It is no secret that the COVID-19 pandemic drastically changed the way we work and, importantly for the commercial real estate sector, the type of office space companies used. During the pandemic, economists estimate that occupancy in the major office markets of the U.S. fell from 95% at the end of February 2020 to 10% at the end of March the same year1. Today, those rates have yet to fully recover with occupancy still hovering around 80% as of April 20242.

The decline in vacancy rates has largely been attributed to companies downsizing office space because of the hybrid work model3. When coupled with rising interest rates, which have pushed down building revenue and raised the cost of refinancing, some are predicting that 2024 could be the year that commercial real estate hits a “breaking point”4.

A number of these predictions suggest that the distress coming “will likely include a swelling number of bankruptcies, mergers, and forced property sales.” To date, we have not seen a significant number of bankruptcies filed by builder owners, but we have seen one significant bankruptcy by a large commercial tenant: WeWork. The WeWork bankruptcy provides some lessons about what the future holds for the commercial real estate industry.

The decline in vacancy rates has largely been attributed to companies downsizing office space because of the hybrid work model3. When coupled with rising interest rates, which have pushed down building revenue and raised the cost of refinancing, some are predicting that 2024 could be the year that commercial real estate hits a “breaking point”4.

A number of these predictions suggest that the distress coming “will likely include a swelling number of bankruptcies, mergers, and forced property sales.” To date, we have not seen a significant number of bankruptcies filed by builder owners, but we have seen one significant bankruptcy by a large commercial tenant: WeWork. The WeWork bankruptcy provides some lessons about what the future holds for the commercial real estate industry.

WeWork: A Case Study

WeWork, which opened its first location in Manhattan in 2011, is a large provider of shared office space5. WeWork’s basic business model relied on the premise that it could lease and refurbish office space and re-let the properties to companies and individuals at a marked-up price6. WeWork filed for bankruptcy in November 2023, citing, among other factors a lack of profitable leases7.

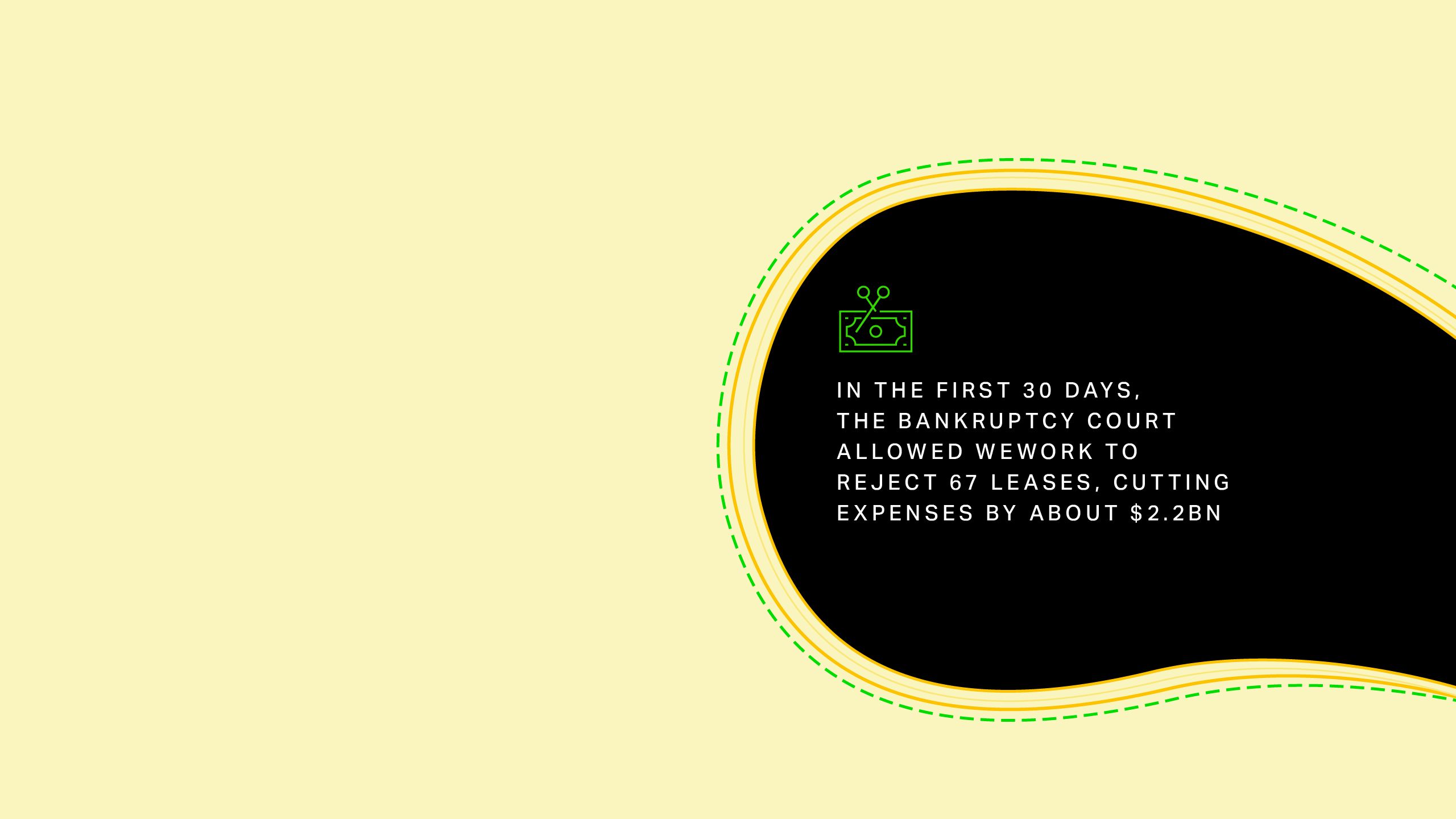

When it first entered bankruptcy, WeWork had approximately 500 leases, which accounted for more than two-thirds of its total cost structure and were valued at roughly $23bn8. In the first 30 days, the bankruptcy court allowed the company to reject 67 leases, cutting expenses by about $2.2bn. These rejections were merely the start of a wave, with many more coming throughout the administration of the Chapter 11 proceedings.

These leases are rejectable as executory contracts under Section 365(a) of the Code, so long as the lease is unexpired (i.e., is a contract under which each party still has material unperformed obligations). The lease must be assumed or rejected in its entirety – debtors cannot merely assume favorable portions of the lease. In doing so, there are a few key considerations to note:

Timing: Section 365(d)(4) of the Code sets special deadlines for commercial real property lease agreements, providing debtors 120 days after filing a Chapter 11 petition to decide whether to reject an unexpired commercial real property lease, though extensions may be granted for good cause for up to an additional 90 days9. Any additional extensions beyond 210 days may only be granted with the prior written consent of the counterparty to the lease10.

Performance: While the debtor is evaluating whether to assume or reject an unexpired lease in the bankruptcy case, it must timely perform all of its obligations under the lease, including paying the full contract rent when due11. The bankruptcy court may choose to grant the debtor-tenant a temporary deferral, not to last longer than the first 60 days, of its obligations under the lease for good cause while the lease is pending rejection or assumption12. If the debtor assumes the lease, it must continue rent payments.

Rejection Damages: Section 502(b)(6) of the Code imposes a special cap on the amount of rejection damages stemming from unexpired real property leases that may be allowed as a claim entitled to receive distributions in the case13. The provision caps the landlord’s recovery to “rent reserved from the greater of (1) one lease year or (2) 15%, not to exceed three years, of the remaining lease term.”14 Notably, this is a cap, not a floor, and thus the damages may be lower.

These debtor-friendly provisions have helped WeWork perform a quick turnaround in its restructuring. At the time of WeWork’s emergence from bankruptcy on June 11, 2024, it had renegotiated more than 190 leases, rejected more than 170, and reduced its annual rent expectations by more than $800mn, or more than $12bn of total future rent obligations15.

WeWork’s Implications for Commercial Building Owners

Bankruptcy has been a helpful tool for WeWork, but it has left certain building owners subject to rejection to pick up the pieces. Those with long term leases beyond three years have no legal recourse to recover damages for the remaining lease years they would be entitled to outside of a bankruptcy.

Given the panoply of tenant-friendly provisions in the bankruptcy code, one lesson from WeWork for commercial building owners is to be open to negotiating both before and after a bankruptcy filing. These statistics provide a key window into the process: not every lease needs to be rejected. Rather, emphasizing the ability to reject leases may provide more room for fair negotiations for debtors straddled with leases, but may also provide building owners with the ability to squeeze slightly more out of a debtor tenant. WeWork was able to enter into amended leases with several building owners, which allow building owners to negotiate for bespoke go-forward terms, rather than being forced to search for a new-tenant after a lease rejection.

Even though some building owners were able to negotiate to avoid the worst outcome in the WeWork bankruptcy, the case provides proof that the demand for office space remains tenuous and that building owners need to think critically about how to navigate this brave new world. Options for building owners include trying to negotiate expensive financing with lenders or to negotiate an out of bankruptcy fire sale to cut their losses.

Further, just as the bankruptcy code provides favorable provisions for tenants, it can be a useful tool for building owners as well. Section 363(b) of the bankruptcy code allows building owners to sell property through the bankruptcy process16. Importantly, under 363(f) the Building Owner may sell the property free and clear of any interests, such as liens, in such property17. Thus, while the future for commercial real estate is uncertain, understanding how to successfully navigate bankruptcy both as a creditor and a debtor, will be key in allowing building owners to navigate these challenging times.

Further, just as the bankruptcy code provides favorable provisions for tenants, it can be a useful tool for building owners as well. Section 363(b) of the bankruptcy code allows building owners to sell property through the bankruptcy process16. Importantly, under 363(f) the Building Owner may sell the property free and clear of any interests, such as liens, in such property17. Thus, while the future for commercial real estate is uncertain, understanding how to successfully navigate bankruptcy both as a creditor and a debtor, will be key in allowing building owners to navigate these challenging times.