Navigating the Shifting ESG Risks in Insolvency and Restructuring

Environmental, Social and Governance or “ESG” risks are becoming more entrenched in the financial markets generally, but they can present themselves in the restructuring world in a number of ways. For example, ESG-related concerns can be the primary reason for a restructuring, either because the business is no longer viable due to a lack of investor interest, declining revenues or legal challenges, or it can drive a company’s emergence from restructuring as investors increasingly look for ESG-focused investment vehicles.

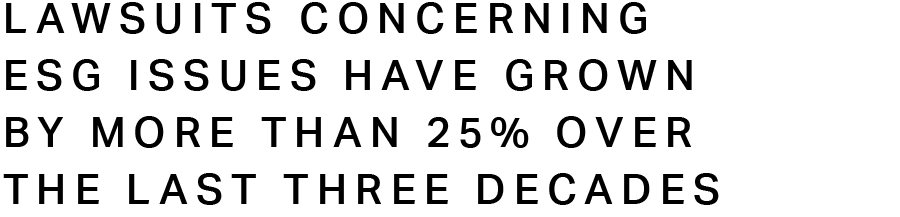

More generally, ESG trends are playing a growing role in restructuring, especially considering the increase in market litigation related to sustainability – lawsuits concerning ESG issues have grown by more than 25% over the last three decades, according to analysis this year by the World Business Council for Sustainable Development1. In recent years, companies have also sought to include new ESG angles in debt issuances to take advantage of the market’s interest. In this article, we explore some of these recent ESG trends in the insolvency and restructuring context, and the implications.

Environmental, Social and Governance or “ESG” risks are becoming more entrenched in the financial markets generally, but they can present themselves in the restructuring world in a number of ways. For example, ESG-related concerns can be the primary reason for a restructuring, either because the business is no longer viable due to a lack of investor interest, declining revenues or legal challenges, or it can drive a company’s emergence from restructuring as investors increasingly look for ESG-focused investment vehicles.

More generally, ESG trends are playing a growing role in restructuring, especially considering the increase in market litigation related to sustainability – lawsuits concerning ESG issues have grown by more than 25% over the last three decades, according to analysis this year by the World Business Council for Sustainable Development1. In recent years, companies have also sought to include new ESG angles in debt issuances to take advantage of the market’s interest. In this article, we explore some of these recent ESG trends in the insolvency and restructuring context, and the implications.

Toxic Tort Cases

One example of a general trend towards environmental-related litigation can be seen in toxic tort class actions. Recent Examples include claims against AT&T in September 2023 in connection with the company’s use of lead-sheathed cables2. In the same month, legal actions were also filed against a number of entities in Hawaii stemming from the devastating wildfires in the state, including the State of Hawaii, the County of Maui, and several utility companies. One lawsuit against Hawaiian Electric alleges that the company negligently caused fires, while the county is accused of negligence in fire prevention and response efforts.

In the longer term, we expect to see an increase in lawsuits from all corners: environmental groups, investors, and ordinary citizens, suing governments as well as private enterprises for environmental liabilities. These could either focus on the failure to comply with environmental guidelines or to provide sufficient transparency. Businesses that are not well-adapted to the current environmental focus are likely to see more distress and insolvency risk. These types of mass tort cases springing from disasters almost always lead to some form of insolvency proceeding, and previous insolvencies provide clues as to how recent restructurings could play out.

For example, PG&E filed for bankruptcy in 2019 after its faulty equipment sparked several fires in California, including the 2018 Camp Fire that killed 84 people. The company ended up reaching a $13.5bn settlement with the victims of that wildfire and several others in 2015, 2016, and 2017. The restructuring played out amid a confluence of climate regulation and private markets. Because of state law, PG&E essentially had uncapped liability for any wildfires caused by the company’s equipment, which put the entity under a significant amount of pressure, even if there were other alleged causes for the fires.

We continue to track legislation that relates to corporate accountability and climate, as companies will need to respond to this and mitigate the risk of loss. For example, the California legislature has recently passed two climate-related legislative measures to standardize climate disclosures, align public investments with climate objectives and raise the criteria for companies to promote climate action3. This is especially important because there is a strong correlation between the increase in environmental liabilities, litigation and insolvency, as demonstrated by the fact that, as mentioned, liabilities can result in mass tort litigation, which is often followed by insolvency.

Toxic Tort Cases

One example of a general trend towards environmental-related litigation can be seen in toxic tort class actions. Recent Examples include claims against AT&T in September 2023 in connection with the company’s use of lead-sheathed cables2. In the same month, legal actions were also filed against a number of entities in Hawaii stemming from the devastating wildfires in the state, including the State of Hawaii, the County of Maui, and several utility companies. One lawsuit against Hawaiian Electric alleges that the company negligently caused fires, while the county is accused of negligence in fire prevention and response efforts.

In the longer term, we expect to see an increase in lawsuits from all corners: environmental groups, investors, and ordinary citizens, suing governments as well as private enterprises for environmental liabilities. These could either focus on the failure to comply with environmental guidelines or to provide sufficient transparency. Businesses that are not well-adapted to the current environmental focus are likely to see more distress and insolvency risk. These types of mass tort cases springing from disasters almost always lead to some form of insolvency proceeding, and previous insolvencies provide clues as to how recent restructurings could play out.

For example, PG&E filed for bankruptcy in 2019 after its faulty equipment sparked several fires in California, including the 2018 Camp Fire that killed 84 people. The company ended up reaching a $13.5bn settlement with the victims of that wildfire and several others in 2015, 2016, and 2017. The restructuring played out amid a confluence of climate regulation and private markets. Because of state law, PG&E essentially had uncapped liability for any wildfires caused by the company’s equipment, which put the entity under a significant amount of pressure, even if there were other alleged causes for the fires.

We continue to track legislation that relates to corporate accountability and climate, as companies will need to respond to this and mitigate the risk of loss. For example, the California legislature has recently passed two climate-related legislative measures to standardize climate disclosures, align public investments with climate objectives and raise the criteria for companies to promote climate action3. This is especially important because there is a strong correlation between the increase in environmental liabilities, litigation and insolvency, as demonstrated by the fact that, as mentioned, liabilities can result in mass tort litigation, which is often followed by insolvency.

Specific Sectors

Key industries where we are clearly seeing ESG trends having an impact in the restructuring space include metals and mining and oil and gas. The options for the companies in these sectors are diminishing as they hold onto assets or production methods that are not clean or sustainable.

Many companies that have coal assets, for example, are looking to sell these. Perhaps the most prominent of these stories is the empire created by Indian billionaire, Gautam Adani. At the beginning of 2023, one of the suggestions for dealing with the Adani Group’s debt was to monetize its coal assets, but it failed to proceed as there were few investors willing to enter the space4.

ESG trends can have an impact on the appetite of investors to provide funding, particularly in the case of large conglomerates with investments in different sectors (some of which are not considered to be clean assets). This can significantly limit the options for those businesses when they require liquidity.

Specific Sectors

Key industries where we are clearly seeing ESG trends having an impact in the restructuring space include metals and mining and oil and gas. The options for the companies in these sectors are diminishing as they hold onto assets or production methods that are not clean or sustainable.

Many companies that have coal assets, for example, are looking to sell these. Perhaps the most prominent of these stories is the empire created by Indian billionaire, Gautam Adani. At the beginning of 2023, one of the suggestions for dealing with the Adani Group’s debt was to monetize its coal assets, but it failed to proceed as there were few investors willing to enter the space4.

ESG trends can have an impact on the appetite of investors to provide funding, particularly in the case of large conglomerates with investments in different sectors (some of which are not considered to be clean assets). This can significantly limit the options for those businesses when they require liquidity.

Litigation or Regulation?

Any emphasis on regulating environmental liability is likely to be led by efforts in the UK and EU. Historically, the U.S. has been big on talk and small on action in regulating this space, particularly at the federal level, and instead we expect a greater focus will be on private and state litigation in the country. Notably, the U.S. court system is relatively easy to access, and ESG trends provide an avenue to concoct arguments on environmental liability. This approach remains a costlier affair in Europe and the UK, where unsuccessful litigants are more likely to be faced with having to pay their opponents’ legal fees.

Process and issues will likely be driven by the specific jurisdiction in which a lawsuit is filed. For multinational groups those could be numerous and not necessarily the ones where the operations are conducted. We are seeing increasing amounts of parent companies headquartered in the UK, for example, being held liable for corporate torts of subsidiary companies located in emerging markets. Environmental regulations or legislation in different jurisdictions can, thus, sometimes be effectively “overridden” by the transnational aspect of lawsuits and the sophistication of the legal system in which the lawsuit is filed.

Litigation or Regulation?

Any emphasis on regulating environmental liability is likely to be led by efforts in the UK and EU. Historically, the U.S. has been big on talk and small on action in regulating this space, particularly at the federal level, and instead we expect a greater focus will be on private and state litigation in the country. Notably, the U.S. court system is relatively easy to access, and ESG trends provide an avenue to concoct arguments on environmental liability. This approach remains a costlier affair in Europe and the UK, where unsuccessful litigants are more likely to be faced with having to pay their opponents’ legal fees.

Process and issues will likely be driven by the specific jurisdiction in which a lawsuit is filed. For multinational groups those could be numerous and not necessarily the ones where the operations are conducted. We are seeing increasing amounts of parent companies headquartered in the UK, for example, being held liable for corporate torts of subsidiary companies located in emerging markets. Environmental regulations or legislation in different jurisdictions can, thus, sometimes be effectively “overridden” by the transnational aspect of lawsuits and the sophistication of the legal system in which the lawsuit is filed.

ESG-Focused Financing

Investors are increasingly keen to embrace nature-linked causes as part of bond issuances or debt exchanges, as highlighted in Cleary Gottlieb’s Emerging Market Restructuring Journal5. But while, initially, the primary market focus was on ‘green’ and ‘blue’ bonds and financings – where proceeds of the issuances are used for a specific project of purpose – for the past few years there has been an exponential growth in the number of sustainability-linked financings not tied to a specific project.

Rather, in these instances the issuer agrees to adhere to certain targets related to a broader array of causes including social targets, for example, gender equality in management, and financing pricing is linked to the extent a company meets these specific targets.

There are a number of issues with these instruments though, including those related to the reporting and auditing of the extent to which companies are meeting such targets. We expect this will continue to be a hot topic, especially considering that investors are growing more cautious about potential greenwashing by companies.

We also expect to see more sophisticated terms being included in these financings in the near future. One of the ideas that has been toyed with is a requirement for a debtor to invest the benefits that it receives (as financing costs) from these financings into specific ESG projects.

Companies will increasingly have to grapple with ESG concerns, whether in the context of litigation, funding, or regulation. We will continue to monitor the trends and report on how they fit within the debt space.