Navigating an Increasingly Polarized ESG Landscape

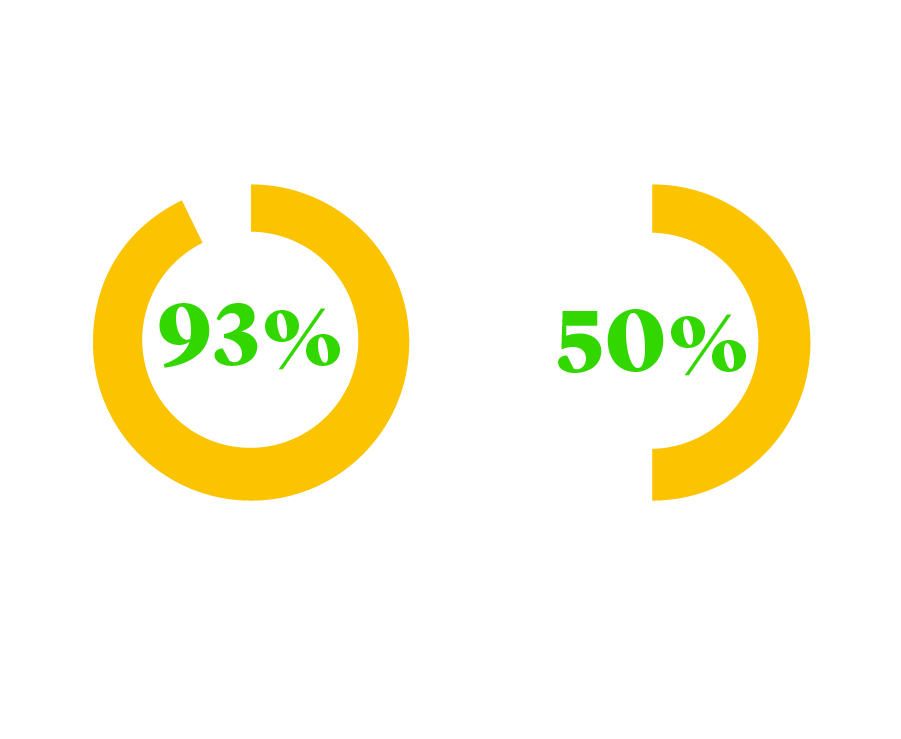

Pressure from investors over the past decade has persuaded many fund sponsors from around the world to create firm-wide ESG policies and, in many cases, to launch fund products where ESG considerations are integrated into investment decision making. A recent survey conducted by Bain & Company found that 93% of investors would walk away from an investment opportunity today if it represented an ESG concern, with 50% citing enhanced performance as a reason to insist on strong ESG credentials1. This trend was accelerated by the Inflation Reduction Act, which further incentivized ESG investing by including funding, programs and incentives to accelerate the transition to a clean energy economy.

But with the proliferation of ESG fund products has come the attention of regulators and legislators, both at the federal and state level. Sponsors currently managing or contemplating launching a product with an ESG angle or focus will need to consider any restrictions that may apply to the product’s targeted investor base (particularly pension plan investors). They will also need to assess how the product will fit within all applicable ESG frameworks, which may in some respects create tensions between a sponsor’s fundraising professionals and its legal and compliance department. Threading that needle may require careful tailoring of strategies and related fund disclosure. Set forth below is an overview of the current ESG regulatory landscape in the U.S. and suggestions on steps sponsors can take now to ease friction in fundraising as the situation continues to evolve.

Pressure from investors over the past decade has persuaded many fund sponsors from around the world to create firm-wide ESG policies and, in many cases, to launch fund products where ESG considerations are integrated into investment decision making. A recent survey conducted by Bain & Company found that 93% of investors would walk away from an investment opportunity today if it represented an ESG concern, with 50% citing enhanced performance as a reason to insist on strong ESG credentials1. This trend was accelerated by the Inflation Reduction Act, which further incentivized ESG investing by including funding, programs and incentives to accelerate the transition to a clean energy economy.

But with the proliferation of ESG fund products has come the attention of regulators and legislators, both at the federal and state level. Sponsors currently managing or contemplating launching a product with an ESG angle or focus will need to consider any restrictions that may apply to the product’s targeted investor base (particularly pension plan investors). They will also need to assess how the product will fit within all applicable ESG frameworks, which may in some respects create tensions between a sponsor’s fundraising professionals and its legal and compliance department. Threading that needle may require careful tailoring of strategies and related fund disclosure. Set forth below is an overview of the current ESG regulatory landscape in the U.S. and suggestions on steps sponsors can take now to ease friction in fundraising as the situation continues to evolve.

Federal ESG Regulation

Securities and Exchange Commission (SEC)

The SEC’s approach to ESG regulation in the context of private funds is focused on disclosure and the elimination of greenwashing. To that end, the SEC proposed a new rule last year that would create additional questions and other disclosure obligations in a sponsor’s Form ADV relating to ESG investing2. Those questions would effectively create four ESG categories for private funds: non-ESG; ESG integration; ESG-focused; and ESG impact, which loosely correspond to Article 6, 8, “8+” and 9 funds under the EU’s Sustainable Finance Disclosure Regulation (SFDR). An adopting release with respect to these changes is expected later this year.

Department of Labor (DOL)

The U.S. DOL is responsible for issuing guidance under the Employment Retirement Income Security Act (ERISA), which is the federal law that sets forth the rules for investing and managing the assets of private pension plans. Through the years, the DOL has issued quite a bit of guidance regarding the extent to which ESG factors can be considered by fiduciaries to such plans. This guidance has varied largely in lockstep with the political leanings of the presidential administration. Under the Trump administration, the DOL adopted a rule that prohibited ERISA fiduciaries from considering any non-pecuniary factors in selecting plan investments. In November 2022, the DOL under the Biden administration replaced the Trump-era guidance with a new rule providing that, when making investment decisions, an ERISA fiduciary must reasonably determine which factors are relevant to a risk and return analysis and these factors may, but need not, include ESG considerations.

The new rule has been viewed as largely more permissive than its predecessor with respect to the consideration of ESG factors and has been (and continues to be) the subject of challenges on various fronts. U.S. legislators passed a bill to overturn the new rule, and President Biden used his first veto to keep the new rule in place. In addition, a group of 25 Republican state attorneys general (AGs) have filed suit in the U.S. District Court for the Northern District of Texas, Amarillo division, seeking to have the new rule invalidated. Although the U.S. Supreme Court has not previously opined on the consideration of ESG factors by fiduciaries, it has indicated a contrarian stance to ESG generally, recently ruling against the U.S. Environmental Protection Agency’s authority in two cases, West Virginia v. EPA and Sackett v. EPA.

Federal ESG Regulation

Securities and Exchange Commission (SEC)

The SEC’s approach to ESG regulation in the context of private funds is focused on disclosure and the elimination of greenwashing. To that end, the SEC proposed a new rule last year that would create additional questions and other disclosure obligations in a sponsor’s Form ADV relating to ESG investing2. Those questions would effectively create four ESG categories for private funds: non-ESG; ESG integration; ESG-focused; and ESG impact, which loosely correspond to Article 6, 8, “8+” and 9 funds under the EU’s Sustainable Finance Disclosure Regulation (SFDR). An adopting release with respect to these changes is expected later this year.

Department of Labor (DOL)

The U.S. DOL is responsible for issuing guidance under the Employment Retirement Income Security Act (ERISA), which is the federal law that sets forth the rules for investing and managing the assets of private pension plans. Through the years, the DOL has issued quite a bit of guidance regarding the extent to which ESG factors can be considered by fiduciaries to such plans. This guidance has varied largely in lockstep with the political leanings of the presidential administration. Under the Trump administration, the DOL adopted a rule that prohibited ERISA fiduciaries from considering any non-pecuniary factors in selecting plan investments. In November 2022, the DOL under the Biden administration replaced the Trump-era guidance with a new rule providing that, when making investment decisions, an ERISA fiduciary must reasonably determine which factors are relevant to a risk and return analysis and these factors may, but need not, include ESG considerations.

The new rule has been viewed as largely more permissive than its predecessor with respect to the consideration of ESG factors and has been (and continues to be) the subject of challenges on various fronts. U.S. legislators passed a bill to overturn the new rule, and President Biden used his first veto to keep the new rule in place. In addition, a group of 25 Republican state attorneys general (AGs) have filed suit in the U.S. District Court for the Northern District of Texas, Amarillo division, seeking to have the new rule invalidated. Although the U.S. Supreme Court has not previously opined on the consideration of ESG factors by fiduciaries, it has indicated a contrarian stance to ESG generally, recently ruling against the U.S. Environmental Protection Agency’s authority in two cases, West Virginia v. EPA and Sackett v. EPA.

U.S. State Level Activity

Division Among the States Along Party Lines

It is at the state level that discord has really taken hold, with a widening gulf between those taking a pro- and anti-ESG stance. State and local pension plans, while outside the scope of ERISA, are subject to state laws (which are often analogous to ERISA) and, as a result, to the whims of state governors, legislators and AGs, who are well positioned to push through legislation that reflects their political views. On March 16, 2023, in response to President Biden’s pending veto of the Congressional bill to overturn the new DOL rule, 19 Republican governors signed a pact to fight the Biden administration’s perceived ESG agenda by adopting their own anti-ESG legislation3.

Anti-ESG Legislation

Anti-ESG legislation generally takes one of two forms: legislation that in some way prohibits fiduciaries from using ESG criteria in making investment decisions for state plans; and anti-boycott legislation that prohibits fiduciaries from investing state plan money in a fund or with a fund sponsor that “boycotts” industries like fossil fuels and gun manufacturing. Prohibitive ESG legislation often mirrors the Trump-era DOL rule, requiring state plan fiduciaries to consider only pecuniary and not ESG factors. Approximately 20 states have adopted some form of anti-ESG legislation so far.

Other State AG Activity

In addition to fighting the DOL rule in federal court, many state AGs have embarked on an anti-ESG letter writing campaign to threaten asset managers. On March 30, 2023, 21 state AGs sent a letter to 53 top asset managers raising concerns about their proxy voting on ESG issues and questioning their involvement in ESG initiatives like Climate Action 100+ and the Net Zero Asset Managers Initiative. More recently, multiple state AGs have sent civil investigative demands and subpoenas to asset managers to gather additional information regarding their involvement in ESG initiatives and how they cast ESG-related proxy votes.

U.S. State Level Activity

Division Among the States Along Party Lines

It is at the state level that discord has really taken hold, with a widening gulf between those taking a pro- and anti-ESG stance. State and local pension plans, while outside the scope of ERISA, are subject to state laws (which are often analogous to ERISA) and, as a result, to the whims of state governors, legislators and AGs, who are well positioned to push through legislation that reflects their political views. On March 16, 2023, in response to President Biden’s pending veto of the Congressional bill to overturn the new DOL rule, 19 Republican governors signed a pact to fight the Biden administration’s perceived ESG agenda by adopting their own anti-ESG legislation3.

Anti-ESG Legislation

Anti-ESG legislation generally takes one of two forms: legislation that in some way prohibits fiduciaries from using ESG criteria in making investment decisions for state plans; and anti-boycott legislation that prohibits fiduciaries from investing state plan money in a fund or with a fund sponsor that “boycotts” industries like fossil fuels and gun manufacturing. Prohibitive ESG legislation often mirrors the Trump-era DOL rule, requiring state plan fiduciaries to consider only pecuniary and not ESG factors. At least 13 states have adopted some form of anti-ESG legislation so far.

Other State AG Activity

In addition to fighting the DOL rule in federal court, many state AGs have embarked on an anti-ESG letter writing campaign to threaten asset managers. On March 30, 2023, 21 state AGs sent a letter to 53 top asset managers raising concerns about their proxy voting on ESG issues and questioning their involvement in ESG initiatives like Climate Action 100+ and the Net Zero Asset Managers Initiative. More recently, multiple state AGs have sent civil investigative demands and subpoenas to asset managers to gather additional information regarding their involvement in ESG initiatives and how they cast ESG-related proxy votes.

Proxy Voting

On March 30, 2023, 21 state AGs sent a letter to 53 top asset managers raising concerns about their proxy voting on ESG issues and questioning their involvement in ESG initiatives.

Walking the Line

It is important to note that many of the state ESG-related laws are generally drafted to regulate “investment managers” and “fiduciaries” to state plans, not the investment advisers that manage the commingled funds in which they invest, which instead have a fiduciary duty to the fund as a whole and not to particular investors. From a fund manager’s perspective, state laws are relevant because they inform how state plans, a critical segment of potential investors, will make decisions about which funds they invest in. Despite this distinction, some states are pushing the general partners (GPs) and managers of the funds in which their state plans have invested or may invest to provide various assurances and representations that the fund will be managed in accordance with that particular state’s ESG objectives. In order to facilitate fundraising, private fund sponsors should consider what steps they can take now to help minimize friction both between federal and state legislation, and between pro- and anti-state approaches to ESG. Sponsors should also consider the ideal level of flexibility to maintain with respect to their approach to ESG, as the political and regulatory environment continues to evolve.

Walking the Line

It is important to note that many of the state ESG-related laws are generally drafted to regulate “investment managers” and “fiduciaries” to state plans, not the investment advisers that manage the commingled funds in which they invest, which instead have a fiduciary duty to the fund as a whole and not to particular investors. From a fund manager’s perspective, state laws are relevant because they inform how state plans, a critical segment of potential investors, will make decisions about which funds they invest in. Despite this distinction, some states are pushing the general partners (GPs) and managers of the funds in which their state plans have invested or may invest to provide various assurances and representations that the fund will be managed in accordance with that particular state’s ESG objectives. In order to facilitate fundraising, private fund sponsors should consider what steps they can take now to help minimize friction both between federal and state legislation, and between pro- and anti-state approaches to ESG. Sponsors should also consider the ideal level of flexibility to maintain with respect to their approach to ESG, as the political and regulatory environment continues to evolve.

Below are six steps Private Fund Sponsors can take now to help avoid ESG headaches later:

Fiduciary Status: Avoid agreeing in side letters to fiduciary status under state law with respect to any public pension plans. Agreeing to such a status may result in applicability of the state ESG rules and restrictions to the fund’s GP and/or manager, where such rules would not otherwise apply. Consider instead offering alternative comfort regarding the general protections afforded by fiduciary status to the fund under partnership law and the Advisers Act. Private fund sponsors should consult with legal counsel on how to address these issues in the context of “funds of one” with public pension plans.

Marketing Materials and Form ADV: To the extent that any disclosure by the sponsor includes a discussion of how the sponsor and its advisory affiliates incorporate ESG factors into investment decisions, such disclosure should be carefully reviewed by legal counsel.

Expense Provisions: Review disclosure regarding ESG-related expenses in the fund’s organizational and disclosure documents with legal counsel to ensure consistency with the fund’s ESG approach.

Fund Name: Consider the potential implications of using ESG-related buzz words, such as “ESG,” “impact” and “climate,” in the name of a new fund. Though these naming conventions have become popular in terms of marketing a fund, care should be given to not overstate the investment thesis and risk-return profile of a particular fund, and thereby put the fund squarely in the crosshairs of regulators.

Internal Awareness: Educate fundraising professionals about the sensitivities in investor communications regarding ESG. Investor relations and business teams should consult with legal and compliance to ensure that all ESG-related communications are consistent with the fund disclosure and internal ESG policies and procedures.

Due Diligence Requests: Draft a standard response to ESG-related due diligence questions for ERISA and public pension plan investors. Not only will this create efficiencies in the due diligence process, but it will also help ensure that consistent disclosures are provided across the fund’s investor base.

Where Next?

It remains to be seen how the political battle over ESG will play out. A recent study by Coller Capital indicates that only 4% of investors expect a large number of GPs will deprioritize ESG as a result of the anti-ESG movement in the U.S.4. But for now, at least, ESG continues to be a polarizing issue in the U.S., creating a great deal of uncertainty and complexity for private fund sponsors who should work with their legal counsel to navigate this evolving landscape with care.

Michael J. Albano

Partner

New York

T: +1 212 225 2438

malbano@cgsh.com

V-Card

Elizabeth Dyer

Partner

New York

T: +1 212 225 2170

edyer@cgsh.com

V-Card