Private Equity

Market Snapshot

2024 Roundup

Private Equity Market Snapshot

2024 Roundup

With the biggest election year in history and peak interest rates behind us, 2024 didn’t deliver the market rebound some anticipated, but it has set the stage for a continued market recovery in 2025.

Overall, private equity activity in 2024 remained relatively subdued, with central banks holding interest rates high throughout H1. Nonetheless, deal activity in 2024 surpassed 2023 in both deal value and deal count. Two years of sluggish activity in Europe have led to increased pressures on fund managers to sell portfolio companies to generate liquidity and deploy capital in parallel to make new acquisitions1.

With the cost of borrowing continuing to fall with inflation and more political certainty in both the UK and the U.S., including following the first Budget of the Labour government, market participants appear to be overall more optimistic looking toward 2025.

Deal Activity Picked Up Year-on-Year

With central banks across Europe lowering interest rates in H2, and greater availability of debt financing, data showed signs of convergence between buyer and seller valuation expectations, resulting in increased dealmaking. The European private market saw respectable year-on-year growth in 2024, predicted to be 27.5% in terms of deal value and 11.5% in terms of deal count, according to data from Pitchbook, by year end2.

This was, at least to some degree, boosted by an increase in megadeals, with median deal size increasing 40% compared with 20233. Examples include Advent’s divestment of Evri to Apollo for €3.2Bn and the acquisition of Nord Anglia Education by an EQT-led consortium for $14.5Bn. The sectors driving much of this growth are IT and energy, specifically sustainable energy, infrastructure and software4. A number of high profile transactions have been recently announced in professional services – which continues to be a popular subsector – including Cinven’s significant strategic investment in Grant Thornton UK and the majority acquisition of Evelyn Partners by Apax.

However, despite increased activity, exit numbers remained subdued. The same data from Pitchbook predicts exits finishing roughly flat year-on-year, albeit down 34.3% compared to the highs of 2021. In the UK, exit value in H1 2024 was 71% lower than in H2 2023 and 8.8% lower than in H1 2023. In particular, H1 lacked large exits with almost half of total exits coming in under £25Mn. The public markets did not provide a popular alternative to the M&A track. While the new UK Listing Rules came into force in 2024, it is still too early to determine whether these will have any meaningful impact on the attractiveness of the UK as a listing venue, with concerns remaining around the depth of the liquidity pool.

There were beneficiaries of these market conditions. With a relatively modest number of exits and a hesitant IPO market, 2024 has seen a surge of secondaries market activity as investors sought alternative sources of liquidity. Data from Jefferies shows that global secondary deal volume (including both GP- and LP-led) was up 58% for H1 2024 against the same period last year at $68Bn5, and some investment banks are predicting a record-breaking year of $150Bn, beating the highs of 2021 at $132Bn6.

This was, at least to some degree, boosted by an increase in megadeals, with median deal size increasing 40% compared with 20233. Examples include Advent’s divestment of Evri to Apollo for €3.2Bn and the acquisition of Nord Anglia Education by an EQT-led consortium for $14.5Bn. The sectors driving much of this growth are IT and energy, specifically sustainable energy, infrastructure and software4. A number of high profile transactions have been recently announced in professional services – which continues to be a popular subsector – including Cinven’s significant strategic investment in Grant Thornton UK and the majority acquisition of Evelyn Partners by Apax.

However, despite increased activity, exit numbers remained subdued. The same data from Pitchbook predicts exits finishing roughly flat year-on-year, albeit down 34.3% compared to the highs of 2021. In the UK, exit value in H1 2024 was 71% lower than in H2 2023 and 8.8% lower than in H1 2023. In particular, H1 lacked large exits with almost half of total exits coming in under £25Mn. The public markets did not provide a popular alternative to the M&A track. While the new UK Listing Rules came into force in 2024, it is still too early to determine whether these will have any meaningful impact on the attractiveness of the UK as a listing venue, with concerns remaining around the depth of the liquidity pool.

There were beneficiaries of these market conditions. With a relatively modest number of exits and a hesitant IPO market, 2024 has seen a surge of secondaries market activity as investors sought alternative sources of liquidity. Data from Jefferies shows that global secondary deal volume (including both GP- and LP-led) was up 58% for H1 2024 against the same period last year at $68Bn5 ,and some investment banks are predicting a record-breaking year of $150Bn, beating the highs of 2021 at $132Bn6.

Notable Trends in the Mid-Market

One notable sector, both in terms of deal activity and fundraising, was the mid-market. Real Deals data for Q3 2024 showed an increase in deals valued between €50Mn and €150Mn by 9.5% to 138, with value rising by 16.5% to €11.9Bn. Similarly, deals valued between €150Mn and €250Mn for the same quarter also grew by 9.5% to 23, with value rising by more than 14% to €4.4Bn7.

In the UK, mid-market private equity investment activity also outperformed the overall UK private equity market. Data from KPMG showed the number of mid-market deals declined in H1 2024 compared to H1 2023 by only 11% to 321, compared to the overall market which declined 20% to 656 for the same period8.

Limited partners have also started to favour mid-market strategies9. According to data from Rede Partners for H1 2024, 57% of LPs (up 15% from H1 2023) plan to allocate more capital to the lower mid-market and 42% (up 4% from H1 2023) are seeking greater exposure to mid-market funds10. With more value creation and less leverage, the mid-market is often perceived as offering potential for stronger returns independent of prevailing interest rates and macro-economic conditions. Another driver for investors’ interest in the mid-market may also be diversification of their portfolios and investors being attracted to GPs with sector specialisations.

In response, we are also seeing larger, global firms looking to implement mid-market investment strategies. In September, KKR announced that it had closed its $4.6Bn Ascendant Fund, its first investment vehicle solely focussed on mid-market businesses in North America11. Similarly, Cinven and Advent International have each announced plans to set up mid-market investment strategies, with the former focusing on deals valued between £200Mn to £600Mn in the UK, Germany and Spain and the latter on global deals valued between $50Mn and $200Mn.

Notable Trends in the Mid-market

One notable sector, both in terms of deal activity and fundraising, was the mid-market. Real Deals data for Q3 2024 showed an increase in deals valued between €50Mn and €150Mn by 9.5% to 138, with value rising by 16.5% to €11.9Bn. Similarly, deals valued between €150Mn and €250Mn for the same quarter also grew by 9.5% to 23, with value rising by more than 14% to €4.4Bn.7

In the UK, mid-market private equity investment activity also outperformed the overall UK private equity market. Data from KPMG showed the number of mid-market deals declined in H1 2024 compared to H1 2023 by only 11% to 321, compared to the overall market which declined 20% to 656 for the same period8.

Limited partners have also started to favour mid-market strategies9. According to data from Rede Partners for H1 2024, 57% of LPs (up 15% from H1 2023) plan to allocate more capital to the lower mid-market and 42% (up 4% from H1 2023) are seeking greater exposure to mid-market funds10. With more value creation and less leverage, the mid-market is often perceived as offering potential for stronger returns independent of prevailing interest rates and macro-economic conditions. Another driver for investors’ interest in the mid-market may also be diversification of their portfolios and investors being attracted to GPs with sector specialisations.

In response, we are also seeing larger, global firms looking to implement mid-market investment strategies. In September, KKR announced that it had closed its $4.6Bn Ascendant Fund, its first investment vehicle solely focussed on mid-market businesses in North America11. Similarly, Cinven and Advent International have each announced plans to set up mid-market investment strategies, with the former focusing on deals valued between £200Mn to £600Mn in the UK, Germany and Spain and the latter on global deals valued between $50Mn and $200Mn.

Increase in Take-private Transactions

Despite a relatively lukewarm market, 2024 is on track to see a modest increase in sponsor-led take-private transactions in the U.S. and Europe, with 72 deals announced having a value of $132Bn as at the end of Q3 (compared with 97 deals announced having a value of $153Bn in 2023)12.

While the UK accounted for nearly half of European take-private deal activity in H1 2024 (eight deals with a total value of £8.2 billion)13, the number of private equity-backed bids in the UK actually decreased in that period to 43% of all firm offers announced (compared to 56% in H1 2023)14. This reflected the more significant role played by strategic buyers in 2024 who were able to utilise cash-heavy balance sheets and the ability to offer share consideration, in the face of targets’ value expectations due to high financing costs.

2024 has so far seen 13 private equity-led firm offers announced in the UK worth a combined £16.2 billion. Several of these (including, Darktrace, Hipgnosis Songs and IQGeo Group) were made by U.S. private equity firms, which have continued to explore take-private transactions in Europe due to more favourable macro-economic conditions and lower valuations. These factors are also contributing to a de-listing trend in London – 48 firm takeover offers were made in 2024 (down slightly from 50 in 2023) compared to 13 IPOs (down from 19 in 2023), resulting in one of the quietest years for listings in over a decade. In addition, the number of listed companies on London’s junior market, AIM, is now barely over 700, its lowest level in 20 years15. This continued trend throughout 2024 demonstrates the attractiveness of London-listed assets for take-private transactions.

Increase in Take-private Transactions

Despite a relatively lukewarm market, 2024 is on track to see a modest increase in sponsor-led take-private transactions in the U.S. and Europe, with 72 deals announced having a value of $132Bn as at the end of Q3 (compared with 97 deals announced having a value of $153Bn in 2023)12.

While the UK accounted for nearly half of European take-private deal activity in H1 2024 (eight deals with a total value of £8.2 billion)13, the number of private equity-backed bids in the UK actually decreased in that period to 43% of all firm offers announced (compared to 56% in H1 2023)14. This reflected the more significant role played by strategic buyers in 2024 who were able to utilise cash-heavy balance sheets and the ability to offer share consideration, in the face of targets’ value expectations due to high financing costs.

2024 has so far seen 13 private equity-led firm offers announced in the UK worth a combined £16.2 billion. Several of these (including, Darktrace, Hipgnosis Songs and IQGeo Group) were made by U.S. private equity firms, which have continued to explore take-private transactions in Europe due to more favourable macro-economic conditions and lower valuations. These factors are also contributing to a de-listing trend in London – 48 firm takeover offers were made in 2024 (down slightly from 50 in 2023) compared to 13 IPOs (down from 19 in 2023), resulting in one of the quietest years for listings in over a decade. In addition, the number of listed companies on London’s junior market, AIM, is now barely over 700, its lowest level in 20 years15 . This continued trend throughout 2024 demonstrates the attractiveness of London-listed assets for take-private transactions.

UK Budget

Various UK tax announcements made this year will affect private equity sponsors and investment professionals. Two key items are changes to the carried interest regime and abolition of the non-dom regime.

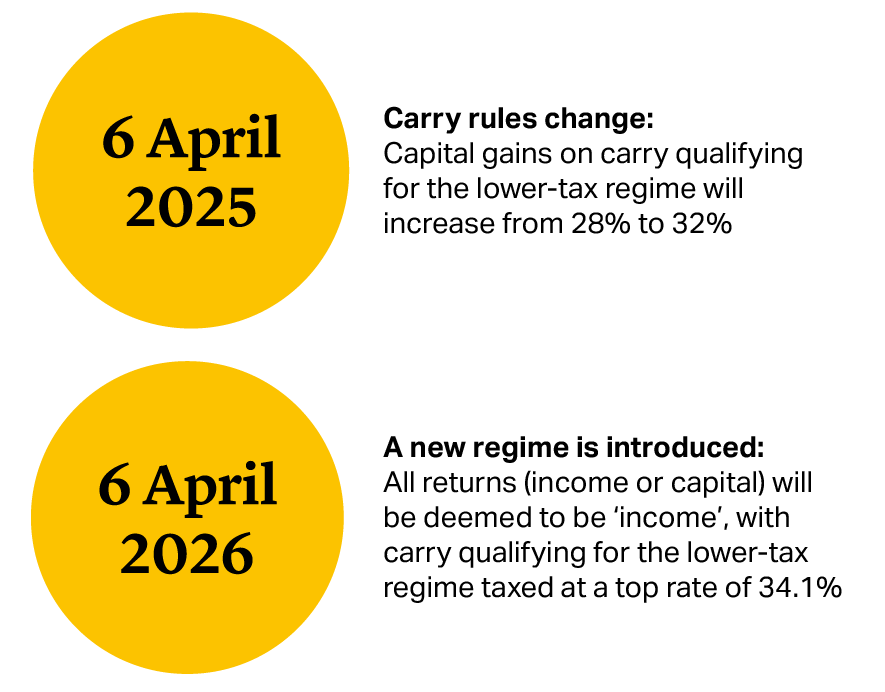

From 6 April 2025 to 5 April 2026, the only change to the carry rules is that the rate of tax applicable to the capital gains component of carry qualifying for the lower-tax regime will be increased from 28% to 32%. However, from 6 April 2026, a new regime will be introduced under which all returns (income or capital) will be deemed to be income, with carry qualifying for the lower-tax regime taxed at a top rate of just under 34.1%. This means that investment professionals who receive qualifying carried interest weighted towards capital gains will in many cases be subject to a higher effective rate of tax than currently. On the other hand, investment professionals receiving qualifying carried interest weighted towards other kinds of returns (such as dividends and interest) may find that their effective tax rate is reduced.

UK Budget

Various UK tax announcements made this year will affect private equity sponsors and investment professionals. Two key items are changes to the carried interest regime and abolition of the non-dom regime.

From 6 April 2025 to 5 April 2026, the only change to the carry rules is that the rate of tax applicable to the capital gains component of carry qualifying for the lower-tax regime will be increased from 28% to 32%. However, from 6 April 2026, a new regime will be introduced under which all returns (income or capital) will be deemed to be income, with carry qualifying for the lower-tax regime taxed at a top rate of just under 34.1%. This means that investment professionals who receive qualifying carried interest weighted towards capital gains will in many cases be subject to a higher effective rate of tax than currently. On the other hand, investment professionals receiving qualifying carried interest weighted towards other kinds of returns (such as dividends and interest) may find that their effective tax rate is reduced.

Two new conditions in order to qualify for the 34.1% tax rate are being considered: a minimum co-investment requirement and a minimum holding period for the carried interest. These are subject to ongoing consultation, as are other details, including ways to address the impact of repealing automatic access for employees (as opposed to LLP members) to the lower-tax regime. The repeal of the rule for employees may be of particular relevant to credit funds if they have struggled with the current qualifying conditions. It is possible that some relaxation of those qualifying conditions will be made available for such funds so long as they are engaged in what HMRC considers to be long term investment activity. Our tax team will be part of the working group engaged with HMRC in the ongoing consultation.

Note that existing structures will not be excluded from the new regime, but transitional rules may be considered for the potential new qualifying conditions.

While the new carried interest regime appears less far reaching than some had feared, sponsors should plan for administrative changes and a potential need to introduce structural changes to their carry arrangements.

The abolition of the non-dom regime will take effect from 6 April 2025. From that date, all UK residents will be subject to tax on their worldwide income and gains, irrespective of remittance to the UK, subject to an exemption for individuals within their first four years of residence who will not be subject to tax on eligible foreign income and gains (FIG). Former remittance basis users will continue to pay tax on FIG arising before 6 April 2025 when remitted to the UK, subject to a lower rate of tax if such amounts are designated as taxable under a temporary repatriation facility before 5 April 2028. There will also be the possibility of rebasing certain non-UK capital assets to their value as at 5 April 2017.

Two new conditions in order to qualify for the 34.1% tax rate are being considered: a minimum co-investment requirement and a minimum holding period for the carried interest. These are subject to ongoing consultation, as are other details, including ways to address the impact of repealing automatic access for employees (as opposed to LLP members) to the lower-tax regime. The repeal of the rule for employees may be of particular relevant to credit funds if they have struggled with the current qualifying conditions. It is possible that some relaxation of those qualifying conditions will be made available for such funds so long as they are engaged in what HMRC considers to be long term investment activity. Our tax team will be part of the working group engaged with HMRC in the ongoing consultation.

Note that existing structures will not be excluded from the new regime, but transitional rules may be considered for the potential new qualifying conditions.

While the new carried interest regime appears less far reaching than some had feared, sponsors should plan for administrative changes and a potential need to introduce structural changes to their carry arrangements.

The abolition of the non-dom regime will take effect from 6 April 2025. From that date, all UK residents will be subject to tax on their worldwide income and gains, irrespective of remittance to the UK, subject to an exemption for individuals within their first four years of residence who will not be subject to tax on eligible foreign income and gains (FIG). Former remittance basis users will continue to pay tax on FIG arising before 6 April 2025 when remitted to the UK, subject to a lower rate of tax if such amounts are designated as taxable under a temporary repatriation facility before 5 April 2028. There will also be the possibility of rebasing certain non-UK capital assets to their value as at 5 April 2017.

Looking Ahead

While 2024 has continued the trend of subdued deal activity, there are reasons to be cautiously optimistic looking toward 2025.

Continued easing of macroeconomic conditions along with increasing political certainty, particularly in developed markets, suggest favourable dealmaking conditions are ahead. Moreover, equity capital markets regulatory reform and the backlog of maturing PE-owned investments16 may drive increased activity for IPOs in 2025 – dealmakers will be closely watching SHEIN’s potential London listing, which would provide a welcome boost. An increase in IPOs would generate more transaction activity as sponsor’s look to both deploy dry powder accumulated over the last several years and return capital to investors.

There is also plenty to get excited about as advancements in AI continue to provide attractive targets in the technology sector, and the PE industry continues to innovate new strategies to deliver value for investors.

This article was prepared with contributions from Cleary associates Thomas Peet and James Soussa.

Looking Ahead

While 2024 has continued the trend of subdued deal activity, there are reasons to be cautiously optimistic looking toward 2025.

Continued easing of macroeconomic conditions along with increasing political certainty, particularly in developed markets, suggest favourable dealmaking conditions are ahead. Moreover, equity capital markets regulatory reform and the backlog of maturing PE-owned investments16 may drive increased activity for IPOs in 2025 – dealmakers will be closely watching SHEIN’s potential London listing, which would provide a welcome boost. An increase in IPOs would generate more transaction activity as sponsor’s look to both deploy dry powder accumulated over the last several years and return capital to investors.

There is also plenty to get excited about as advancements in AI continue to provide attractive targets in the technology sector, and the PE industry continues to innovate new strategies to deliver value for investors.

This article was prepared with contributions from Cleary associates Thomas Peet and James Soussa.