Five years ago, in a now-famous TED Talk, Bill Gates described a global pandemic as one of the greatest threats to an ill-prepared world. In 2020, his warning hit home when governments were forced to take unprecedented steps to protect public health, effectively putting their economies into recession in the process. As countries deal with the enormous health and economic repercussions of COVID-19, the result has been to shine a light on the strengths and weaknesses of healthcare in Europe and around the globe, and spark national and international debate on the delivery and protection of healthcare services, drugs and equipment.

For the past decade, healthcare has become an increasingly important part of the private equity investment universe – from early-stage biotech funding and buyouts of multinational makers of over-the-counter health and beauty products, to deals for care homes and medical device manufacturers.

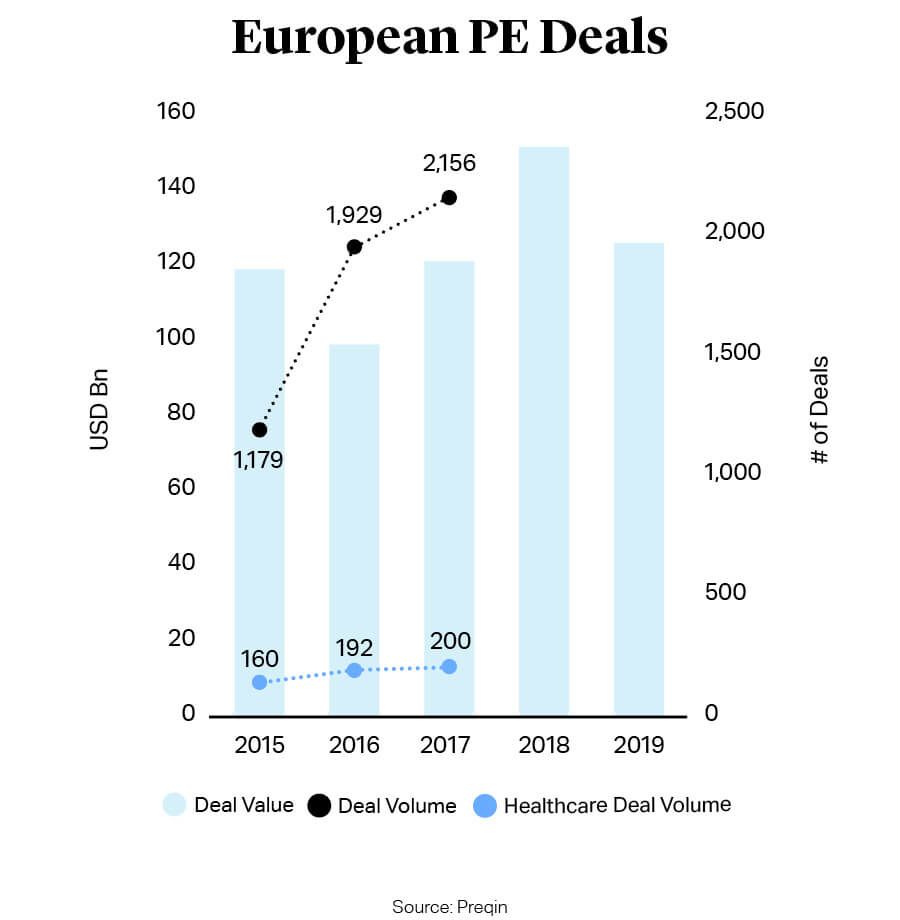

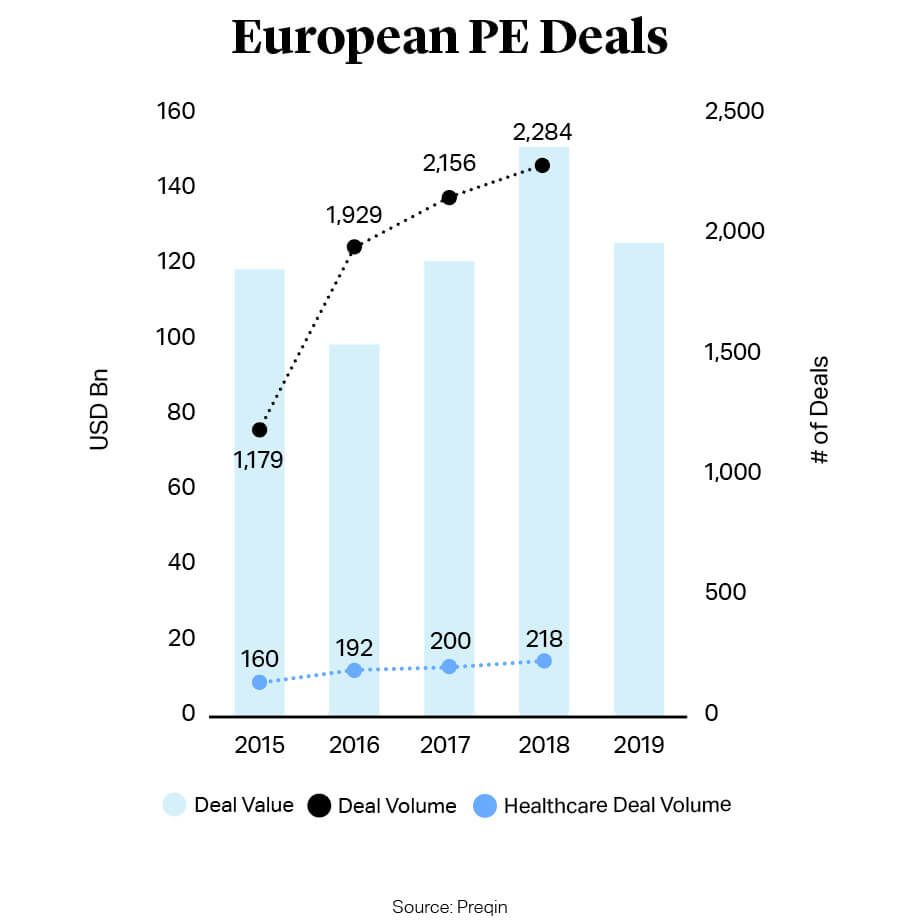

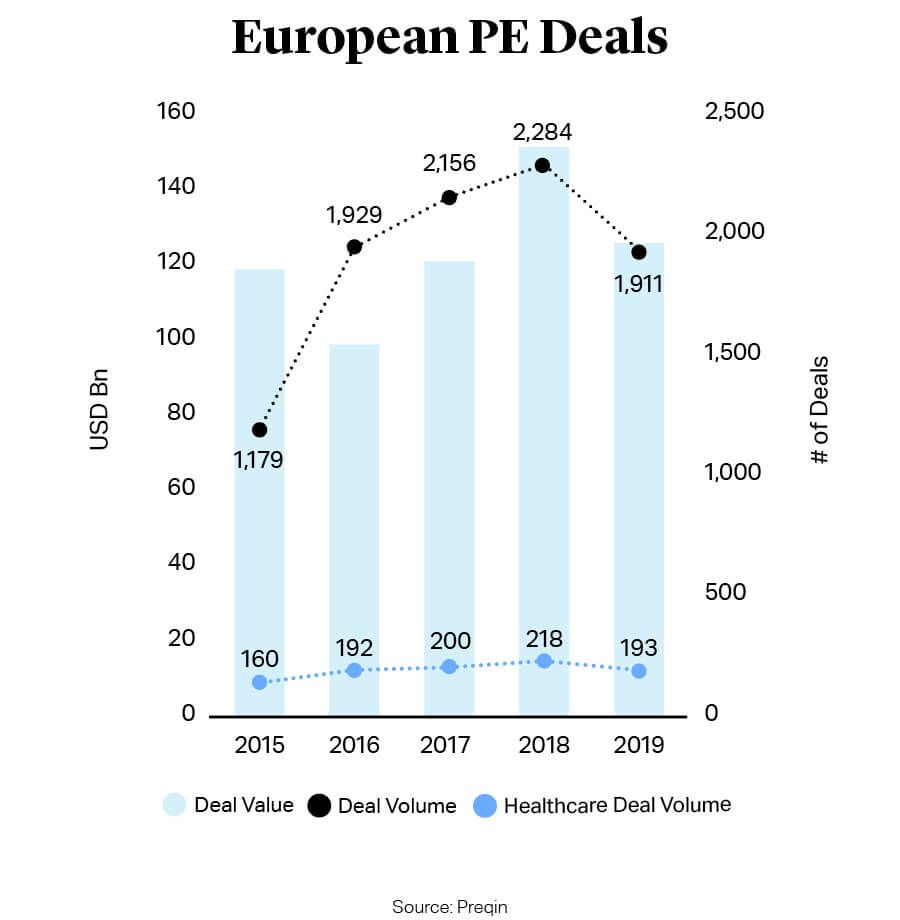

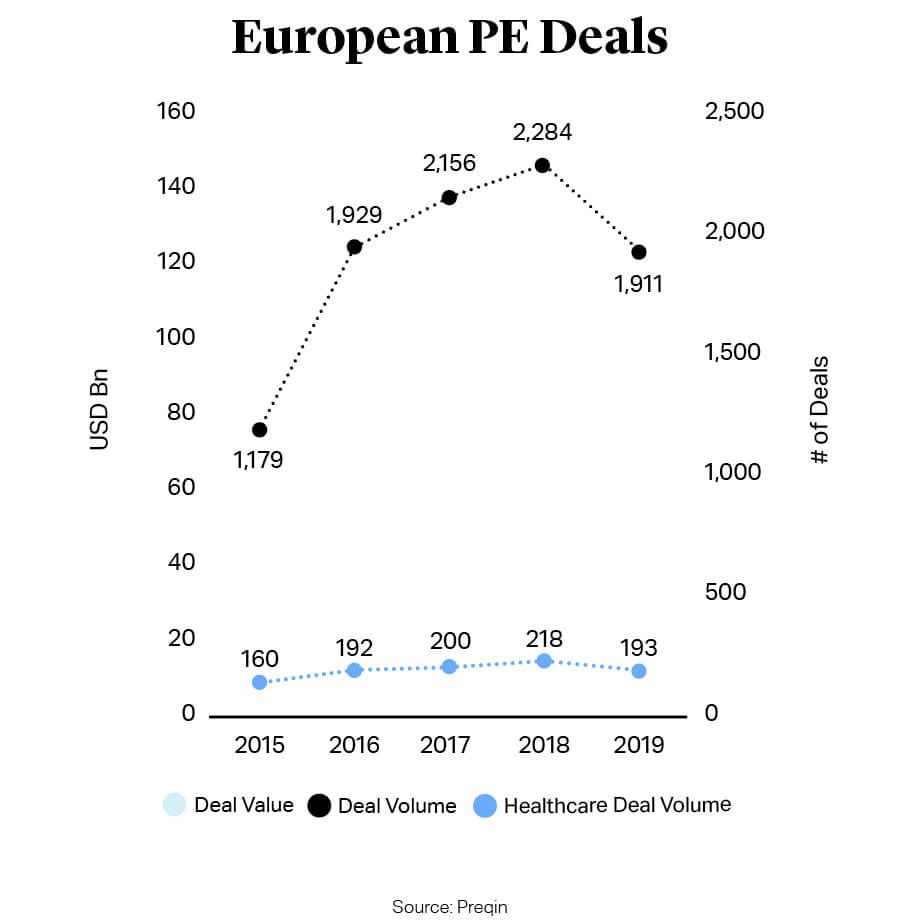

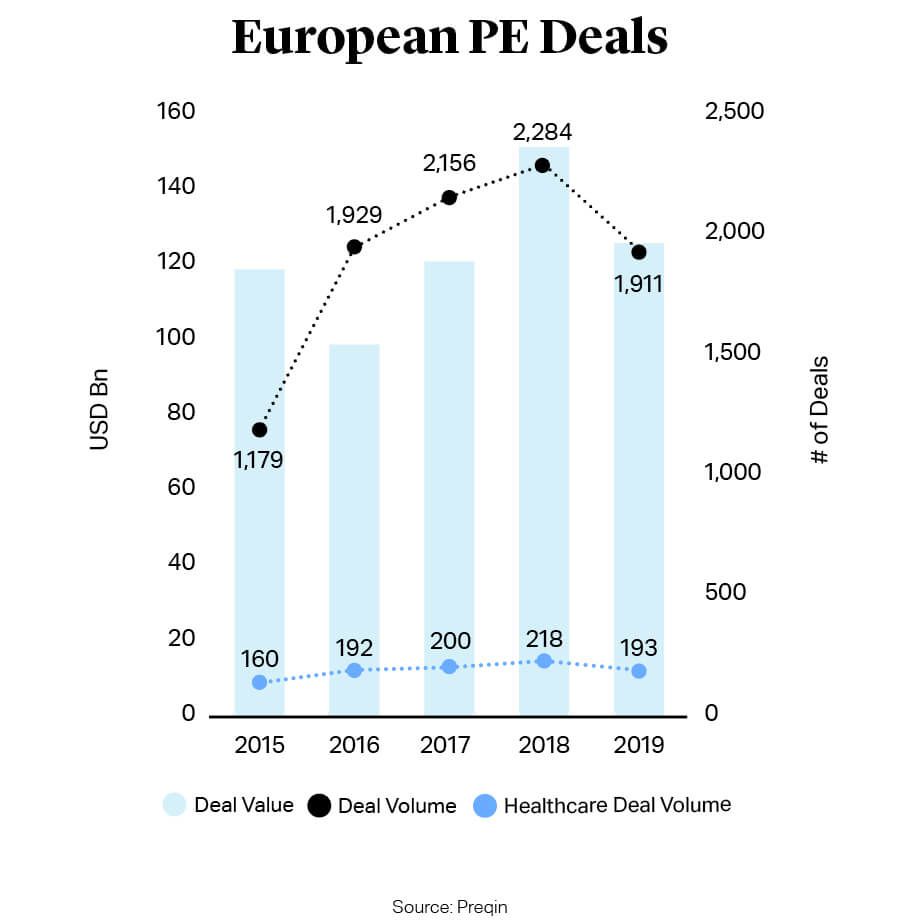

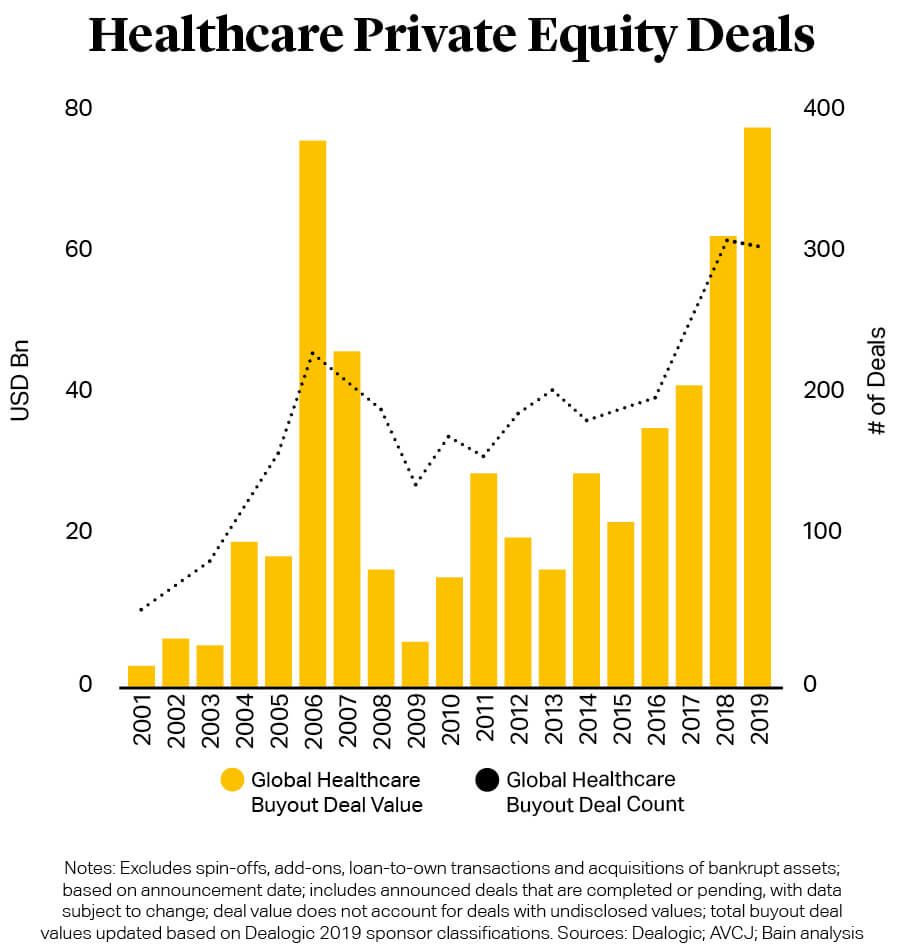

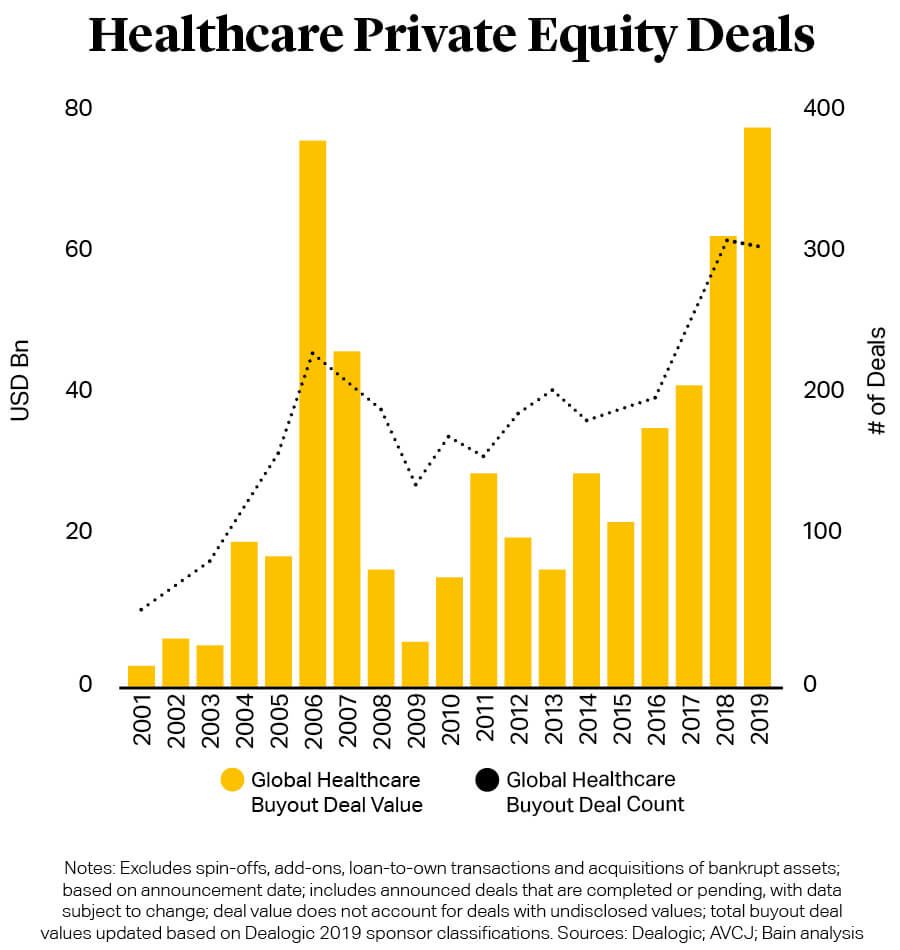

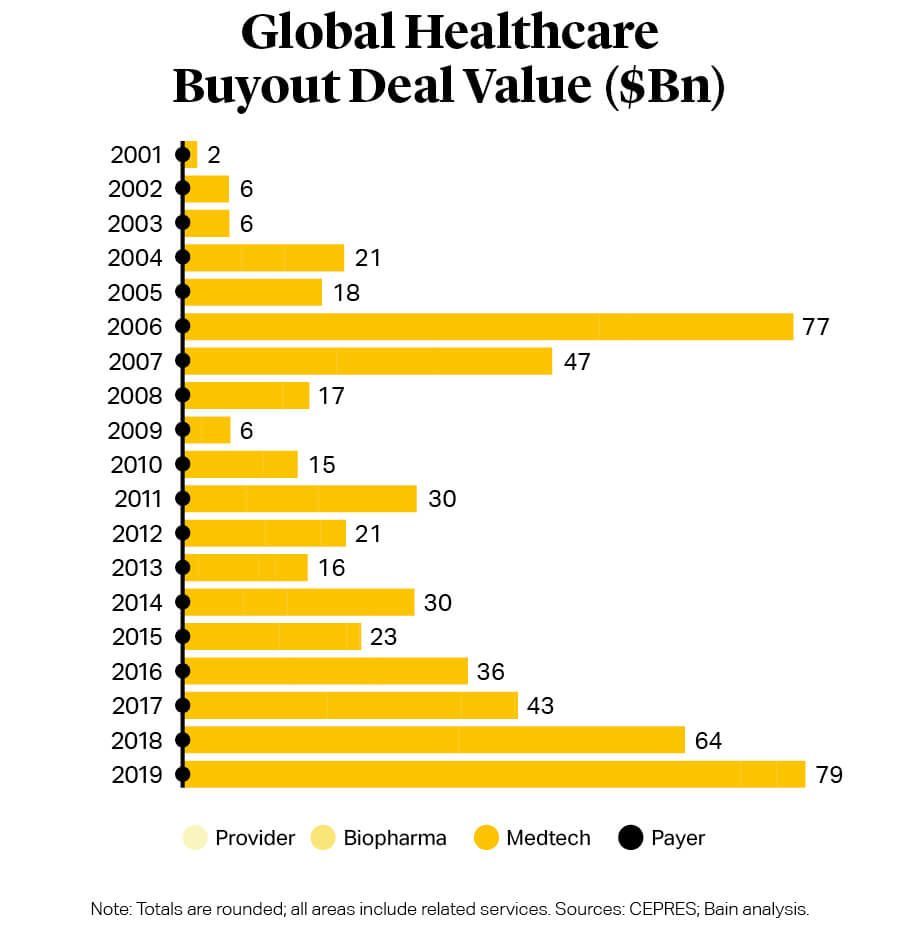

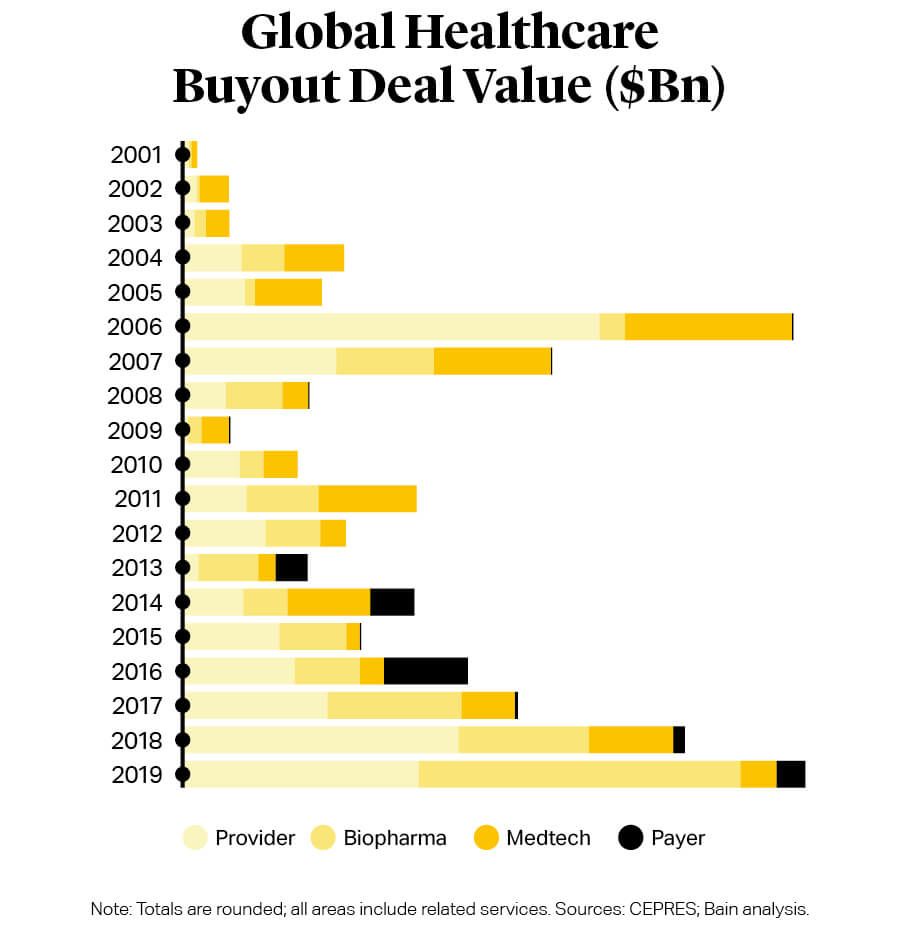

Private equity investment in healthcare in Europe rose to a record $19.7 billion in 2019, up from $17.8 billion the previous year, according to Bain & Co. The increase came as overall private equity investment volume slowed due to rising fears of an economic downturn – European private equity investment declined 17% in 2019 to $125.1 billion, Preqin data showed. It is a clear demonstration of healthcare’s increasing prominence in private equity portfolios, accounting for over 15% of private equity investment today compared with around 10% at the start of the decade{{1}}{{{Global Healthcare Private Equity and Corporate M&A Report 2020</br>Source: Bain}}}.

The healthcare sector is driven by long-term macro trends, including ageing populations in developed economies, and rising disposable incomes in emerging markets{{2}}{{{World Economic Outlook</br>Source: IMF}}}. The sector is also characterised by inefficiencies in the delivery of healthcare services and so is ripe for disruption through technology. This provides opportunities for private equity sponsors looking to deploy their capital and considerable expertise.

But healthcare investment is not without its challenges. Europe, and the emerging markets that attract private equity investment through the European offices of private equity sponsors, present a patchwork of different models, from tax-funded healthcare systems that predominate in the UK and Scandinavian countries (and which may resist the entry of private capital in some segments of healthcare delivery), to schemes backed by compulsory insurance in the Netherlands, to hybrid models combining public and private funding in France and Germany. In some emerging markets, lower levels of government investment in healthcare has led to a growth in privately owned and run hospitals and other healthcare providers. Asset prices are driven up by competition between private equity sponsors and industry players with strong balance sheets. Regulatory scrutiny is also on the increase as national protectionism grows and governments seek to take tighter control of critical healthcare supplies, access to potential vaccines and intellectual property.

In this report, we delve deeper into opportunities for private equity in Europe and emerging markets, particularly at the intersection of technology and healthcare, as well as biopharma product development. We also highlight the risks from regulatory oversight and suggest some key due diligence considerations for acquirers. In doing so, we reveal a dynamic sector in which we expect to see continued strong appetite from sponsors.

The healthcare sector is driven by long-term macro trends, including ageing populations in developed economies, and rising disposable incomes in emerging markets{{2}}{{{World Economic Outlook

Source: IMF}}}. The sector is also characterised by inefficiencies in the delivery of healthcare services and so is ripe for disruption through technology. This provides opportunities for private equity sponsors looking to deploy their capital and considerable expertise.

But healthcare investment is not without its challenges. Europe, and the emerging markets that attract private equity investment through the European offices of private equity sponsors, present a patchwork of different models, from tax-funded healthcare systems that predominate in the UK and Scandinavian countries (and which may resist the entry of private capital in some segments of healthcare delivery), to schemes backed by compulsory insurance in the Netherlands, to hybrid models combining public and private funding in France and Germany. In some emerging markets, lower levels of government investment in healthcare has led to a growth in privately owned and run hospitals and other healthcare providers. Asset prices are driven up by competition between private equity sponsors and industry players with strong balance sheets. Regulatory scrutiny is also on the increase as national protectionism grows and governments seek to take tighter control of critical healthcare supplies, access to potential vaccines and intellectual property.

In this report, we delve deeper into opportunities for private equity in Europe and emerging markets, particularly at the intersection of technology and healthcare, as well as biopharma product development. We also highlight the risks from regulatory oversight and suggest some key due diligence considerations for acquirers. In doing so, we reveal a dynamic sector in which we expect to see continued strong appetite from sponsors.

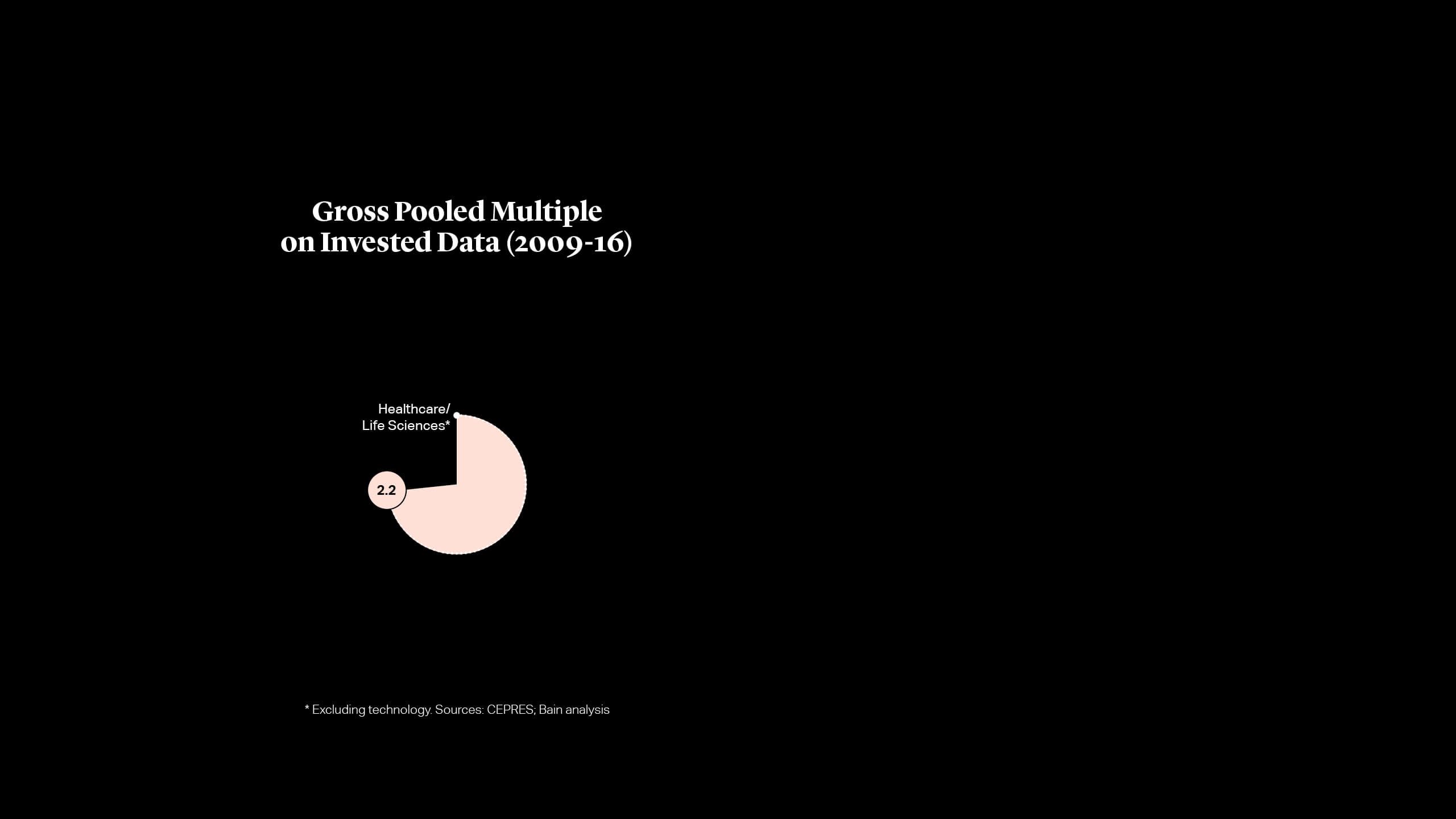

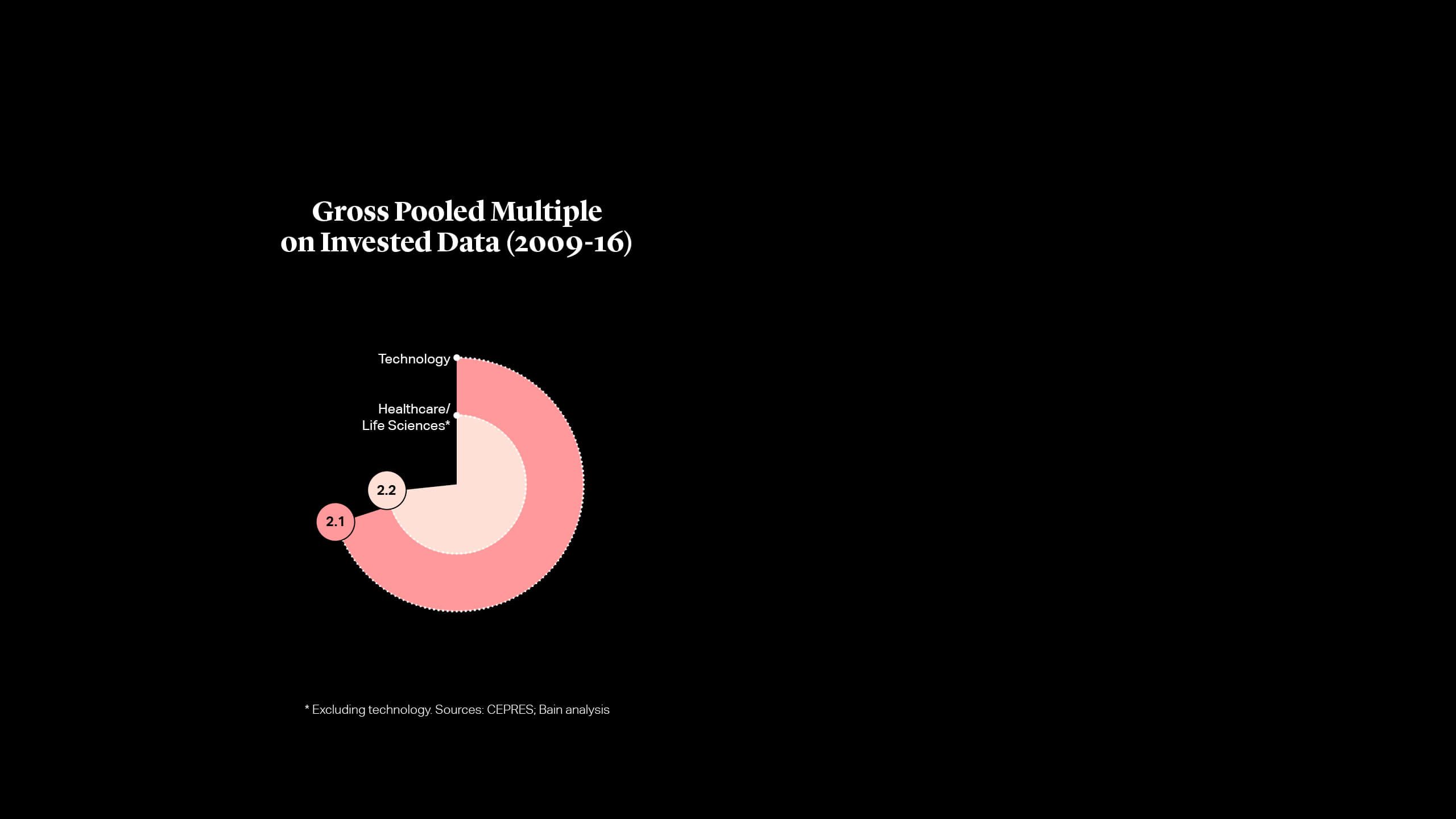

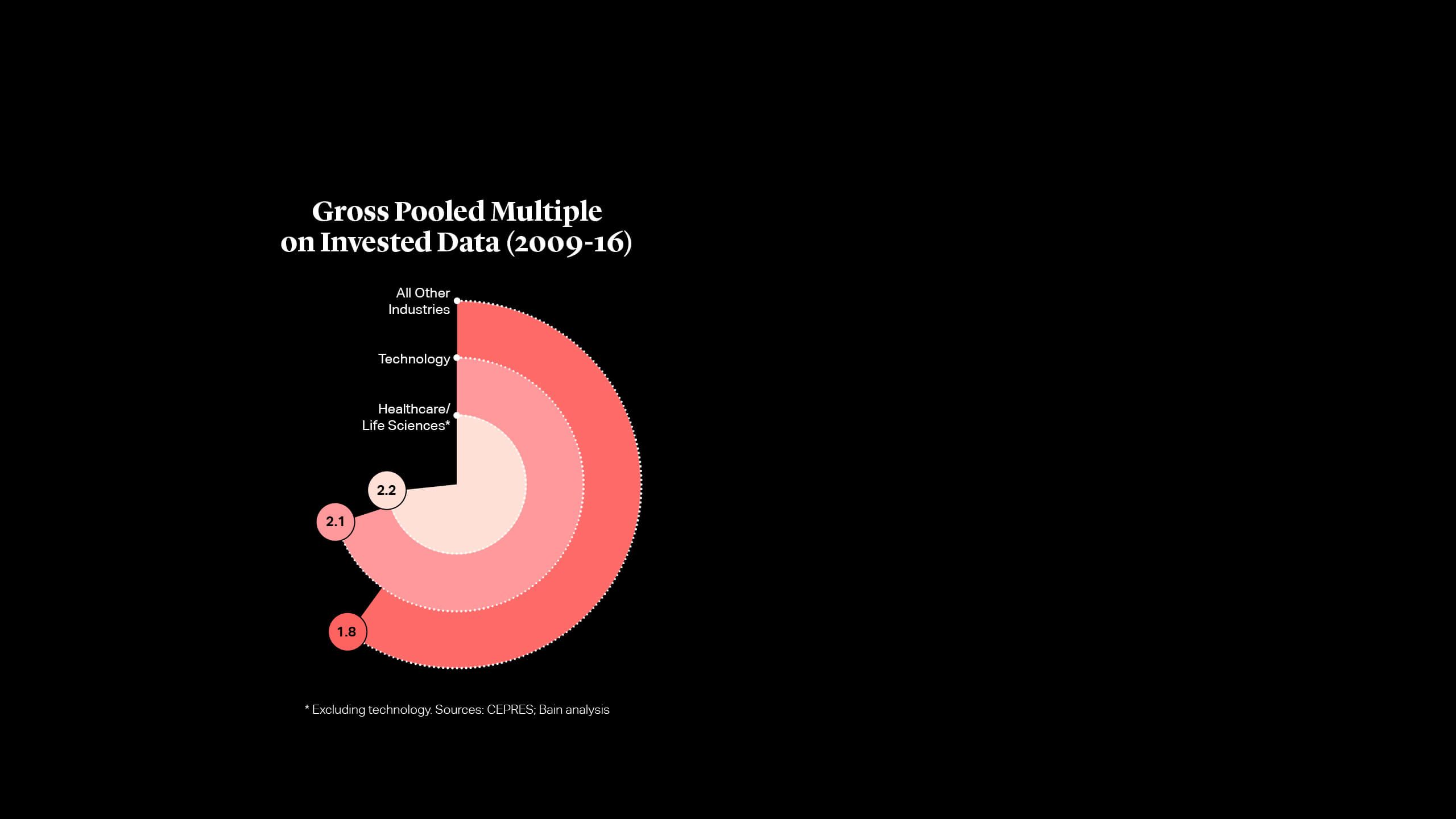

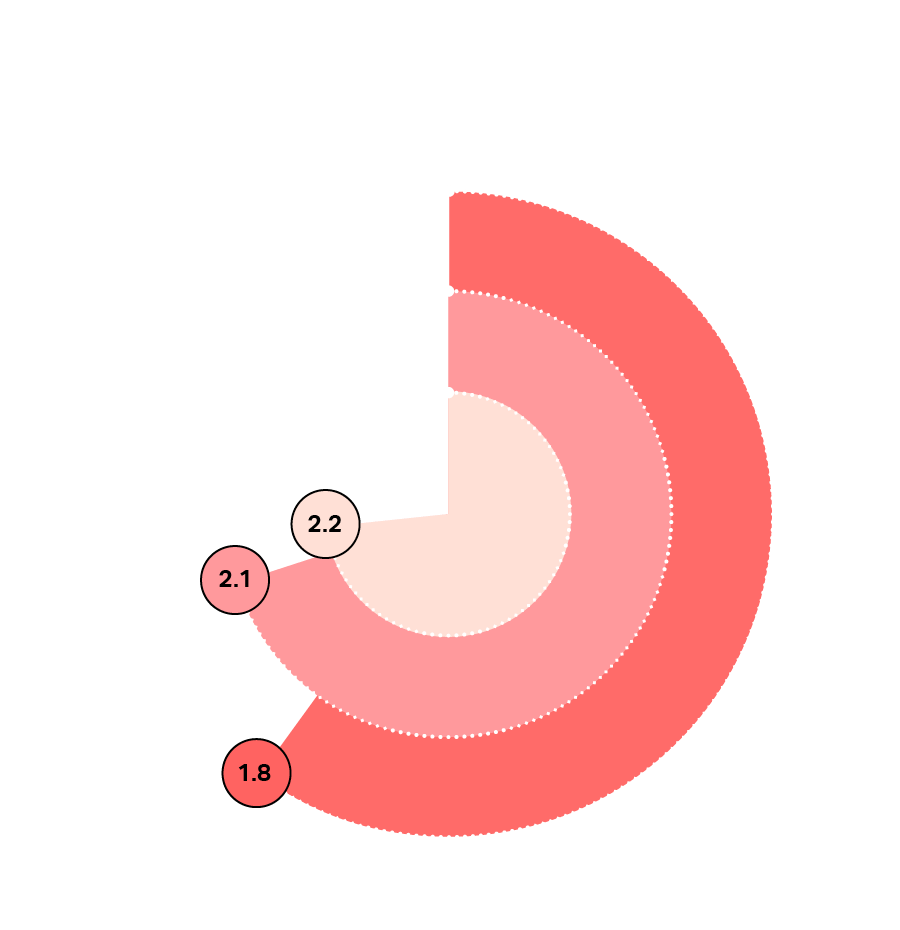

Alongside healthcare, technology companies have long been a focus for private equity investment globally, and technology has proved to be one of the best returning sectors. According to analysis by Bain & Co of CEPRES data, healthcare deals generated 2.2 times capital invested and tech 2.1 times, while all other sectors produced a combined return of 1.8 times (multiple of capital invested, 2009-2016){{3}}{{{Global Healthcare Private Equity and Corporate M&A Report 2020</br>Source: Bain}}}.

Global private equity investment in healthcare tech doubled last year to $17.5 billion from $8.6 billion in 2018, according to Bain & Co{{4}}{{{Global Healthcare Private Equity and Corporate M&A Report 2020</br>Source: Bain}}}. This growth was led by a buoyant US market and the takeover of health survey business Press Ganey for a reported figure of over $4 billion{{5}}{{{EQT and CPPIB to acquire a majority equity stake in Waystar in transaction valued at $2.7 billion</br>Source: PR Newswire}}} by a consortium headed by Leonard Green. Capital is also increasingly targeting new technologies in Europe, such as Eurazeo’s €300 million deal for Dutch Ophthalmic Research Centre, a maker of hi-tech equipment for eye surgeries.

The Move to New IT Systems

The WannaCry ransomware attack on older Windows operating systems in 2017 exposed the vulnerability of outdated healthcare IT when it wreaked havoc on the UK’s NHS, where many trusts and other entities still relied on IT going back to the early 2000s. The NHS put the total cost of the attack at about £92 million{{6}}{{{WannaCry cyber-attack cost the NHS £92m after 19,000 appointments were cancelled</br>Source: National Health Executive}}}, and in 2019 admitted that more than 2,000 computers were still running on software that was two decades old{{7}}{{{NHS still running Windows XP on over 2,000 computers despite spate of cyber attacks</br>Source: CityAM}}}.

As healthcare systems digitise information, there are opportunities for private equity in back-end IT, as well as more innovative apps, such as those making it easier for patients to book hospital and GP appointments. Last year, for instance, Investcorp took a majority stake in Cambio{{8}}{{{Investcorp to acquire a majority stake in Cambio Healthcare Systems</br>Source: Private Equity Wire}}}, a Swedish company that provides software for electronic health records and has more than 150,000 users of its software solutions, particularly in Sweden, Denmark and the UK. Investcorp is supporting Cambio’s continued international expansion with a view to a future stock market listing.

Opportunities also abound outside of Europe’s most developed markets. Warsaw-based DocPlanner, an online appointments booking system already present in Turkey, Brazil and Mexico as well as Spain and Italy, raised almost $90 million from investors in 2019 to continue its global roll-out{{9}}{{{DocPlanner raises $89.8 million to simplify doctor appointment bookings</br>Source: VentureBeat}}}.

Increasing numbers of innovative start-ups focused on healthcare IT are presenting opportunities for venture capital. And as those venture-backed start-ups achieve success and scale, more opportunities are emerging for larger growth-oriented and buyout-focused private equity sponsors to invest and scale up operations.

The Power of Artificial Intelligence and Data

The use of artificial intelligence software in healthcare is accelerating, particularly in the field of diagnostics. London-based Babylon Health achieved a $2 billion valuation in 2019 for its AI-based health services, including a chatbot system that uses AI to generate diagnoses based on user responses{{10}}{{{ Babylon Health confirms $550M raise at $2B+ valuation to expand its AI-based health services</br>Source: Tech Crunch}}}.

And within diagnostics, there is significant focus on solutions that can identify cancers. The European Commission has made €35 million available, as part of its Horizon 2020 innovation programme, to help fund projects that develop AI tools to analyse scans and images for cancer diagnostics{{11}}{{{EU invests €35 million to develop Artificial Intelligence solutions for cancer prevention and treatment</br>Source: European Commission}}}.

Building AI modelling can require large numbers of real-life examples to allow AI engines to learn. Hospital networks and private care providers owned by private equity investors hold exactly this type of data. This means that private equity sponsors are in a strong position to collaborate with AI developers, bringing both data and capital to help develop ground-breaking diagnosis technologies that can improve patient outcomes through better and more accurate data analytics and modelling.

Alongside healthcare, technology companies have long been a focus for private equity investment globally, and technology has proved to be one of the best returning sectors. According to analysis by Bain & Co of CEPRES data, healthcare deals generated 2.2 times capital invested and tech 2.1 times, while all other sectors produced a combined return of 1.8 times (multiple of capital invested, 2009-2016){{3}}{{{Global Healthcare Private Equity and Corporate M&A Report 2020 Source: Bain}}}.

Global private equity investment in healthcare tech doubled last year to $17.5 billion from $8.6 billion in 2018, according to Bain & Co{{4}}{{{Global Healthcare Private Equity and Corporate M&A Report 2020 Source: Bain}}}. This growth was led by a buoyant US market and the takeover of health survey business Press Ganey for a reported figure of over $4 billion{{5}}{{{EQT and CPPIB to acquire a majority equity stake in Waystar in transaction valued at $2.7 billion Source: PR Newswire}}} by a consortium headed by Leonard Green. Capital is also increasingly targeting new technologies in Europe, such as Eurazeo’s €300 million deal for Dutch Ophthalmic Research Centre, a maker of hi-tech equipment for eye surgeries.

The Move to New IT Systems

The WannaCry ransomware attack on older Windows operating systems in 2017 exposed the vulnerability of outdated healthcare IT when it wreaked havoc on the UK’s NHS, where many trusts and other entities still relied on IT going back to the early 2000s. The NHS put the total cost of the attack at about £92 million{{6}}{{{WannaCry cyber-attack cost the NHS £92m after 19,000 appointments were cancelled

Source: National Health Executive}}}, and in 2019 admitted that more than 2,000 computers were still running on software that was two decades old{{7}}{{{NHS still running Windows XP on over 2,000 computers despite spate of cyber attacks

Source: CityAM}}}.

As healthcare systems digitise information, there are opportunities for private equity in back-end IT, as well as more innovative apps, such as those making it easier for patients to book hospital and GP appointments. Last year, for instance, Investcorp took a majority stake in Cambio{{8}}{{{Investcorp to acquire a majority stake in Cambio Healthcare Systems

Source: Private Equity Wire}}}, a Swedish company that provides software for electronic health records and has more than 150,000 users of its software solutions, particularly in Sweden, Denmark and the UK. Investcorp is supporting Cambio’s continued international expansion with a view to a future stock market listing.

Opportunities also abound outside of Europe’s most developed markets. Warsaw-based DocPlanner, an online appointments booking system already present in Turkey, Brazil and Mexico as well as Spain and Italy, raised almost $90 million from investors in 2019 to continue its global roll-out{{9}}{{{DocPlanner raises $89.8 million to simplify doctor appointment bookings

Source: VentureBeat}}}.

Increasing numbers of innovative start-ups focused on healthcare IT are presenting opportunities for venture capital. And as those venture-backed start-ups achieve success and scale, more opportunities are emerging for larger growth-oriented and buyout-focused private equity sponsors to invest and scale up operations.

The Power of Artificial Intelligence and Data

The use of artificial intelligence software in healthcare is accelerating, particularly in the field of diagnostics. London-based Babylon Health achieved a $2 billion valuation in 2019 for its AI-based health services, including a chatbot system that uses AI to generate diagnoses based on user responses{{10}}{{{ Babylon Health confirms $550M raise at $2B+ valuation to expand its AI-based health services

Source: Tech Crunch}}}.

And within diagnostics, there is significant focus on solutions that can identify cancers. The European Commission has made €35 million available, as part of its Horizon 2020 innovation programme, to help fund projects that develop AI tools to analyse scans and images for cancer diagnostics{{11}}{{{EU invests €35 million to develop Artificial Intelligence solutions for cancer prevention and treatment</br>Source: European Commission}}}.

Building AI modelling can require large numbers of real-life examples to allow AI engines to learn. Hospital networks and private care providers owned by private equity investors hold exactly this type of data. This means that private equity sponsors are in a strong position to collaborate with AI developers, bringing both data and capital to help develop ground-breaking diagnosis technologies that can improve patient outcomes through better and more accurate data analytics and modelling.

Over-the-counter drugs and generics are areas of continued activity for private equity firms. While the segment is competitive and entry prices are high, the attraction of cash-generative businesses combined with the potential for driving efficiency gains and consolidating fragmented sectors remains strong.

Private equity activity in the pharma sector hit a new high in 2019 with EQT, ADIA and PSP’s $10.1 billion buyout of Nestlé Skin Health (now Galderma), which makes prescription and consumer skin care products. In the current climate, this deal exemplifies the heightened investment opportunities in private and public companies creating specialised drugs and treatments within highly attractive growth sectors.

Generics

The generic and biogeneric industries have presented lucrative investment opportunities for private equity in recent years. Specialist players have developed a sophisticated approach to the development of generic alternatives, monitoring successful branded products for patent cliffs. Lower cost generic products are in high demand in many parts of the world, especially in the emerging markets, and opportunities exist for long-term supply contracts (including with NGOs active in emerging markets) that will yield dependable cash flows. The generics industry also offers opportunities for vertical integration (which we discuss further, below), for example by marrying product dossier development with manufacturing, sales and marketing authorisation capabilities.

Getting Comfortable with Biopharma

Biopharma has historically been less of a focus for private equity due to the higher risk of failure and the cash demands of research and development, but that is changing. Sponsors are increasingly attuned to opportunities in newer biopharma ventures as well as more mature companies requiring investment and expertise to increase scale or implement change. CVC’s 2018 purchase of the Recordati family’s majority stake in the listed Italian rare diseases specialist of the same name for €3 billion highlighted the opportunity in helping families manage succession issues{{12}}{{{CVC in talks over €3bn stake in Recordati pharma business</br>Source: FT</br>CVC Fund VII acquires controlling stake in Recordati S.p.A.</br>Source: CVC}}}.

In the first half of 2020, COVID-19 forced many biopharma companies to put clinical trials on hold, in some cases rendering existing trial samples useless and, in others, forcing new priorities and a reorganisation of development pipelines. Just in March, Swiss biotechnology firm Addex Therapeutics announced that its clinical trial for treatments relating to Parkinson’s disease had been delayed as a result of the pandemic{{13}}{{{Coronavirus shuts down trials of drugs for multiple other diseases</br>Source: Nature}}}, while Provention Bio’s investigational therapy study to treat Type 1 diabetes was also postponed{{14}}{{{The impact of COVID-19 on clinical trials</br>Source: PMLiVE}}}. At least 43% of the clinical trials identified by the US National Library of Medicine as stopped or postponed since January 2020 cited COVID-19 as the reason{{15}}{{{Covid-19 is forcing pharma to rethink clinical trials</br>Source: Chemistry World}}}. As a result, many more businesses may need funding and could be open to private equity investment to restart operations or streamline product portfolios.

The situation is made more difficult by the uncertain outlook and volatility of valuations. In such instances, private equity may adopt a variety of investment structures as alternatives to ordinary equity, including preferred equity (perhaps with warrants attached) or contingent value rights (CVR) instruments, to help protect against downside risks while capturing upside potential. There are other participation and reward mechanisms, such as earn-outs and milestone payments, or agreements for access to royalty streams.

Vertical Integration Plays

Recent large-scale tie-ups in the US highlighted the cost and revenue benefits of vertical mergers combining insurers with retailers or service providers. The $70 billion deal agreed by pharmacy chain CVS for healthcare insurer Aetna in 2017 aimed to reduce costs for consumers and improve services.

One of private equity’s clear strengths is the ability to piece together investments to create greater value. In the pharma sector in Europe, this can happen through vertical mergers to build companies that combine payers with healthcare services, or manufacturers with sales and distribution. For instance, in an industry where drug prices are tightly controlled and care providers often have to pass through drugs at cost, vertically integrated companies can access margins others cannot. Alternatively, companies combining the delivery of care with pharmacies can have greater power to negotiate better prices with large pharma companies.

Over-the-counter drugs and generics are areas of continued activity for private equity firms. While the segment is competitive and entry prices are high, the attraction of cash-generative businesses combined with the potential for driving efficiency gains and consolidating fragmented sectors remains strong.

Private equity activity in the pharma sector hit a new high in 2019 with EQT, ADIA and PSP’s $10.1 billion buyout of Nestlé Skin Health (now Galderma), which makes prescription and consumer skin care products. In the current climate, this deal exemplifies the heightened investment opportunities in private and public companies creating specialised drugs and treatments within highly attractive growth sectors.

Generics

The generic and biogeneric industries have presented lucrative investment opportunities for private equity in recent years. Specialist players have developed a sophisticated approach to the development of generic alternatives, monitoring successful branded products for patent cliffs. Lower cost generic products are in high demand in many parts of the world, especially in the emerging markets, and opportunities exist for long-term supply contracts (including with NGOs active in emerging markets) that will yield dependable cash flows. The generics industry also offers opportunities for vertical integration (which we discuss further, below), for example by marrying product dossier development with manufacturing, sales and marketing authorisation capabilities.

Getting Comfortable with Biopharma

Biopharma has historically been less of a focus for private equity due to the higher risk of failure and the cash demands of research and development, but that is changing. Sponsors are increasingly attuned to opportunities in newer biopharma ventures as well as more mature companies requiring investment and expertise to increase scale or implement change. CVC’s 2018 purchase of the Recordati family’s majority stake in the listed Italian rare diseases specialist of the same name for €3 billion highlighted the opportunity in helping families manage succession issues{{12}}{{{CVC in talks over €3bn stake in Recordati pharma business Source: FT CVC Fund VII acquires controlling stake in Recordati S.p.A. Source: CVC}}}.

In the first half of 2020, COVID-19 forced many biopharma companies to put clinical trials on hold, in some cases rendering existing trial samples useless and, in others, forcing new priorities and a reorganisation of development pipelines. Just in March, Swiss biotechnology firm Addex Therapeutics announced that its clinical trial for treatments relating to Parkinson’s disease had been delayed as a result of the pandemic{{13}}{{{Coronavirus shuts down trials of drugs for multiple other diseases Source: Nature}}}, while Provention Bio’s investigational therapy study to treat Type 1 diabetes was also postponed{{14}}{{{The impact of COVID-19 on clinical trials Source: PMLiVE}}}. At least 43% of the clinical trials identified by the US National Library of Medicine as stopped or postponed since January 2020 cited COVID-19 as the reason{{15}}{{{Covid-19 is forcing pharma to rethink clinical trials Source: Chemistry World}}}. As a result, many more businesses may need funding and could be open to private equity investment to restart operations or streamline product portfolios.

The situation is made more difficult by the uncertain outlook and volatility of valuations. In such instances, private equity may adopt a variety of investment structures as alternatives to ordinary equity, including preferred equity (perhaps with warrants attached) or contingent value rights (CVR) instruments, to help protect against downside risks while capturing upside potential. There are other participation and reward mechanisms, such as earn-outs and milestone payments, or agreements for access to royalty streams.

Vertical Integration Plays

Recent large-scale tie-ups in the US highlighted the cost and revenue benefits of vertical mergers combining insurers with retailers or service providers. The $70 billion deal agreed by pharmacy chain CVS for healthcare insurer Aetna in 2017 aimed to reduce costs for consumers and improve services.

One of private equity’s clear strengths is the ability to piece together investments to create greater value. In the pharma sector in Europe, this can happen through vertical mergers to build companies that combine payers with healthcare services, or manufacturers with sales and distribution. For instance, in an industry where drug prices are tightly controlled and care providers often have to pass through drugs at cost, vertically integrated companies can access margins others cannot . Alternatively, companies combining the delivery of care with pharmacies can have greater power to negotiate better prices with large pharma companies.

Buy-and-build is a core strategy in many private equity sponsors’ playbooks. With stiff competition and high asset prices in healthcare, they will continue to be an attractive way of creating scale and added value. Some can be vertical integration plays (as noted above). Other investments can seek to build scale by consolidating fragmented product ranges, or build operators spanning multiple geographies. In the generic and OTC pharma space, Germany’s Stada (acquired by Bain Capital and Cinven in 2017) has achieved both product range and geographic scale, adding multiple brand portfolios from groups such as Takeda and GSK, while bolting on smaller companies such as Walmark which has a focus on Central and Eastern Europe.

Private hospitals and healthcare services are another area of activity, both in Europe and emerging markets. In some emerging economies, there is less consistency between hospitals, which in turn leads to opportunities for operators with a quality offering and a reputable brand. Successfully-built companies can then find exits to larger international groups or via IPOs on local or international exchanges.

Healthcare conglomerates face considerable scrutiny, both from regulators and from shareholders. The push towards greater efficiency and leaner models is resulting in divestments of sizeable and often very successful divisions that are deemed non-core to the company’s strategic vision. Nestlé’s sale of its skin care business followed sustained pressure from activist investor Daniel Loeb’s Third Point fund{{16}}{{{Daniel Loeb's Third Point Calls for More Change at Nestlé -- 2nd Update</br>Source: Fox Business}}}. By the same token, large and mega-M&A deals aimed at creating strength or specialism in a particular field are leading to demands from regulators for the sale of brands or divisions focused on particular markets.

While the uncertainty and economic turmoil caused by the COVID-19 pandemic has hampered some buyouts and dampened corporate M&A, the fundamental deal drivers for carve-outs remain intact. As markets recover, debt financing should be available on attractive terms for quality businesses, and we expect carve-out activity to increase.

COVID-19 has added to financial pressures on companies in all sectors. On the whole, we observe less distress and need for restructuring in healthcare, but many successful companies continue to need financing to operate, expand or produce new drugs and services. In April this year, Warburg Pincus agreed a deal to invest in French gene and cell therapy group Polyplus-Transfection, alongside existing backer ArchiMed, to accelerate the development, production and sale of its therapies{{17}}{{{Growth investment is set to accelerate Polyplus' expansion in partnership with Warburg Pincus and ArchiMed</br>Source: PR Newswire}}}.

With capital, operational skills and expertise from previous deals in healthcare and other sectors, minority private equity is increasingly welcome among listed and private family-owned businesses that are not yet ready for a full exit. Moreover, companies are open to more innovative structures, such as convertible securities or preferred equity, which can give sponsors debt-like protection with potential equity upside should the company perform strongly. In addition, techniques to bridge the gap in cases of valuation uncertainties have become more popular, including contingent or earn-out payments and contingent value rights. Finally, “toe-hold” investments allow private equity sponsors to gain limited exposure to an investment target (potentially at a lower valuation), with a view to taking a greater or controlling stake as the relationship between the private equity sponsor and the target grows, and the target company matures.

Buy-and-Build

Buy-and-build is a core strategy in many private equity sponsors’ playbooks. With stiff competition and high asset prices in healthcare, they will continue to be an attractive way of creating scale and added value. Some can be vertical integration plays (as noted above). Other investments can seek to build scale by consolidating fragmented product ranges, or build operators spanning multiple geographies. In the generic and OTC pharma space, Germany’s Stada (acquired by Bain Capital and Cinven in 2017) has achieved both product range and geographic scale, adding multiple brand portfolios from groups such as Takeda and GSK, while bolting on smaller companies such as Walmark which has a focus on Central and Eastern Europe.

Private hospitals and healthcare services are another area of activity, both in Europe and emerging markets. In some emerging economies, there is less consistency between hospitals, which in turn leads to opportunities for operators with a quality offering and a reputable brand. Successfully-built companies can then find exits to larger international groups or via IPOs on local or international exchanges.

Corporate Carve-Outs

Healthcare conglomerates face considerable scrutiny, both from regulators and from shareholders. The push towards greater efficiency and leaner models is resulting in divestments of sizeable and often very successful divisions that are deemed non-core to the company’s strategic vision. Nestlé’s sale of its skin care business followed sustained pressure from activist investor Daniel Loeb’s Third Point fund{{16}}{{{Daniel Loeb's Third Point Calls for More Change at Nestlé -- 2nd Update

Source: Fox Business}}}. By the same token, large and mega-M&A deals aimed at creating strength or specialism in a particular field are leading to demands from regulators for the sale of brands or divisions focused on particular markets.

While the uncertainty and economic turmoil caused by the COVID-19 pandemic has hampered some buyouts and dampened corporate M&A, the fundamental deal drivers for carve-outs remain intact. As markets recover, debt financing should be available on attractive terms for quality businesses, and we expect carve-out activity to increase.

Minority and Toe-Hold Investments

COVID-19 has added to financial pressures on companies in all sectors. On the whole, we observe less distress and need for restructuring in healthcare, but many successful companies continue to need financing to operate, expand or produce new drugs and services. In April this year, Warburg Pincus agreed a deal to invest in French gene and cell therapy group Polyplus-Transfection, alongside existing backer ArchiMed, to accelerate the development, production and sale of its therapies{{17}}{{{Growth investment is set to accelerate Polyplus' expansion in partnership with Warburg Pincus and ArchiMed

Source: PR Newswire}}}.

With capital, operational skills and expertise from previous deals in healthcare and other sectors, minority private equity is increasingly welcome among listed and private family-owned businesses that are not yet ready for a full exit. Moreover, companies are open to more innovative structures, such as convertible securities or preferred equity, which can give sponsors debt-like protection with potential equity upside should the company perform strongly. In addition, techniques to bridge the gap in cases of valuation uncertainties have become more popular, including contingent or earn-out payments and contingent value rights. Finally, “toe-hold” investments allow private equity sponsors to gain limited exposure to an investment target (potentially at a lower valuation), with a view to taking a greater or controlling stake as the relationship between the private equity sponsor and the target grows, and the target company matures.

Even before COVID-19, governments and regulators in Europe were taking a more active approach to scrutinising investment – and often being ever more innovative in doing so. When Swiss group Roche made an approach for US-based gene therapy developer Spark, the UK’s Competition and Markets Authority intervened even though Spark did not have a competing product in the UK market. Instead, the regulator based its investigation on expected future competition involving the firm’s yet-to-be-marketed haemophilia drug, and asserted jurisdiction over the case based on the merging companies’ shares of UK-based research personnel engaged in a specific type of gene therapy. While the CMA (as well as the US Federal Trade Commission) cleared the deal late last year, the investigation resulted in a ten-month delay.

The UK recently introduced a specific test into its merger legislation allowing the Government to intervene in acquisitions that might threaten the country’s ability to respond to public health emergencies. Other jurisdictions around Europe are taking a similar stance.

We see three trends currently shaping the regulatory response in Europe:

Antitrust Authorities Want to be Part of the Solution, Not the Problem

With healthcare in the spotlight, as well as concerns about foreign direct investment, market regulators and policymakers are likely to investigate deals to ensure that companies and ultimately consumers are protected. There will be positive developments too. Germany’s Digital Healthcare Act will open up digital care provision, such as online consultations, by allowing them to be reimbursed, driving more investment in digital health.

The Impact of Deals on Research and Development

Regulators are increasingly looking beyond issues of price and competition and have a keen focus on protecting or encouraging innovation. Any investment in a company with an R&D division is likely to attract scrutiny.

Enforcement in Pharma

Questions of price fixing and abusive practices in pharma are of particular concern, particularly as drug pricing can be high, prices are often paid from the public purse, and producers can develop monopoly positions. In 2016, for example, the UK’s CMA fined US group Pfizer and its distributor Flynn Pharma £90 million for sharply increasing prices of an epilepsy drug as it came off patent. This case is still being investigated after the courts overturned parts of the CMA’s decision, while upholding others. This is just one of several excessive pricing cases that have been brought in the UK and elsewhere in Europe.

Antitrust Authorities Want to be Part of the Solution, Not the Problem

With healthcare in the spotlight, as well as concerns about foreign direct investment, market regulators and policymakers are likely to investigate deals to ensure that companies and ultimately consumers are protected. There will be positive developments too. Germany’s Digital Healthcare Act will open up digital care provision, such as online consultations, by allowing them to be reimbursed, driving more investment in digital health.

The Impact of Deals on Research and Development

Regulators are increasingly looking beyond issues of price and competition and have a keen focus on protecting or encouraging innovation. Any investment in a company with an R&D division is likely to attract scrutiny.

Enforcement in Pharma

Questions of price fixing and abusive practices in pharma are of particular concern, particularly as drug pricing can be high, prices are often paid from the public purse, and producers can develop monopoly positions. In 2016, for example, the UK’s CMA fined US group Pfizer and its distributor Flynn Pharma £90 million for sharply increasing prices of an epilepsy drug as it came off patent. This case is still being investigated after the courts overturned parts of the CMA’s decision, while upholding others. This is just one of several excessive pricing cases that have been brought in the UK and elsewhere in Europe.

Ring-fencing R&D, promising to keep jobs in the company’s home country, maintaining or onshoring production facilities, and committing not to share critical intellectual property with co-investors are among the potential concessions that could ease the passing of deals.

Uncertainty about the global outlook has forced many companies to reduce or even cancel their earnings forecasts for 2020. As a result, private equity firms are becoming more proactive and granular in their assessment of potential investments. Below, we highlight key due diligence considerations for sponsors looking at both buyout and minority deals in healthcare.

Pharma businesses routinely enter into strategic joint ventures, joint R&D, licences, options and other collaborative agreements. These types of arrangement require expert due diligence to analyse intellectual property ownership and data access rights, regulatory responsibilities, risk exposure, and forecast expenditure and revenues including buy-ins or milestone payments.

Valuations of pharma and healthcare companies are often strongly linked to the value of their intellectual property. Prospective buyers must take a forensic approach to investigating registered IP portfolios, including patents and trade marks, the extent of unregistered rights in data and high-value software, and third party litigation risk, to validate targets’ asset valuations and third party risk profile, including encumbrances on future growth.

Compliance with applicable personal and healthcare data processing laws, such as the EU General Data Protection Regulation (GDPR) or US Health Insurance Portability and Accountability Act (HIPAA), is paramount for companies processing and analysing highly sensitive health or biometric data. The sensitivity and often significant value of R&D data – including personal data – in the sector, combined with the prevalence, frequency and growing sophistication of cyberattacks and intrusions, means that state-of-the-art data protection, privacy and cybersecurity diligence is increasingly essential for unearthing material threats and vulnerabilities for pre-signing risk allocation or post-closing remediation.

Healthcare businesses in Europe need extensive regulatory licences and permissions to carry out regulated operations across manufacturing, distribution, marketing and sales. Due diligence should focus on ensuring that companies have the necessary authorisations, take adequate steps to ensure the safety of products and protection of patients’ interests, and have been compliant and transparent with regulators. Legal due diligence should be supported by technical pharmaceutical appraisal, for example to ensure that dossiers for key products are complete.

As heavily regulated companies, healthcare groups in Europe and emerging markets often have regular interactions with government officials. “Cash for referrals” practices, also known as “kickbacks”, may also be widespread in some segments of the healthcare chain and may fall under a regulatory grey area within the target’s home market. Buyers should review the target’s anti-bribery and corruption procedures, as well as its compliance history. Assessments should include background checks on management and in-person interviews. The extra-territorial reach of anticorruption laws in jurisdictions such as the UK and US also means that buyers should be prepared to have to enhance anti-bribery and corruption procedures in targets to match their own standards.

Collaborative Arrangements

Pharma businesses routinely enter into strategic joint ventures, joint R&D, licences, options and other collaborative agreements. These types of arrangement require expert due diligence to analyse intellectual property ownership and data access rights, regulatory responsibilities, risk exposure, and forecast expenditure and revenues including buy-ins or milestone payments.

Intellectual Property

Valuations of pharma and healthcare companies are often strongly linked to the value of their intellectual property. Prospective buyers must take a forensic approach to investigating registered IP portfolios, including patents and trade marks, the extent of unregistered rights in data and high-value software, and third party litigation risk, to validate targets’ asset valuations and third party risk profile, including encumbrances on future growth.

Data Protection, Privacy and Cybersecurity

Compliance with applicable personal and healthcare data processing laws, such as the EU General Data Protection Regulation (GDPR) or US Health Insurance Portability and Accountability Act (HIPAA), is paramount for companies processing and analysing highly sensitive health or biometric data. The sensitivity and often significant value of R&D data – including personal data – in the sector, combined with the prevalence, frequency and growing sophistication of cyberattacks and intrusions, means that state-of-the-art data protection, privacy and cybersecurity diligence is increasingly essential for unearthing material threats and vulnerabilities for pre-signing risk allocation or post-closing remediation.

Regulatory Risks

Healthcare businesses in Europe need extensive regulatory licences and permissions to carry out regulated operations across manufacturing, distribution, marketing and sales. Due diligence should focus on ensuring that companies have the necessary authorisations, take adequate steps to ensure the safety of products and protection of patients’ interests, and have been compliant and transparent with regulators. Legal due diligence should be supported by technical pharmaceutical appraisal, for example to ensure that dossiers for key products are complete.

Bribery and Corruption

As heavily regulated companies, healthcare groups in Europe and emerging markets often have regular interactions with government officials. “Cash for referrals” practices, also known as “kickbacks”, may also be widespread in some segments of the healthcare chain and may fall under a regulatory grey area within the target’s home market. Buyers should review the target’s anti-bribery and corruption procedures, as well as its compliance history. Assessments should include background checks on management and in-person interviews. The extra-territorial reach of anticorruption laws in jurisdictions such as the UK and US also means that buyers should be prepared to have to enhance anti-bribery and corruption procedures in targets to match their own standards.

What’s Next For Private Equity Investment in Healthcare?

Private equity investment in healthcare has been on an upward trajectory over the last decade to achieve new records in 2019. The large and homogenous US market has historically been the focus of many global sponsors. Investments like Nestlé Skin Health, however, have highlighted the scale and quality of businesses in Europe, particularly as the US healthcare regime faces further uncertainty in this Presidential election year. European healthcare companies can have global footprints and be exposed to positive secular trends in both developed and emerging markets. Furthermore, Europe, with strong links to emerging markets particularly in Africa and South Asia, as well as international capital markets expertise, often serves as a launch pad for private equity investment into many parts of the developing world.

The COVID-19 pandemic is putting healthcare provision and security in the spotlight. As the world wrestles with the impact on healthcare systems and the economy, there will be compelling opportunities for private equity to invest in companies that generate attractive returns while reducing costs, increasing efficiency and delivering better outcomes.

At the same time, deals will be subject to greater regulatory scrutiny and will require more careful due diligence to navigate existing and emerging requirements. Private equity firms need to understand the regional landscape in European healthcare, be able to identify and manage the key due diligence risks and have clear answers for regulators’ searching questions.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

David J. Billington

Partner

London

T: +44 20 7614 2263

dbillington@cgsh.com

V-Card

Paul Gilbert

Partner

London

T: +44 20 7614 2335

pgilbert@cgsh.com

V-Card

Ferdisha Snagg

Senior Attorney

London

T: +44 20 7614 2251

fsnagg@cgsh.com

V-Card