Private Equity Snapshot

European Investment

Remains Resilient in

Challenging Conditions

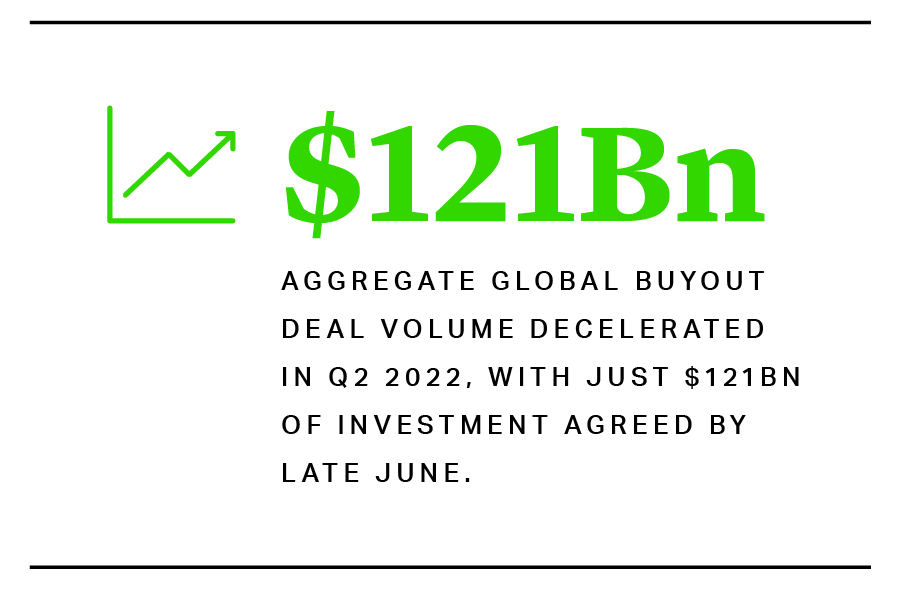

Conflict in Ukraine, persistent inflation, political instability, rising interest rates, and fear of recession set the backdrop for rising caution in the first half of 2022. Against record private equity and venture capital investment in the rebound of 2021, sponsor activity slowed as enthusiasm for lightning-quick deals gave way to more circumspection – although compared with longer term averages, investment levels remained robust. Aggregate global buyout deal value dipped only moderately in the first quarter of 2022 but decelerated more noticeably in the second, with just $121bn of investment agreed by late June, compared with the record of $236bn during Q2 of 2021, according to Preqin. VC investment also fell significantly from 2021 highs.

Auction processes lengthened to reflect the increased need for due diligence into a wider range of potential risks, including the ability of a target to withstand economic and supply chain turbulence. While some auction terms evened out, overall, the terms remained seller favourable, with buyers still generally expected to seek warranty & indemnity insurance for recourse.

Mega-Deals and Take-Privates Remain a Feature

The availability of capital in the hands of large, experienced managers was also in full evidence in the first half of the year. Appetite for “mega-deals” was not off the table, as Blackstone and the Benetton family targeted Italian infrastructure group Atlantia and were reported to be close to securing the green light from the Italian government for their €58bn bid in June. Other notable deals included Hg buying a large minority stake in Swedish-founded enterprise software firm IFS from EQT and TA Associates at a $10bn valuation1.

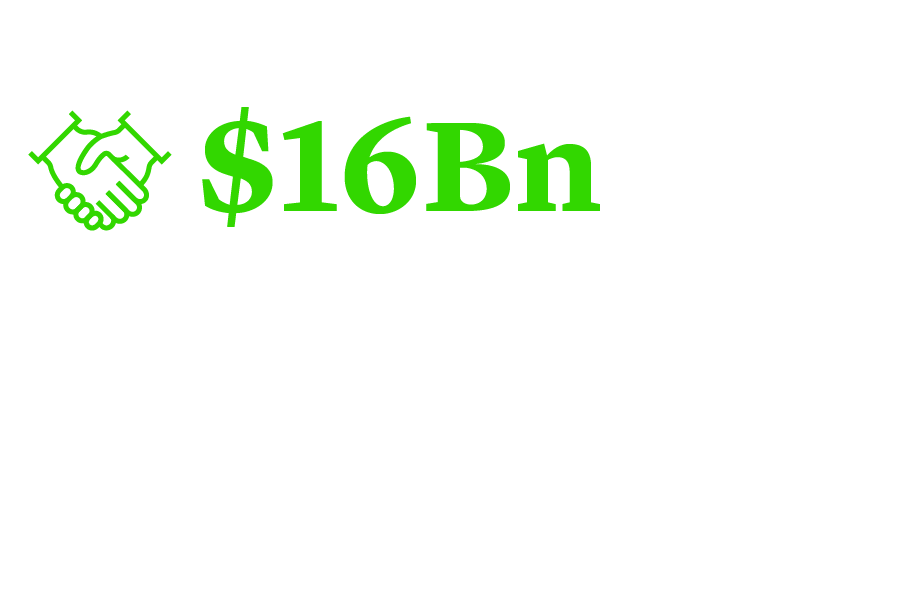

In the public markets, share prices came under pressure, and sponsors identified buying opportunities. The UK remained front and centre for take-privates, but other European markets including the Netherlands also saw activity. Towards the end of first quarter, a consortium of Elliott Management’s private equity arm and Brookfield agreed a $16bn takeover of UK-based TV ratings group Nielsen2, while in July financial publisher Euromoney Institutional Investor agreed to a £1.61bn offer from Astorg and Epiris, their fifth approach after four rejected overtures3.

VC Funding Slowdown as Start-Ups Feel the Squeeze

Europe and the UK saw a record high in VC activity during the opening months of 2022, with UK activity alone reaching a record high of $9bn4. Notable funding rounds included $1bn raised by UK fintech Checkout.com, valuing it at $40bn5, and $550mn for French healthtech Doctolib, giving it a valuation of $6.4bn6. However, Q2 saw activity follow the slowdown witnessed in North America and Asia earlier this year, with UK activity dropping to $7.1bn7.

There were also signs of the market disruption affecting some of Europe’s most highly valued start-ups as the first half progressed. Swedish payments group Klarna announced that it was laying off 700 staff – some 10% of its global workforce – to contain costs and conserve cash, as its valuation decreased rapidly from 2021 highs. Others, including grocery delivery start-ups Gorillas and Getir also reduced staff numbers.

Leading Sponsors Raising Record Funds

Underpinning private equity activity has been a period of strong fundraising, particularly for some of the largest and most sought-after funds in the market. Advent International announced that it had reached the $25bn hard cap for its tenth global fund in May, while in Europe, Hg raised $8bn for its large-cap Saturn fund and was reported to be seeking over $6bn for its mid-market vehicle. Other large funds are in the pipeline, including EQT, which is seeking €20bn for its tenth fund8, a near 30% increase on its predecessor which reached final close in April 2021.

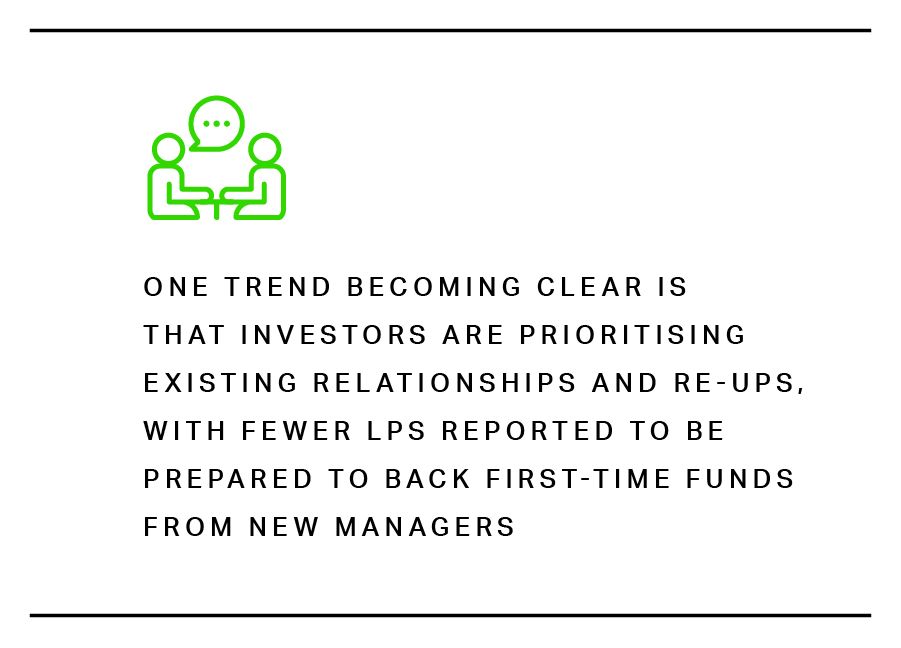

One trend becoming clear is that investors are prioritising existing relationships and re-ups, with fewer LPs reported to be prepared to back first-time funds from new managers9.

H2 Private Equity Outlook

Late June marked private equity’s main annual gathering in Berlin. The SuperReturn event captured the market mood over several interesting days – caution combined with optimism for investment opportunities in the market dislocation. Carlyle Group’s European co-head Marco de Benedetti argued that private equity investment has peaked10. However, KKR’s European co-head Philipp Freise predicted that the crisis would trigger a wave of innovation and accelerate the transformation of the European economy11.

Although the active deal pipeline is still relatively full, in the weeks and months to come it is likely that only the more resilient assets will be brought to market. Companies struggling in the headwinds are more likely to be held back. Much could change in short time – a resolution to the conflict in Ukraine could be the precursor to another burst of investment activity. However, unless a period of geopolitical calm can also calm rising inflation and interest rates, the more circumspect climate will continue.

Buyer and Seller Expectations Diverge

Auctions that started in the first half, or which are being prepared for launch over the summer, continue to feature seller-friendly terms and come with full valuation expectations that might have reflected conditions at the start of the year. Sell-side advisers are sending large numbers of teasers to prospective buyers, although increasing numbers of sponsors are prepared to walk away from processes if they are unconvinced. In June, listed UK fashion group Ted Baker was forced to go back to previous bidders after Authentic Brands – its preferred bidder, with backers including CVC and HPS Investment Partners – withdrew12.

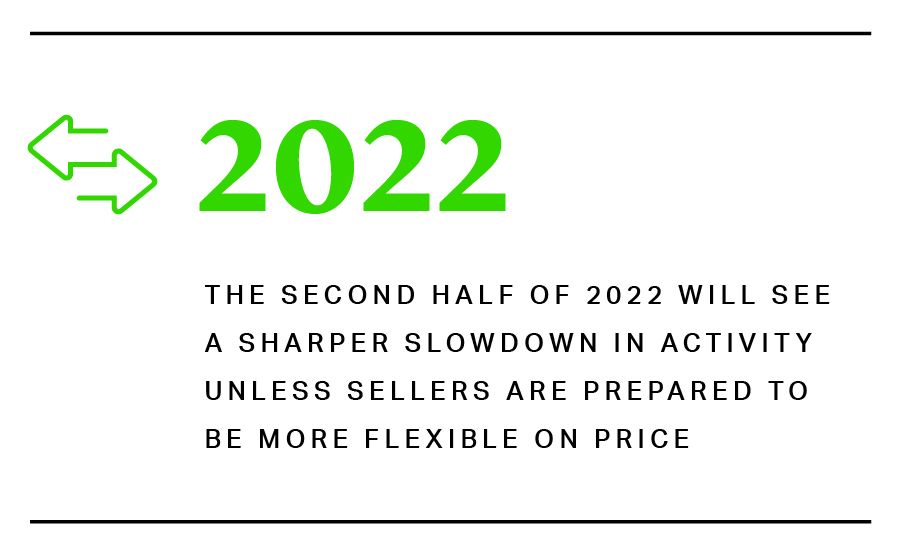

The second half of 2022 will see a sharper slowdown in activity unless sellers are prepared to be more flexible on price. Following Thoma Bravo’s move to renegotiate a price reduction for its takeover of U.S. software group Anaplan, there may also be scope for sponsors to take a harder line on deals in Europe.

Private Debt Grows its Share of the Financing Mix

While European banks continue to lend for buyouts, that supply of financing is reducing. By mid-June, quarterly European leveraged loan issuance was just €5.9bn, putting the continent on track for its worst performance since the first quarter of 200913.

Unlike the financial crisis, however, sponsors have financing options in the growing private debt market. Traditional lenders are also syndicating debt directly to private debt funds, which could ensure that financing remains available – albeit with higher pricing – for strong companies throughout the second half of 2022.

Michael J. Preston

Partner

London

T: +44 20 7614 2255

mpreston@cgsh.com

V-Card

Gabriele Antonazzo

Partner

London

T: +44 20 7614 2353

gantonazzo@cgsh.com

V-Card