Private Equity

Market Snapshot

November 2023

Private equity activity remained subdued in the third quarter of 2023 in the face of persistent challenging conditions. Global investment value was down 18% year-on-year to $105bn, according to S&P Global Market Intelligence, with the number of deals also contracting to 2,668 from almost 4,000 in the third quarter of last year. Quarter-on-quarter investment value showed only a modest decline, indicating that the downturn may be bottoming, albeit at around a third of the maximum quarterly level seen during 20211.

The data contains signals of more positive momentum in Europe. The continent posted the highest investment value of any region in September, thanks to the largest deals globally in both private equity and venture capital. TDR and I Squared launched a competing offer to buy Spanish industrial testing company Applus for almost $2.4bn, while Sweden’s H2 Green Steel raised €1.5bn in venture funding from investors including Altor, GIC, Temasek, and Al Gore’s Just Climate fund.

Private equity activity remained subdued in the third quarter of 2023 in the face of persistent challenging conditions. Global investment value was down 18% year-on-year to $105bn, according to S&P Global Market Intelligence, with the number of deals also contracting to 2,668 from almost 4,000 in the third quarter of last year. Quarter-on-quarter investment value showed only a modest decline, indicating that the downturn may be bottoming, albeit at around a third of the maximum quarterly level seen during 20211.

The data contains signals of more positive momentum in Europe. The continent posted the highest investment value of any region in September, thanks to the largest deals globally in both private equity and venture capital. TDR and I Squared launched a competing offer to buy Spanish industrial testing company Applus for almost $2.4bn, while Sweden’s H2 Green Steel raised €1.5bn in venture funding from investors including Altor, GIC, Temasek, and Al Gore’s Just Climate fund.

Public markets continue to yield opportunities for private equity. In early October, Apollo agreed a £506mn deal for The Restaurant Group, the UK-listed owner of the Wagamama chain, following Permira’s £703mn investment in biopharma services company Ergomed in early September, which highlighted ongoing interest and opportunity in the British biotech and healthcare space.

However, persistent volatility and tough negotiations with company boards present complexity for private equity firms. A recent survey from Numis found that almost three-quarters of dealmakers have shifted their focus towards private companies, in anticipation of a wave of private equity divestments – a change from last year when the same proportion were eyeing more take-privates2.

Public markets continue to yield opportunities for private equity. In early October, Apollo agreed a £506mn deal for The Restaurant Group, the UK-listed owner of the Wagamama chain, following Permira’s £703mn investment in biopharma services company Ergomed in early September, which highlighted ongoing interest and opportunity in the British biotech and healthcare space.

However, persistent volatility and tough negotiations with company boards present complexity for private equity firms. A recent survey from Numis found that almost three-quarters of dealmakers have shifted their focus towards private companies, in anticipation of a wave of private equity divestments – a change from last year when the same proportion were eyeing more take-privates2.

Private Equity Exit Activity Begins to Thaw

The shift in focus to privately held opportunities coincides with a pick-up in private equity sales in the third quarter. The number of private equity exits globally in Q3 was 467, up 21.6% year-on-year, according to Preqin data cited by S&P Global. Europe was again at the forefront of activity with Dutch investment group Parcom Capital’s sale of chemicals company Univar for some $8bn3, the largest exit of the period.

While the geopolitical backdrop has become more uncertain, and many firms are taking a conservative and cautious approach, private equity sponsors are becoming more active in preparing companies for sale. We expect an increase in the number of assets coming to market in early 2024, should global conditions remain relatively unchanged.

Not all routes are seen as reliable, however. At a Financial Times event, EQT CEO Christian Sinding highlighted “dysfunction” in IPO markets and indicated that the firm was considering selling shares in companies directly among its 1,100 LPs4. The move could signal an evolution of the continuation fund model for larger sponsors with broad investor bases.

Pressure to Return Capital to Investors Continues to Rise

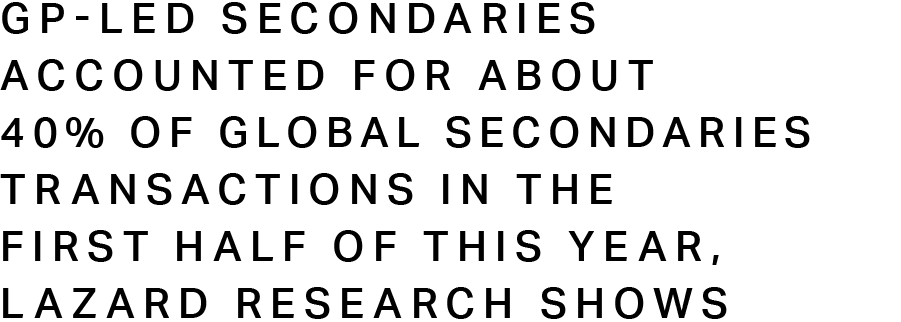

In a period of reduced exit activity, private equity firms have become more creative with solutions to return capital to investors. GP-led secondaries accounted for about 40% of global secondaries transactions in the first half of this year, Lazard research shows. Such deals have been important in providing liquidity from both single assets and portfolios. However, the disconnect between buyer and seller expectations has been weighing on the secondaries market just as it has on the primary deal market. Secondaries volume was down by some 28% over the period to $43bn5, although Lazard is forecasting a rebound in the second half as it expects valuation gaps to narrow.

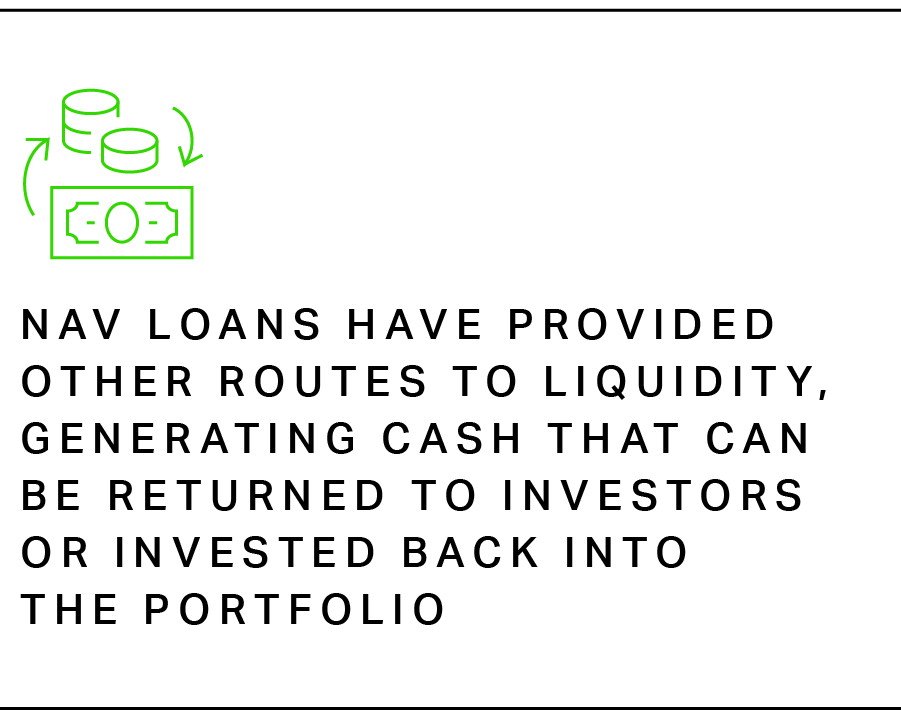

NAV loans have provided other routes to liquidity, generating cash that can be returned to investors or invested back into the portfolio. Such mechanisms are increasingly prevalent but can be expensive – with interest rates of 10%, and in some cases even higher6– and add to leverage levels across private equity structures.

Pressure to Return Capital to Investors Continues to Rise

In a period of reduced exit activity, private equity firms have become more creative with solutions to return capital to investors. GP-led secondaries accounted for about 40% of global secondaries transactions in the first half of this year, Lazard research shows. Such deals have been important in providing liquidity from both single assets and portfolios. However, the disconnect between buyer and seller expectations has been weighing on the secondaries market just as it has on the primary deal market. Secondaries volume was down by some 28% over the period to $43bn5, although Lazard is forecasting a rebound in the second half as it expects valuation gaps to narrow.

NAV loans have provided other routes to liquidity, generating cash that can be returned to investors or invested back into the portfolio. Such mechanisms are increasingly prevalent but can be expensive – with interest rates of 10%, and in some cases even higher6– and add to leverage levels across private equity structures.

A narrowing of the bid-ask spread, potentially facilitated by the peaking of interest rates and greater visibility over their medium-term outlook, could provide more of the certainty needed to unlock the exit market, thereby generating more substantial returns of capital to investors.

That activity would, in turn, help to stimulate the flow of capital back into new private equity funds via the fundraising market. The conditions have lengthened the time needed to raise capital but have not necessarily reduced appetite for leading funds. Earlier this year, EQT extended deadlines for its flagship fund, but its Q3 announcement stated it was now close to its €20bn target and homing in on its €21.5bn hard cap7. In line with the general improvement in private equity investment and exit activity, we see more firms preparing to bring new vehicles to market.

UK Politicians Court Private Equity to Support Long-Term Policy

Ahead of a UK general election, widely expected next year, politicians have begun courting private equity. Research from industry association Invest Europe shows that the European private equity industry had dry powder of €348bn at the end of 20228, providing substantial firepower that could support the transition to a greener economy. Senior officials from both the Conservative and Labour parties attended the BVCA Summit in London, with Labour’s Shadow Economic Secretary to the Treasury, Tulip Siddiq, acknowledging the potentially “very huge role” for private investment9.

Nonetheless, the political and regulatory backdrop could give rise to some changes for the industry. The UK’s financial watchdog, the FCA, announced in late September that it would be launching a review of private markets valuations10. At the same time, the status quo on taxation is also under threat, with the Labour Party leadership having already promised to end the carried interest tax advantage for private equity managers11. While the political climate shows some positive signs for private equity, it may not all be plain sailing.

UK Politicians Court Private Equity to Support Long-Term Policy

Ahead of a UK general election, widely expected next year, politicians have begun courting private equity. Research from industry association Invest Europe shows that the European private equity industry had dry powder of €348bn at the end of 20228, providing substantial firepower that could support the transition to a greener economy. Senior officials from both the Conservative and Labour parties attended the BVCA Summit in London, with Labour’s Shadow Economic Secretary to the Treasury, Tulip Siddiq, acknowledging the potentially “very huge role” for private investment9.

Nonetheless, the political and regulatory backdrop could give rise to some changes for the industry. The UK’s financial watchdog, the FCA, announced in late September that it would be launching a review of private markets valuations10. At the same time, the status quo on taxation is also under threat, with the Labour Party leadership having already promised to end the carried interest tax advantage for private equity managers11. While the political climate shows some positive signs for private equity, it may not all be plain sailing.