The COP summits are less ideologically contentious than they have been in the past due to a growing consensus held by policymakers about the impact of climate change on the way all people live their lives. Legislative momentum is gathering as countries seek to create the legal and regulatory framework that will enable their compliance with stated net zero targets. Having a robust approach to accessing critical minerals and metals needed for green energy is essential. The U.S. has passed a slew of legislation that impacts the attainment of these targets since 2013 and has quickened its pace since the release of the Department of Energy’s 2021 Critical Minerals Strategy1.

The European Union (EU) and the UK are no laggards. In March, the European Commission presented its new Critical Raw Metals Act, which states that no third country should provide more than 65% of any strategic raw material2. It leaves room for domestic sourcing, a large component of which is expected to come from recycling refined products. The UK’s Critical Minerals Strategy touches on similar themes including enhanced supply chain transparency3. Developing diversified and strong supply chains, almost all of which will originate in Africa, will be crucial to the EU, UK and U.S. meeting their decarbonization targets.

Africa is home to sizeable platinum, nickel, copper, cobalt, lithium, graphite, and titanium deposits – all of which are essential components of green technology including batteries and electric vehicles (EVs). For example, 70% of global cobalt reserves are located in the Democratic Republic of Congo (DRC); Zimbabwe hosts the world’s second largest deposits of chromium ore; Madagascar, Mozambique, and Tanzania have significant graphite deposits; and the Republic of Guinea contains the world’s largest bauxite reserves. For most of these countries, their political risk profile has complexities that can trigger unexpected upheaval which further complicates an already challenging operating environment.

While investors are seeking to mitigate the political and operational risks, the mining policy environment is shifting as African governments seek to reposition their countries in the global value chain. On July 8, 2023, Namibia banned the export of certain unprocessed crucial minerals including lithium ore, cobalt, and graphite. Eight months prior, the Zimbabwean government banned all unprocessed lithium exports and has recently announced plans to establish a lithium-ion battery plant. Other countries are expected to follow suit as they look to move beyond exporting raw materials and develop local industries.

Africa is home to sizeable platinum, nickel, copper, cobalt, lithium, graphite, and titanium deposits – all of which are essential components of green technology including batteries and electric vehicles (EVs). For example, 70% of global cobalt reserves are located in the Democratic Republic of Congo (DRC); Zimbabwe hosts the world’s second largest deposits of chromium ore; Madagascar, Mozambique, and Tanzania have significant graphite deposits; and the Republic of Guinea contains the world’s largest bauxite reserves. For most of these countries, their political risk profile has complexities that can trigger unexpected upheaval which further complicates an already challenging operating environment.

While investors are seeking to mitigate the political and operational risks, the mining policy environment is shifting as African governments seek to reposition their countries in the global value chain. On July 8, 2023, Namibia banned the export of certain unprocessed crucial minerals including lithium ore, cobalt, and graphite. Eight months prior, the Zimbabwean government banned all unprocessed lithium exports and has recently announced plans to establish a lithium-ion battery plant. Other countries are expected to follow suit as they look to move beyond exporting raw materials and develop local industries.

The DRC and Zambia have established a Joint Electric Vehicle Battery Initiative that will facilitate the creation of a new sector by establishing a special economic zone (SEZ) “dedicated to the production of battery precursors, batteries, and electric vehicles”4. A fresh attempt to leverage new investor interest in minerals and metals driven by the green energy transition to develop new industries is commendable. Frameworks such as the Southern African Development Community (SADC) Regional Mining Vision and ECOWAS (Economic Community of West African States) Model Mining and Minerals Development Act will help to ensure closer cross-border policy alignment while leveraging economies of scale and greater stability of supply.

However, the two main factors that will hold back African countries’ progression along the value chain are limited domestic demand for processed metals and minerals, and erratic power supply. A determining factor in the commercial viability of African governments’ development of mid and downstream industries is their proximity to other parts of the value chain. An efficient battery production process favors close proximity between a mine and a chemical plant to produce the battery precursor material that will be used to make battery cathodes. Transporting battery cathodes is tricky and necessitates a nearby battery cell manufacturing plant, which needs to be close to EV manufacturers to best serve the client and beat competitors. The final component needed to ensure commercial viability and success is a large domestic market. Currently, no African market has sufficient local demand or the charging infrastructure to accommodate EVs.

Reliable access to power is required in order for all phases of the value chain to operate efficiently from mine site to the battery production plant. Zambia has been experiencing crippling power blackouts (outages) for up to 12 hours for the past three years. Neighboring Zimbabwe has occasionally experienced outages lasting up to 20 hours. This is due to erratic weather patterns – floods, droughts, and cyclones – displacing tens of thousands, exacerbating food insecurity by destroying food harvests, and placing a drag on economic growth due to triggering power supply interruptions. The Southern African region is heavily reliant on hydroelectricity and the Kariba Dam, jointly administered by Zambia and Zimbabwe, has not reached full capacity since 20115.

Regional hegemon South Africa is in the doldrums due to years of maladministration and corruption targeting its state power producer Eskom. The power blackouts that previously only affected its neighbors are now a daily occurrence. This has forced mining companies and downstream industries, including car manufacturers in South Africa, to reduce their reliance on the national grid and seek greater energy independence by using renewable energy and costly diesel generators. It is within this context that regional policymakers are seeking to move further along the mining value chain. It is not an exercise in futility, but it is one that requires greater dexterity, stronger regional coordination, and more targeted public-private partnerships to create a more conducive business environment.

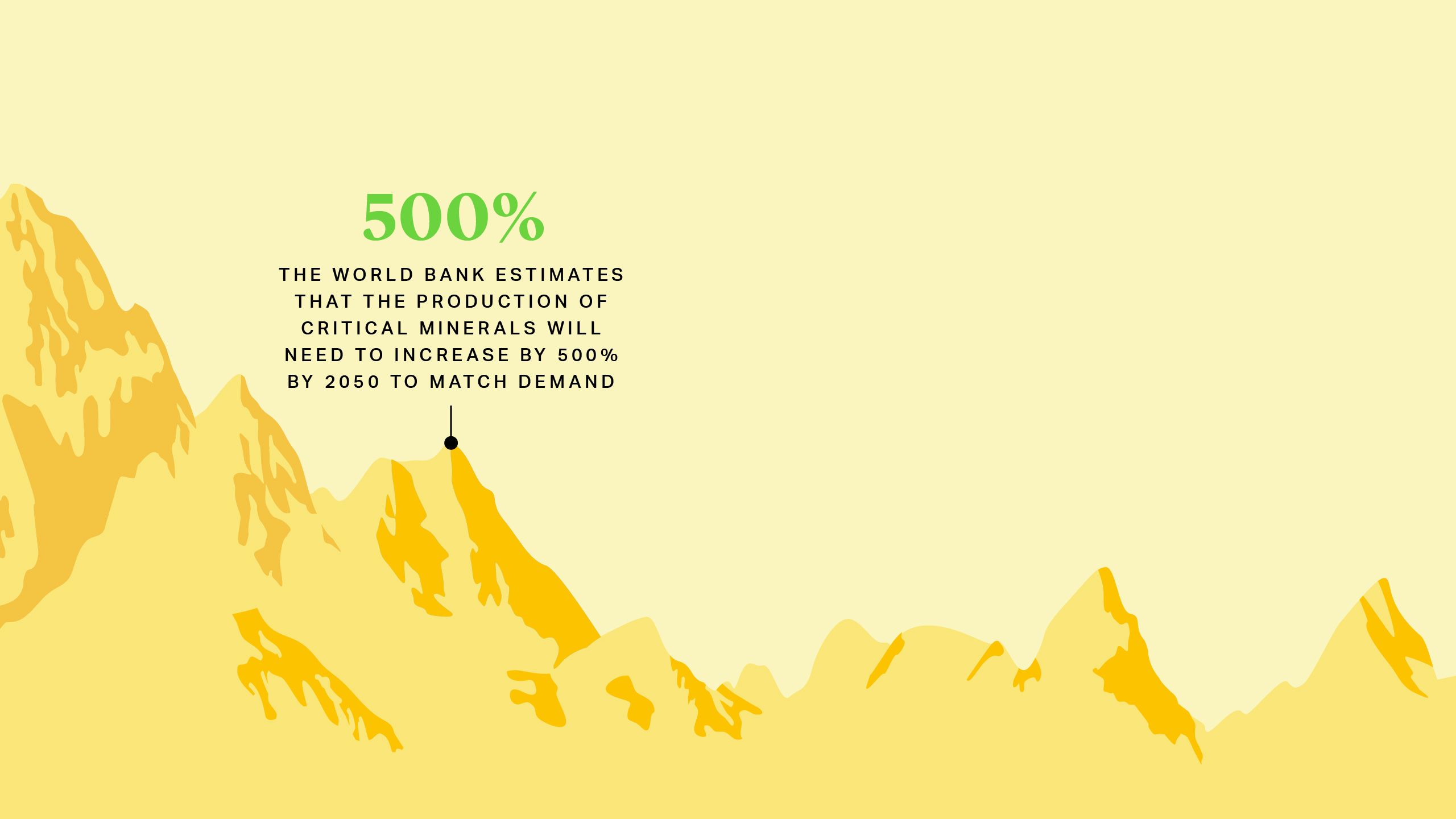

A 2020 World Bank study estimates that the production of critical minerals will need to increase by 500% by 2050 to match demand6. It takes an average of 17 years to develop a new mineral discovery and start production, meaning supply will lag demand driven by countries seeking to meet their just energy transition targets. The pace of the development of new mining projects will be further slowed down by the underinvestment in the region’s ailing power grid.

Inga Dams and Africa Energy Output

Source: BBC (using data from EDF and American Energy Agency)

Source: BBC (using data from EDF and American Energy Agency)

The oft-touted Grand Inga Hydroelectric Scheme, which involves developing six additional hydroelectric power stations located in the DRC, can potentially add 43,200 MW to the Southern African Power Pool when completed. This mammoth project comes at an estimated $80bn price tag and the technical challenges are formidable. The World Bank has yet to publicly announce a return to discussions after pulling out in 2016 due to a change in “strategic direction” from what was discussed with the government two years prior7. The project has a multitude of moving pieces and has long been characterized with a “too big, it will fail” sentiment. However, boosting regional power generation and improving transmission in some form is crucial to attracting greater investment in the mining industry and developing downstream industries.

The oft-touted Grand Inga Hydroelectric Scheme, which involves developing six additional hydroelectric power stations located in the DRC, can potentially add 43,200 MW to the Southern African Power Pool when completed. This mammoth project comes at an estimated $80bn price tag and the technical challenges are formidable. The World Bank has yet to publicly announce a return to discussions after pulling out in 2016 due to a change in “strategic direction” from what was discussed with the government two years prior7. The project has a multitude of moving pieces and has long been characterized with a “too big, it will fail” sentiment. However, boosting regional power generation and improving transmission in some form is crucial to attracting greater investment in the mining industry and developing downstream industries.

The U.S., EU, UK, and partner countries will benefit from supporting African countries’ efforts to industrialize and move from simply exporting raw minerals to playing a more substantive role in the global economy as it transitions towards green energy. Encouraging and financially backing attempts to localize the critical minerals value chain has several benefits, including reducing the overall carbon emissions footprint of the final product and developing local industries and job creation efforts which ultimately address endemic poverty and associated national and local insecurity.

There is also a strategic imperative to supporting Africa’s industrialization. China presently has 90% of global rare earth elements (REE) processing capacity, and the EU and U.S. are reliant on it for refined graphite and lithium ore which form part of the core requirements of its green energy calculations. The Global North is vulnerable to restrictions and/or reductions in supply. Diversification is essential.

The U.S., EU, UK, and partner countries will benefit from supporting African countries’ efforts to industrialize and move from simply exporting raw minerals to playing a more substantive role in the global economy as it transitions towards green energy. Encouraging and financially backing attempts to localize the critical minerals value chain has several benefits, including reducing the overall carbon emissions footprint of the final product and developing local industries and job creation efforts which ultimately address endemic poverty and associated national and local insecurity.

There is also a strategic imperative to supporting Africa’s industrialization. China presently has 90% of global rare earth elements (REE) processing capacity, and the EU and U.S. are reliant on it for refined graphite and lithium ore which form part of the core requirements of its green energy calculations. The Global North is vulnerable to restrictions and/or reductions in supply. Diversification is essential.

Interestingly, China adopted a similar policy stance in the 1990s to the one taken by some African governments during this new minerals and metals boom. It reclassified REE as strategic and legislated that foreign companies had to jointly process REE with Chinese companies8. This, coupled with lax environmental, health, and safety standards, led to China’s mid-stream dominance today. While some African policymakers may be inspired by this approach, it has come at a significant environmental cost.

The meaning and implication of a just energy transition are not universal. The environmental consequences of policy changes implemented in the Global North, in line with the broad international sentiment about the need to reduce carbon emissions, are felt in the Global South. While Western countries are seeking to transition to cleaner energy, developing countries are seeking access to energy. A long history of poor practices by states, mining companies, and non-state actors lingers and links the two halves in new ways.

There is an energy access gap and closing it is in the best interests of Western governments and companies seeking security of critical mineral supply. As mines become increasingly mechanized, the job creation potential diminishes, African governments have an opportunity to advocate for local procurement and support small businesses. They need to do their part by providing relevant training to ensure they have the requisite skills and capacity. Rhetoric around tackling illicit financial flows needs to change to tough action, and all parties interested in enabling accountability need to push for contract transparency as well as free, prior, and informed consent (FPIC) of communities directly impacted by mining activity9.

Exceeding, rather than simply complying with national regulations in host countries will increasingly be required of actors that want to extract value. The scrutiny and rebuke for violations may not immediately come from host governments; ideas and approaches are being cross-pollinated by an increasingly interconnected web of investigative journalists, civil society organizations, and indigenous groups. The consumer base is also changing as new global norms about climate change start to trickle down and guide their wallets. A muddled approach towards the “right way” to bring about this energy transition with a semblance of justice will be paved with good intentions and filled with papered-over potholes about what not to do. The hope is that we all don’t get lost along the way yet again.