When billionaire Roman Abramovich bought Chelsea Football Club in 2003, the headline-grabbing deal valued the top-flight London-based team at £140mn, including £80mn in debt. Just under two decades later the club was sold to an investment consortium led by U.S. financier Todd Boehly and California-headquartered private equity (PE) firm Clearlake Capital for £2.5bn, with the consortium pledging an additional £1.75bn of investment into the club during its ownership1. Not only did the price represent an 18-fold increase in the enterprise value of the club, but it also reflected the growing shift in ownership for the world’s largest sporting franchises. Once considered trophy assets for high-net-worth individuals, sports investments have become institutional grade assets that can benefit from PE value creation techniques to generate attractive long-term returns.

When billionaire Roman Abramovich bought Chelsea Football Club in 2003, the headline-grabbing deal valued the top-flight London-based team at £140mn, including £80mn in debt. Just under two decades later the club was sold to an investment consortium led by U.S. financier Todd Boehly and California-headquartered private equity (PE) firm Clearlake Capital for £2.5bn, with the consortium pledging an additional £1.75bn of investment into the club during its ownership1. Not only did the price represent an 18-fold increase in the enterprise value of the club, but it also reflected the growing shift in ownership for the world’s largest sporting franchises. Once considered trophy assets for high-net-worth individuals, sports investments have become institutional grade assets that can benefit from PE value creation techniques to generate attractive long-term returns.

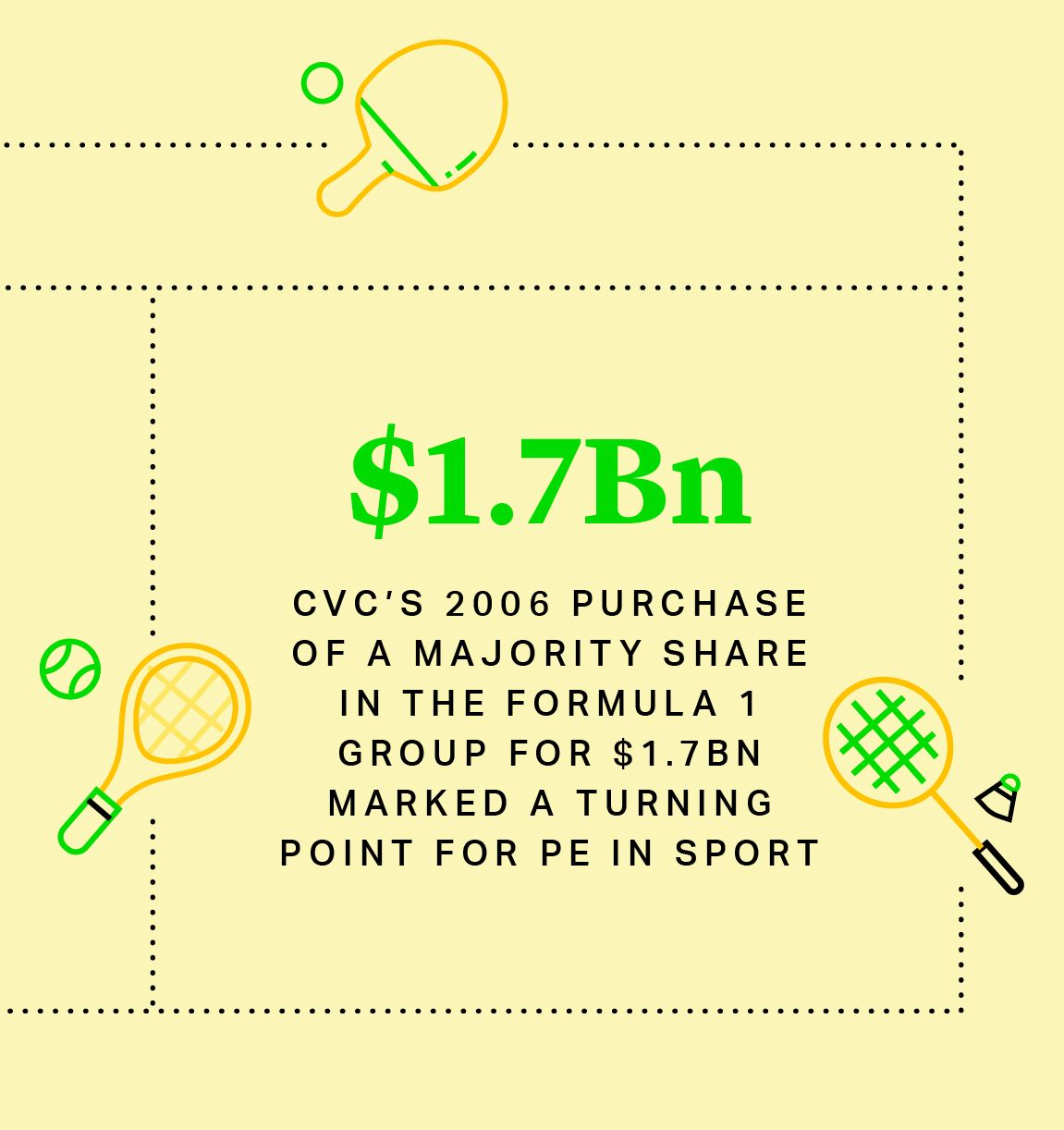

Although not the first PE firm to invest in motor racing, CVC’s 2006 purchase of a majority share in the Formula 1 Group for $1.7bn marked a turning point for PE in sport. Over the next decade, until its sale to media group Liberty Global in 2016, the sport grew to achieve an annual turnover of $1.8bn and a valuation of $8bn at exit. For CVC, it was one of its most successful ever investments, with its return on equity reported at 450%2.

CVC has followed up with further sports deals including Six Nations Rugby, Spain’s La Liga football, the Women’s Tennis Association, France’s Ligue 1 football and Volleyball World. Other firms have seen opportunity in targeting a range of sports, with Silver Lake completing investments in the owner of Manchester City Football Club, the mixed martial arts events organizer Ultimate Fighting Championship and New Zealand Rugby, while Sixth Street has made investments in the San Antonio Spurs, Real Madrid and FC Barcelona. According to Pitchbook, more than a third of clubs in Europe’s ‘Big Five’ football leagues are backed by U.S. based private equity, venture capital or other forms of private capital3.

The scale of opportunity in the sector has led to established PE firms raising dedicated funds, such as the $3.7 billion raised by Ares to invest in sports leagues, teams and media and entertainment companies. Meanwhile, PE firms solely dedicated to investment in sports and related media have been formed, such as Bluestone Equity Partners, a firm co-led by former National Basketball Association executive Bobby Sharma, which successfully raised its inaugural $300mn growth equity fund focused on the global sports, media and entertainment industry. In September 2023, Dynasty Equity (another recently formed sports-sector PE firm) acquired a strategic minority equity stake in Liverpool Football Club with an investment reported to be over $100mn4.

Although not the first PE firm to invest in motor racing, CVC’s 2006 purchase of a majority share in the Formula 1 Group for $1.7bn marked a turning point for PE in sport. Over the next decade, until its sale to media group Liberty Global in 2016, the sport grew to achieve an annual turnover of $1.8bn and a valuation of $8bn at exit. For CVC, it was one of its most successful ever investments, with its return on equity reported at 450%2.

CVC has followed up with further sports deals including Six Nations Rugby, Spain’s La Liga football, the Women’s Tennis Association, France’s Ligue 1 football and Volleyball World. Other firms have seen opportunity in targeting a range of sports, with Silver Lake completing investments in the owner of Manchester City Football Club, the mixed martial arts events organizer Ultimate Fighting Championship and New Zealand Rugby, while Sixth Street has made investments in the San Antonio Spurs, Real Madrid and FC Barcelona. According to Pitchbook, more than a third of clubs in Europe’s ‘Big Five’ football leagues are backed by U.S. based private equity, venture capital or other forms of private capital3.

The scale of opportunity in the sector has led to established PE firms raising dedicated funds, such as the $3.7 billion raised by Ares to invest in sports leagues, teams and media and entertainment companies. Meanwhile, PE firms solely dedicated to investment in sports and related media have been formed, such as Bluestone Equity Partners, a firm co-led by former National Basketball Association executive Bobby Sharma, which successfully raised its inaugural $300mn growth equity fund focused on the global sports, media and entertainment industry. In September 2023, Dynasty Equity (another recently formed sports-sector PE firm) acquired a strategic minority equity stake in Liverpool Football Club with an investment reported to be over $100mn4.

The COVID-19 pandemic and subsequent recovery shone a new light on the potential in sport for PE and institutional investors. With live sporting events suspended or played in front of empty stadiums, the global sports market contracted by 15% to $388bn in 2020, according to the Sports Global Market Report 2021 from the Business Research Company5. However, the market rapidly recovered lost ground when in-person attendance returned, growing to $512bn in 2023 with continued growth expected to take the global sports market to almost $624bn in 20276.

The growth in global turnover linked to the sports sector is driven in part by the increasingly sophisticated creation of revenue streams, using digital distribution platforms to leverage brands and associated image rights across a range of products, services and sectors. The increasing value of traditional media rights deals, driven by recession-resistant consumer demand, is also an important factor. For example, Deloitte’s Money League looks at the revenues of the top 20 football clubs in the world and shows that – excluding the pandemic – matchday revenues have been relatively stable since 2015, while commercial and broadcast revenues have expanded steadily7.

The COVID-19 pandemic and subsequent recovery shone a new light on the potential in sport for PE and institutional investors. With live sporting events suspended or played in front of empty stadiums, the global sports market contracted by 15% to $388bn in 2020, according to the Sports Global Market Report 2021 from the Business Research Company5. However, the market rapidly recovered lost ground when in-person attendance returned, growing to $512bn in 2023 with continued growth expected to take the global sports market to almost $624bn in 20276.

The growth in global turnover linked to the sports sector is driven in part by the increasingly sophisticated creation of revenue streams, using digital distribution platforms to leverage brands and associated image rights across a range of products, services and sectors. The increasing value of traditional media rights deals, driven by recession-resistant consumer demand, is also an important factor. For example, Deloitte’s Money League looks at the revenues of the top 20 football clubs in the world and shows that – excluding the pandemic – matchday revenues have been relatively stable since 2015, while commercial and broadcast revenues have expanded steadily7.

Against this backdrop of revenue growth, undervalued assets in the sporting world are being identified, with financial investors realizing that as well as helping to grow revenues, they can also bring to bear vast experience driving efficiencies and producing cost savings. PE is responding – there has been a plethora of dealmaking activity in Europe’s ‘Big Five’ football leagues, for example, with dealmaking value reaching €4.9bn in 2022 and forecast to grow to nearly €10.6bn this year8.

PE activity is primarily focused on tapping into growth in the consumer base for international sports by developing marketing and distribution opportunities tied to leagues and major events, as well as clubs and their stars. CVC’s €2bn investment in Spain’s LaLiga in 2021, dubbed Project Boost, aimed to help the league and teams to improve technology, innovation and internationalization, while identifying new growth initiatives. Under the terms of the agreement, the league’s participating clubs must allocate 70% of CVC’s investment to areas including international development, brand and product development, as well as a content development plan for digital platforms and social media. Of the remainder, up to 15% can be used to sign players, with the rest available for reducing debt9. By building a series of investments, in one or (increasingly) across different sports, PE firms can leverage greater bargaining power with broadcasters and other commercial partners, which in turn can unlock benefits for investee leagues as they gain from the PE firms’ focus on sales and marketing, as well as their broad-ranging commercial relationships.

Against this backdrop of revenue growth, undervalued assets in the sporting world are being identified, with financial investors realizing that as well as helping to grow revenues, they can also bring to bear vast experience driving efficiencies and producing cost savings. PE is responding – there has been a plethora of dealmaking activity in Europe’s ‘Big Five’ football leagues, for example, with dealmaking value reaching €4.9bn in 2022 and forecast to grow to nearly €10.6bn this year8.

PE activity is primarily focused on tapping into growth in the consumer base for international sports by developing marketing and distribution opportunities tied to leagues and major events, as well as clubs and their stars. CVC’s €2bn investment in Spain’s LaLiga in 2021, dubbed Project Boost, aimed to help the league and teams to improve technology, innovation and internationalization, while identifying new growth initiatives. Under the terms of the agreement, the league’s participating clubs must allocate 70% of CVC’s investment to areas including international development, brand and product development, as well as a content development plan for digital platforms and social media. Of the remainder, up to 15% can be used to sign players, with the rest available for reducing debt9. By building a series of investments, in one or (increasingly) across different sports, PE firms can leverage greater bargaining power with broadcasters and other commercial partners, which in turn can unlock benefits for investee leagues as they gain from the PE firms’ focus on sales and marketing, as well as their broad-ranging commercial relationships.

Excitingly for the growth of sports that might be considered non-mainstream, the aim of helping franchises expand their reach is going far beyond the most high-profile sports. In January 2022, General Atlantic became a significant investor in Chess.com – the world’s largest chess platform with over 75 million registered users. The aim of the deal is to help the game expand its following and for the platform to develop new revenue-generating content10. Such an investment is an example of what PE can do very well – identify pockets of underinvestment within a wider asset class, potentially having the most growth potential. However, even very established sports that already have huge addressable markets can see dramatic growth, with the adoption of more fan-friendly formats to broaden appeal and generate new revenues.

The Indian Premier League T20 Cricket, which features 10 teams from cities across the country, attracted more than half a billion viewers for its 2023 season11. CVC spent $736mn on the Ahmedabad franchise in 2021, with its Gujarat Titans team subsequently winning the competition in 2022 and securing second place in 2023. Following its success in the league, the team launched its own streetwear clothing collection to further tap demand among its followers12. The value now attached to the IPL is particularly remarkable considering the tournament is only played over two months, although IPL teams appear to be attempting to address this by acquiring franchises in new markets.

New technology has unlocked other ways to monetize sporting brands and star power. The football World Cup in Qatar in 2022 gave players including Lionel Messi and Cristiano Ronaldo the opportunity to market non-fungible tokens (NFTs) to fans13. Innovative online retailers like Fanatics can seize viral sports moments to supply fans with custom apparel on-demand14. In the age of social media, athletes and clubs are able to directly engage with fans and over-the-top streaming services can create additional revenue streams beyond the linear TV broadcasting format.

Despite all the success, there have been challenges - some leagues have been resistant to accepting PE investment due to push back from certain clubs or fanbases. Proposed deals by PE firms to invest in the media and commercial rights of Germany’s Bundesliga and Italy’s Serie A have been repeatedly blocked by some holdout clubs. The latest attempt to sell a stake in the Bundesliga’s media and commercial rights failed to obtain approval from the requisite number of clubs in May 2023; however, German football chiefs have insisted they remain open to investment from private equity15. Silver Lake’s investment in the All Blacks was initially met with strong resistance, and was only concluded after extended discussions with the body that represents players. Indeed, one of the great attractions of sport as an investment – the passion that supporters have for their teams – also presents one of the great difficulties. Successful investments in sports can be time-consuming and often require the ability to build consensus with a large number of stakeholders, including clubs, players, supporter-led groups, local community associations and in certain cases government regulators. All of this often takes place under a glare of publicity.

Excitingly for the growth of sports that might be considered non-mainstream, the aim of helping franchises expand their reach is going far beyond the most high-profile sports. In January 2022, General Atlantic became a significant investor in Chess.com – the world’s largest chess platform with over 75 million registered users. The aim of the deal is to help the game expand its following and for the platform to develop new revenue-generating content10. Such an investment is an example of what PE can do very well – identify pockets of underinvestment within a wider asset class, potentially having the most growth potential. However, even very established sports that already have huge addressable markets can see dramatic growth, with the adoption of more fan-friendly formats to broaden appeal and generate new revenues.

The Indian Premier League T20 Cricket, which features 10 teams from cities across the country, attracted more than half a billion viewers for its 2023 season11. CVC spent $736mn on the Ahmedabad franchise in 2021, with its Gujarat Titans team subsequently winning the competition in 2022 and securing second place in 2023. Following its success in the league, the team launched its own streetwear clothing collection to further tap demand among its followers12. The value now attached to the IPL is particularly remarkable considering the tournament is only played over two months, although IPL teams appear to be attempting to address this by acquiring franchises in new markets.

New technology has unlocked other ways to monetize sporting brands and star power. The football World Cup in Qatar in 2022 gave players including Lionel Messi and Cristiano Ronaldo the opportunity to market non-fungible tokens (NFTs) to fans13. Innovative online retailers like Fanatics can seize viral sports moments to supply fans with custom apparel on-demand14. In the age of social media, athletes and clubs are able to directly engage with fans and over-the-top streaming services can create additional revenue streams beyond the linear TV broadcasting format.

Despite all the success, there have been challenges - some leagues have been resistant to accepting PE investment due to push back from certain clubs or fanbases. Proposed deals by PE firms to invest in the media and commercial rights of Germany’s Bundesliga and Italy’s Serie A have been repeatedly blocked by some holdout clubs. The latest attempt to sell a stake in the Bundesliga’s media and commercial rights failed to obtain approval from the requisite number of clubs in May 2023; however, German football chiefs have insisted they remain open to investment from private equity15. Silver Lake’s investment in the All Blacks was initially met with strong resistance, and was only concluded after extended discussions with the body that represents players. Indeed, one of the great attractions of sport as an investment – the passion that supporters have for their teams – also presents one of the great difficulties. Successful investments in sports can be time-consuming and often require the ability to build consensus with a large number of stakeholders, including clubs, players, supporter-led groups, local community associations and in certain cases government regulators. All of this often takes place under a glare of publicity.

Unlike the European sport leagues, U.S. sports leagues are traditionally based around a fixed group of franchises competing in the same tournament from year-to-year, without the risk of relegation (or the reward of promotion). This has made ownership of American sports teams a relatively stable investment compared to the risk of investing in an equally successful European team. While the strongest and wealthiest clubs generally do not run the risk of relegation in their league, it can and does happen. Leicester City won the Premiership – England’s top flight football competition – in the 2015/2016 season, but were relegated to the second tier Championship in 2023. Historically, however, ownership rules in the U.S. have prohibited investment by “non-individuals” such as corporates, PE firms and financial institutions. However, in recent years American sports leagues have opened up the role that PE investors can play, by offering secondary market liquidity to existing owners. The NBA16, Major League Baseball, Major League Soccer and National Hockey League have all changed their ownership rules to allow some form of passive minority PE investment in their teams.

In 2021 the NBA reformed its bylaws to allow pre-approved PE firms to acquire passive non-controlling stakes in NBA teams. However, to prevent the same beneficial owner from having indirect influence over competing teams, no one PE firm can acquire more than 20% of an individual NBA team and each NBA team can have a maximum 30% of ownership by PE investors17.

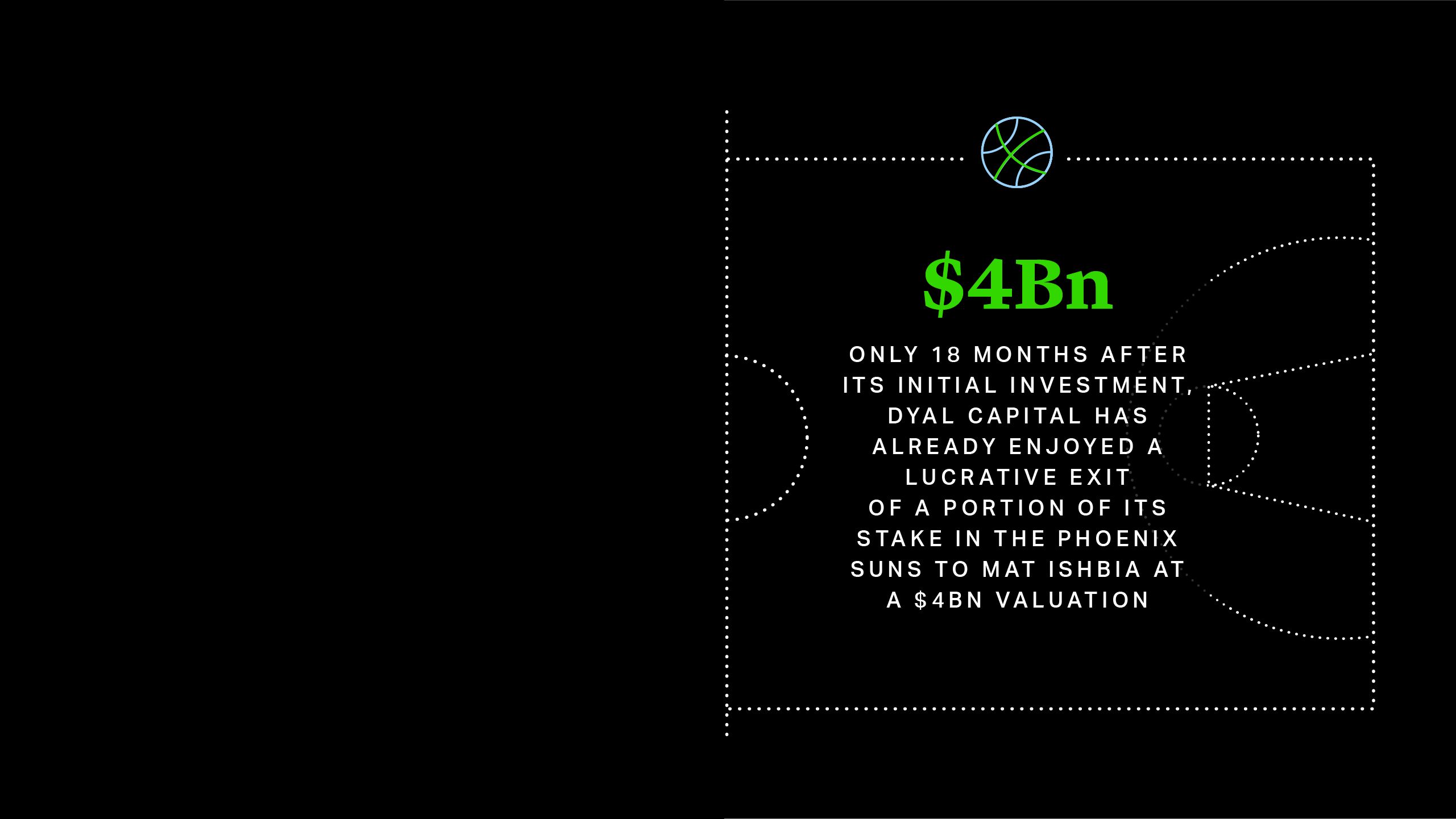

In response to the reforms, Dyal Capital raised its Homecourt Fund and has deployed the proceeds to acquire minority stakes in the Atlanta Hawks, Phoenix Suns and Sacramento Kings18. Meanwhile, competitor sports fund Arctos Partners acquired minority stakes in the Sacramento Kings, Golden State Warriors, Philadelphia 76ers and Utah Jazz19. Sportico reported that only 18 months after its initial investment, Dyal Capital has already enjoyed a lucrative exit of a portion of its stake in the Phoenix Suns to Mat Ishbia - the $4bn valuation for the Suns in December 2022 being the largest valuation ever recorded for an NBA team20. With U.S. sports betting legalization set to further increase monetization opportunities and given the trend growth in the value of sports media rights, valuations of U.S. sports teams are expected to rise exponentially in the coming years.

In 2021 the NBA reformed its bylaws to allow pre-approved PE firms to acquire passive non-controlling stakes in NBA teams. However, to prevent the same beneficial owner from having indirect influence over competing teams, no one PE firm can acquire more than 20% of an individual NBA team and each NBA team can have a maximum 30% of ownership by PE investors17.

In response to the reforms, Dyal Capital raised its Homecourt Fund and has deployed the proceeds to acquire minority stakes in the Atlanta Hawks, Phoenix Suns and Sacramento Kings18. Meanwhile, competitor sports fund Arctos Partners acquired minority stakes in the Sacramento Kings, Golden State Warriors, Philadelphia 76ers and Utah Jazz19. Sportico reported that only 18 months after its initial investment, Dyal Capital has already enjoyed a lucrative exit of a portion of its stake in the Phoenix Suns to Mat Ishbia - the $4bn valuation for the Suns in December 2022 being the largest valuation ever recorded for an NBA team20. With U.S. sports betting legalization set to further increase monetization opportunities and given the trend growth in the value of sports media rights, valuations of U.S. sports teams are expected to rise exponentially in the coming years.

Women’s sport is seen as a fast-growing market with potential for broader distribution and monetization, creating a potentially huge opportunity for PE investment. The final of the women’s football European Championship in July 2022 was the most watched women’s football game in British history, with 17.4 million viewers on BBC One and a further 5.9 million on digital platforms21. The Lionesses’ victory in the tournament accelerated interest in the sport, and opened it to a much wider engaged audience. Attendance at Barclays Women’s Super League matches increased by 200% in the months following the event, reaching 6,000 per week. Meanwhile, the 2023 Women’s World Cup final drew a peak audience of 12 million viewers on BBC One and 5.6 million viewers in Spain22.

Research from The Sports Consultancy and advisory firm BDO indicates that women’s sport could be a better long-term investment given the greater opportunity for growth and development and the more flexible business structures relative to men’s sport, albeit starting from a far smaller base23. Revenues from women’s sport are expected to reach £1bn by 2030 from £350mn in 2021. While this would still be a very small fraction of the revenues generated by men’s sport, it represents a faster growth rate than for the overall sports market24.

Women’s sport is seen as a fast-growing market with potential for broader distribution and monetization, creating a potentially huge opportunity for PE investment. The final of the women’s football European Championship in July 2022 was the most watched women’s football game in British history, with 17.4 million viewers on BBC One and a further 5.9 million on digital platforms21. The Lionesses’ victory in the tournament accelerated interest in the sport, and opened it to a much wider engaged audience. Attendance at Barclays Women’s Super League matches increased by 200% in the months following the event, reaching 6,000 per week. Meanwhile, the 2023 Women’s World Cup final drew a peak audience of 12 million viewers on BBC One and 5.6 million viewers in Spain22.

Research from The Sports Consultancy and advisory firm BDO indicates that women’s sport could be a better long-term investment given the greater opportunity for growth and development and the more flexible business structures relative to men’s sport, albeit starting from a far smaller base23. Revenues from women’s sport are expected to reach £1bn by 2030 from £350mn in 2021. While this would still be a very small fraction of the revenues generated by men’s sport, it represents a faster growth rate than for the overall sports market24.

PE investments in tournaments such as The Six Nations and Silver Lake’s investment in the holding group behind Manchester City have included support for women’s sports teams and events as part of the broader project. But increasingly, PE is targeting standalone opportunities in women’s sports organizations. While in mid-2022 the UK’s Football Association turned down PE offers for participation in a new commercial entity to hold the Women’s Super League (WSL) and Championship in favor of other financing options25, the WSL is once again reported to be considering the possibility of raising up to £100mn in new funding from outside investors in order to help develop the game26. Meanwhile, CVC agreed a deal with the Women’s Tennis Association to invest $150mn in return for a 20% stake in the league’s commercial rights27. In March 2023, the two announced a strategic partnership, with CVC investing capital via its managed funds to drive growth of the sport28.

Deal Structures

While deal structures will naturally vary, PE investments in sport typically involve the creation of corporate vehicles in which the sponsors hold a minority economic stake, but a majority governance stake, to manage the commercial aspects of the relevant sport or league, such as media, broadcasting, sponsorship and other commercial rights. This allows existing shareholders and sporting organizations to loosen the reigns over the monetization of such rights, while maintaining control over sporting and regulatory matters, including oversight of league rules, regulatory and governance oversight and player welfare.

As in other contexts, the success of these structures hinges on the legal relationship between the various shareholders and other stakeholders to best reflect the commercial intentions of the parties. Shareholders’ agreements will need to be carefully drafted to ensure that the division of responsibility and control is clearly defined at the outset of an investment, that there are appropriate mechanisms for resolving shareholder disputes and deadlocks and the paths for exiting an investment are made explicit.

As the popularity of PE investment in sports continues to grow, we expect to see a greater number of private, PE and other institutional sponsors investing in the same or similar assets, giving rise to more complex capital structures, joint ownership rights and potential conflicts of interests, all of which will compound the importance of the negotiation of governance and structuring arrangements.

Exits

Sports investments tend to be longer in duration than traditional PE transactions in other sectors, in part reflecting the long-term growth opportunities as sports followings scale up, as well as the consistent cash flows which fixed term broadcasting and sponsorship details can provide. In addition, as many sports teams and leagues are considered to be cultural and heritage assets, exits are often defined by a high level of public and regulatory scrutiny. While successful cash-generative business will always be attractive to new institutional buyers, or appeal to public market investors in an IPO, PE firms may need to structure deals carefully with exits in mind.

Considerations can include the granting of call rights in favor of partners or other key stakeholders to buy out PE involvement over time or even, for riskier investments, put options. PE investors have also sold stakes to continuation funds that take over ownership of the interest after a number of years, giving limited partners the opportunity to exit or roll their holding into a new vehicle. Following a competitive process in 2019, Bridgepoint decided to reinvest in MotoGP and Superbike event organizer Dorna, alongside pension fund Canadian Pension Plan Investment Board, which had acquired a large minority stake in the business in 201229.

Tax Considerations

Tax is another important consideration for PE sponsors when structuring investments and exit opportunities in relation to sports assets. Investments that focus on media or merchandising rights are likely to involve valuable royalty payments, often cross-border. These can come with their own suite of tax challenges such as withholding taxes, transfer pricing, and occasionally more novel taxes including diverted profits taxes and direct taxes on offshore IP owners deriving income from certain jurisdictions. Sports businesses with digital platforms generating sales and advertising revenues may also need to consider the various digital services taxes that have been put into effect in many jurisdictions.

While not the principal focus of this article, traditional PE funds are not the only class of financial investors who have upped their investments in sport. In recent years, sovereign funds have made significant investment in a wide variety of sports, with Qatar’s sovereign wealth fund buying stakes in teams in the NBA, National Hockey League and Women’s NBA in June 202330. Saudi Arabia’s Public Investment Fund has also made moves, reportedly regarding Formula One, the purchase of Newcastle United and more recently agreeing the merger of the PGA and the Saudi-funded LIV golf league31.

These investments offer sovereign funds opportunities to diversify state economies and connect with global brands that reach global audiences. The scale of investment, if sustained, could be game-changing for a number of sports.

While not the principal focus of this article, traditional PE funds are not the only class of financial investors who have upped their investments in sport. In recent years, sovereign funds have made significant investment in a wide variety of sports, with Qatar’s sovereign wealth fund buying stakes in teams in the NBA, National Hockey League and Women’s NBA in June 202330. Saudi Arabia’s Public Investment Fund has also made moves, reportedly regarding Formula One, the purchase of Newcastle United and more recently agreeing the merger of the PGA and the Saudi-funded LIV golf league31.

These investments offer sovereign funds opportunities to diversify state economies and connect with global brands that reach global audiences. The scale of investment, if sustained, could be game-changing for a number of sports.

PE investment in sports is on the upswing as sponsors tune into the opportunities emerging at increasingly institutional scale, with sovereign investors now amongst those actively seeking a piece of the action. The ability of PE firms to bring commercial and technological expertise to sports leagues and teams seeking to reach an ever-expanding audience make an appealing match.

Deals can be structured to give PE sponsors a share of upside from new commercial vehicles focused on developing and maximizing revenue streams, while avoiding the day-to-day pressures of sporting decisions. However, emotions can still run high around the sector, so caution and due diligence are essential.