The pandemic and its aftermath are causing growing levels of sovereign debt distress – particularly in certain emerging markets. As growing numbers of sovereigns face the prospect of debt restructuring, it is important to consider current and anticipated dispute resolution trends and plan ahead. The robustness of Collective Action Clauses (CACs) has finally been put to the test over recent years and further CAC litigation seems likely. Previous disputes, such as those resulting from Argentina’s ongoing sovereign debt crisis, also led to action under International Investment Agreements (IIAs) and this trend looks likely to return in the coming years.

CACs and Holdout Litigation

Argentina and Ecuador were not only two of the pandemic’s biggest sovereign restructurings, they were also the first real tests for the capability of CACs, which have become a mainstay in sovereign bonds since 2003, to reduce litigation by “holdout” sovereign creditors. CACs address growing concerns over minority creditor holdouts during sovereign debt restructuring negotiations, in which minority creditors refuse to accept a majority-agreed restructuring and litigate for full repayment of their debt.

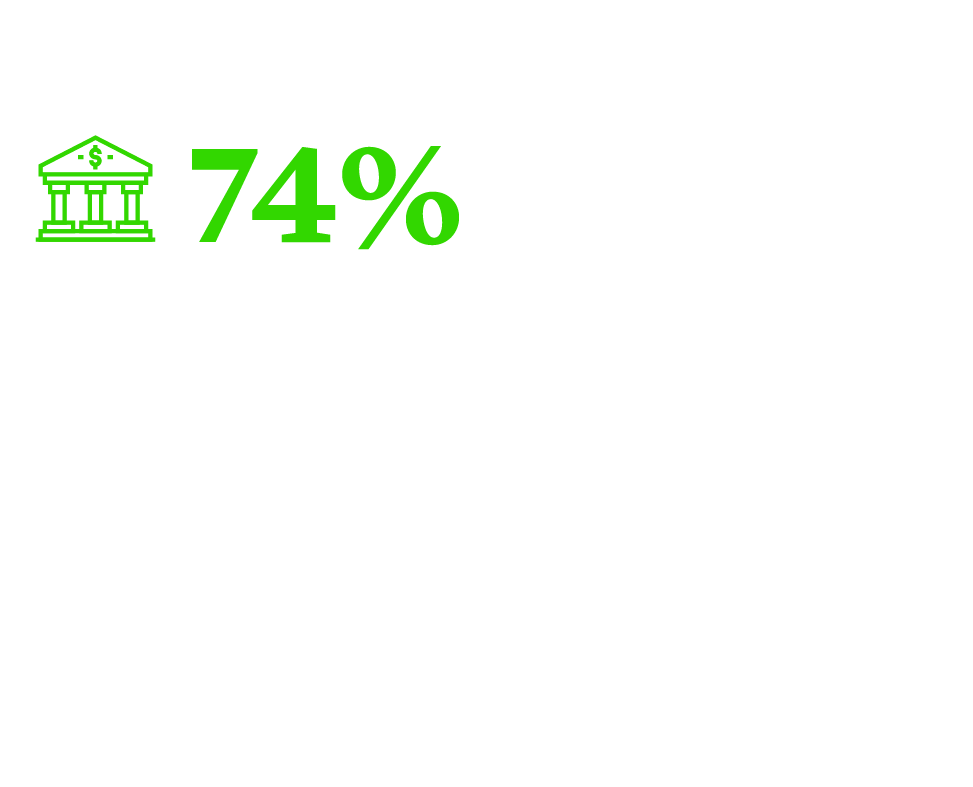

CACs bind all bondholders where a specified supermajority of bondholders agrees to the terms of a debt restructuring. From January 2005 to 2012, 99% of the aggregate value of bonds issued under New York law included some form of CAC1. The International Capital Markets Association (ICMA) published the first model CAC clause in 2014, which was revised in 2015. According to IMF data, 74% of all new sovereign bond issuances made between October 1, 2014 and October 31, 2016 included the ICMA clause, making it the market standard.2

Through the use of CACs, Argentina and Ecuador restructured approximately $65bn and $17.4bn respectively. For Argentina, there was no litigation filed by “holdouts” in connection with the restructuring, and for Ecuador there was one case in which the SDNY court upheld Ecuador’s use of the CAC. With the rise of CACs, disputes between sovereigns and creditors may occur less frequently in future restructurings, but it could give way, instead, to growing numbers of inter-creditor disputes.

International Arbitration Under IIAs

IIAs are bilateral or multilateral treaties concluded between States to offer certain rights and protections in their territory to foreign investors from other contracting States.

IIAs usually provide that investment disputes between a foreign investor and its host State can be resolved by an international arbitral tribunal. During past sovereign debt crises, creditors have frequently used IIA arbitration to challenge sovereign debt restructurings, and distressed sovereigns should be prepared for this to happen again.

Various arbitral tribunals interpreting IIAs in disputes relating to sovereign debt crises have found the agreement to include sovereign bonds within the scope of protected “investments”. In particular, Argentina’s prolonged sovereign debt crisis in the early 2000s triggered many significant investment arbitration disputes, including several cases brought by Italian bondholders. Similarly, the Hellenic Republic’s debt restructuring of 2012 gave rise to several investment treaty arbitrations, amongst which was the Poštová banka v. Hellenic Republic case.3

In the Argentine cases, the respondent State argued on each occasion, unsuccessfully, that the claimants did not have a protected “investment”. The tribunals in Fedax, Abaclat, Ambiente Ufficio and Alemanni all found that government debt instruments, including sovereign-issued promissory notes and instruments purchased in the secondary market, constitute an “investment” under the applicable bilateral investment treaty (BIT) and the ICSID Convention.4

Each of these decisions resulted from a case-by-case analysis rather than a sweeping rule. In contrast, the tribunal in Poštová banka found that interests in Greek government bonds do not qualify as protected investments under the Slovakia-Greece BIT, focusing on the specific wording of that investment treaty and the fact that its “investment” definition did not expressly refer to public debt or public obligations. The Poštová banka tribunal noted that sovereign debt cannot be equated to private indebtedness or corporate debt, since it is an instrument of government monetary and economic policy and an important tool for the handling of social and economic policies of a State.

More controversially, the Abaclat decision opened the door to a “mass” group of claimants, acting under a single BIT. Similarly, in 2020, the tribunal in Adamakopoulos v. Cyprus allowed a mass claim under the Greek-Cyprus and Belgium-Luxembourg-Cyprus investment treaties.5

Moreover, some recent investment agreements contain clauses explicitly limiting creditors’ ability to challenge sovereign debt restructurings through investment treaty arbitration6. This is likely to stem these kinds of claims in the future.

Enforcement

Asset enforcement is a key area of claimants’ litigation strategies. Even to the extent creditors are successful through litigation or arbitration, it does not always mean that they will get paid, particularly in the context of litigation against a sovereign. Sovereign immunity protects most State-owned assets from seizure. This includes properties held by diplomatic and consular missions of a sovereign abroad, and assets held by its central bank. However, and subject to local laws, sovereign immunity does not usually cover sovereigns’ assets used for commercial activities, potentially putting certain stakes in private companies or other commercial use property at risk.

Assets that leave the sovereign’s jurisdiction may be particularly at risk of seizure, which can lead to additional litigation in multiple jurisdictions. Attempting to seize extraterritorial assets can be a long and expensive process on both sides, however – sometimes with little to show for it at the end. Elliott Capital’s high profile 2012 capture of the Argentine naval ship ARA Libertad ultimately came to nothing, for example: the ship was released a few months later pursuant to an order of the International Tribunal for the Law of the Sea. The Supreme Court of Ghana separately confirmed thereafter that the ship had been improperly restrained and that “[t]here should accordingly be no further seizures of military assets of sovereign states by Ghanian courts”.

At a time when a sovereign debt crisis is looking increasingly likely in several parts of the world, it is important to learn lessons from past events like the Argentine and Euro crises. These trends we have outlined above look set to develop during 2022 and beyond.

Christopher P. Moore

Partner

London

T: +44 20 7614 2227

New York

T: +1 212 225 2836

cmoore@cgsh.com

V-Card

Laurie Achtouk‑Spivak

Counsel

Paris

T: +33 1 40 74 68 00

lachtoukspivak@cgsh.com

V-Card

Rathna Ramamurthi

Associate

Washington, D.C.

T: +1 202 974 1515

rramamurthi@cgsh.com

V-Card