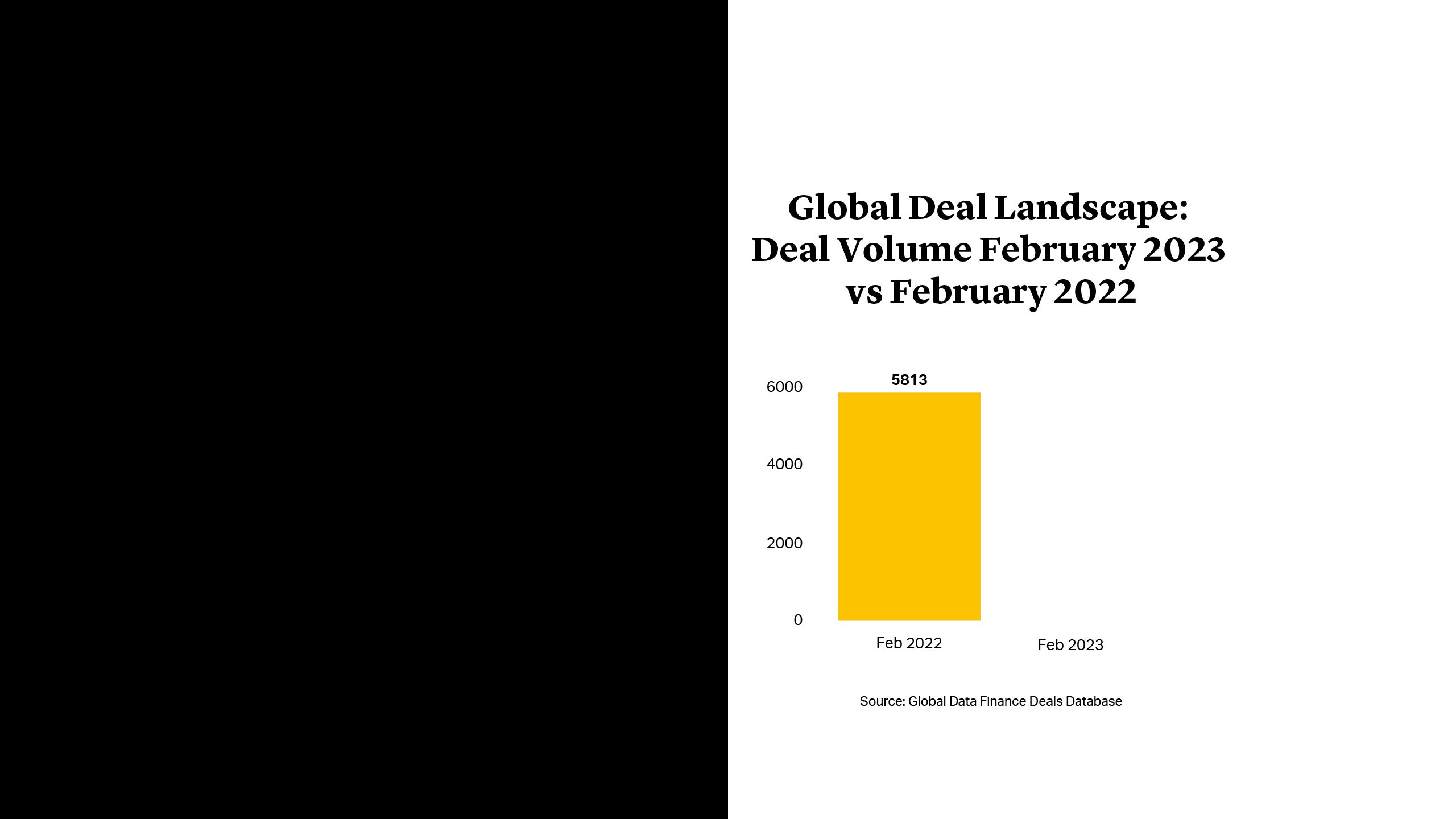

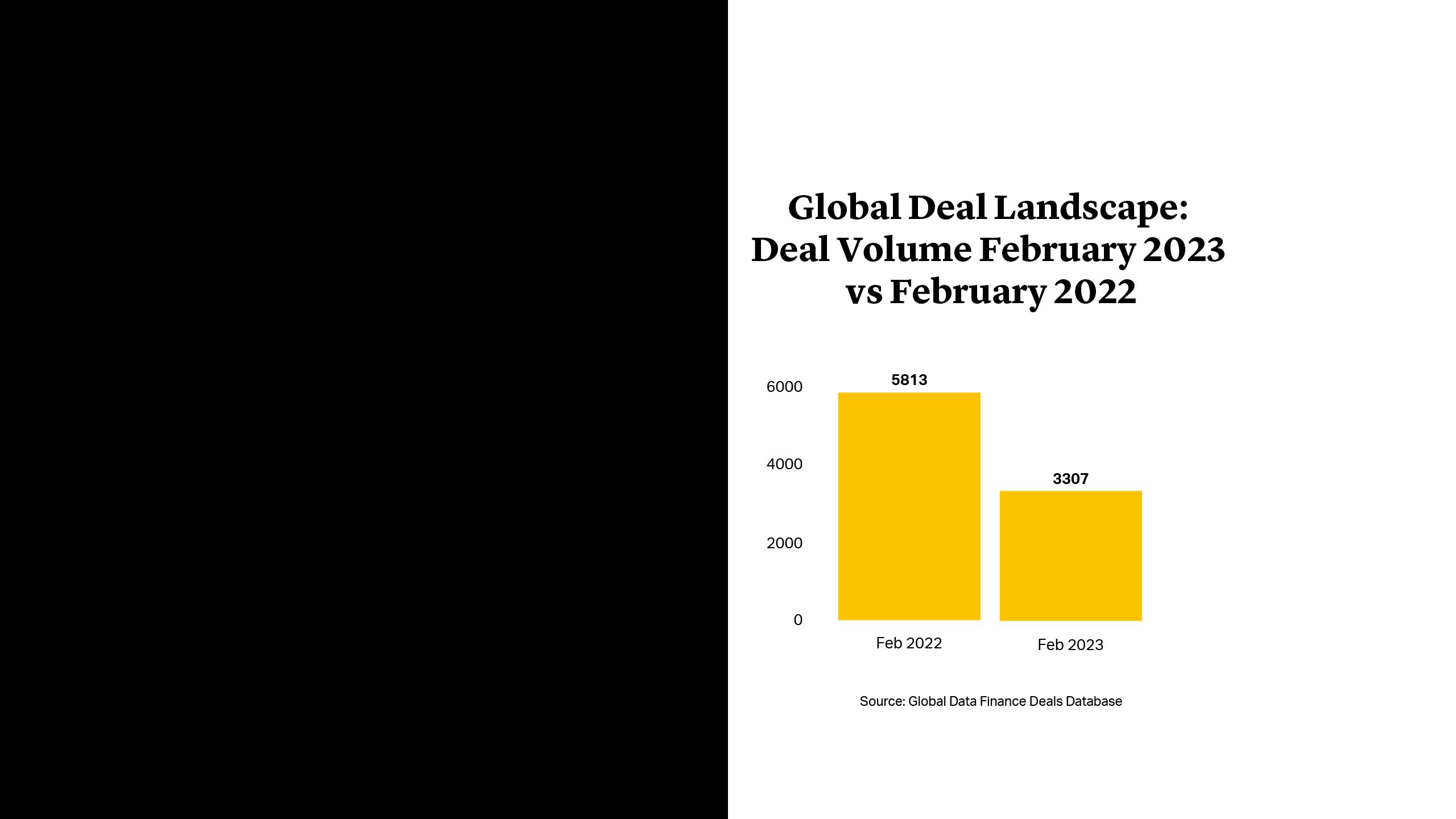

Global dealmaking has slumped in recent months as macroeconomic turmoil, coupled with geopolitical uncertainty, has opened up a gap between buyers and sellers. Year-on-year deal volumes fell by 43.1% in the 12 months to February 2023. Germany was no exception, recording a decline of 46.7%1.

This mismatch in pricing expectations is expected to be transitory. Deal activity will resume as private markets valuations adjust, and as greater clarity emerges around the depth of the downturn. In the meantime, however, there is one area of the economy that appears to be defying cyclicality — the energy transition, or as it is known in Germany, the Energiewende.

Global dealmaking has slumped in recent months as macroeconomic turmoil, coupled with geopolitical uncertainty, has opened up a gap between buyers and sellers. Year-on-year deal volumes fell by 43.1% in the 12 months to February 2023. Germany was no exception, recording a decline of 46.7%1.

This mismatch in pricing expectations is expected to be transitory. Deal activity will resume as private markets valuations adjust, and as greater clarity emerges around the depth of the downturn. In the meantime, however, there is one area of the economy that appears to be defying cyclicality — the energy transition, or as it is known in Germany, the Energiewende.

Investor Appetite Spurs Energy Transition Offerings

Despite a lack of distributions and the pervasive denominator effect, institutional investor appetite for financing the energy transition remains strong. Supported by Europe’s Sustainable Finance Disclosure Regulation (SFDR), funds with a decarbonization agenda are optimally positioned in what is otherwise undoubtedly a challenging fundraising environment.

The market has responded to this demand with a number of new energy transition products, including some very substantial offerings. Brookfield Asset Management raised $15bn for its energy transition debut in 2022 and is already close to being fully invested with plans for a successor vehicle underway. Blackstone, meanwhile, has created a dedicated energy transition business targeting what it terms the $3.5tn of capital investment required annually to meet global carbon reduction goals.

Elsewhere, TPG Rise Climate amassed $7.3bn last year and a team of former Riverstone partners spun out to form Sandbrook Capital, which is seeking to target mid-market energy transition opportunities. Tikehau Capital has raised €1bn to help fight global warming by funding the growth of emerging corporate leaders in the energy transition space and investing in European SMEs providing the tools to respond to the climate emergency. Golding Capital Partners has also expanded its product range with a €300mn fund focused on investments helping achieve the goals defined by climate agreements.

Energy transition product launches are clearly proliferating at a remarkable rate as appetite for sustainability continues to outstrip market uncertainty.

Accelerating the Energiewende

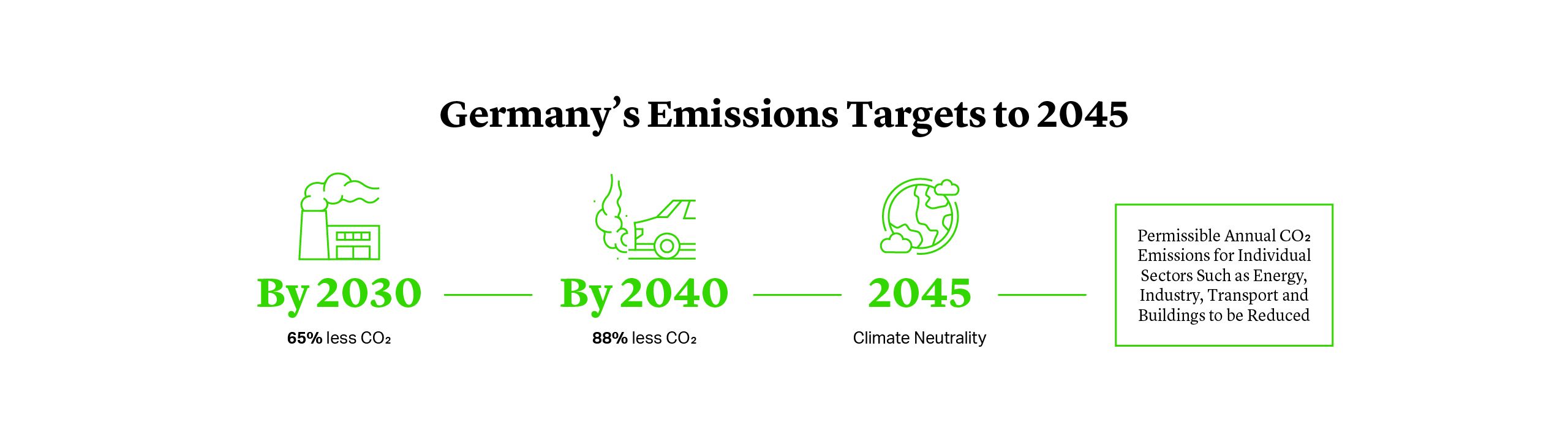

At the same time, Germany’s coalition government is significantly ramping up the country’s energy transition efforts, particularly after the wake-up call provided by Russia’s invasion of Ukraine. Once an early mover in the world of Cleantech, the Energiewende had arguably lost momentum in the run up to the war, but a series of new laws were created in 2022 to get Germany’s transition back on track.

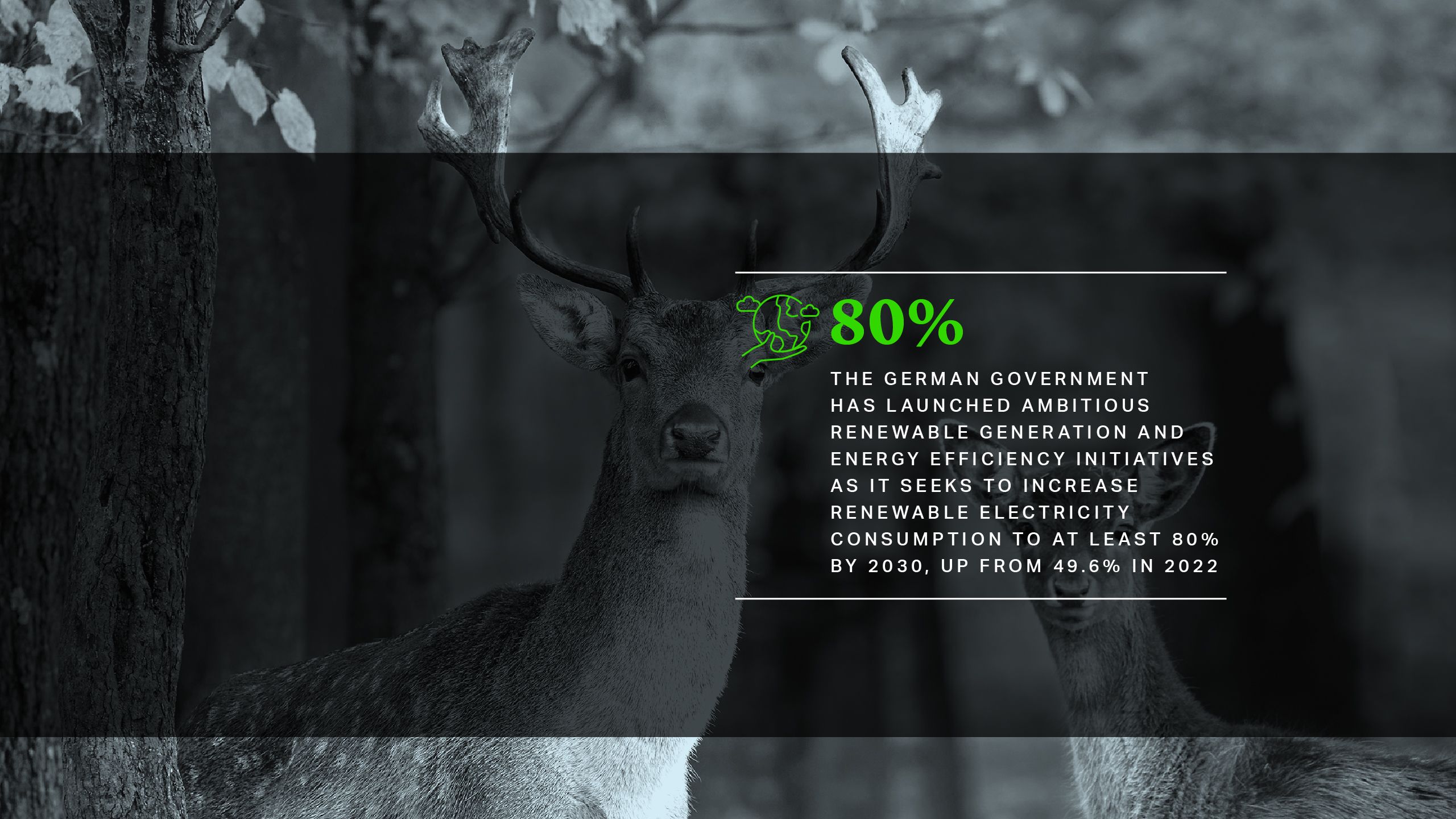

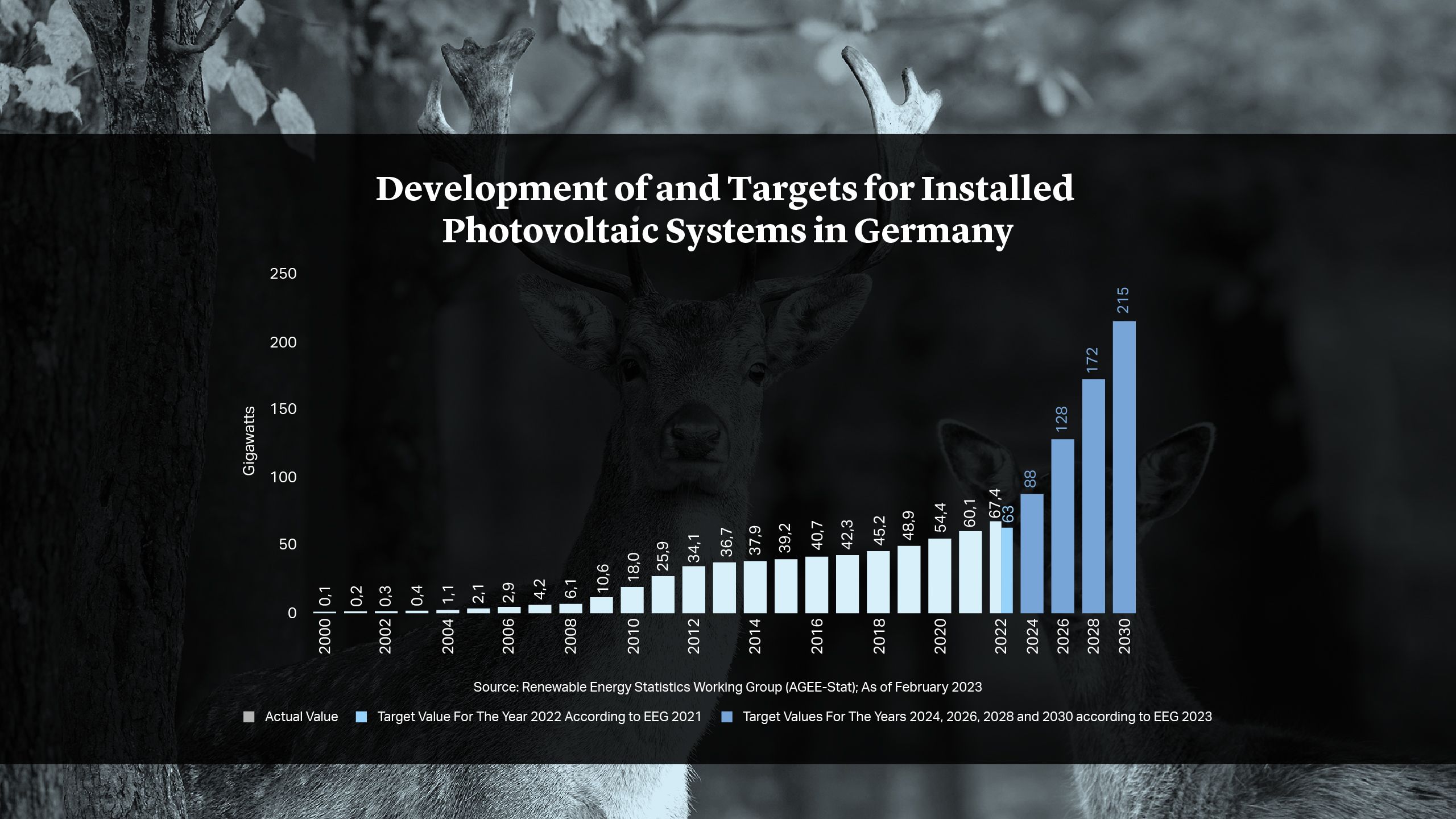

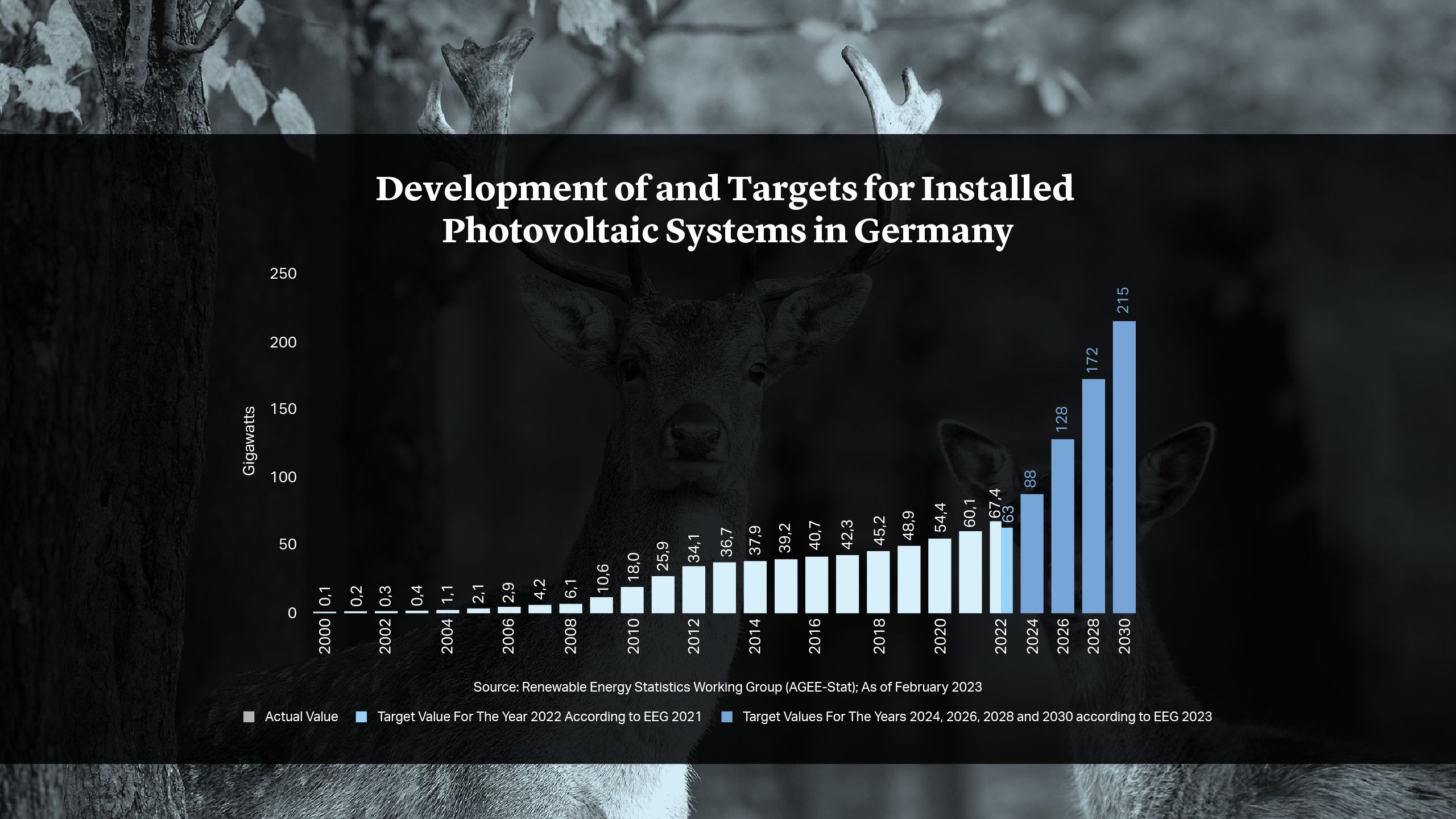

Indeed, despite the return of coal-fired power plants and the construction of new import infrastructure for liquefied natural gas to shore up short-term supply security, the government has launched some of the most ambitious renewable generation and energy efficiency initiatives that the country has seen as it seeks to increase renewable electricity consumption to at least 80% by 2030, up from 49.6% in 20222.

This is creating significant investment opportunities for private capital in the construction of new onshore and offshore wind projects, as well as distributed solar. The government is aiming for 115 gigawatts, 30 gigawatts and 215 gigawatts of installed capacity respectively by the 2030 deadline. This means doubling current onshore wind power generation, tripling solar and quadrupling offshore wind. Government subsidies have been increased accordingly and pledges made to ease permitting bottlenecks and guarantee the availability of land.

Critically, a major revamp of the country’s power grid is also planned, in order to cope with the inherent intermittency of renewables. Major investment will be required in transmission infrastructure, in particular, in order to link Germany’s wind capacity in the North with its industrial base in the South. E.on has announced upwards of $30bn of investment in grid modernization, digitization and decarbonization.

Meanwhile, at the same time as investing in the production and transmission of clean electricity, Germany is also taking a lead when it comes to reducing demand. The country aims to reduce consumption by 20% and has mandated a set of energy savings provisions including a range of heating system maintenance and optimization measures, creating additional impetus for an energy efficiency sector that is already a firm private equity favorite.

The scope of the investment opportunity in Germany was demonstrated by a €215mn series D funding round in Enpal, led by TPG Rise Climate, earlier this year. Enpal has 30,000 customers in the country, installing over 2,000 solar energy systems per month, as well as integrated packages covering everything from EV chargers to smart energy management. The company has surpassed €400mn in revenues, finished 2022 in profitability and has been ranked the number one fastest growing energy company in Europe3.

Accelerating the Energiewende

At the same time, Germany’s coalition government is significantly ramping up the country’s energy transition efforts, particularly after the wake-up call provided by Russia’s invasion of Ukraine. Once an early mover in the world of Cleantech, the Energiewende had arguably lost momentum in the run up to the war, but a series of new laws were created in 2022 to get Germany’s transition back on track.

Indeed, despite the return of coal-fired power plants and the construction of new import infrastructure for liquefied natural gas to shore up short-term supply security, the government has launched some of the most ambitious renewable generation and energy efficiency initiatives that the country has seen as it seeks to increase renewable electricity consumption to at least 80% by 2030, up from 49.6% in 20222.

This is creating significant investment opportunities for private capital in the construction of new onshore and offshore wind projects, as well as distributed solar. The government is aiming for 115 gigawatts, 30 gigawatts and 215 gigawatts of installed capacity respectively by the 2030 deadline. This means doubling current onshore wind power generation, tripling solar and quadrupling offshore wind. Government subsidies have been increased accordingly and pledges made to ease permitting bottlenecks and guarantee the availability of land.

Critically, a major revamp of the country’s power grid is also planned, in order to cope with the inherent intermittency of renewables. Major investment will be required in transmission infrastructure, in particular, in order to link Germany’s wind capacity in the North with its industrial base in the South. E.on has announced upwards of $30bn of investment in grid modernization, digitization and decarbonization.

Meanwhile, at the same time as investing in the production and transmission of clean electricity, Germany is also taking a lead when it comes to reducing demand. The country aims to reduce consumption by 20% and has mandated a set of energy savings provisions including a range of heating system maintenance and optimization measures, creating additional impetus for an energy efficiency sector that is already a firm private equity favorite.

The scope of the investment opportunity in Germany was demonstrated by a €215mn series D funding round in Enpal, led by TPG Rise Climate, earlier this year. Enpal has 30,000 customers in the country, installing over 2,000 solar energy systems per month, as well as integrated packages covering everything from EV chargers to smart energy management. The company has surpassed €400mn in revenues, finished 2022 in profitability and has been ranked the number one fastest growing energy company in Europe3.

Decarbonizing Industry

The decarbonization of industries such as steel, cement and chemicals is also critical to the energy transition in Germany, which is both Europe’s biggest economy and its biggest emitter. Ambitious and detailed targets for reducing these emissions are enshrined in law and support packages are in place to bolster the development of new technologies such as green hydrogen and to help drive demand for clean energy through Carbon Contracts for Difference.

But corporates are also looking to raise funds to support the necessary upgrading of their businesses through the sale of non-core divisions and minority stakes, which may create an interesting new source of deal flow for private markets players as well.

Chemicals companies, for example, may seek to channel proceeds from disposals into costly green transformations, while utilities can use the capital from carve-outs to upgrade networks and develop the infrastructure required for electric vehicles.

A similar trend has already played out in the telecommunications space as incumbents sought to free up capital to fund the rollout of 5G and other industry developments. GIP and KKR took a stake in Vantage Towers alongside Vodafone, for example, and Deutsche Telekom sold a stake in Deutsche Funkturm, Germany’s biggest provider of radio infrastructure, to DigitalBridge and Brookfield. As pressure to decarbonize mounts for Germany’s industrial giants, expect similar moves in the country’s hard-to-abate sectors.

Indeed, in a market where M&A opportunities are, for now at least, scarce and fundraising tough, Germany’s Energiewende narrative is looking increasingly compelling for private markets. The weight of institutional capital is leaning heavily towards sustainability at the same time that Germany’s transition is moving up several gears.

This confluence of forces is likely to produce compelling propositions across the board, from growth capital investments in emerging clean technologies and energy efficiency solutions, to infrastructure generation and transmission plays, as well as corporate carve-outs for private equity.

The energy transition, it seems, is the one mega theme capable of overpowering today’s deal flow inertia.