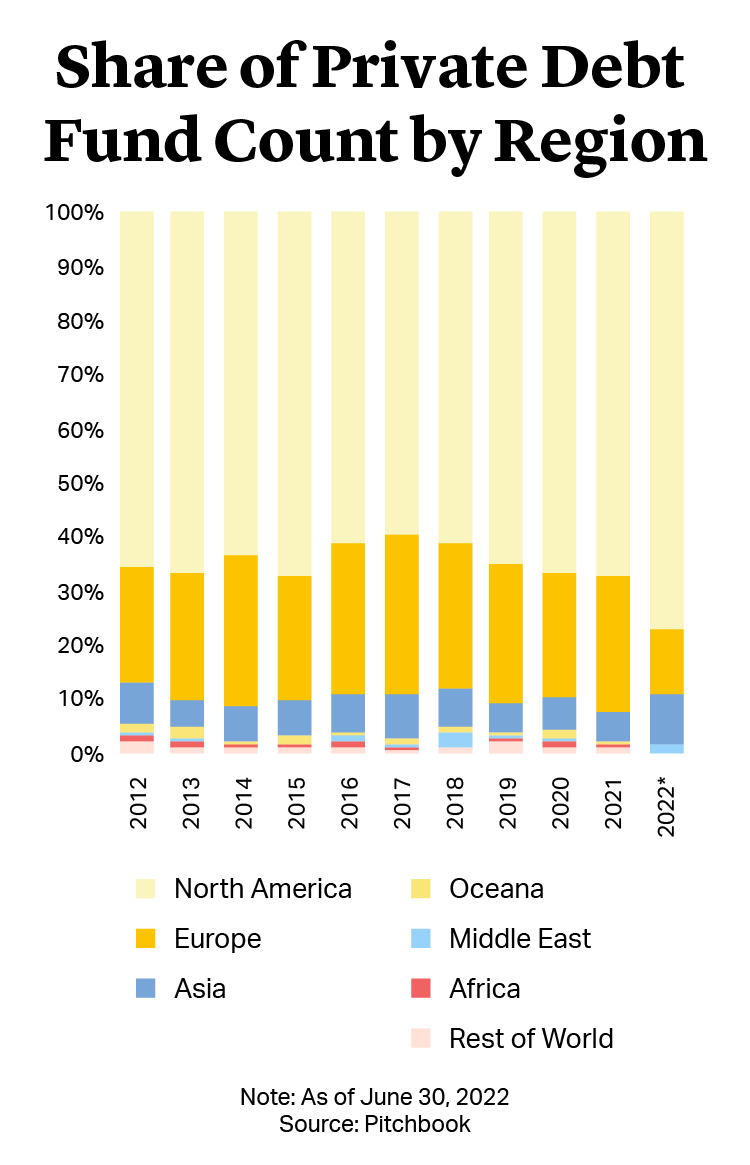

Asia Pacific Private Debt: An Industry Poised for Growth

From international giants to local players that have come of age, private equity investors of all stripes are jostling for position in a relatively young Asia Pacific private debt industry that is now poised for growth.

Large global sponsors have made decisive moves in this space in the last 12 months, including: Apollo, which recently launched its Asia Pacific credit strategy with $1.25bn1, KKR, which raised $1.1bn for its inaugural Asia credit fund2, and Blackstone, which is seeking an additional $4.5bn for its Asia Pacific private credit business3.

At the same time, experienced local buyout managers such as MBK Partners and PAG have broadened their horizons with private debt offerings. MBK Partners raised its second private debt special situations fund with $1.8bn of commitments last year, a marked step-up from its $850mn predecessor.

$1.8bn

MBK Partners raised its second private debt special situations fund with $1.8bn of commitments last year, a marked step-up from its $850mn predecessor

An Evolving Market

In some ways, the evolution of the Asia Pacific private debt market was inevitable and has been similar to the development of other alternatives, where Asia has generally tracked the path of the U.S. and European markets in a compressed timeframe. The U.S. and European private debt industries grew significantly during the years following the Global Financial Crisis. While the capitalization of banks in Asia Pacific has generally held up well during the pandemic, the region is nonetheless facing a tightening of banking requirements in several markets, notably Australia and South Korea, as regulations increase capital costs against sub-investment grade lending4.

Meanwhile, banks across the region also continue to focus their attention on large corporates, leaving a pronounced lending gap for SMEs. Indeed, a lack of access to finance has long been a challenge facing SMEs, especially in the Asia Pacific region, which represents a significant portion of the multi-trillion dollar global funding gap5.

The Private Debt Edge

By contrast, private debt is often utilized for smaller borrowers. Private debt providers, including private equity firms, are also actively catering to the needs of borrowers in Asia Pacific, developing flexible structures such as the ever popular unitranche and accordion facilities that accommodate follow-on acquisitions, where a bank would typically need to renegotiate a pre-existing loan.

Well capitalized local sovereign and institutional investors make logical partners for these global players, with their ‘on the ground’ presence and regional expertise. KKR, for example, entered into a strategic partnership with Mubadala and Apollo partnered with Australian superannuation fund Hostplus. The National Pension Service of Korea, meanwhile, has also disclosed plans to form a separate debt team as it steps up its activity in the space.

At the same time, Asia Pacific’s domestic private markets industry is flourishing. Populated by a number of spinouts from investment banks and international firms, the local share of fundraising has grown exponentially over the years6. A number of leading firms in the region have reached a point in their maturation where they are looking to expand their platforms – again mirroring trends we have seen elsewhere in the world. It is logical for a private equity firm interacting daily with SME businesses to add a debt solution to its equity offering.

And, for now at least, the competitive dynamics remain attractive for new entrants.

Well capitalized local sovereign and institutional investors make logical partners for these global players, with their ‘on the ground’ presence and regional expertise. KKR, for example, entered into a strategic partnership with Mubadala and Apollo partnered with Australian superannuation fund Hostplus. The National Pension Service of Korea, meanwhile, has also disclosed plans to form a separate debt team as it steps up its activity in the space.

At the same time, Asia Pacific’s domestic private markets industry is flourishing. Populated by a number of spinouts from investment banks and international firms, the local share of fundraising has grown exponentially over the years6. A number of leading firms in the region have reached a point in their maturation where they are looking to expand their platforms – again mirroring trends we have seen elsewhere in the world. It is logical for a private equity firm interacting daily with SME businesses to add a debt solution to its equity offering.

And, for now at least, the competitive dynamics remain attractive for new entrants.

A Bright Future for Asia Pacific Private Debt

It is still early days, of course. In the first three quarters of 2022, total capital raised by private debt funds globally exceeded $172bn7. As of September 2022, APAC-focused private debt funds had raised $6.7bn8. But the tide is turning. Asia Pacific-based private debt AUM has grown at an average rate of 29% over the past five years compared to the global average of 17%. Active fund managers for private debt in the Asia Pacific region also increased from 249 in 2018 to 382 by September 2022, an impressive 53% jump9.

Furthermore, in the first half of 2022 private debt fundraising in Asia Pacific exceeded that in Europe for the first time10. Corporates in the region are also becoming ever more sophisticated, seeking out alternative channels to raise capital without equity dilution, while private equity firms are adopting increasingly complex capital structures to enhance their returns. Indeed, all the indications are that Asia Pacific private credit is a market set for significant growth.

31.5x

Asia had an estimated ratio of 31.5x for private equity to private debt AUM in 2021, compared to a much tighter 5.3x and 3.8x in the U.S. and Europe respectively

Chris C. Lee

Partner

Hong Kong

T: +852 2532 7477

chrlee@cgsh.com

V-Card

Kenneth S. Blazejewski

Partner

New York

T: +1 212 225 2729

kblazejewski@cgsh.com

V-Card

Jamal Fulton

Partner

New York

T: +1 212 225 2988

jfulton@cgsh.com

V-Card