Consortium Deals Provide Options for Private Equity in Challenging Market

Consortium investments became a mainstay of buoyant pre- and post-COVID-19 markets by allowing private equity buyers to team up with peers to broach investments stretching into the double-digit billions. Such structures are now showing their value in a deteriorating environment, as sponsors seek ways to de-risk smaller investments and remain competitive in challenging financing markets. Alongside fellow private equity firms, sponsors are finding willing co-investors and co-sponsors in large cash-rich sovereign wealth funds, particularly from the Middle East.

Consortia Drive Ever Larger Investments in Europe

In the run up to the pandemic, consortium deals in Europe hit new heights as private equity firms joined forces to pursue ever larger targets. In early 2020, Advent International and Cinven teamed up with German foundation RAG-Stiftung and one of the largest Middle Eastern sovereign wealth funds to buy Thyssenkrupp’s elevators business for some €17bn, one of Europe’s largest ever private equity deals.

After the sharp shock of COVID-19, large club deals came back with a raft of investments in Europe and the U.S., including Blackstone, the Carlyle Group and Hellman & Friedman’s $34bn purchase of U.S. healthcare company Medline with the same Middle Eastern sovereign wealth fund. That recent high-water mark could be eclipsed should Blackstone and the Benetton family’s €54bn takeover of listed Italian infrastructure group Atlantia go ahead, following recent regulatory approvals.

Megadeals Constrained but Consortia Pursue Smaller Investments

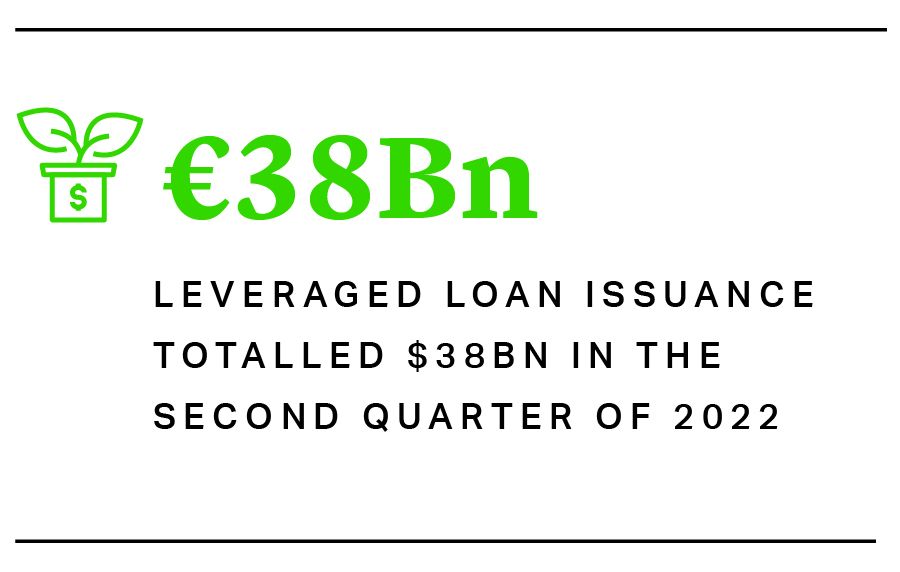

While private equity firms still have substantial dry powder to deploy, deteriorating macroeconomic conditions – particularly in debt markets – are weighing on their ability to conclude deals. Leveraged loan issuance totalled €38bn in the second quarter of 2022, according to the Association for Financial Markets Europe, decelerating from the first quarter and down 48% on the same period last year1. At the same time, many large institutions are facing allocation pressures that are constraining their investment in private equity funds and assets.

To contend with the anticipated short-term disruption, some private equity firms are pursuing all equity funding, in the hope of raising debt or syndicating equity when markets improve. Others are turning to club deals for relatively small cheques to de-risk investments and share the equity requirement. In October, JP Morgan’s private equity arm One Equity teamed up with UK firm Buckthorn Partners to buy British construction group Amey from Ferrovial for £400mn, in a deal that included a loan from the seller2. The following month, Swedish vehicle glass repair firm Cary Group returned to private hands after accepting a £670mn (SEK9.2bn) offer from CVC and Nordic Capital3.

Megadeals Constrained but Consortia Pursue Smaller Investments

While private equity firms still have substantial dry powder to deploy, deteriorating macroeconomic conditions – particularly in debt markets – are weighing on their ability to conclude deals. Leveraged loan issuance totalled €38bn in the second quarter of 2022, according to the Association for Financial Markets Europe, decelerating from the first quarter and down 48% on the same period last year1. At the same time, many large institutions are facing allocation pressures that are constraining their investment in private equity funds and assets.

To contend with the anticipated short-term disruption, some private equity firms are pursuing all equity funding, in the hope of raising debt or syndicating equity when markets improve. Others are turning to club deals for relatively small cheques to de-risk investments and share the equity requirement. In October, JP Morgan’s private equity arm One Equity teamed up with UK firm Buckthorn Partners to buy British construction group Amey from Ferrovial for £400mn, in a deal that included a loan from the seller2. The following month, Swedish vehicle glass repair firm Cary Group returned to private hands after accepting a £670mn (SEK9.2bn) offer from CVC and Nordic Capital3.

Middle East Funds Target New Investments

While many investors are being squeezed by falling portfolio valuations and reduced distributions, other large investors are actively looking for opportunities. Middle East funds, buoyed by rising oil revenues and the strong dollar, are eyeing international markets. Royal Group, an investment firm controlled by a top Abu Dhabi royal, plans to invest up to $10bn into U.S. and European assets hit by fears of a global recession4.

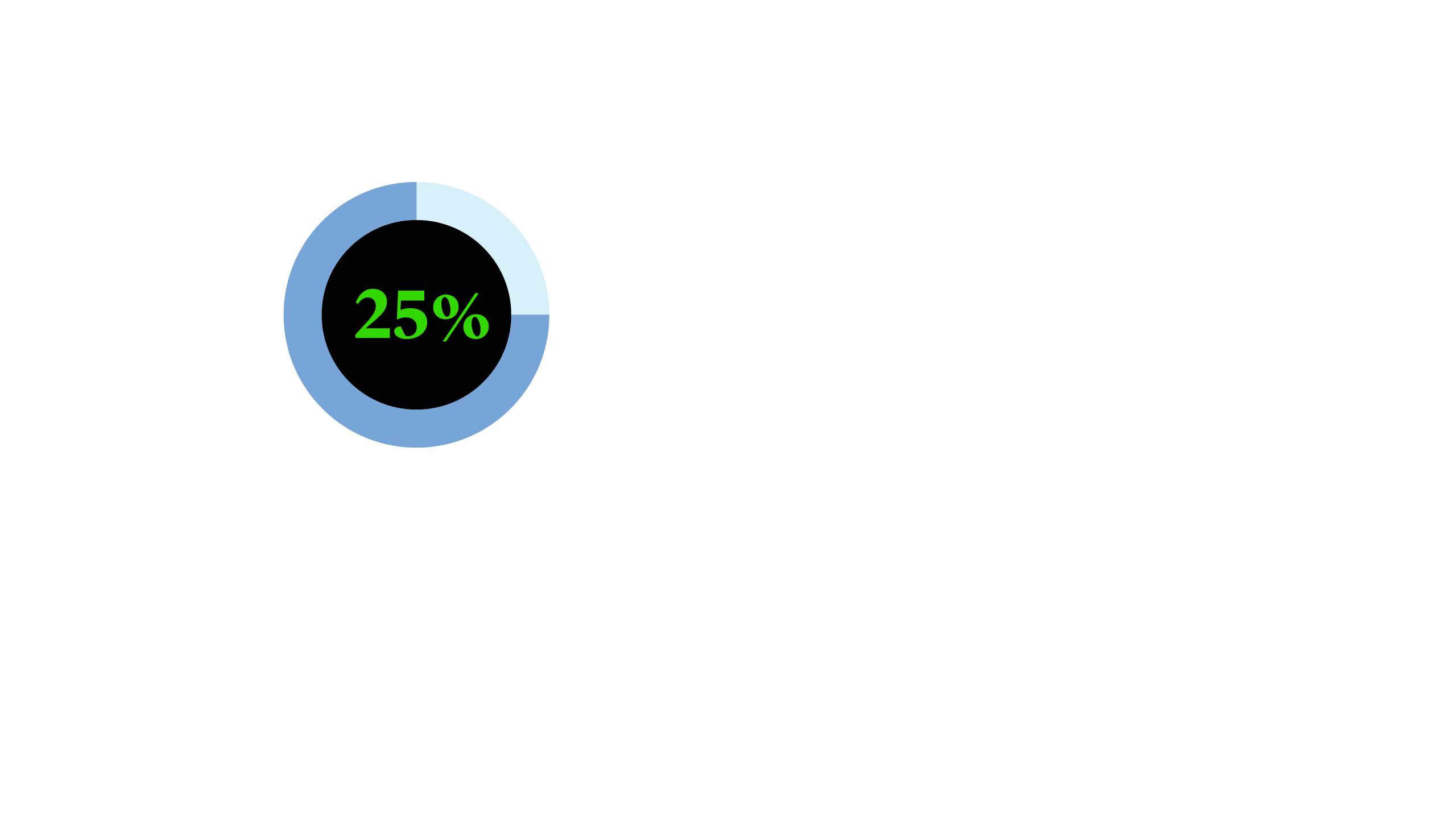

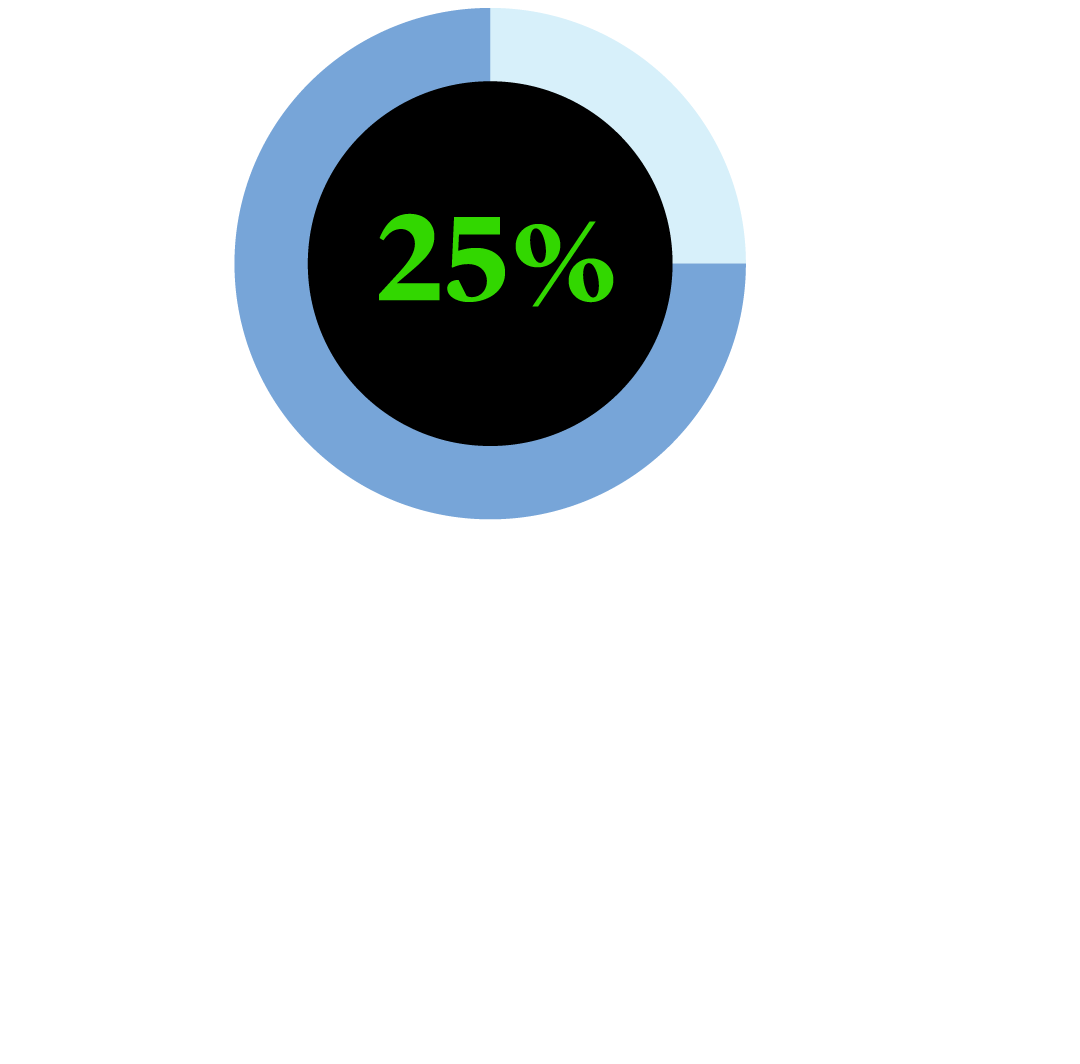

The scale and performance of some of the Middle East funds is only now becoming clear. Saudi Arabia recently opened the books of its Public Investment Fund (PIF) in a transparency drive that revealed that it earned a 25% return last year as assets under management hit $608bn5. PIF is a cornerstone backer of Softbank’s Vision Fund and recently joined forces with U.S. firm Cain International to invest $900mn into luxury hotelier Aman Group6.

Middle East Funds Target New Investments

While many investors are being squeezed by falling portfolio valuations and reduced distributions, other large investors are actively looking for opportunities. Middle East funds, buoyed by rising oil revenues and the strong dollar, are eyeing international markets. Royal Group, an investment firm controlled by a top Abu Dhabi royal, plans to invest up to $10bn into U.S. and European assets hit by fears of a global recession4.

The scale and performance of some of the Middle East funds is only now becoming clear. Saudi Arabia recently opened the books of its Public Investment Fund (PIF) in a transparency drive that revealed that it earned a 25% return last year as assets under management hit $608bn5. PIF is a cornerstone backer of Softbank’s Vision Fund and recently joined forces with U.S. firm Cain International to invest $900mn into luxury hotelier Aman Group6.

Working With Sovereign Wealth Funds

With substantial firepower in challenging market conditions, Middle East sovereign wealth funds are natural partners for private equity on consortium deals. They are increasingly prepared to take large minority exposure to investments, but also demand higher levels of involvement and company access. Below are some considerations for private equity firms thinking about teaming up with sovereign wealth funds.

Sovereign wealth funds have long been active investors in private equity. As market conditions worsen, they will represent a large, liquid and willing source of capital for consortium deals.

Read more about consortium investments in our paper:

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card

Chris Macbeth

Partner

Abu Dhabi

T: +971 2 412 1730

cmacbeth@cgsh.com

V-Card

Michael James

Partner

London

T: +44 20 7614 2219

mjames@cgsh.com

V-Card

Sophie Smith

Counsel

London

T: +44 20 7614 2380

sosmith@cgsh.com

V-Card