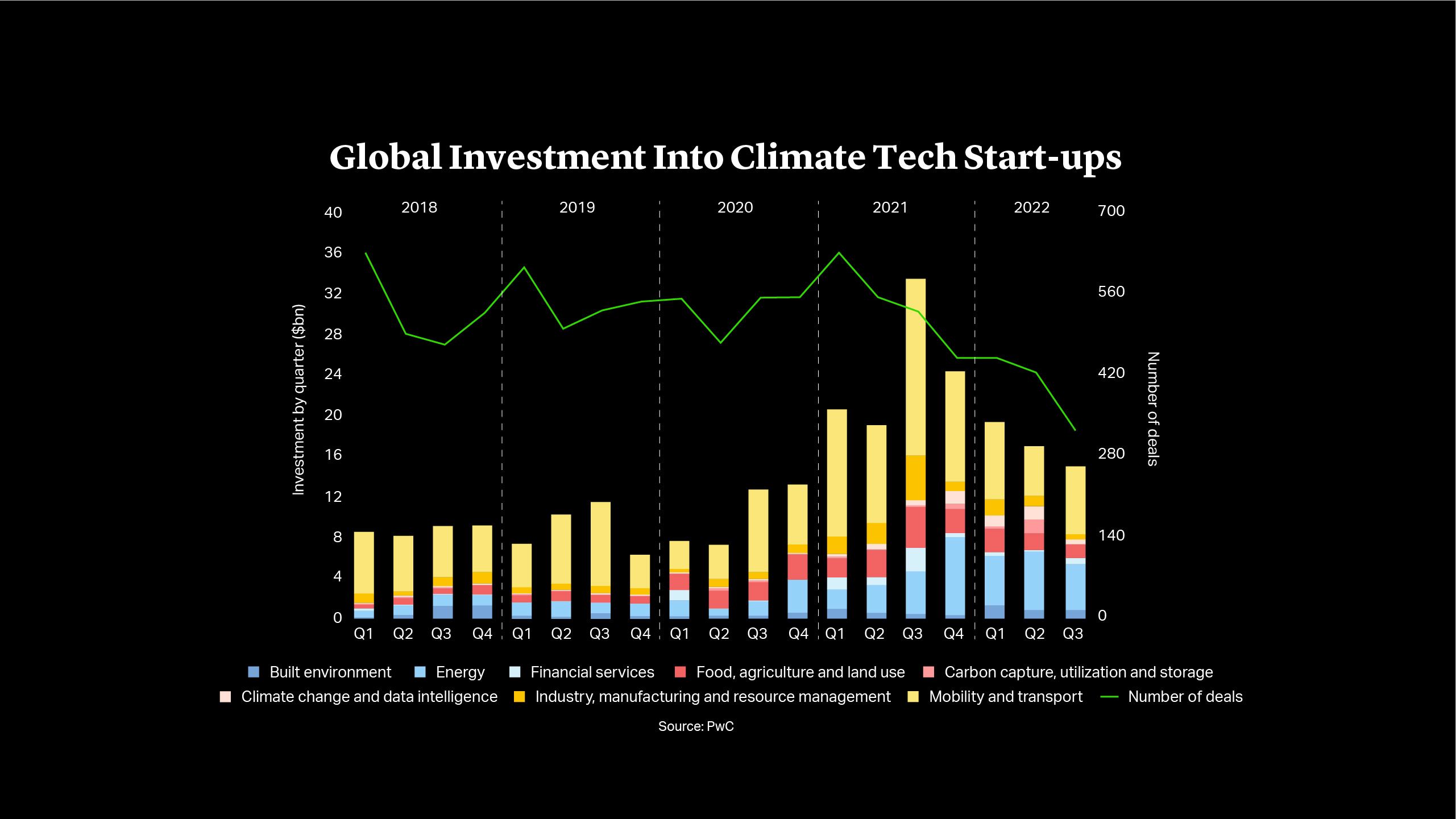

At the same time, investors are highly focused on deals with strong sustainability credentials. A great example of this is Blackstone’s acquisition of a majority stake in Emerson’s Climate Technologies in Q4 last year. According to data from PwC, venture investment in climate tech accounted for over a quarter of all investment in 2022, with quarterly investment in the range of $15-20bn throughout the year10.

Momentum has continued with Berlin-based solar start-up Enpal raising €215mn in a January funding round led by the TPG Rise Climate fund that valued the business at €2.2bn. The sector is likely to see even stronger investment in 2023 as the EU targets subsidies and tax credits for green businesses in an attempt to compete with the U.S. Inflation Reduction Act11.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card