Authorities beyond the European Union – including, perhaps surprisingly, authorities in certain European member states – are considering their own digital regulation initiatives. While these initiatives are generally less advanced than the EU’s efforts, they may come to have a significant impact on how digital markets operate in these jurisdictions. 2023 will refine our understanding of these efforts and of when they may come into force.

European Member States

In a context where the Digital Markets Act (DMA) is enacted under the aegis of harmonizing how European enforcers approach digital contestability concerns, one would expect there to be less-and-less to say about initiatives at the member state level. But a key thematic for 2023 will be how EU and national enforcers will reconcile what currently appear to be potentially diverging enforcement activities. Olivier Guersent, the Director General of DG Competition, speaking on Cleary Gottlieb’s Antitrust Review podcast last year1, reflected that the enactment of the DMA will mean a “completely new way of cooperating within the European competition network.” 2023 will begin to reveal how this cooperation will work in practice.

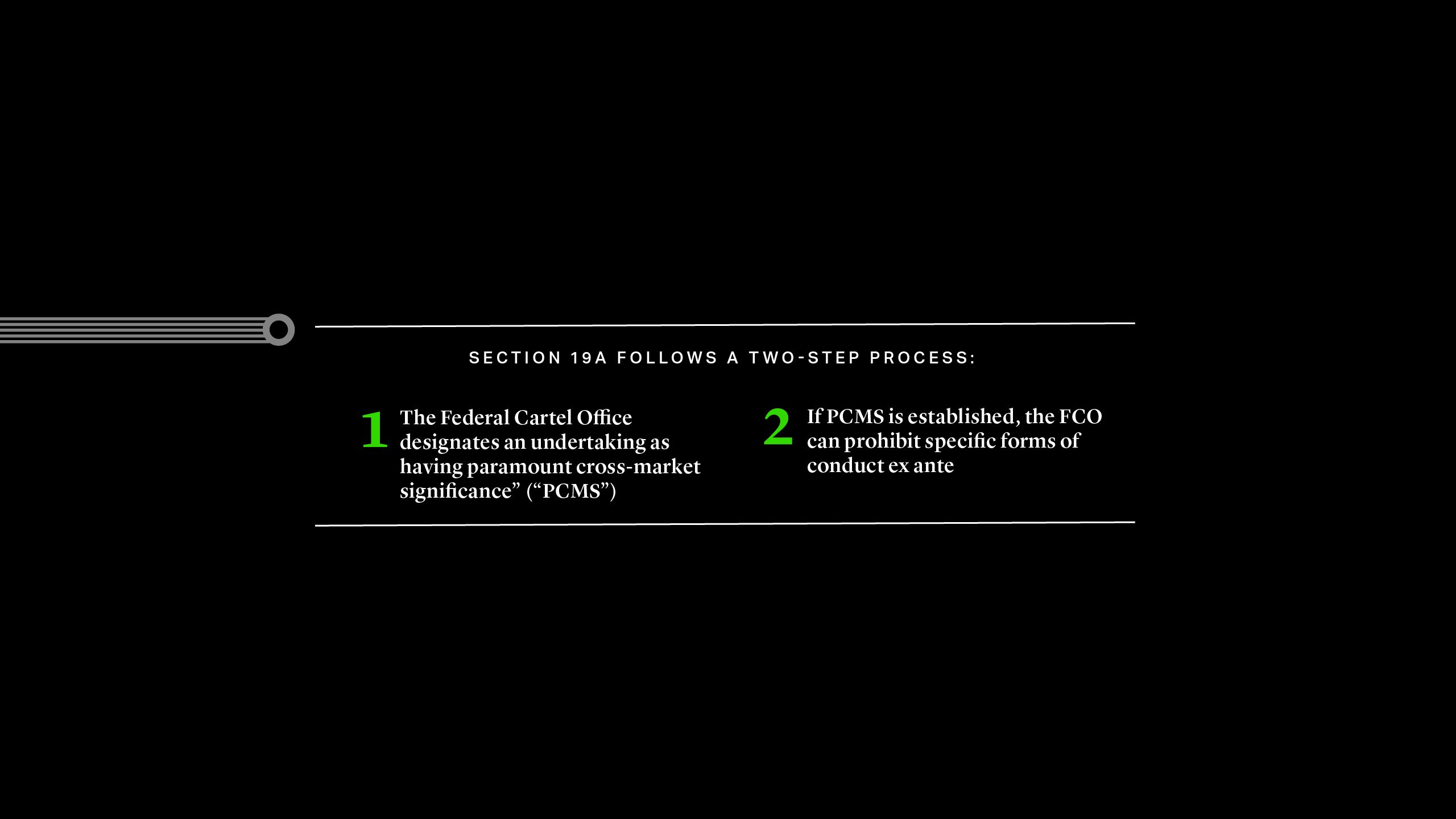

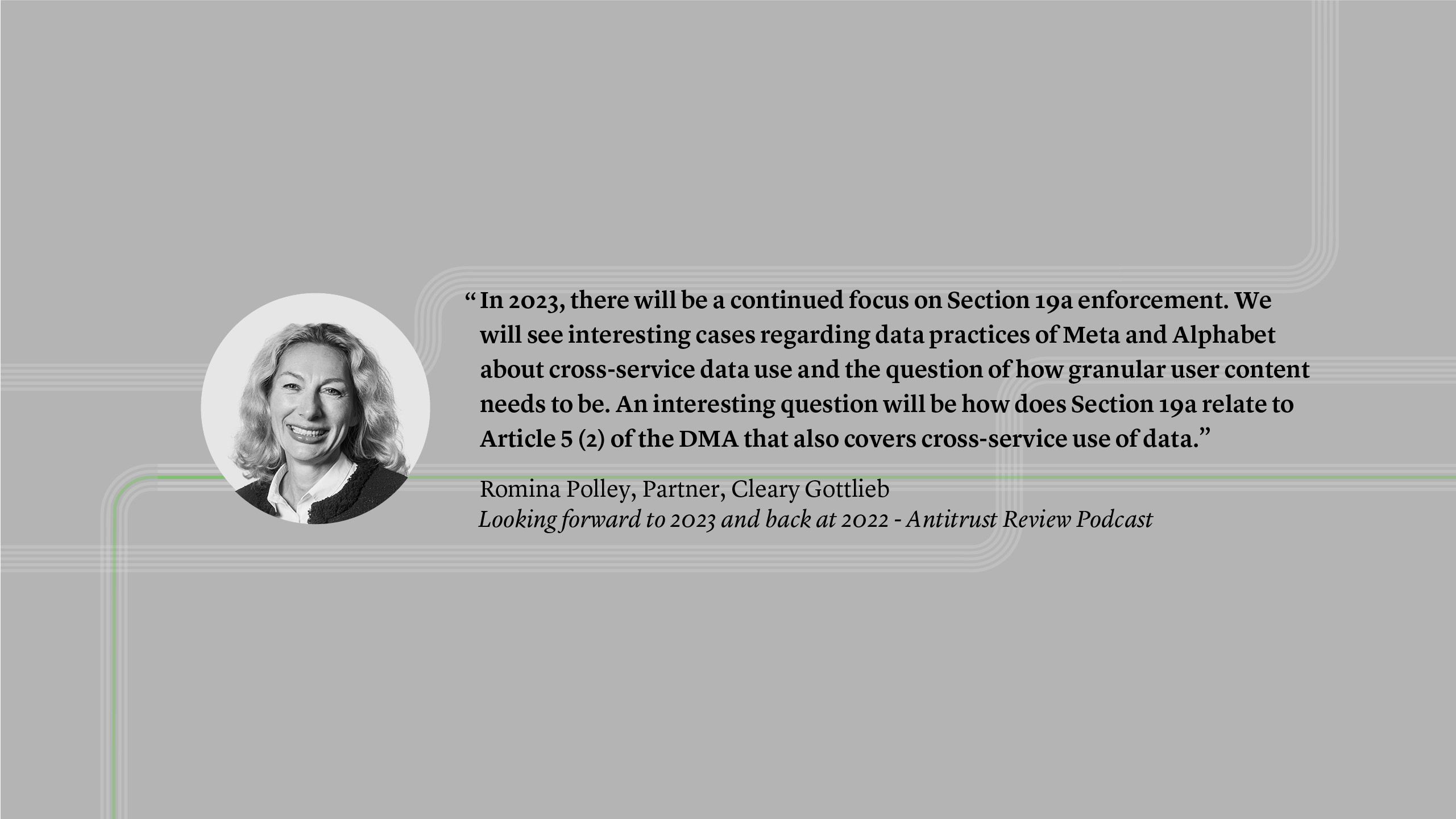

The key test case will be Germany’s approach to enforcing its relatively new “Section 19a ARC” regulation, which covers the same ground as the DMA and pursues the same contestability objectives. As we explain in more detail in our Handbook2, this rule enables the Federal Cartel Office (“FCO”) to intervene in digital markets without establishing anticompetitive effects based on a two-step process:

This approach is similar to the DMA’s approach of identifying gatekeepers that are then prohibited from certain forms of conduct. The FCO has opened a range of cases under this new regime, targeting Meta, Amazon, Google; often based on allegations that mirror the specific requirements under the DMA. Apple and Microsoft are expected to see similar cases this year.

In other member states – notably in France and Italy – enforcers have continued to bring antitrust actions in digital cases relating to concepts such as usage of rival data and data access; both thematics that are addressed by the DMA under Articles 6(2) and 6(10).

As with the European Commission’s own antitrust enforcement cases, these national cases may see the early application of the DMA’s rules. However, were national enforcers to resolve these matters based on their own priorities and approaches, then the DMA’s ability to achieve coherence is likely to be scuppered before its rules even take effect. While public resolutions of these matters are unlikely before the second half of 2023, this is a key topic to watch in order to understand the impact the DMA is likely to have on European digital markets.

UK

As we previously explained3, the Queen’s Speech in May 2022 announced that the government would publish a draft Digital Markets, Competition and Consumer Bill, which would provide the Competition and Markets Authority (CMA) with new regulatory tools in the digital space (explained in more detail in our Handbook). Over the summer of last year, this effort appeared to have been deprioritized, but in the Autumn Statement the Sunak government tabled it for presentation to lawmakers “in the third Parliamentary session”– implying that the bill would be published in Q1 or early Q2 of this year. It is not yet clear whether the recent changes to the UK government departments (including the break-up of the Department of Business, Energy and Industrial Strategy (BEIS), the previous sponsoring department) will result in delay. While the draft is still unlikely to make it into law in 2023, this year should provide more clarity on its content and on how it will interact with existing antitrust enforcement in this area by the CMA’s Digital Markets Unit (which currently operates in “shadow” form pending the legislation).

UK

As we previously explained3, the Queen’s Speech in May 2022 announced that the government would publish a draft Digital Markets, Competition and Consumer Bill, which would provide the Competition and Markets Authority (CMA) with new regulatory tools in the digital space (explained in more detail in our Handbook). Over the summer of last year, this effort appeared to have been deprioritized, but in the Autumn Statement the Sunak government tabled it for presentation to lawmakers “in the third Parliamentary session”– implying that the bill would be published in Q1 or early Q2 of this year. It is not yet clear whether the recent changes to the UK government departments (including the break-up of the Department of Business, Energy and Industrial Strategy (BEIS), the previous sponsoring department) will result in delay. While the draft is still unlikely to make it into law in 2023, this year should provide more clarity on its content and on how it will interact with existing antitrust enforcement in this area by the CMA’s Digital Markets Unit (which currently operates in “shadow” form pending the legislation).

In the meantime, the CMA is progressing existing antitrust investigations into digital platforms and has opened several new cases. For instance, the CMA referred its Mobile Ecosystems market study to an in-depth market investigation into cloud gaming and mobile browsers in November 2022. This reference came despite the CMA concluding in December 2021 in its interim report that a market investigation wasn’t necessary in light of the forthcoming legislation. The change in approach may evidence a desire within the CMA to make use of its existing toolbox during the delay to sectoral legislation.

The other development to watch in the UK is the progress of the Online Safety Bill – a cousin to the Digital Services Act (DSA) – that features “duties of care” for social media and search companies. The bill was initially introduced in March 2022 but has made slow progress since. The current government has backed an amended version that removes duties to assess content that is “legal but harmful” to adults, and that may therefore make progress also in 2023. Again, the recent changes to UK government departments may have an impact on timing if responsibility for this digital regulation is moved from the ‘refocused’ Department for Digital, Culture, Media and Sport.

In the meantime, the CMA is progressing existing antitrust investigations into digital platforms and has opened several new cases. For instance, the CMA referred its Mobile Ecosystems market study to an in-depth market investigation into cloud gaming and mobile browsers in November 2022. This reference came despite the CMA concluding in December 2021 in its interim report that a market investigation wasn’t necessary in light of the forthcoming legislation. The change in approach may evidence a desire within the CMA to make use of its existing toolbox during the delay to sectoral legislation.

The other development to watch in the UK is the progress of the Online Safety Bill – a cousin to the Digital Services Act (DSA) – that features “duties of care” for social media and search companies. The bill was initially introduced in March 2022 but has made slow progress since. The current government has backed an amended version that removes duties to assess content that is “legal but harmful” to adults, and that may therefore make progress also in 2023. Again, the recent changes to UK government departments may have an impact on timing if responsibility for this digital regulation is moved from the ‘refocused’ Department for Digital, Culture, Media and Sport.

U.S.

While 2022 was characterized by a slew of digital regulation proposals focused on curbing “self-preferencing” by digital platforms, 2023 is likely to see less attention on new digital regulations, at least at the federal level. Despite benefitting from some bipartisan support, none of the proposals introduced last year progressed through the legislative process, largely due to concerns over privacy, security, and content moderation. These proposals will face longer odds in the now-divided chambers of the U.S. legislature.

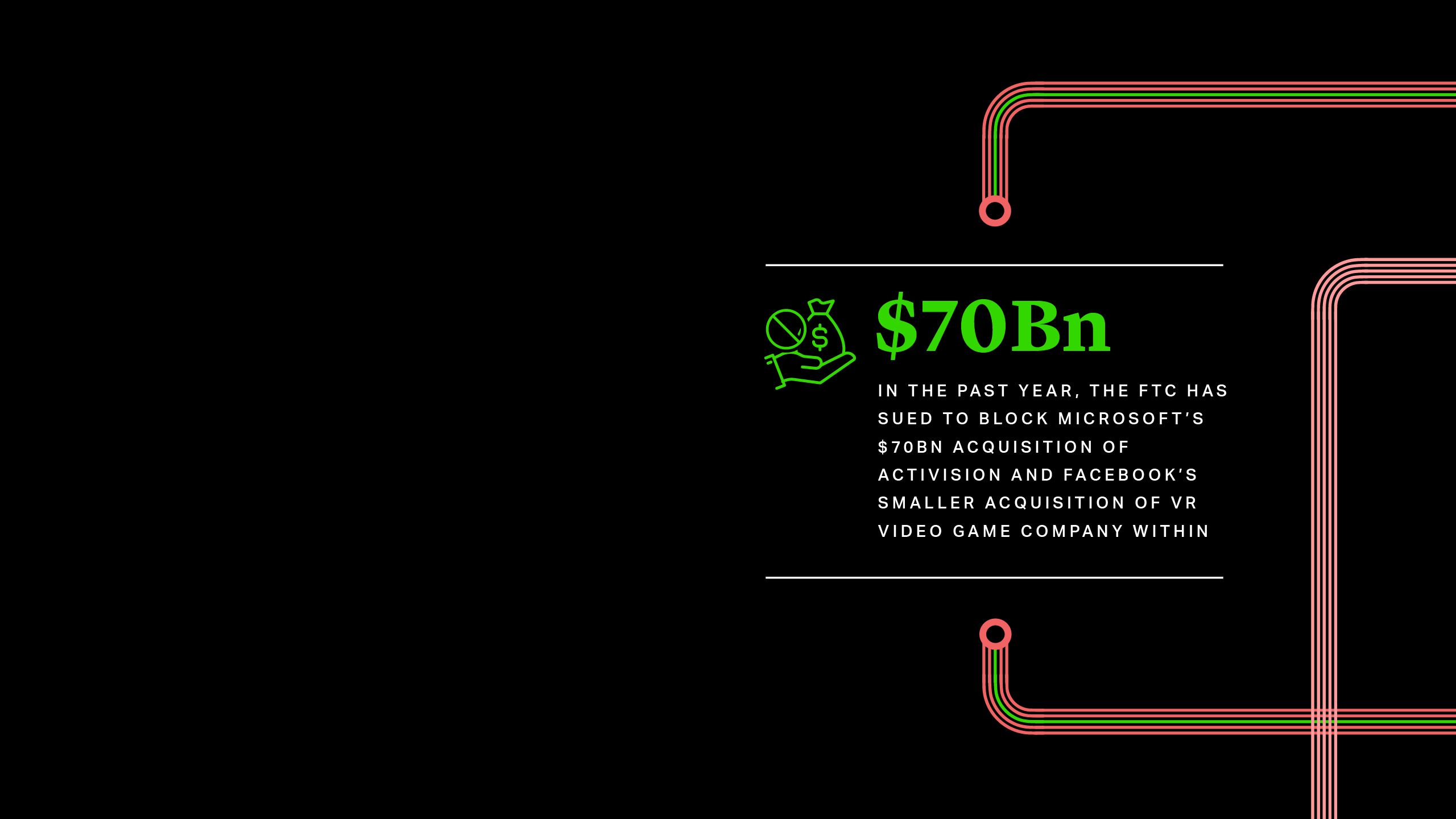

This is not to say that interventions in digital markets are not a policy priority. Federal enforcement against digital platforms under existing laws is likely to continue in 2023. In the past year, the Federal Trade Commission (FTC) has sued to block Microsoft’s $70bn acquisition of Activision and Facebook’s smaller acquisition of VR video game company Within, although Facebook ultimately prevailed in Court. And in January this year, the Department of Justice brought claims against Google, calling for a break-up of its digital advertising business. The FTC also continues to pursue its challenge to the long-consummated acquisitions of Instagram (2012) and WhatsApp (2014). Beyond these publicly filed suits, the agencies have opened a number of probes into the major digital platforms.

Australia

We end our review of the year-to-come in Australia, which we also discussed in our Digital Regulation Handbook. Australia has been catching up on the global digital regulation trend, but is still at a preparatory stage.

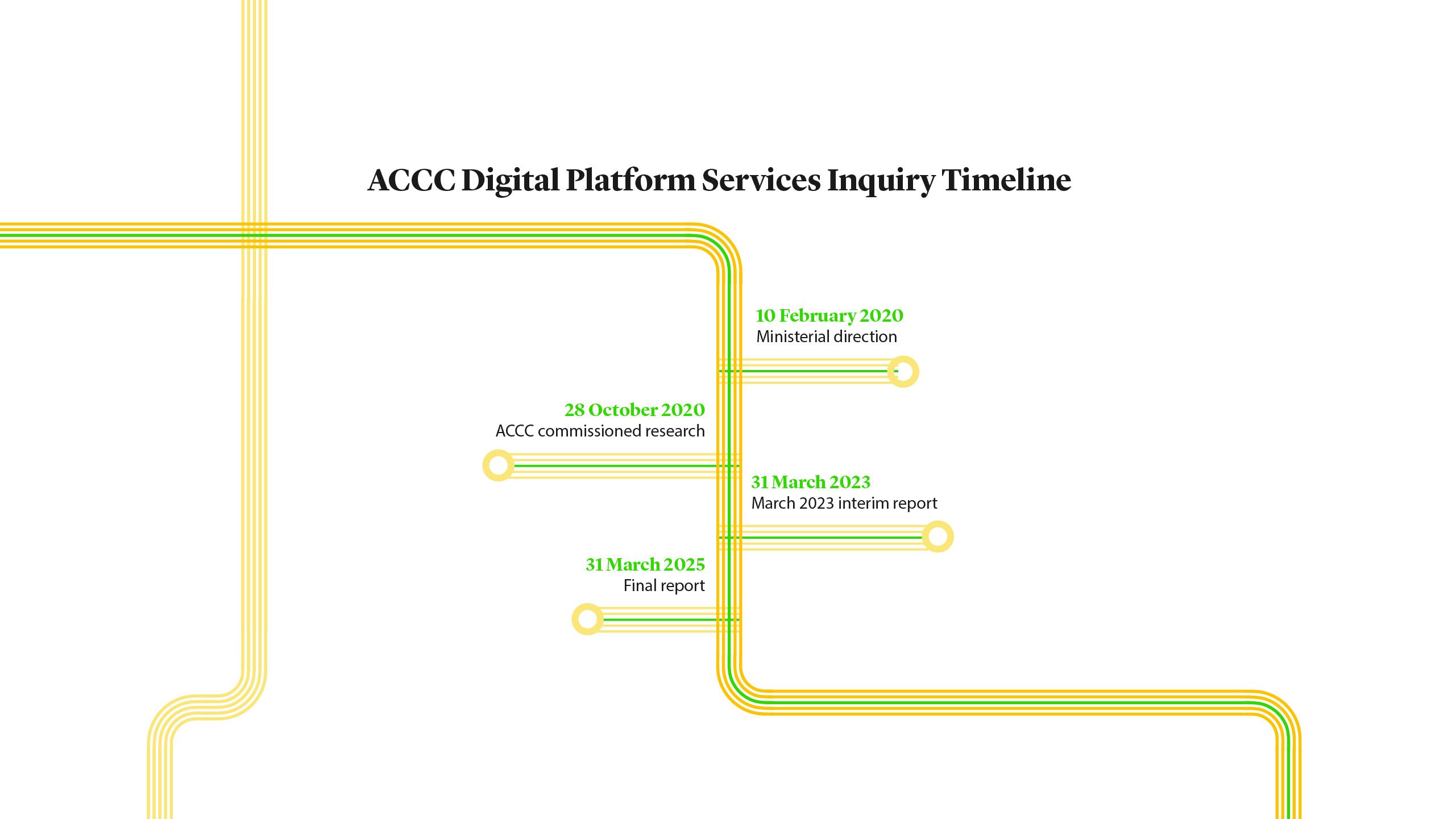

The Australian Competition and Consumer Commission (ACCC) is now halfway through its major inquiry into digital platform services, which has been in progress since 2020 and is due to conclude in 2025. The former ACCC chair had called for “ex ante rules to describe what [digital platforms] should and shouldn’t do,” anxious that “if Australia doesn’t get on board, the bus will leave without us.” The inquiry is designed to map out such potential rules.

As part of its inquiry, the ACCC published its fifth interim report on November 11, 2022. The report recommends mandatory, service-specific codes of conduct for designated digital platforms, operating under high-level principles that would be enshrined in primary legislation. While the precise content of the rules remains uncertain, the interim report provided examples of potential rules including prohibitions on anticompetitive self-preferencing, tying, and bundling; transparency requirements in ad tech; and choice screens.

With another interim report due in March 2023, the upcoming year should see further refinements to what the recommended rules may be. We also expect more details on their substantive content and scope.

Whatever the outcome of regulatory efforts in individual jurisdictions, global themes and patterns are emerging and provide an early insight into these initiatives’ likely impact.

Whatever the outcome of regulatory efforts in individual jurisdictions, global themes and patterns are emerging and provide an early insight into these initiatives’ likely impact.

Nicholas Levy

Partner

London

T: +44 20 7614 2243

Brussels

T: +32 2 287 2311

nlevy@cgsh.com

V-Card

Jackie Holland

Partner

London

T: +44 20 7614 2233

Brussels

jaholland@cgsh.com

V-Card

Leah Brannon

Partner

Washington, D.C.

T: +1 202 974 1508

lbrannon@cgsh.com

V-Card

Henry Mostyn

Partner

London

T: +44 20 7614 2241

hmostyn@cgsh.com

V-Card

Conor Opdebeeck‑Wilson

Associate

Brussels

T: +32 22872211

copdebeeckwilson@cgsh.com

V-Card

Michael Goldenberg

Associate

Washington, D.C.

T: +1 202 974 1642

mgoldenberg@cgsh.com

V-Card