Updates to Italy’s Insolvency Code

February 2025

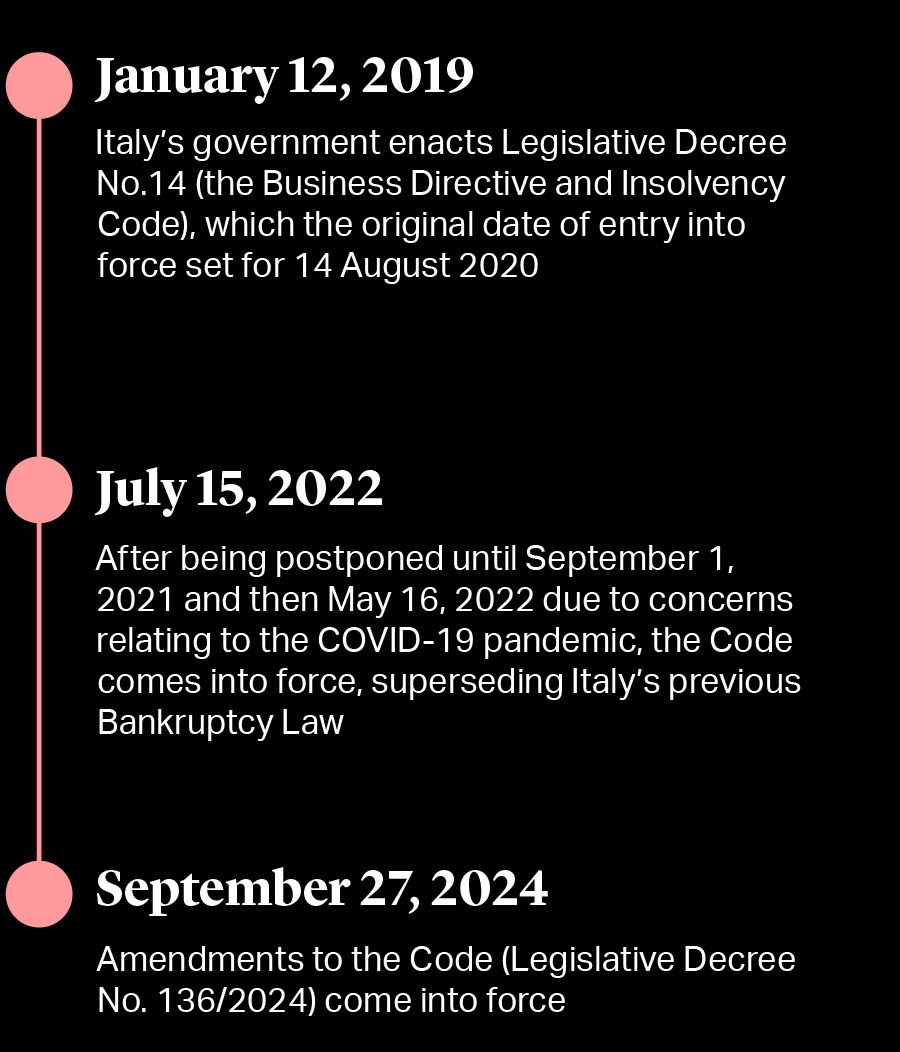

Italy’s Code on Business Distress and Insolvency (the “Code”) has been partly amended and rectified just over two years after its entry into force on July 15, 2022.

The changes are primarily intended to take stock of the initial application of the Code, in order to clarify certain interpretative issues that have arisen and further align it to EU Directive 1023/2019 (the “EU Insolvency Directive”), which the Code sought to implement. The amendments are set forth in Legislative Decree No. 136/2024 (the “Amendment Decree”), which came into force the day after its publication in the Official Journal on September 27, 2024.

Italy’s Code on Business Distress and Insolvency (the “Code”) has been partly amended and rectified just over two years after its entry into force on July 15, 2022.

The changes are primarily intended to take stock of the initial application of the Code, in order to clarify certain interpretative issues that have arisen and further align it to EU Directive 1023/2019 (the “EU Insolvency Directive”), which the Code sought to implement. The amendments are set forth in Legislative Decree No. 136/2024 (the “Amendment Decree”), which came into force the day after its publication in the Official Journal on September 27, 2024.

The most salient changes comprise:

- The preservation of existing credit lines in case of out-of-court composition proceedings (composizione negoziata della crisi; “Composition”);

- the extension of restructuring of tax claims to Composition;

- the clarification of the notion of “liquidation value” for purposes of the absolute and relative priority rules in a judicial composition with creditors (concordato preventivo; the “Concordato”);

- revised requirements for a cross-class cram-down in a Concordato;

- stability and execution of extraordinary corporate transactions made in a restructuring context; and

- restructurings of corporate groups.

The changes brought about by the Amendment Decree also apply to all restructurings and other proceedings under the Code pending on the date of its entry into force.

Key Dates in Italy’s Business Distress and Insolvency Code

Hover to find out more

The most salient changes comprise:

- The preservation of existing credit lines in case of out-of-court composition proceedings (composizione negoziata della crisi; “Composition”);

- the extension of restructuring of tax claims to Composition;

- the clarification of the notion of “liquidation value” for purposes of the absolute and relative priority rules in a judicial composition with creditors (concordato preventivo; the “Concordato”);

- revised requirements for a cross-class cram-down in a Concordato;

- stability and execution of extraordinary corporate transactions made in a restructuring context; and

- restructurings of corporate groups.

The changes brought about by the Amendment Decree also apply to all restructurings and other proceedings under the Code pending on the date of its entry into force.

Key Dates in Italy’s Business

Distress and Insolvency Code

Existing Credit Lines in a Composition

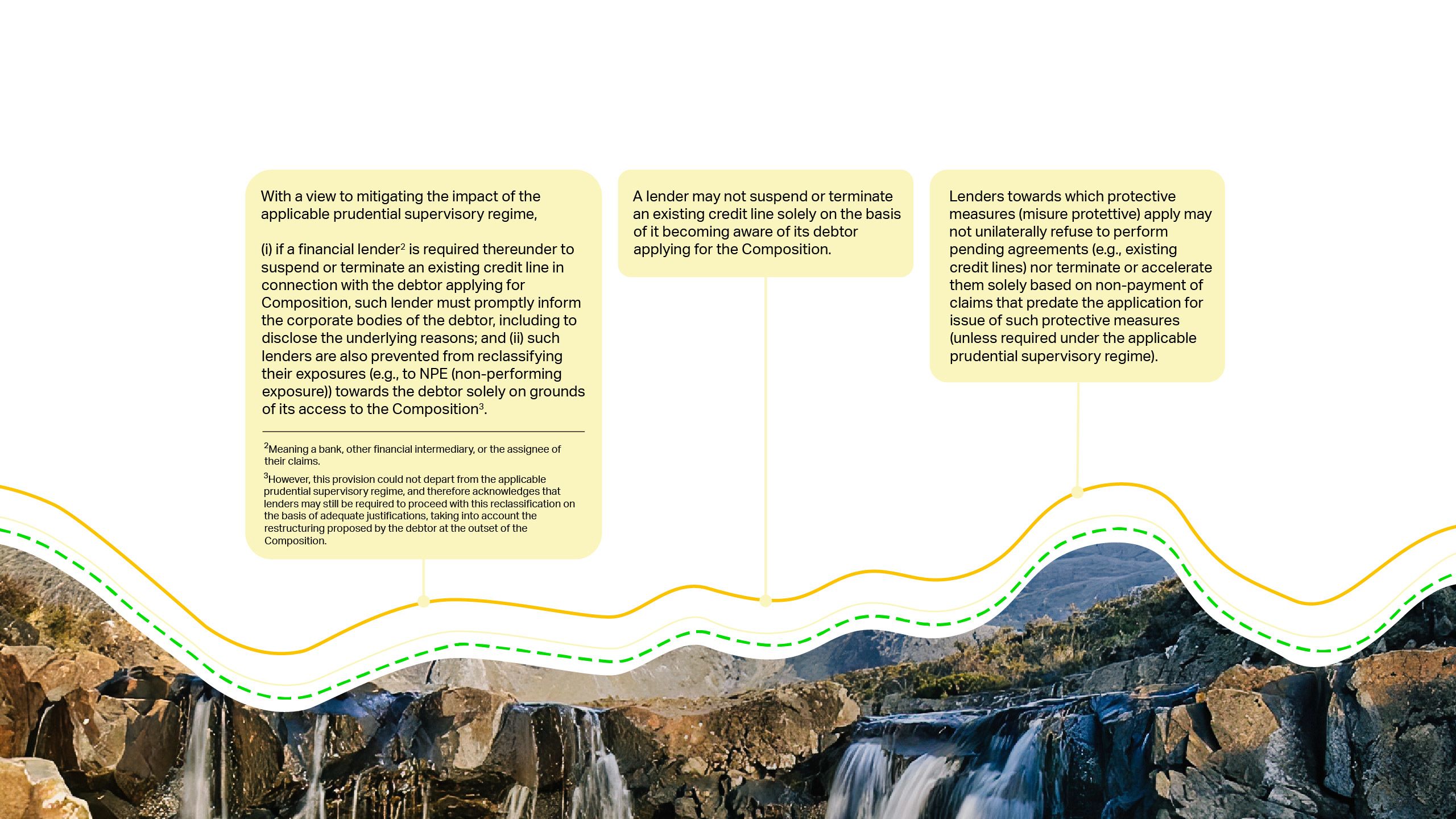

A Composition is an out-of-court process whereby a distressed debtor may seek to restructure1, provided that recovery appears reasonably possible, with the assistance of a third-party expert appointed by the local chamber of commerce. Courts are in principle not involved, except in limited cases (e.g., when a debtor seeks a stay or similar protections pending the Composition).

In this context, the debtor’s access to financing is obviously crucial, including in the form of preserving the ability to draw from existing credit lines, as the Amendment Decree seeks to facilitate. More specifically:

Finally, in order to balance the above restrictions and constraints, the Amendment Decree clarifies that the continuation of the contractual relationship with the debtor does not automatically entail liability for the lender4.

Restructuring of Tax Claims

in a Composition

The Amendment Decree also seeks to fill a significant gap, in that it extends to Composition proceedings the ability to restructure certain5 tax claims6.

Because in a Composition any restructuring must be consensual, tax claims may be restructured only pursuant to an agreement between the debtor and the tax administration. This agreement is proposed by the debtor and must enclose (a) the opinion of a third-party expert certifying the advantage of the proposal over a judicial liquidation, and (b) a report from the debtor’s auditors confirming the accuracy of the underlying financial data.

The agreement must then be submitted to the court for its authorization and terminates in case the debtor subsequently becomes subject to a judicial liquidation or is otherwise found insolvent, or in case the debtor does not fulfill its payment obligations thereunder within 60 days of the applicable term.

Restructuring of Tax Claims in a Composition

The Amendment Decree also seeks to fill a significant gap, in that it extends to Composition proceedings the ability to restructure certain5 tax claims6.

Because in a Composition any restructuring must be consensual, tax claims may be restructured only pursuant to an agreement between the debtor and the tax administration. This agreement is proposed by the debtor and must enclose (a) the opinion of a third-party expert certifying the advantage of the proposal over a judicial liquidation, and (b) a report from the debtor’s auditors confirming the accuracy of the underlying financial data.

The agreement must then be submitted to the court for its authorization and terminates in case the debtor subsequently becomes subject to a judicial liquidation or is otherwise found insolvent, or in case the debtor does not fulfill its payment obligations thereunder within 60 days of the applicable term.

Clarifications on the Absolute and Relative Priority Rules in a Concordato

A Concordato may be used either to effect a piecemeal liquidation of the debtor’s assets or to allow the continuation of the debtor’s business as a going concern7 (the “Business Continuity Concordato”).

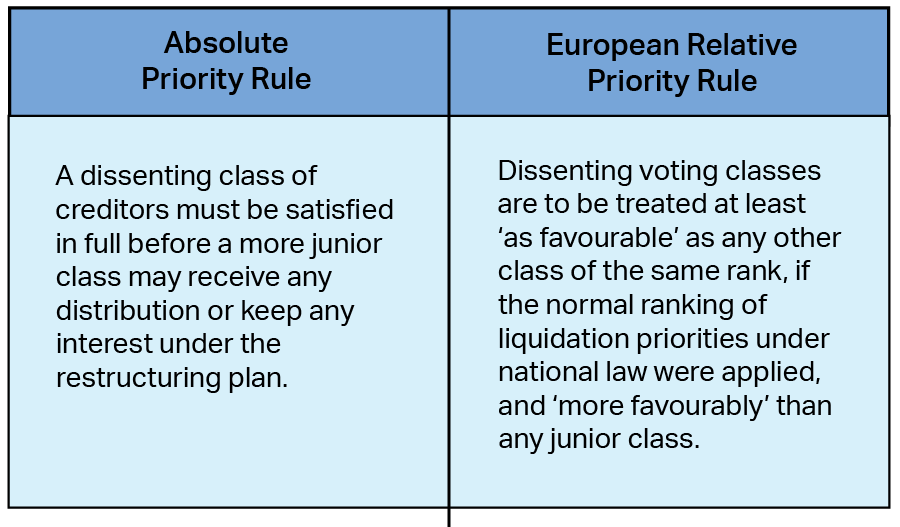

In this latter type of Concordato, the EU Insolvency Directive granted Member States the option to adopt either an “absolute priority rule” or a “relative priority rule” to the payment of creditors. Except with respect to claims of employees,8 Italy has opted for the latter in the Code, in the following form:

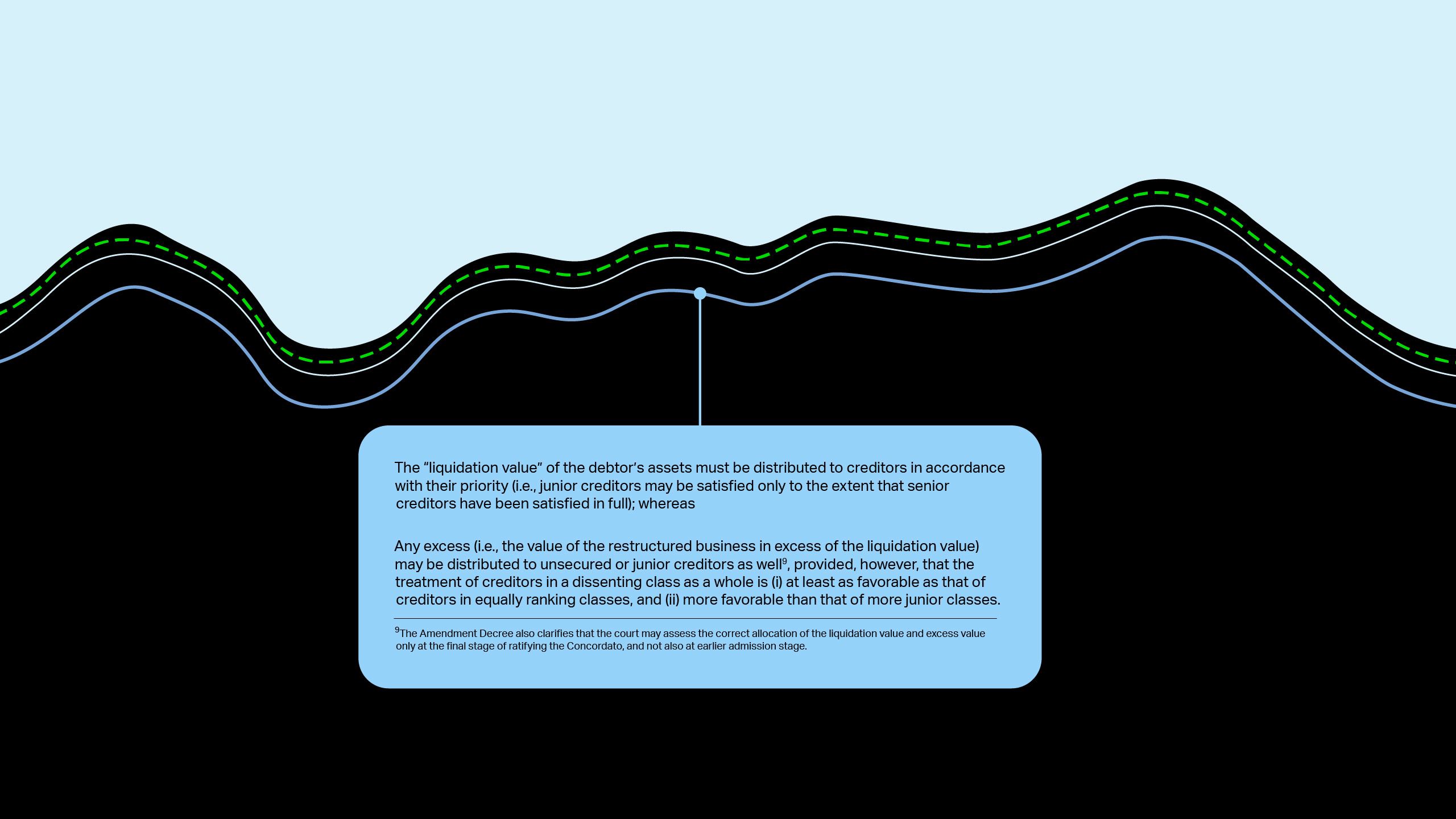

However, the concrete application of these provisions has given rise to interpretative uncertainties, primarily regarding the concept of “liquidation value”, because neither the EU Insolvency Directive nor the Code provided sufficient guidelines on this notion.

In this regard, the Amendment Decree has defined “liquidation value” as the value of the proceeds that can be expected10 from the sale (occurring as part of a judicial liquidation) of the debtor’s “assets and rights”, including such higher value as it could be obtained from (i) the sale of the business as a going-concern (as opposed to a piecemeal liquidation) and (ii) the exercise of potential claw-back or liability actions.

However, the concrete application of these provisions has given rise to interpretative uncertainties, primarily regarding the concept of “liquidation value”, because neither the EU Insolvency Directive nor the Code provided sufficient guidelines on this notion.

In this regard, the Amendment Decree has defined “liquidation value” as the value of the proceeds that can be expected10 from the sale (occurring as part of a judicial liquidation) of the debtor’s “assets and rights”, including such higher value as it could be obtained from (i) the sale of the business as a going-concern (as opposed to a piecemeal liquidation) and (ii) the exercise of potential claw-back or liability actions.

Changes to the Cross-Class

Cram-Down

As a general rule, approval of a Business Continuity Concordato requires the favorable vote of (i) a majority of creditors (by value) admitted to vote, and (ii) all voting classes.

However, failure to achieve the voting classes’ approval may be overruled by the court (so-called “cram-down”) at the subsequent stage of ratification (omologa), subject to various conditions.

Prior to the Amendment Decree, these conditions included approval of the Concordato proposal by the majority of creditor classes, provided that (a) at least one class of secured creditors approved it, or (b), absent approval by any such class, a class of creditors that, based on the ordinary ranking of claims, would be satisfied, at least in part, with the restructuring proceeds in excess of the liquidation value (based on a valuation of the debtor as a going concern) approved the Concordato.

However, this condition had raised interpretative issues, as it was unclear what “absent approval by any such class” actually meant. Accordingly, the Amendment Decree has clarified that this expression refers to the Concordato plan not having been approved by the majority of classes, in which case the court may still ratify it if the plan has at least been approved by a class of creditors that (i), under the plan, are not offered a full recovery on their claims, but (ii) would receive at least a partial recovery even if the absolute priority rule also applied in respect of the value exceeding the “liquidation value”.

Extraordinary Corporate Transactions

The Amendment Decree also impacts extraordinary corporate transactions carried out in the context of, or pursuant to, a Concordato.

In particular, the Amendment Decree seeks to consolidate and stabilize the effects of these transactions (i.e., mergers, de-mergers, corporate conversions) if these are envisaged in the Concordato plan, providing that:

- oppositions by creditors (whether of the debtor or of other companies involved in the transaction) must be lodged in the context of the court hearing convened to ratify the Concordato11 (as opposed to the ordinary venues in case these transactions take place outside a Concordato);

- withdrawal rights of the shareholders normally arising in connection with a merger, de-merger, or corporate conversion are suspended until completion of the transaction;

- once the Concordato plan is ratified by the court12, including by means of a non-final ruling (because an appeal is pending or still possible), the underlying corporate resolution (e.g., the shareholders’ meeting resolution approving the merger) may not be annulled even if found in breach of the law and, therefore, the relevant transaction may not be affected. The only consequence would be indemnification, whose award must be satisfied as a super-priority claim (prededucibile). The same rule also applies in case of termination or annulment of the Concordato after its court ratification.

Further, the Amendment Decree also seeks to ensure that, if a plan envisages an extraordinary corporate transaction (e.g., a share capital increase instrumental to a debt-equity swap, a merger, or de-merger), this is effectively consummated even if the shareholders do not cooperate. To that end, shareholders’ meeting resolutions may indeed be replaced by the relevant court ruling, and possible ensuing implementing actions shall be carried out by the debtor’s directors (or, in case of their inertia, a judicial administrator appointed upon request of any interested party).

Extraordinary Corporate Transactions

The Amendment Decree also impacts extraordinary corporate transactions carried out in the context of, or pursuant to, a Concordato.

In particular, the Amendment Decree seeks to consolidate and stabilize the effects of these transactions (i.e., mergers, de-mergers, corporate conversions) if these are envisaged in the Concordato plan, providing that:

- oppositions by creditors (whether of the debtor or of other companies involved in the transaction) must be lodged in the context of the court hearing convened to ratify the Concordato11 (as opposed to the ordinary venues in case these transactions take place outside a Concordato);

- withdrawal rights of the shareholders normally arising in connection with a merger, de-merger, or corporate conversion are suspended until completion of the transaction;

- once the Concordato plan is ratified by the court12, including by means of a non-final ruling (because an appeal is pending or still possible), the underlying corporate resolution (e.g., the shareholders’ meeting resolution approving the merger) may not be annulled even if found in breach of the law and, therefore, the relevant transaction may not be affected. The only consequence would be indemnification, whose award must be satisfied as a super-priority claim (prededucibile). The same rule also applies in case of termination or annulment of the Concordato after its court ratification.

Further, the Amendment Decree also seeks to ensure that, if a plan envisages an extraordinary corporate transaction (e.g., a share capital increase instrumental to a debt-equity swap, a merger, or de-merger), this is effectively consummated even if the shareholders do not cooperate. To that end, shareholders’ meeting resolutions may indeed be replaced by the relevant court ruling, and possible ensuing implementing actions shall be carried out by the debtor’s directors (or, in case of their inertia, a judicial administrator appointed upon request of any interested party).

Group Restructurings

The Amendment Decree also tries to further coordinate and facilitate group-wide restructurings. In particular:

- a group-wide Concordato or group-wide restructuring agreement may be started by means of a single petition filed by the group parent company13. Consistently, the Amendment Decree clarifies that a restructuring of a group’s tax and/or social security claims may also be proposed by a means of a single proposal that the group parent company submits to a single office of the tax and social security administrations;

- as in the case of a standalone Business Continuity Concordato, the Amendment Decree provides that creditors of the group companies pursuing this type of Concordato may be satisfied with the proceeds from the going concern even if these do not represent the prevailing source of their recovery (the balance coming from the proceeds of the liquidation of other assets no longer used for the business);

- the requirements for court-ratification of a Concordato must be met for each group company participating in the restructuring;

- in case a group company participating in the group Concordato is a creditor of the group parent company in respect of a loan or financing that the former granted to the latter, its claim is no longer subordinated by operation of law;

- the court may order at any time the separation of the single group-wide proceeding in case it detects a conflict of interest between the different group companies or between the interests of their respective creditors. Similarly, in case of a judicial liquidation, the court must order the separation of the group-wide proceeding in the event that the bankruptcy trustee intends to start a liability action against any group company for abusive exercise of “direction and coordination”.

Group Restructurings

The Amendment Decree also tries to further coordinate and facilitate group-wide restructurings. In particular:

A group-wide Concordato or group-wide restructuring agreement may be started by means of a single petition filed by the group parent company13. Consistently, the Amendment Decree clarifies that a restructuring of a group’s tax and/or social security claims may also be proposed by a means of a single proposal that the group parent company submits to a single office of the tax and social security administrations;

As in the case of a standalone Business Continuity Concordato, the Amendment Decree provides that creditors of the group companies pursuing this type of Concordato may be satisfied with the proceeds from the going concern even if these do not represent the prevailing source of their recovery (the balance coming from the proceeds of the liquidation of other assets no longer used for the business);

The requirements for court-ratification of a Concordato must be met for each group company participating in the restructuring;

In case a group company participating in the group Concordato is a creditor of the group parent company in respect of a loan or financing that the former granted to the latter, its claim is no longer subordinated by operation of law;

The court may order at any time the separation of the single group-wide proceeding in case it detects a conflict of interest between the different group companies or between the interests of their respective creditors. Similarly, in case of a judicial liquidation, the court must order the separation of the group-wide proceeding in the event that the bankruptcy trustee intends to start a liability action against any group company for abusive exercise of “direction and coordination”.

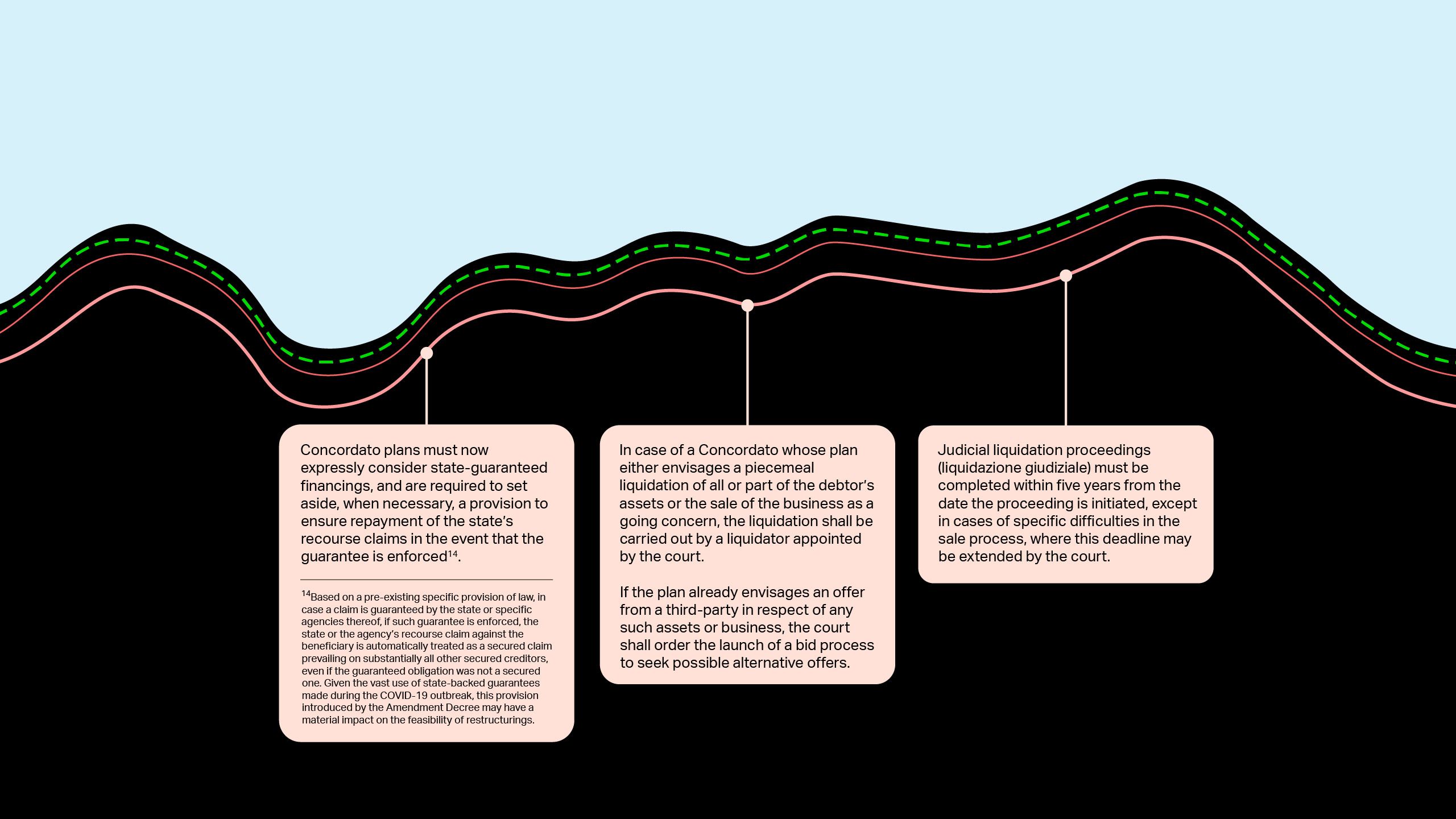

Other Relevant Amendments

Other notable changes brought about by the Amendment Decree include: