Last year was a turbulent economic and political period, to say the least. Despite a great deal of hope as economies emerged from the dark days of the pandemic, Russia’s decision to invade Ukraine led to disruption in the global economy, impacting supply chains and causing a rise in prices for everything from food to energy.

Western nations rushed to demonstrate their solidarity with Ukraine by rolling out an unprecedented set of sanctions targeting Russia and its economy in a bid to isolate the country from the global financial system. Russia has responded to these sanctions with its own set of countermeasures, creating a complex legal environment for foreign investors. In this article, we look at the measures taken by those on both sides, and outline what these sanctions mean for those invested in Russian sovereign debt.

Last year was a turbulent economic and political period, to say the least. Despite a great deal of hope as economies emerged from the dark days of the pandemic, Russia’s decision to invade Ukraine led to disruption in the global economy, impacting supply chains and causing a rise in prices for everything from food to energy.

Western nations rushed to demonstrate their solidarity with Ukraine by rolling out an unprecedented set of sanctions targeting Russia and its economy in a bid to isolate the country from the global financial system. Russia has responded to these sanctions with its own set of countermeasures, creating a complex legal environment for foreign investors. In this article, we look at the measures taken by those on both sides, and outline what these sanctions mean for those invested in Russian sovereign debt.

How Foreign Ownership

Has Changed

In general, the Russian government sells two types of bonds to foreign investors. These include Eurobonds – those denominated in foreign currencies (usually in dollars) that form part of Russia’s external debt; and local currency bonds (i.e., federal loan obligations or OFZs) – these are denominated in Russian rubles which form part of the state’s internal debt. In both instances, these bonds are issued by the Ministry of Finance of the Russian Federation.

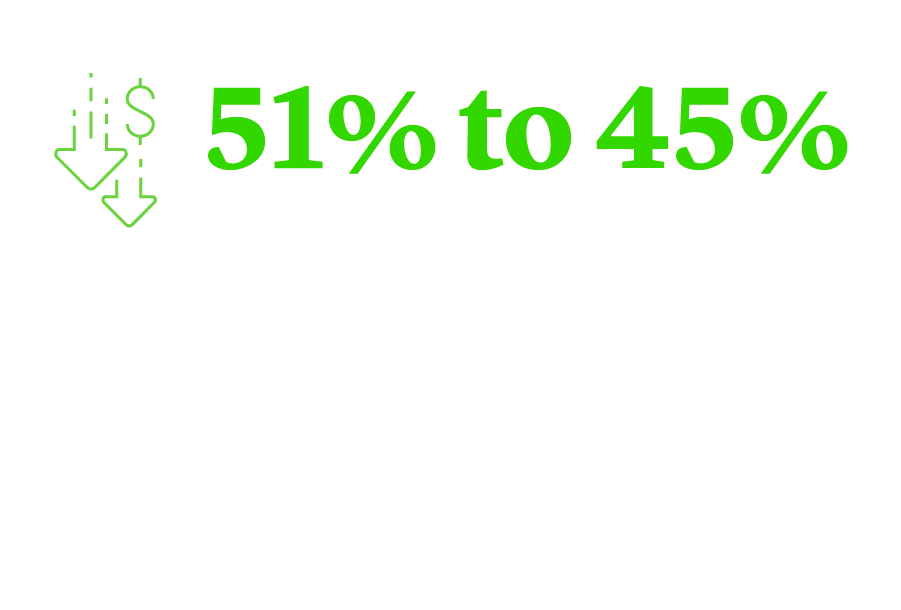

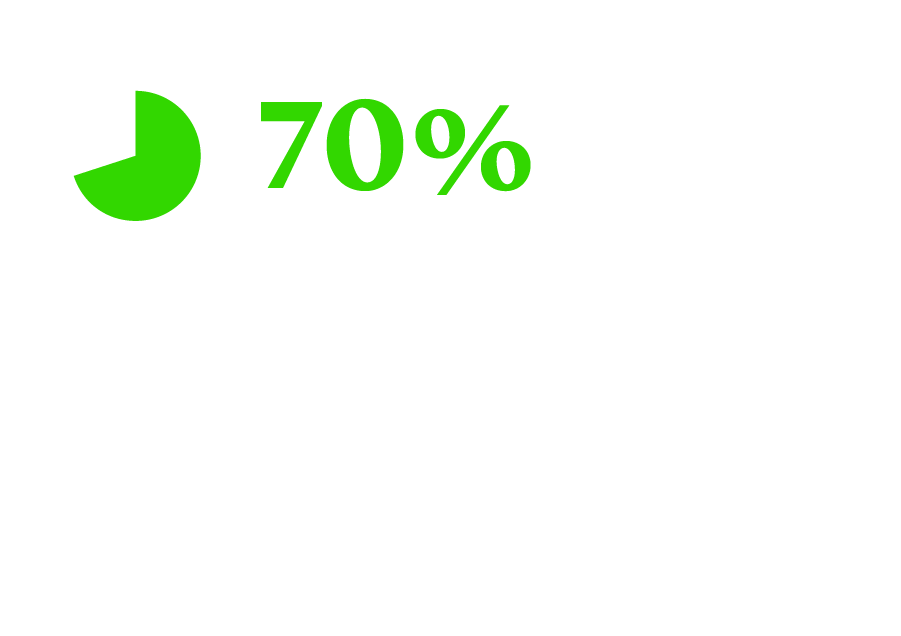

Since Russia’s invasion of Ukraine, foreign ownership of sovereign Eurobonds has started to fall. In January 2022, the share of these bonds owned by foreign investors stood at 51.1%, representing circa $20bn. By January 2023, that figure had fallen to 45%, or $16bn, according to Russia’s Central Bank. Meanwhile, foreign ownership of local currency sovereign bonds has seen an even steeper decline, falling from 19.9% (roughly RUB3.1tn) in January 2022 to 11.1% (circa RUB2.0tn) in January 2023.

How Foreign Ownership

Has Changed

In general, the Russian government sells two types of bonds to foreign investors. These include Eurobonds – those denominated in foreign currencies (usually in dollars) that form part of Russia’s external debt; and local currency bonds (i.e., federal loan obligations or OFZs) – these are denominated in Russian rubles which form part of the state’s internal debt. In both instances, these bonds are issued by the Ministry of Finance of the Russian Federation.

Since Russia’s invasion of Ukraine, foreign ownership of sovereign Eurobonds has started to fall. In January 2022, the share of these bonds owned by foreign investors stood at 51.1%, representing circa $20bn. By January 2023, that figure had fallen to 45%, or $16bn, according to Russia’s Central Bank. Meanwhile, foreign ownership of local currency sovereign bonds has seen an even steeper decline, falling from 19.9% (roughly RUB3.1tn) in January 2022 to 11.1% (circa RUB2.0tn) in January 2023.

Western Sanctions1

The U.S.

The U.S. has imposed sanctions targeting Russian sovereign debt since 2019, when the country prohibited U.S. financial institutions from participating in the primary market for non-ruble denominated bonds issued by the Russian sovereign, including Russia’s Central Bank (“CBR”), the Russian National Wealth Fund (“NWF”), and Russian Ministry of Finance (“MinFin”)2. At that time, the prohibition did not apply to local currency bonds or the secondary market for Russian sovereign debt. Subsequently, in 2021, the U.S. prohibited American financial institutions from participating in the primary market for both ruble and non-ruble denominated bonds issued after June 14, 2021, by the CBR, the NWF and the MinFin3. Again, the secondary market for Russian sovereign debt remained outside the scope of U.S. sanctions on sovereign debt, but this situation changed in 2022.

U.S. Sanctions on Russian Sovereign Debt

In late February 2022, the U.S. prohibited the same financial institutions from participating in the secondary market for ruble or non-ruble denominated bonds issued after March 1, 2022 by the CBR, NWF, or MinFin. In addition, it prohibited U.S. persons from engaging in any transactions involving the same institutions, including any transfer of assets to such entities and any foreign exchange transactions for or on behalf of such entities. The U.S. Department of the Treasury’s Office of Foreign Assets Control (“OFAC”) clarified that, subject to the above-referenced secondary trading restrictions on U.S. financial institutions, the prohibition does not apply to trading in the secondary markets for debt issued by the CBR, the NWF or MinFin, provided that no such entity was a counterparty to the transaction and no other restrictions were triggered. The ban, however, applied whenever dollar interest or principal payments were made on Russian sovereign debt given that dollar payments clear through the U.S. financial system. Although OFAC temporarily authorized such payments, the general license lapsed on May 25, 2022, and has since not been renewed. Since then, U.S. persons have required a specific license to continue to receive dollar interest or principal payments on Russian sovereign debt.

As part of a further escalation in April 2022, the U.S. introduced a sweeping ban on “new investments,” which, as OFAC clarified in June 2022, prohibits U.S. persons from purchasing both new and existing debt securities issued by an entity in Russia. The restrictions do not prohibit U.S. persons from selling or divesting debt or equity securities issued by an entity in Russia to a non-U.S. person.

Western Sanctions1

The U.S.

The U.S. has imposed sanctions targeting Russian sovereign debt since 2019, when the country prohibited U.S. financial institutions from participating in the primary market for non-ruble denominated bonds issued by the Russian sovereign, including Russia’s Central Bank (“CBR”), the Russian National Wealth Fund (“NWF”), and Russian Ministry of Finance (“MinFin”)2. At that time, the prohibition did not apply to local currency bonds or the secondary market for Russian sovereign debt. Subsequently, in 2021, the U.S. prohibited American financial institutions from participating in the primary market for both ruble and non-ruble denominated bonds issued after June 14, 2021, by the CBR, the NWF and the MinFin3. Again, the secondary market for Russian sovereign debt remained outside the scope of U.S. sanctions on sovereign debt, but this situation changed in 2022.

U.S. Sanctions on Russian Sovereign Debt

In late February 2022, the U.S. prohibited the same financial institutions from participating in the secondary market for ruble or non-ruble denominated bonds issued after March 1, 2022 by the CBR, NWF, or MinFin. In addition, it prohibited U.S. persons from engaging in any transactions involving the same institutions, including any transfer of assets to such entities and any foreign exchange transactions for or on behalf of such entities. The U.S. Department of the Treasury’s Office of Foreign Assets Control (“OFAC”) clarified that, subject to the above-referenced secondary trading restrictions on U.S. financial institutions, the prohibition does not apply to trading in the secondary markets for debt issued by the CBR, the NWF or MinFin, provided that no such entity was a counterparty to the transaction and no other restrictions were triggered. The ban, however, applied whenever dollar interest or principal payments were made on Russian sovereign debt given that dollar payments clear through the U.S. financial system. Although OFAC temporarily authorized such payments, the general license lapsed on May 25, 2022, and has since not been renewed. Since then, U.S. persons have required a specific license to continue to receive dollar interest or principal payments on Russian sovereign debt.

As part of a further escalation in April 2022, the U.S. introduced a sweeping ban on “new investments,” which, as OFAC clarified in June 2022, prohibits U.S. persons from purchasing both new and existing debt securities issued by an entity in Russia. The restrictions do not prohibit U.S. persons from selling or divesting debt or equity securities issued by an entity in Russia to a non-U.S. person.

The EU

The EU followed the U.S. in 2022 and introduced its own restrictive measures. It prohibited directly or indirectly purchasing, selling, or otherwise dealing with transferable securities, including bonds, issued after March 9, 2022, by Russia, its government, the CBR, or a legal person, entity or body acting on behalf of or at the direction of the CBR. Furthermore, the EU introduced a prohibition on refinancing Russian sovereign debt, and banned any transactions related to the management of the reserves and assets of the CBR and the NWF (but, interestingly, not MinFin). It also made the National Settlement Depository, which provides safekeeping and depository services in respect of Russian local currency sovereign bonds and which has acted as paying agent under a number of Russian sovereign Eurobonds, subject to an asset freeze. In practice, the latter meant that there was no longer an active bridge between the NSD and international clearing systems, including Euroclear and Clearstream. Although, in contrast to the U.S., EU sanctions do not per se impose any impediments to receiving payments under Russian sovereign bonds, because of the asset freeze imposed on the NSD, any payment made by the NSD to any of the international central securities depositories (ICSDs) is subject to blocking by the latter. Notably, the ICSDs reinforced the blow to investors by announcing the suspension of trading, clearing, and settlement of any ruble-denominated transactions, which effectively left foreign investors trapped in Russian local currency bonds.

The EU

The EU followed the U.S. in 2022 and introduced its own restrictive measures. It prohibited directly or indirectly purchasing, selling, or otherwise dealing with transferable securities, including bonds, issued after March 9, 2022, by Russia, its government, the CBR, or a legal person, entity or body acting on behalf of or at the direction of the CBR. Furthermore, the EU introduced a prohibition on refinancing Russian sovereign debt, and banned any transactions related to the management of the reserves and assets of the CBR and the NWF (but, interestingly, not MinFin). It also made the National Settlement Depository, which provides safekeeping and depository services in respect of Russian local currency sovereign bonds and which has acted as paying agent under a number of Russian sovereign Eurobonds, subject to an asset freeze. In practice, the latter meant that there was no longer an active bridge between the NSD and international clearing systems, including Euroclear and Clearstream. Although, in contrast to the U.S., EU sanctions do not per se impose any impediments to receiving payments under Russian sovereign bonds, because of the asset freeze imposed on the NSD, any payment made by the NSD to any of the international central securities depositories (ICSDs) is subject to blocking by the latter. Notably, the ICSDs reinforced the blow to investors by announcing the suspension of trading, clearing, and settlement of any ruble-denominated transactions, which effectively left foreign investors trapped in Russian local currency bonds.

The UK

In late February and March 2022, the UK restricted the provision of any financial services, including payment transmission services, for the purpose of foreign exchange reserve and asset management to the CBR, the NWF, and MinFin, as well as any persons owned or controlled by any of these entities or acting on their behalf or at their direction. Similar to the U.S., in April 2022 the UK Treasury temporarily authorized financial services for the purposes of the receipt and onward transfer of non-ruble-denominated interest and principal payments from the CBR, the NWF and MinFin in respect of debt issued by them before March 1, 2022. However, the authorization expired on June 30, 2022, and was not extended. Furthermore, the UK extended existing restrictions on dealing with certain financial instruments by prohibiting any dealings with transferable securities, which includes bonds, issued on or after March 1, 2022, by the Russian government. Unlike the U.S. though, an outright prohibition on all new investments to Russia introduced by the UK in July 2022 did not extend to new or existing debt.

The UK

In late February and March 2022, the UK restricted the provision of any financial services, including payment transmission services, for the purpose of foreign exchange reserve and asset management to the CBR, the NWF, and MinFin, as well as any persons owned or controlled by any of these entities or acting on their behalf or at their direction. Similar to the U.S., in April 2022 the UK Treasury temporarily authorized financial services for the purposes of the receipt and onward transfer of non-ruble-denominated interest and principal payments from the CBR, the NWF and MinFin in respect of debt issued by them before March 1, 2022. However, the authorization expired on June 30, 2022, and was not extended. Furthermore, the UK extended existing restrictions on dealing with certain financial instruments by prohibiting any dealings with transferable securities, which includes bonds, issued on or after March 1, 2022, by the Russian government. Unlike the U.S. though, an outright prohibition on all new investments to Russia introduced by the UK in July 2022 did not extend to new or existing debt.

Russian Response

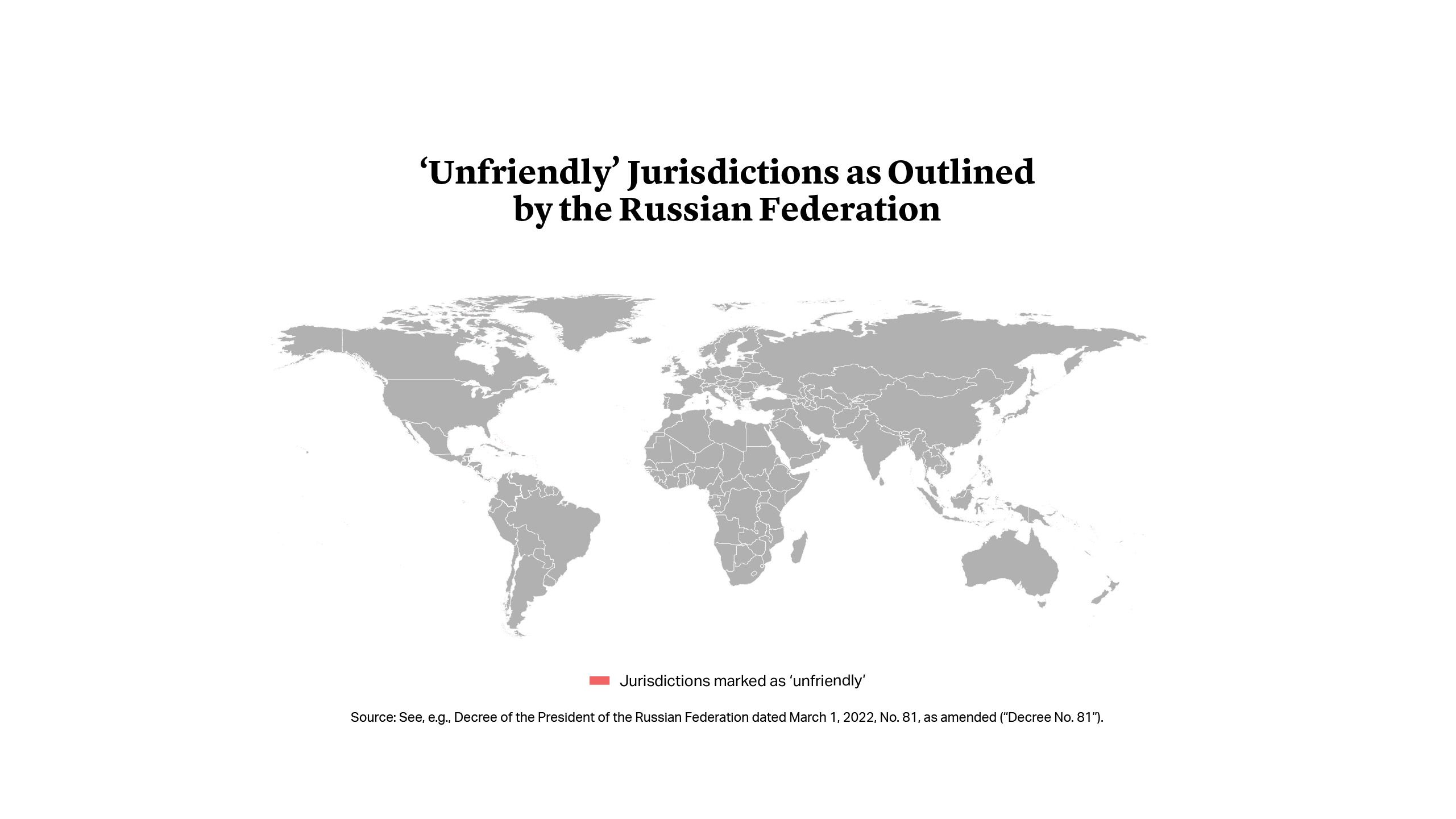

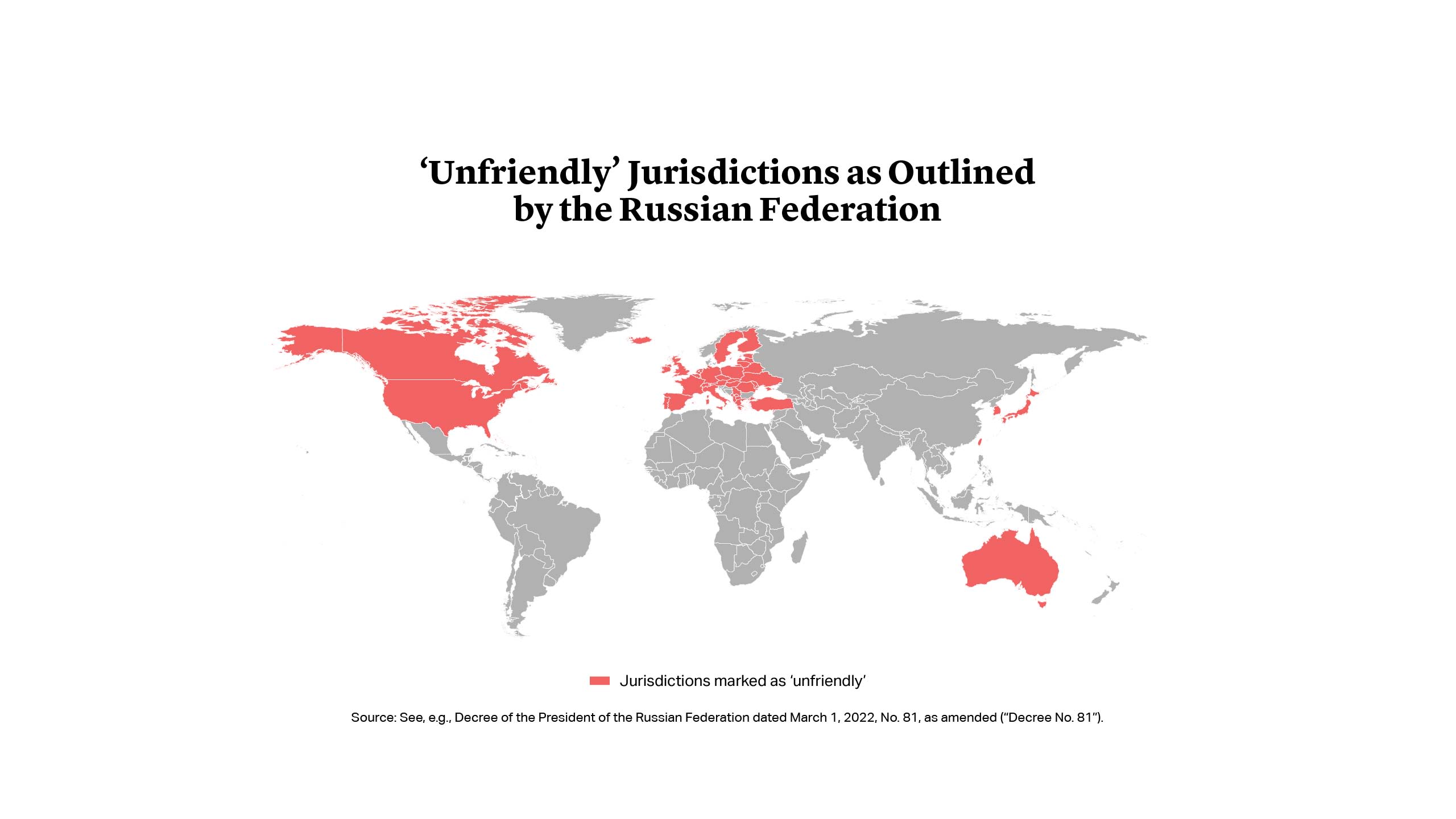

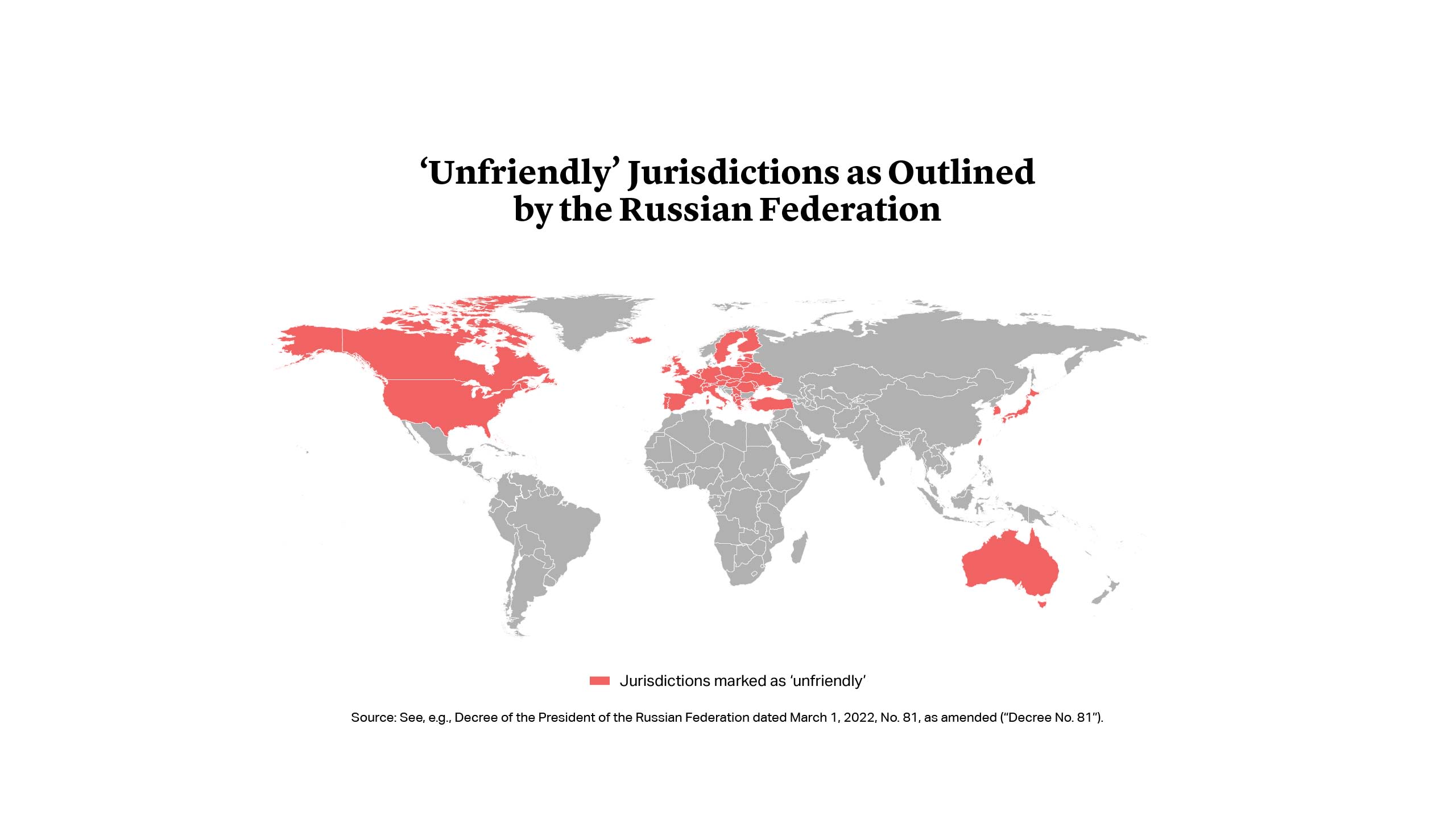

The Russian state reciprocated and introduced countermeasures in response to a rollout of Western sanctions on its sovereign debt – any transactions with sovereign bonds involving Russian financial infrastructure and investors from “unfriendly jurisdictions,” such as the U.S., EU, and UK, now require special clearance by the Russian government. Workarounds, such as SPVs incorporated in “friendly” jurisdictions but controlled by persons from “unfriendly” investors are also prohibited by Russian law. Furthermore, payments on sovereign bonds are now made differently.

Russian Response – From Russia with Love

The Russian state reciprocated and introduced countermeasures in response to a rollout of Western sanctions on its sovereign debt – any transactions with sovereign bonds involving Russian financial infrastructure and investors from “unfriendly jurisdictions,” such as the U.S., EU, and UK, now require special clearance by the Russian government. Workarounds, such as SPVs incorporated in “friendly” jurisdictions but controlled by persons from “unfriendly” investors are also prohibited by Russian law. Furthermore, payments on sovereign bonds are now made differently.

After payments are made to Group I and Group II investors, the residue funds are transferred to a special “I”-type account. In order to get payments from such accounts, Group III investors will need to apply to the NSD, disclosing its holding structure up to an ultimate holder and providing title documents to Eurobonds, which could be particularly difficult given how complicated the majority of holding structures are these days. Foreign investors must also waive any potential claims against MinFin. Once such steps are completed and the NSD is satisfied with the documents, foreign investors could get payments on their personal accounts but through Russian banks. It should be noted that investors from “unfriendly” jurisdictions are eligible to have only restricted “S”-type accounts in Russia4, the funds in which could not be moved out of Russia without a special clearance. Setting aside the issue of how many Russian banks are subject to Western sanctions, moving out of foreign infrastructure and getting payments on sovereign Eurobonds in Russia is not an appealing option for the majority, if not all, foreign investors.

Although a different regime applies to sovereign local currency bonds, investors from “unfriendly” jurisdictions find themselves in a similar position. Interest payments or principal repayments should be made to restricted “S”-type accounts opened with Russian credit institutions. Furthermore, even if payments on local currency bonds were made through the normal payment routes, considering the asset freeze imposed by the EU on the NSD and the suspension of settlement of ruble-denominated payments by ICSDs, it is unlikely that funds would reach foreign investors.

Only time will tell us to what extent the Western sanctions will really affect Russia. What is clear, however, is that both the package of measures implemented by the West, and the countersanctions put forward by Russia, have created a highly complex legal landscape for foreign investors in sovereign bonds, and this is proving a significant challenge for many to navigate. With no end to the war in sight, these investors will continue to bear a significant cost as a result.

After payments are made to Group I and Group II investors, the residue funds are transferred to a special “I”-type account. In order to get payments from such accounts, Group III investors will need to apply to the NSD, disclosing its holding structure up to an ultimate holder and providing title documents to Eurobonds, which could be particularly difficult given how complicated the majority of holding structures are these days. Foreign investors must also waive any potential claims against MinFin. Once such steps are completed and the NSD is satisfied with the documents, foreign investors could get payments on their personal accounts but through Russian banks. It should be noted that investors from “unfriendly” jurisdictions are eligible to have only restricted “S”-type accounts in Russia4, the funds in which could not be moved out of Russia without a special clearance. Setting aside the issue of how many Russian banks are subject to Western sanctions, moving out of foreign infrastructure and getting payments on sovereign Eurobonds in Russia is not an appealing option for the majority, if not all, foreign investors.

Although a different regime applies to sovereign local currency bonds, investors from “unfriendly” jurisdictions find themselves in a similar position. Interest payments or principal repayments should be made to restricted “S”-type accounts opened with Russian credit institutions. Furthermore, even if payments on local currency bonds were made through the normal payment routes, considering the asset freeze imposed by the EU on the NSD and the suspension of settlement of ruble-denominated payments by ICSDs, it is unlikely that funds would reach foreign investors.

Only time will tell us to what extent the Western sanctions will really affect Russia. What is clear, however, is that both the package of measures implemented by the West, and the countersanctions put forward by Russia, have created a highly complex legal landscape for foreign investors in sovereign bonds, and this is proving a significant challenge for many to navigate. With no end to the war in sight, these investors will continue to bear a significant cost as a result.

Polina Lyadnova

Partner

London

T: +44 20 7614 2355

plyadnova@cgsh.com

V-Card

Jim Ho

Partner

London

T: +44 20 7614 2284

jho@cgsh.com

V-Card

Chase D. Kaniecki

Partner

Washington, D.C.

T: +1 202 974 1792

ckaniecki@cgsh.com

V-Card