At the time of writing, Europe has plenty of gas in storage, demand remains muted and Liquified Natural Gas (LNG) supplies look healthy. After soaring following Russia’s invasion of Ukraine, energy prices have come down, sitting lower than in June 2022 and only a fraction of the record highs seen in August of the same year.

Yet, volatility remains. The front-month TTF benchmark contract1 rose from about €23/MWh in early June to over €41/MWh by the middle of the month2. Production outages in Norway, the imminent closure of the Groningen gas field in the Netherlands, which is expected in October this year, as well as energy demand for cooling amid warm weather this summer have lent support to prices.

This is a reminder that Europe is not out of the woods yet.

At the time of writing, Europe has plenty of gas in storage, demand remains muted and Liquified Natural Gas (LNG) supplies look healthy. After soaring following Russia’s invasion of Ukraine, energy prices have come down, sitting lower than in June 2022 and only a fraction of the record highs seen in August of the same year.

Yet, volatility remains. The front-month TTF benchmark contract1 rose from about €23/MWh in early June to over €41/MWh by the middle of the month2. Production outages in Norway, the imminent closure of the Groningen gas field in the Netherlands, which is expected in October this year, as well as energy demand for cooling amid warm weather this summer have lent support to prices.

This is a reminder that Europe is not out of the woods yet.

Energy Levels Improved

Gas storage levels in Europe are looking much healthier than in 2022. Transparency data from Gas Infrastructure Europe (GIE) shows storage tanks are on average about 76% full, compared with 57% this time last year3. A high penetration of renewables is also contributing to a reduction in demand for gas, thus enabling market players to put more gas into storage. In May 2023, renewables had a bigger share than fossil fuels in the electricity mix for the first time on record, according to data from think tank Ember4. Hydro power levels have also improved across much of Europe after the drought seen last year5.

However, question marks hang over the availability of energy from other sources. France’s nuclear fleet, for instance, faced challenges last year when several reactors were taken offline owing to stress corrosion. For this winter, its production capacities are expected to be five to ten gigawatts higher than last year, but will still be far away from its installed capacity. The possibility of a ‘perfect storm’ this coming winter of still low nuclear output in France, cold weather across Europe and surging demand for LNG in China, as its economy recovers, could be a big test for security of supply.

A report published by the Agency for the Cooperation of Energy Regulators (ACER) on 27 June noted that European gas prices were approaching pre-crisis levels, but cautioned that “supply is overall still tight, exposing prices to unexpected developments.” Meanwhile, it suggested that “China’s LNG demand remains an important factor for EU gas prices going forward6.”

Energy Levels Improved

Gas storage levels in Europe are looking much healthier than in 2022. Transparency data from Gas Infrastructure Europe (GIE) shows storage tanks are on average about 76% full, compared with 57% this time last year3. A high penetration of renewables is also contributing to a reduction in demand for gas, thus enabling market players to put more gas into storage. In May 2023, renewables had a bigger share than fossil fuels in the electricity mix for the first time on record, according to data from think tank Ember4. Hydro power levels have also improved across much of Europe after the drought seen last year5.

However, question marks hang over the availability of energy from other sources. France’s nuclear fleet, for instance, faced challenges last year when several reactors were taken offline owing to stress corrosion. For this winter, its production capacities are expected to be five to ten gigawatts higher than last year, but will still be far away from its installed capacity. The possibility of a ‘perfect storm’ this coming winter of still low nuclear output in France, cold weather across Europe and surging demand for LNG in China, as its economy recovers, could be a big test for security of supply.

A report published by the Agency for the Cooperation of Energy Regulators (ACER) on 27 June noted that European gas prices were approaching pre-crisis levels, but cautioned that “supply is overall still tight, exposing prices to unexpected developments.” Meanwhile, it suggested that “China’s LNG demand remains an important factor for EU gas prices going forward6.”

Renewables Growth

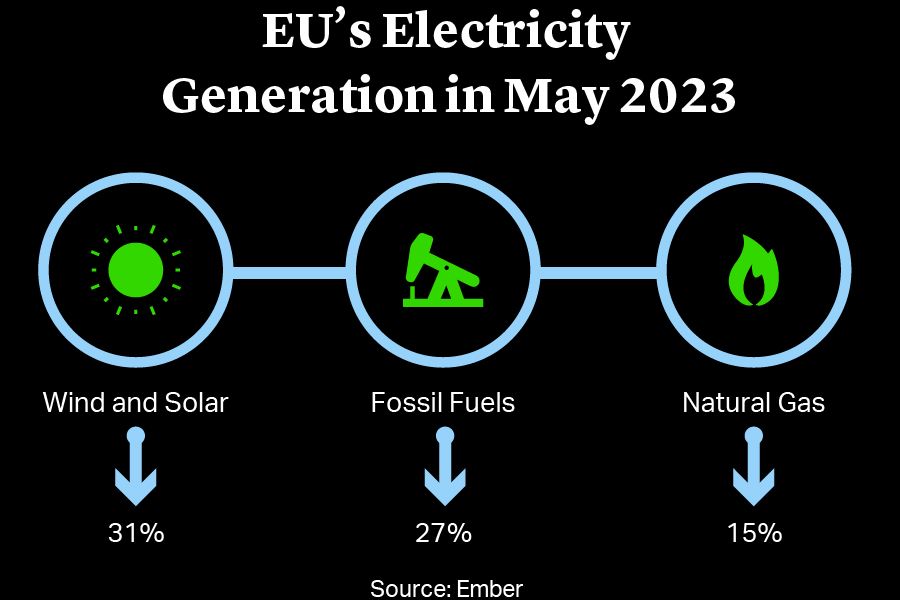

At the EU level, policy initiatives are focusing on making energy markets more resilient to extreme shocks following Russia’s invasion of Ukraine. The expansion of renewable energy is a key priority in this context; more electricity generation from solar and wind can lessen Europe’s dependence on gas imports. Almost a third of the EU’s electricity in May was generated from wind and solar, while fossil fuels generated a record low of 27%7. Natural gas recorded the lowest share of generation since 2018 at just 15% of EU electricity during May.

Renewables Growth

At the EU level, policy initiatives are focusing on making energy markets more resilient to extreme shocks following Russia’s invasion of Ukraine. The expansion of renewable energy is a key priority in this context; more electricity generation from solar and wind can lessen Europe’s dependence on gas imports. Almost a third of the EU’s electricity in May was generated from wind and solar, while fossil fuels generated a record low of 27%7. Natural gas recorded the lowest share of generation since 2018 at just 15% of EU electricity during May.

As for further ambition, the EU is close to agreeing a revised Renewable Energy Directive (RED III) which includes a 42.5% renewables target in final energy consumption by 2030, up from the current 32% target. By comparison, in 2021, about 22% of final energy consumption was from renewables8.

RED III also aims to tackle permitting, which remains a hurdle particularly for onshore wind. In Europe, at least 59 gigawatts of onshore wind capacity — four times the capacity commissioned in 2022 — is held up in various permitting procedures, according to the International Energy Agency (IEA)9. As for offshore wind, growth is still limited in many countries while solar PV installations — particularly small-scale residential and commercial units — are growing rapidly across Europe.

More renewables will help boost energy security in Europe, but it can fall short during those dark winter months when there is little generation from solar and wind sources. Natural gas — a storable fuel with much lower CO2 emissions than coal — will be needed to fill in the supply gaps for many years to come.

The EU Treaty leaves it up to Member States to decide on their own energy mix as long as climate targets — including a 55% cut in greenhouse gas (GHG) emissions by 2030 — are reached. This means EU nations are moving in different directions; Germany has phased out nuclear power whereas France plans to commission a new generation of reactors from the mid-2030s. Hungary is expanding its nuclear power fleet with Paks II and is deploying Russian technology supplied by Rosatom. Nuclear power is a sticking point in EU negotiations, for example concerning the aforementioned RED III where France has been pushing for more recognition of nuclear as a low-carbon energy source and has rallied a dozen like-minded Member States on the role of nuclear power in the EU’s future energy mix10.

As for further ambition, the EU is close to agreeing a revised Renewable Energy Directive (RED III) which includes a 42.5% renewables target in final energy consumption by 2030, up from the current 32% target. By comparison, in 2021, about 22% of final energy consumption was from renewables8.

RED III also aims to tackle permitting, which remains a hurdle particularly for onshore wind. In Europe, at least 59 gigawatts of onshore wind capacity — four times the capacity commissioned in 2022 — is held up in various permitting procedures, according to the International Energy Agency (IEA)9. As for offshore wind, growth is still limited in many countries while solar PV installations — particularly small-scale residential and commercial units — are growing rapidly across Europe.

More renewables will help boost energy security in Europe, but it can fall short during those dark winter months when there is little generation from solar and wind sources. Natural gas — a storable fuel with much lower CO2 emissions than coal — will be needed to fill in the supply gaps for many years to come.

The EU Treaty leaves it up to Member States to decide on their own energy mix as long as climate targets — including a 55% cut in greenhouse gas (GHG) emissions by 2030 — are reached. This means EU nations are moving in different directions; Germany has phased out nuclear power whereas France plans to commission a new generation of reactors from the mid-2030s. Hungary is expanding its nuclear power fleet with Paks II and is deploying Russian technology supplied by Rosatom. Nuclear power is a sticking point in EU negotiations, for example concerning the aforementioned RED III where France has been pushing for more recognition of nuclear as a low-carbon energy source and has rallied a dozen like-minded Member States on the role of nuclear power in the EU’s future energy mix10.

Market Intervention and Joint Action

Despite these challenges, the energy crisis has prompted more collaboration across borders. This is exemplified by joint purchasing of gas through the EU Energy Platform which will give smaller Member States and SMEs better access to LNG, perhaps at more affordable prices. The volumes purchased through this platform are relatively small and will have a limited impact on the overall supply picture, but interest from buyers and sellers has so far exceeded expectations.

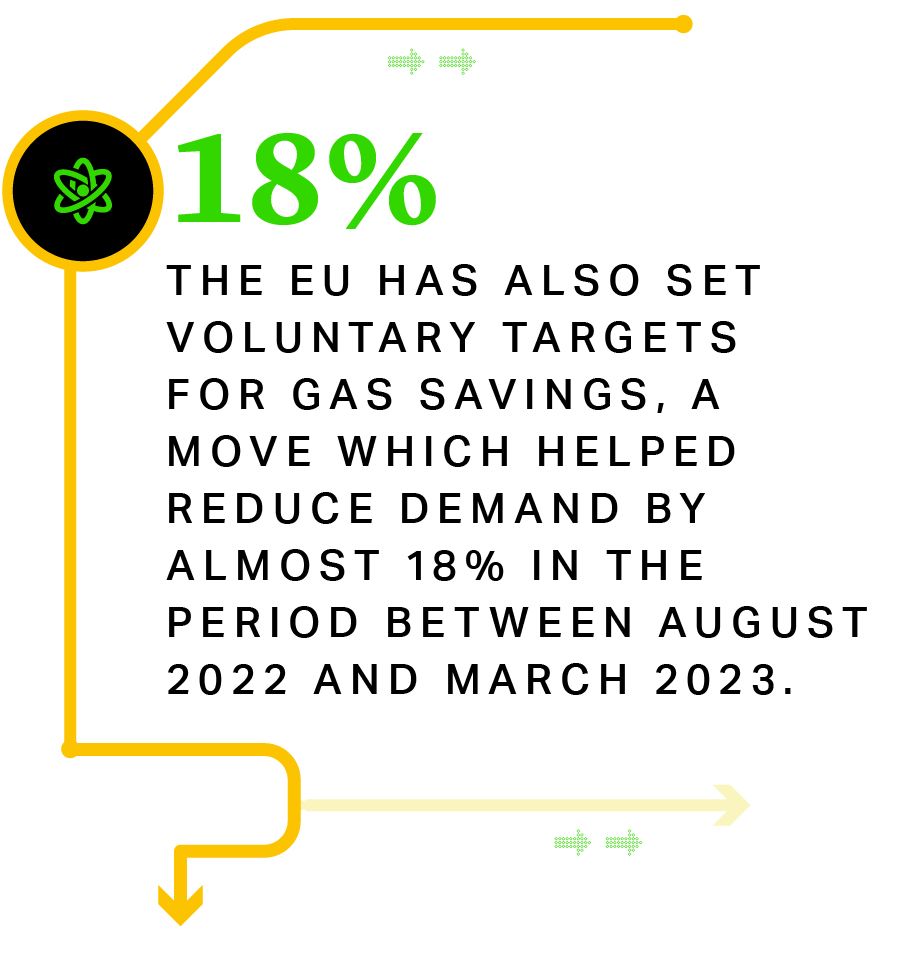

The EU has also set voluntary targets for gas savings, a move which helped reduce demand by almost 18% in the period between August 2022 and March 2023, compared with previous years11. Other temporary interventions at the EU level include a €180/MWh price cap on TTF gas imports, albeit under a number of conditions, and the obligation for storage tanks to be 90% full by 1 November this year. Moreover, the European Commission (EC) is negotiating with banks to secure insurance for companies wishing to store gas in Ukraine, which boasts about 31 billion cubic meters of underground storage capacity. The European Investment Bank (EIB), however, says it will not get involved as it is no longer lending to fossil fuel projects.

Market Intervention and Joint Action

Despite these challenges, the energy crisis has prompted more collaboration across borders. This is exemplified by joint purchasing of gas through the EU Energy Platform which will give smaller Member States and SMEs better access to LNG, perhaps at more affordable prices. The volumes purchased through this platform are relatively small and will have a limited impact on the overall supply picture, but interest from buyers and sellers has so far exceeded expectations.

The EU has also set voluntary targets for gas savings, a move which helped reduce demand by almost 18% in the period between August 2022 and March 2023, compared with previous years11. Other temporary interventions at the EU level include a €180/MWh price cap on TTF gas imports, albeit under a number of conditions, and the obligation for storage tanks to be 90% full by 1 November this year. Moreover, the European Commission (EC) is negotiating with banks to secure insurance for companies wishing to store gas in Ukraine, which boasts about 31 billion cubic meters of underground storage capacity. The European Investment Bank (EIB), however, says it will not get involved as it is no longer lending to fossil fuel projects.

Managing Volatility Amid the Energy Transition

Russia has reduced pipeline gas supplies to Europe drastically since invading Ukraine in February 2022. By Q4 last year, the EU’s Russian pipeline gas imports had fallen by almost 90% year-on-year, according to the EC12. However, though the EU has banned imports of Russian oil and coal, these sanctions do not cover Russian gas. Some Member States are still importing considerable volumes of Russian LNG, including France, Spain and Belgium. Moreover, Hungary has signed new deals with Gazprom for piped gas supply.

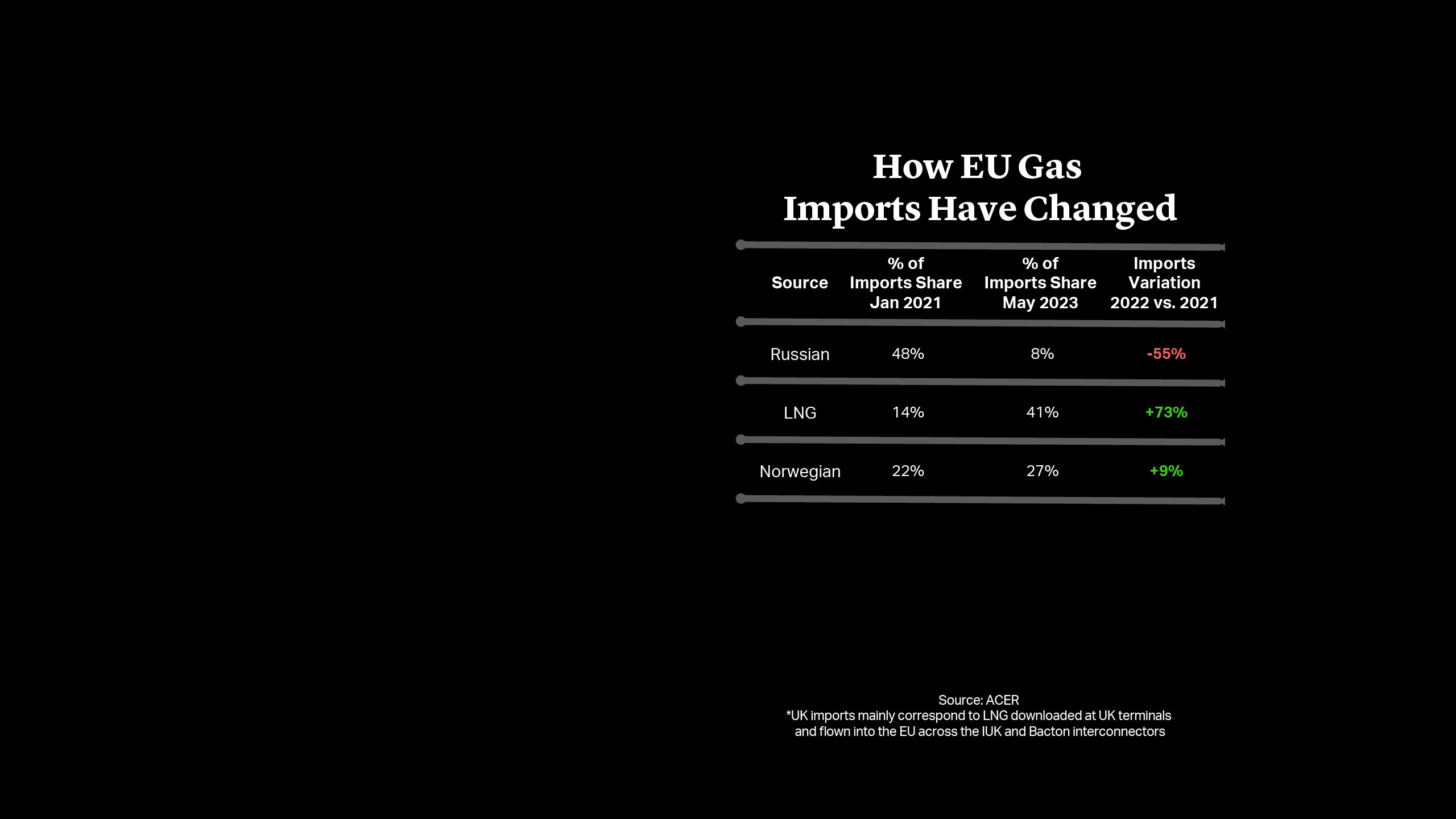

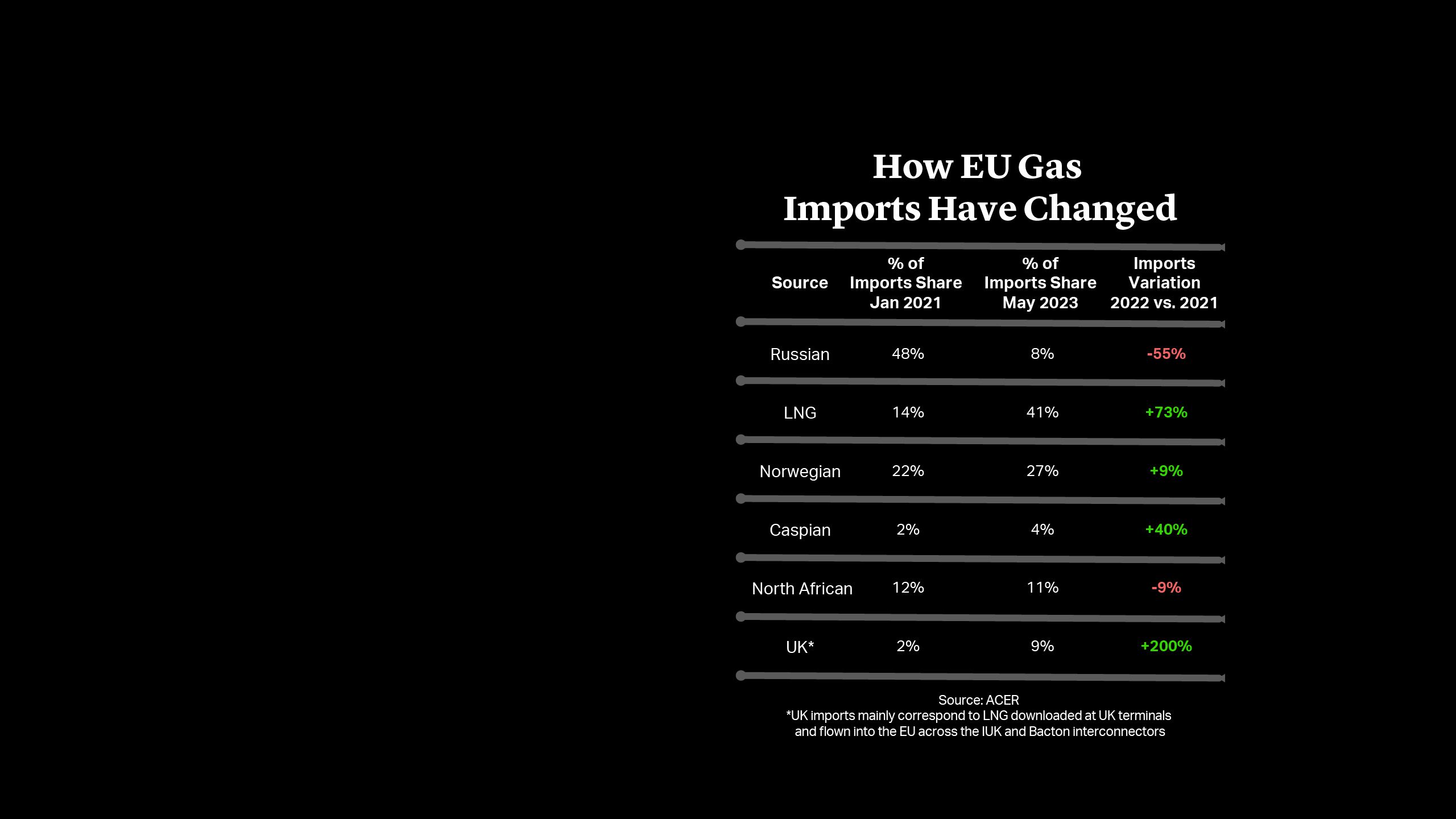

Nevertheless, even if Russia were to halt supplies to the EU completely, the bloc now looks much better prepared for winter 2023/24 than a few months ago. As of May 2023, the share of Russian gas in EU imports was only 8%, while LNG had a share of 41% and Norwegian pipeline gas a share of 27%, according to ACER13.

Yet, concerns over gas shortages will not go away anytime soon. While a relatively mild winter in 2022/23 has helped to improve the supply-demand balance, global competition for LNG deliveries is expected to intensify in the coming years. This is despite more liquefaction projects coming onstream, for example in the U.S. and Qatar.

The EU has demonstrated that it can respond to energy shocks and extreme price volatility. However, plenty of work remains to be done to boost energy security in the longer term while putting the bloc on a trajectory to reach the 55% CO2 reduction target by 2030, as stipulated in the Fit for 55 package. This will require massive investment in the bloc’s electrification and real shift away from fossil fuel combustion. With preliminary data from Eurostat suggesting carbon dioxide emissions in the EU fell by 2.8% in 2022, the reduction in gas consumption could already be contributing towards that effort14.

Managing Volatility Amid the Energy Transition

Russia has reduced pipeline gas supplies to Europe drastically since invading Ukraine in February 2022. By Q4 last year, the EU’s Russian pipeline gas imports had fallen by almost 90% year-on-year, according to the EC12. However, though the EU has banned imports of Russian oil and coal, these sanctions do not cover Russian gas. Some Member States are still importing considerable volumes of Russian LNG, including France, Spain and Belgium. Moreover, Hungary has signed new deals with Gazprom for piped gas supply.

Nevertheless, even if Russia were to halt supplies to the EU completely, the bloc now looks much better prepared for winter 2023/24 than a few months ago. As of May 2023, the share of Russian gas in EU imports was only 8%, while LNG had a share of 41% and Norwegian pipeline gas a share of 27%, according to ACER13.

Yet, concerns over gas shortages will not go away anytime soon. While a relatively mild winter in 2022/23 has helped to improve the supply-demand balance, global competition for LNG deliveries is expected to intensify in the coming years. This is despite more liquefaction projects coming onstream, for example in the U.S. and Qatar.

The EU has demonstrated that it can respond to energy shocks and extreme price volatility. However, plenty of work remains to be done to boost energy security in the longer term while putting the bloc on a trajectory to reach the 55% CO2 reduction target by 2030, as stipulated in the Fit for 55 package. This will require massive investment in the bloc’s electrification and real shift away from fossil fuel combustion. With preliminary data from Eurostat suggesting carbon dioxide emissions in the EU fell by 2.8% in 2022, the reduction in gas consumption could already be contributing towards that effort14.

For more information on anything from the green transition to the state of European energy supplies, click the link to visit our EU Energy Resource Center:

Marco D’Ostuni

Partner

Rome

T: +39 06 6952 2610

mdostuni@cgsh.com

V-Card

François‑Charles Laprévote

Partner

Brussels

T: +32 22872184

fclaprevote@cgsh.com

V-Card

Christophe Wauters

Counsel

Brussels

T: +32 22872198

chwauters@cgsh.com

V-Card

Alessandro Camino

Associate

Milan

T: +39 02 7260 8264

acomino@cgsh.com

V-Card

Cristina Dionisio

Associate

Milan

T: +39 02 7260 8238

cdionisio@cgsh.com

V-Card