The Case for “Creditor-on-Creditor Violence” in European Restructurings

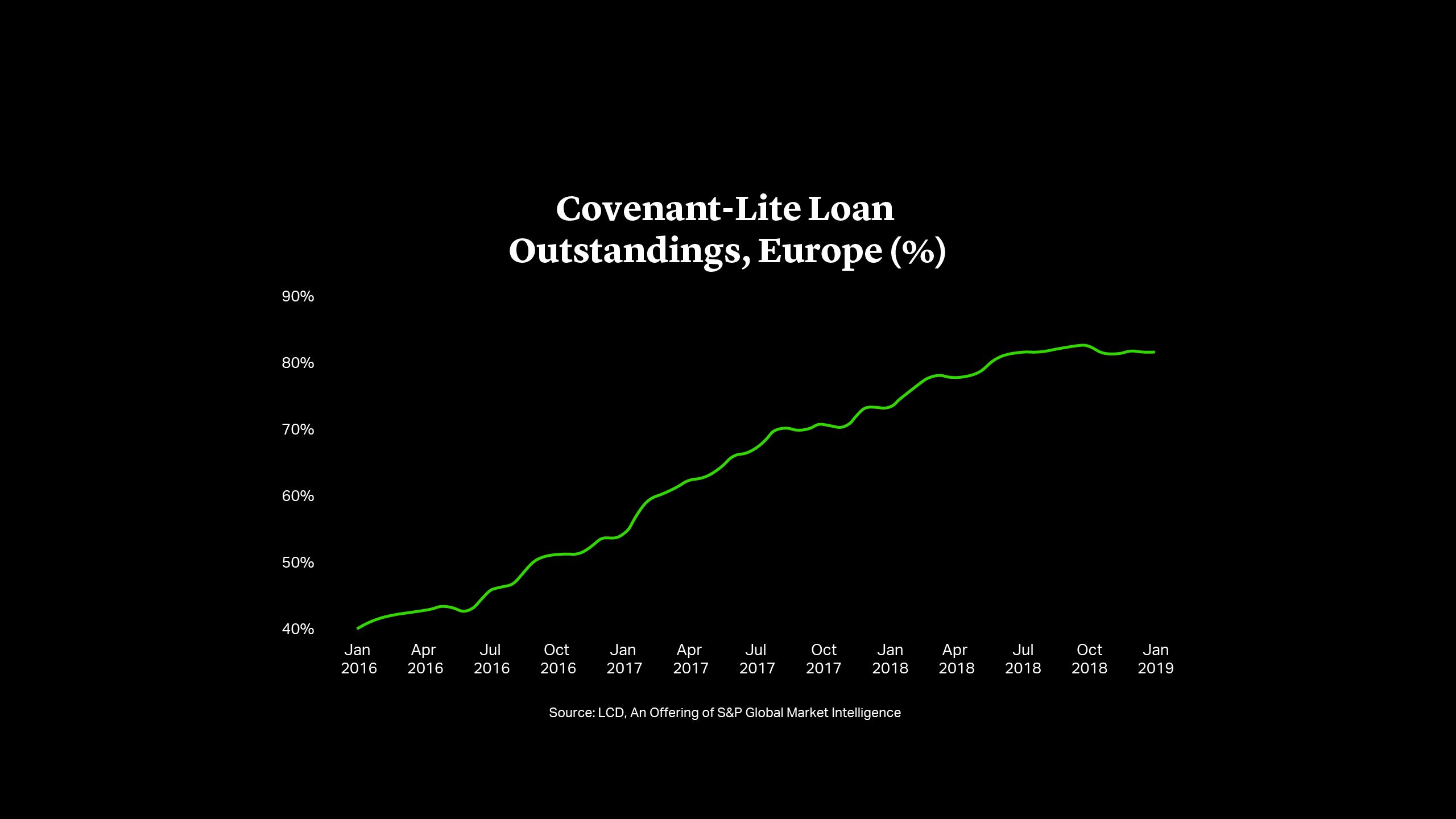

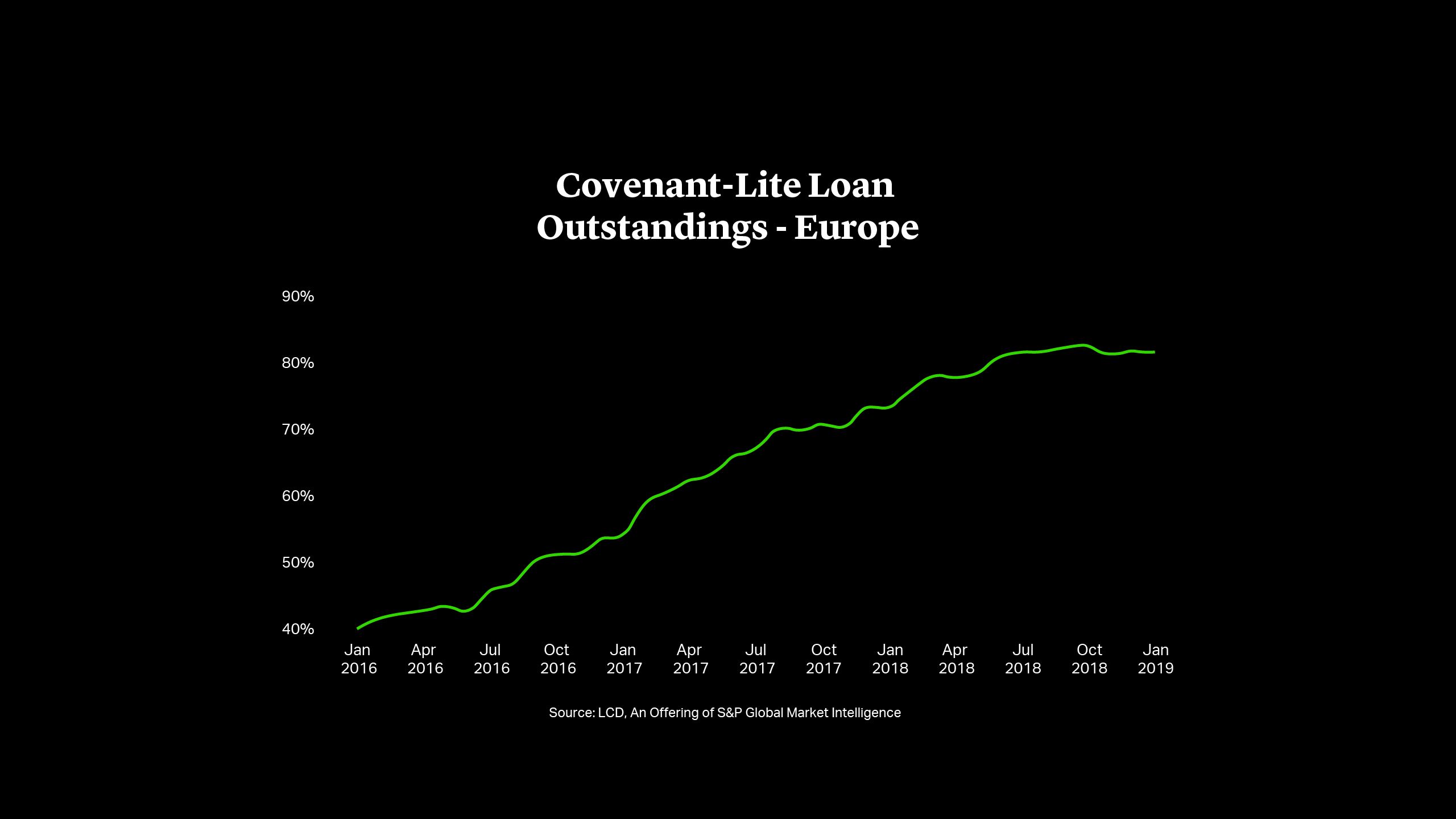

The prevalence of covenant-lite terms on leveraged buyout debt means that many companies today are not showing the warning lights that might typically alert lenders to looming credit issues. The provision of covenant-lite lending boomed in the late 2010s to reach some 82% of all outstanding leveraged loans in 2019, roughly double the level of 2016, according to S&P Global data1. The result of looser lending terms has been fewer cases of restructuring through COVID-19 disruption and more recent inflation-led market volatility.

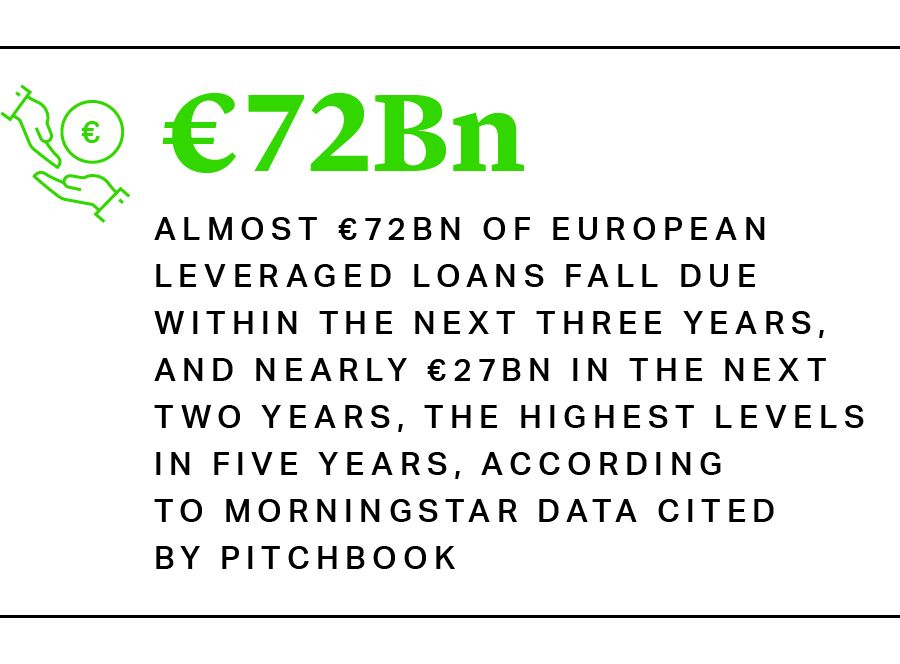

Yet, rising interest rates are combining with falling earnings amid stalling economic growth to put increased pressure on private equity-owned businesses across Europe. The deteriorating economic environment is combining with looming debt maturities and constrained refinancing markets. Almost €72bn of European leveraged loans fall due within the next three years, and nearly €27bn in the next two years, the highest levels in five years, according to Morningstar data cited by PitchBook. Taken together, these factors are creating the conditions for an increase in restructuring cases.

The prevalence of covenant-lite terms on leveraged buyout debt means that many companies today are not showing the warning lights that might typically alert lenders to looming credit issues. The provision of covenant-lite lending boomed in the late 2010s to reach some 82% of all outstanding leveraged loans in 2019, roughly double the level of 2016, according to S&P Global data1. The result of looser lending terms has been fewer cases of restructuring through COVID-19 disruption and more recent inflation-led market volatility.

Yet, rising interest rates are combining with falling earnings amid stalling economic growth to put increased pressure on private equity-owned businesses across Europe. The deteriorating economic environment is combining with looming debt maturities and constrained refinancing markets. Almost €72bn of European leveraged loans fall due within the next three years, and nearly €27bn in the next two years, the highest levels in five years, according to Morningstar data cited by PitchBook. Taken together, these factors are creating the conditions for an increase in restructuring cases.

Private Equity-Backed Companies Face Increased Stress

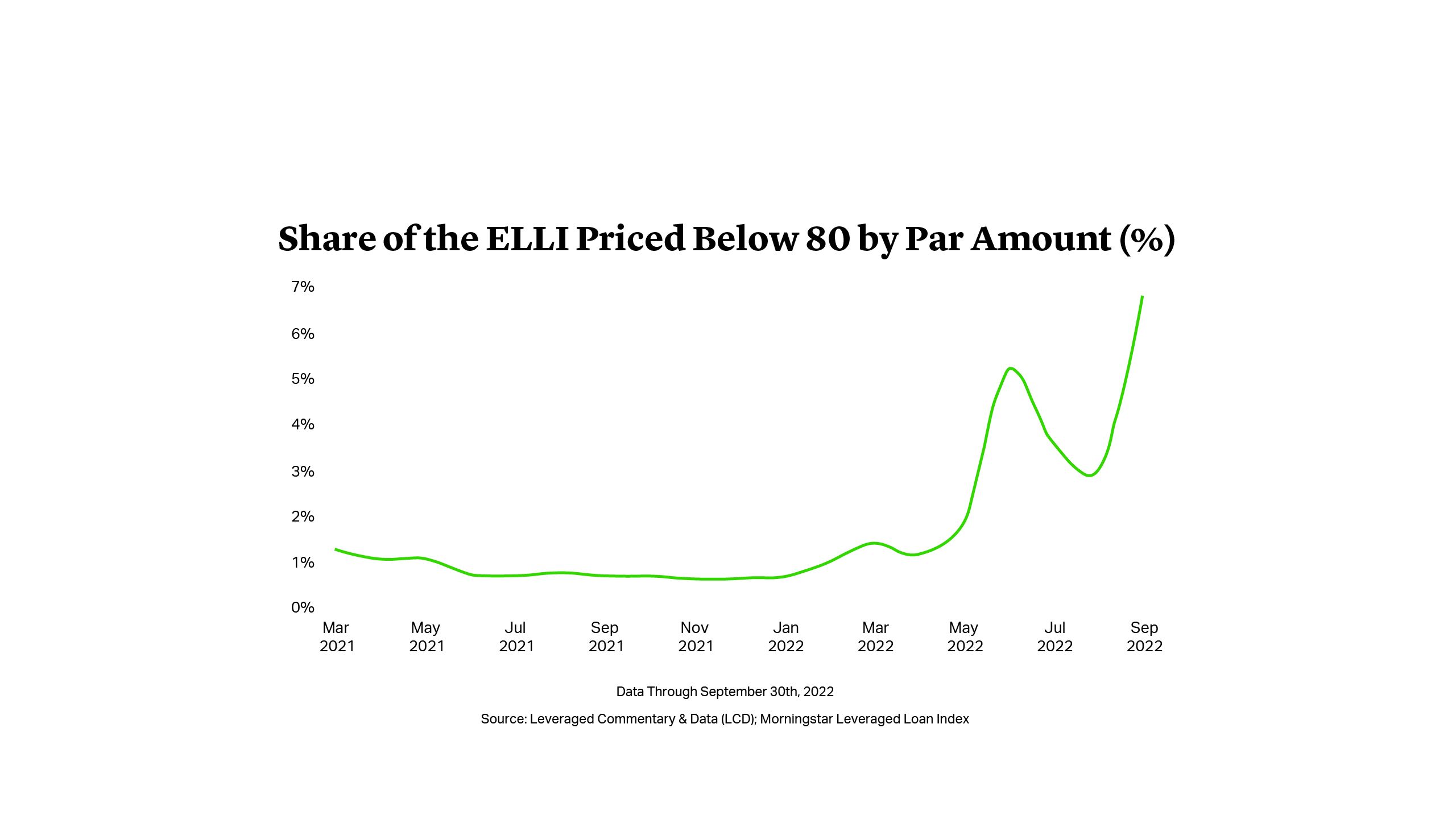

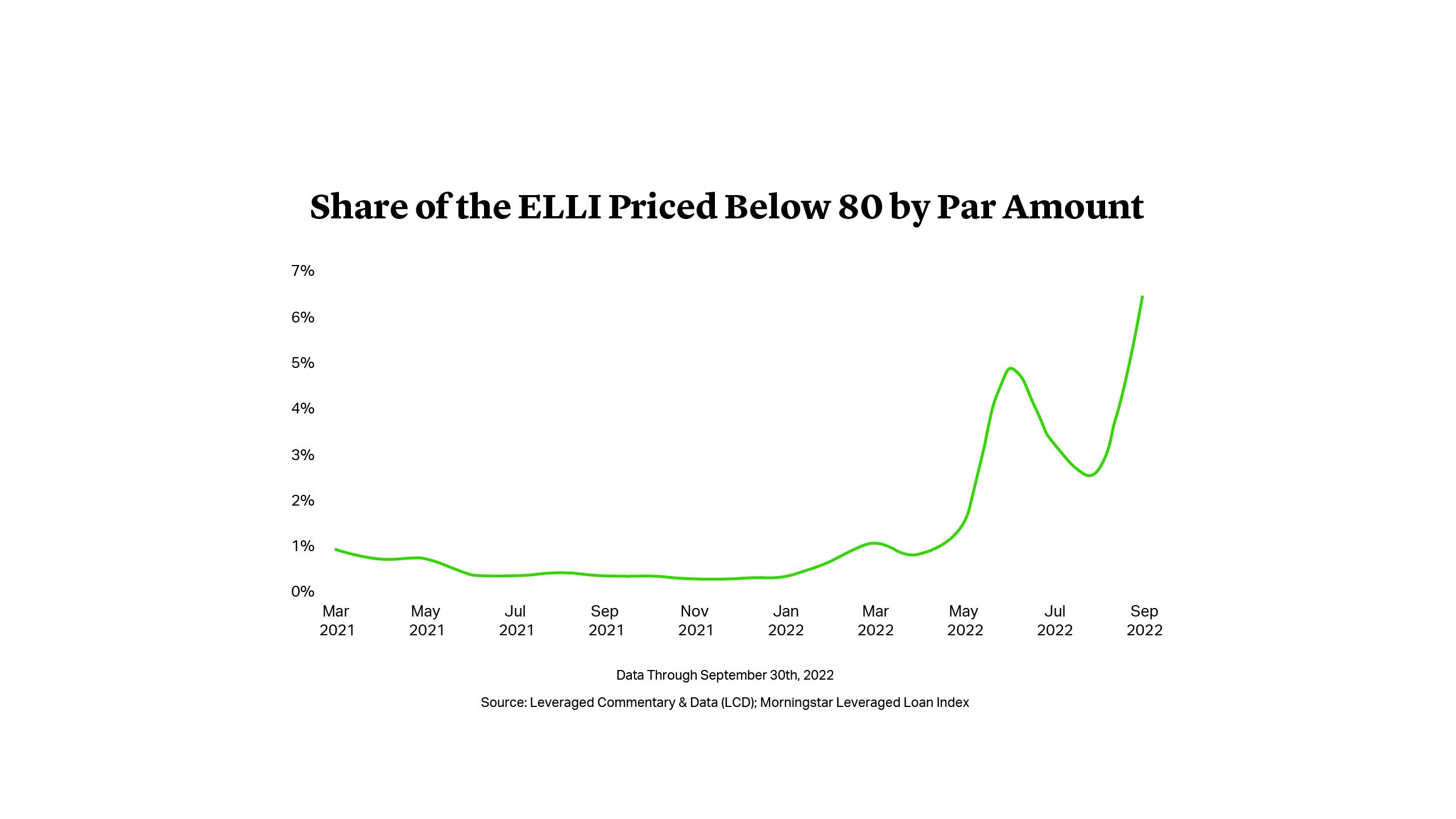

Recent research from ratings agencies indicates that default levels for European leveraged loans are expected to reach 4% in 2023, just one percentage point above the long-term average for the sector, according to M&G Investments2. However, loan pricing is pointing to higher levels of concern among credit investors. By end-September, the proportion of credit trading at distressed levels (below 80% of par value) was 6.5%, with over 30% of loans trading at stressed levels of 80% to 89.99% of par, Morningstar figures showed3.

While covenant-lite debt terms and regulatory frameworks in Europe allow companies to run closer to insolvency levels for longer, some company advisers and directors find themselves in the unprecedented position of warning that businesses are facing liquidity challenges. In such circumstances, private equity firms need to get on the front foot to proactively manage restructurings before they become value-destructive insolvency situations. To do so, they have a number of tools to protect value in their investments and retain control of their portfolio companies.

Private Equity in Position of Strength to Lead Restructurings

Limited covenants on European buyout debt have reduced the ability of lenders to exert pressure on private equity owners when portfolio companies are seen to come under financial stress. The corollary is that sponsors today are in a stronger position to push through restructuring terms and can harness their relationships with certain lenders to manage situations and get influential groups on side.

Known as “creditor on creditor violence”, these scenarios effectively pit one group of creditors against another and can enable private equity owners to stay invested and in control of their companies. They fall into two broad categories:

These arrangements were innovated in 2017 in the case of fashion retailer J.Crew. Faced with looming maturities on its PIK notes, the company moved some $250mn of intellectual property into an unrestricted subsidiary, which it then used as collateral to refinance its notes. In essence, drop-downs allow for certain company assets to be moved out of the broader creditor pool, or for some creditors to receive an enhanced call on those assets in a restructuring scenario.

Seeking additional finance at the height of the pandemic, U.S. bedding company Serta Simmons permitted some existing lenders to exchange their loans for over $1bn in new super-priority debt, a deal from which other lenders were excluded and found their loans subordinated. As such, up-tiering deals enable some creditors to move up the capital structure and past other lenders, giving them priority in a debt restructuring.

Both restructuring mechanisms effectively require sponsors to negotiate with a group of creditors and exclude other lenders from access to the terms. Invariably, such deals can end up in court as excluded creditors look to challenge the agreements. Recent rulings have indicated that sponsors may not have it all their own way. The decision of a New York court in October last year to allow claims to be heard against an “up-tiering” by Oaktree Capital and term lenders to surfing fashion group Boardriders does provide a glimmer of hope to excluded creditors, not necessarily on the terms of the “up-tiering”, but rather the amendment of a “no action” clause to shut down potential litigation4.

Faced with maturing debt, European private equity firms are investigating similar tactics in Europe. BC Partners was reported to have attempted to extend the existing debt package of Israel-headquartered plastic furniture maker Keter with terms that would have given those that agreed a margin uplift, while stripping key covenants from the loan. While the proposal was later dropped, it would have effectively left non-consenting lenders with a potentially unsecured credit at a lower margin than consenting lenders5.

Distressed Debt Funds Reposition for Changing Credit Conditions

The absence of covenant breaches and traditional default scenarios is changing the landscape for distressed debt investors. With private equity firms requiring liquidity options for companies while aiming to remain in control, funds are evolving to take advantage of the new conditions. Oaktree rebranded its flagship vehicle, which raised some $16bn in 2021, as its Opportunities Fund to reflect its approach in a variety of credit situations6. More recently, the firm raised €1.2bn for a European private debt vehicle that aims to help fill the funding gap left by traditional lenders7.

Other firms have moved into the space – alongside their more traditional private equity offerings. BC Partners launched its private credit arm in 2017 and is reported to be seeking $1.25bn for its third fund targeted at U.S. and European opportunities8.

Distressed Debt Funds Reposition for Changing Credit Conditions

The absence of covenant breaches and traditional default scenarios is changing the landscape for distressed debt investors. With private equity firms requiring liquidity options for companies while aiming to remain in control, funds are evolving to take advantage of the new conditions. Oaktree rebranded its flagship vehicle, which raised some $16bn in 2021, as its Opportunities Fund to reflect its approach in a variety of credit situations6. More recently, the firm raised €1.2bn for a European private debt vehicle that aims to help fill the funding gap left by traditional lenders7.

Other firms have moved into the space – alongside their more traditional private equity offerings. BC Partners launched its private credit arm in 2017 and is reported to be seeking $1.25bn for its third fund targeted at U.S. and European opportunities8.

Takeaways for Staying in Control in Challenging Credit Markets

The deteriorating market conditions combined with the proliferation of covenant-lite terms present both opportunities and threats to private equity firms. The fiduciary duties on company directors may lead them to voice their concerns about liquidity or solvency issues impacting businesses. Firms should resist removing directors who raise issues but rather seek to protect companies and their directors against threats from creditors, who themselves may be getting organised and aligned for action.

Sponsors should also be aware that these circumstances give them greater power than they may have had in previous restructuring cycles. To take advantage of the opportunity, it is important to move fast and execute quickly.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card

Michael James

Partner

London

T: +44 20 7614 2219

mjames@cgsh.com

V-Card

Solomon J.Noh

Partner

London

T: +44 20 7614 2306

sjnoh@cgsh.com

V-Card