Since the adoption of EU Directive 2019/1023 on restructuring and insolvency in June 2019, EU member states are implementing the respective legal framework into their local laws. The Czech Government is presently working on a bill known as the Preventive Restructuring Act, intended to enable resolving pre-insolvency situations for companies in financial difficulties without the stigma of an insolvency proceeding.

This article provides a brief overview of current methods of debt restructuring under Czech law and introduces the new possibilities made available under the upcoming Restructuring Act.

Informal restructuring (i.e., outside of formal insolvency proceedings) currently lacks complex legal regulation under Czech law. A debtor in financial distress (i.e., not yet insolvent as defined by the Act) may seek to achieve a restructuring of its indebtedness via negotiations with creditors.

Restructuring Is Currently Achievable on a Contractual Basis Only. The Main Drawbacks Are That:

The latter may very well be a major disincentive for creditors to agree to a contractual restructuring. The current disadvantages of pre-insolvency restructuring may be addressed by the preventive restructuring process under the Restructuring Act.

Czech insolvency law currently distinguishes between two methods of resolving a company’s insolvency.

- Bankruptcy – aimed at selling off the insolvent company’s assets with a pro-rata satisfaction of creditors according to their classes from the proceeds of the sale.

- Reorganization – aimed at rehabilitating the company by implementing various reorganization measures which may be operational (focused on the company’s business, products, etc.).

While bankruptcy means the liquidation of the debtor’s business and the sale of its assets, and so does not represent any restructuring of debts, reorganization typically includes substantial financial reorganization measures, i.e., debt restructuring.

In addition, Czech insolvency law allows for the declaration of a moratorium on debtor assets, giving a company some breathing space to overcome its financial difficulties, and thus averting an insolvency proceeding.

For transparency purposes, any steps and documents related to an ongoing insolvency proceeding (e.g., the decisions of an insolvency court, the notices of the insolvency administrator, creditor applications, or debtor documents) are regularly published in a public insolvency register.

A reorganization proceeding is based on three core processes:

- maintaining the operations of an insolvent company while complying with the given court-approved reorganization plan,

- implementing reorganization measures prescribed by the reorganization plan, and

- the continuous supervision of its implementation by the creditors and the insolvency administrator.

Throughout the reorganization, the insolvent company satisfies the claims of the registered creditors, which are typically reduced by a certain ‘hair-cut’ under the reorganization plan. Necessary claims or those directly intended to maintain operations of the affected business, such as external working capital financing, may be paid by the company preferentially and in full, if the reorganization plan so provides.

The insolvent company may also dispose with its assets in the ordinary course of business. However, certain legal acts are reserved for the insolvency administrator or can only be taken with the consent of a creditors’ committee.

Reorganizations are only available for medium to large companies with a yearly turnover of more than approx. €2mn or with at least 50 employees. This approach may be preferred by creditors, as one of the legal conditions is that the satisfaction of creditors will not be lower than under bankruptcy. Long-term statistical data suggests that the satisfaction of unsecured creditors in bankruptcy is around 4.5% of the nominal value of respective receivables, compared to 10.5% with reorganizations.

A reorganization proceeding is based on three core processes:

- maintaining the operations of an insolvent company while complying with the given court-approved reorganization plan,

- implementing reorganization measures prescribed by the reorganization plan, and

- the continuous supervision of its implementation by the creditors and the insolvency administrator.

Throughout the reorganization, the insolvent company satisfies the claims of the registered creditors, which are typically reduced by a certain ‘hair-cut’ under the reorganization plan. Necessary claims or those directly intended to maintain operations of the affected business, such as external working capital financing, may be paid by the company preferentially and in full, if the reorganization plan so provides.

The insolvent company may also dispose with its assets in the ordinary course of business. However, certain legal acts are reserved for the insolvency administrator or can only be taken with the consent of a creditors’ committee.

Reorganizations are only available for medium to large companies with a yearly turnover of more than approximately €2mn or with at least 50 employees. This approach may be preferred by creditors, as one of the legal conditions is that the satisfaction of creditors will not be lower than under bankruptcy. Long-term statistical data suggests that the satisfaction of unsecured creditors in bankruptcy is around 4.5% of the nominal value of respective receivables, compared to 10.5% with reorganizations.

Czech insolvency law also provides for the possibility of a so-called pre-pack reorganization. This is agreed between the insolvent company and its creditors before filing an insolvency petition, and filed with the reorganization plan. The insolvency court then approves the commencement of the reorganization together with the declaration of insolvency, which speeds up the entire insolvency process.

Pre-pack reorganizations require a higher degree of awareness and flexibility on the part of the debtor’s management staff. They can only be achieved in the event of a debtor detecting their respective financial problems early and beginning negotiations with creditors well in advance.

The number of pre-pack reorganizations is increasing due to their higher success rate. Between 2016 and 2019, 34 of the existing 67 reorganizations were pre-packed1. Yet, reorganizations still represent only a fraction of the total 4,161 insolvency proceedings during this same period. This is due to the legal conditions for entering a reorganization (i.e., the turnover threshold or number of staff) and the unwritten rule that the insolvent company must have something actually worth saving (such as a profitable product) so that creditors are willing to consider approving reorganization.

In practice, most reorganizations are later transformed into bankruptcy proceedings due to the debtor’s inability to comply with the reorganization plan, produce a reorganization plan that could be presented to creditors for approval, or due to the fact the presented plan has not gained creditor or insolvency court approval, or an inability to comply with the reorganization plan after it has been approved.

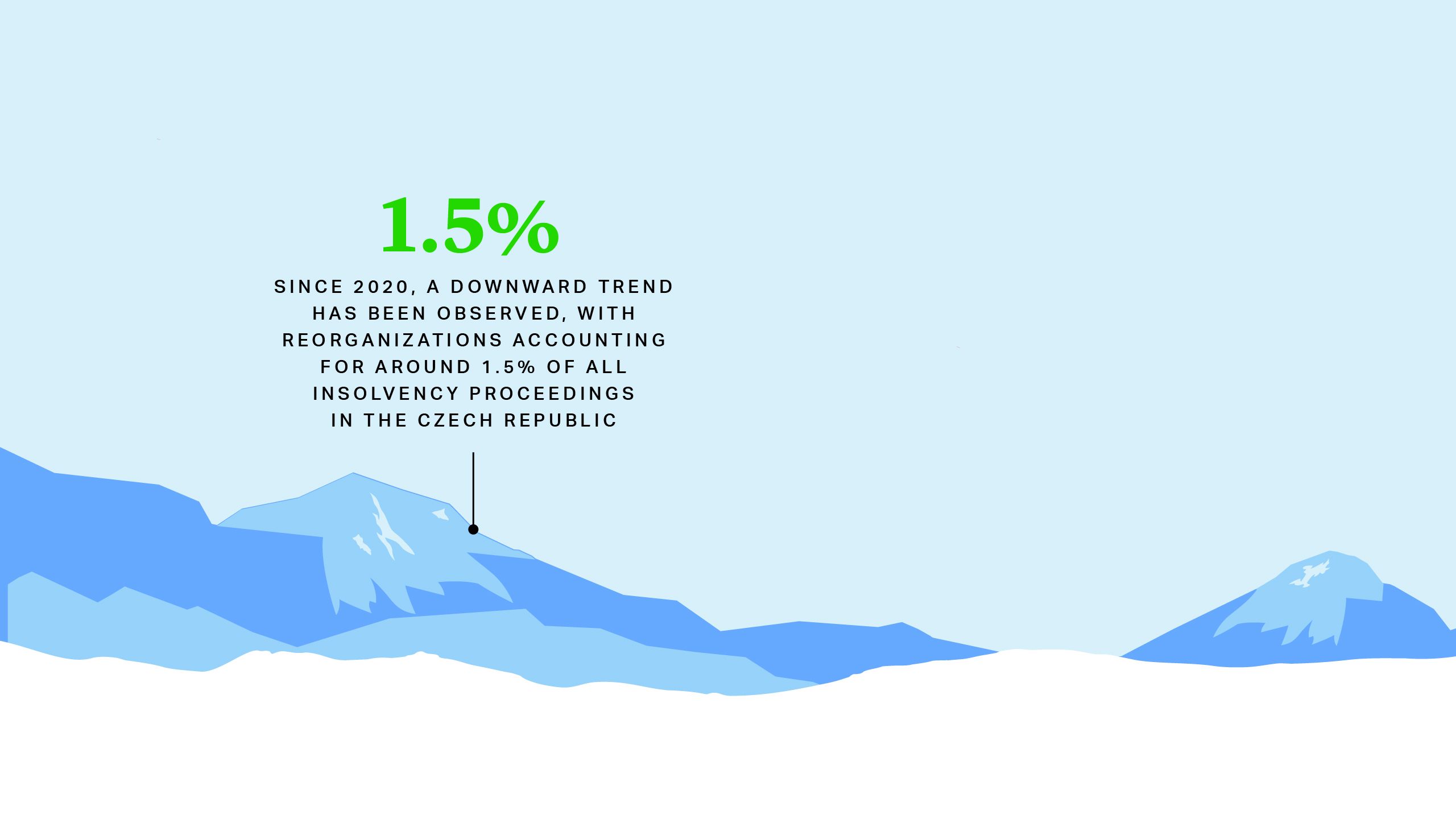

According to recent data, the number of reorganizations is decreasing, while the number of bankruptcy proceedings (i.e., the liquidation of debtor assets) is on the rise. Reorganizations have consistently accounted for between 2-3% of all insolvency proceedings. Since 2020, a downward trend has been observed, with reorganizations accounting for around 1.5% of all insolvency proceedings in the Czech Republic2.

While reorganization is de facto the only viable means of financial indebtedness restructuring via a formal statutory procedure, Czech insolvency law provides for a moratorium on the debtor’s property, which aims to save the given company from imminent bankruptcy. A moratorium–unlike a reorganization–can be granted before the court formally declares the company insolvent, or before the insolvency proceeding is even initiated.

The main purpose of a moratorium is to provide a company with time to address its respective financial difficulties before a court rules on insolvency. It is granted by the insolvency court at the request of the debtor with the consent of a majority of creditors for a period no longer than three months, with the possibility of extending the moratorium for another 30 days.

During the moratorium period, the court cannot issue an insolvency decision, and for its duration, the company may give priority to debt payments directly related to the maintenance of its operations (e.g., energy bills and the supply of raw materials necessary for production). Creditors providing services which are crucial for the maintenance of the business are not entitled to terminate their respective service contracts. A moratorium is terminated upon the expiry of its duration or by a decision of the majority of creditors.

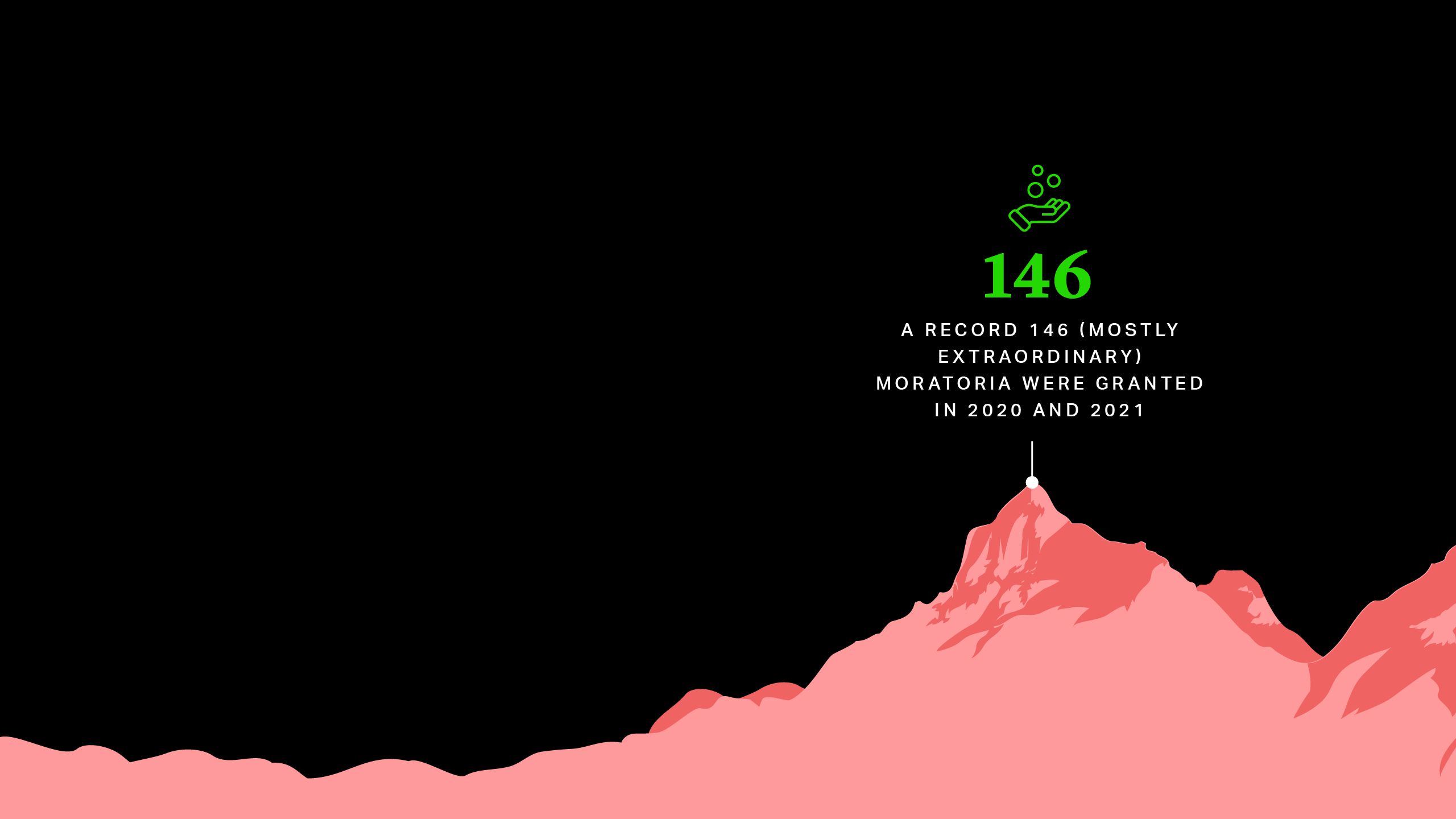

Prior to the COVID-19 pandemic, the number of moratoria varied between two and 18 per year due to the reluctance of creditors to grant approvals. Subsequently, extraordinary moratoria that no longer required the consent of the majority of creditors were newly introduced into Czech insolvency law. A record 146 (mostly extraordinary) moratoria were thus granted in 2020 and 2021.

The Restructuring Act was not implemented within the deadline set by the Directive and is still being drafted, but its main principles should already be evident. This summary is based on the latest draft of the Act, which the Ministry of Justice is still reworking and may be subject to material change.

According to the draft, preventive restructuring will be on a voluntary basis and will serve to avert company insolvency. It may not be approved if the company is already insolvent. The purpose of the planned Restructuring Act is to provide a legal framework to enable companies in financial difficulties to reach a debt restructuring agreement with their creditors.

To initiate the restructuring procedure, a company must draw up a financial rehabilitation plan in which it lists its assets and liabilities, as well as any affected creditors and their division into groups. The plan should also provide a description of the recovery and restructuring measures, and the reasons for their introduction. Adopting the plan is dependent on a decision by company creditors affected by the restructuring. The draft act also envisages a restructuring trustee, but unlike insolvency proceedings, it does not always need to be appointed via a restructuring process and can be appointed by the restructuring court.

Unlike insolvency proceedings, the given restructuring process will not be supervised by the courts. Restructuring proceedings may be triggered ad hoc at the request of the debtor or creditor to resolve disputes arising in debt restructuring negotiations, or the exercise of a power vested in the court by the Restructuring Act, such as granting a moratorium. Thus, separate restructuring proceedings may run concurrently as a part of an overall restructuring–or none at all–unless a disagreement exists between the debtor and affected creditors.

To initiate the restructuring procedure, a company must draw up a financial rehabilitation plan in which it lists its assets and liabilities, as well as any affected creditors and their division into groups. The plan should also provide a description of the recovery and restructuring measures, and the reasons for their introduction. Adopting the plan is dependent on a decision by company creditors affected by the restructuring. The draft act also envisages a restructuring trustee, but unlike insolvency proceedings, it does not always need to be appointed via a restructuring process and can be appointed by the restructuring court.

Unlike insolvency proceedings, the given restructuring process will not be supervised by the courts. Restructuring proceedings may be triggered ad hoc at the request of the debtor or creditor to resolve disputes arising in debt restructuring negotiations, or the exercise of a power vested in the court by the Restructuring Act, such as granting a moratorium. Thus, separate restructuring proceedings may run concurrently as a part of an overall restructuring–or none at all–unless a disagreement exists between the debtor and affected creditors.

The draft Restructuring Act provides for both public and private restructuring. In certain circumstances, the entire restructuring may be conducted in private. This is likely to be the more common form and will involve only the debtor’s key creditors. A public restructuring will take into account all company creditors. Information on its progress will be published in the restructuring register and conducted by the restructuring court, resulting in public disclosure.

In order to avoid the enforcement of creditor claims while the preventive restructuring is pending, a debtor can apply for a moratorium of up to six months, during which the debtor is protected against insolvency petitions and enforcement proceedings.

The concept of preventive restructuring proposed by the Restructuring Act could make it easier for companies to negotiate with creditors to restructure their respective financial indebtedness. This may resolve some of the current disadvantages of informal, contractual restructuring – the preventive restructuring will introduce creditor voting in particular classes, inspired by reorganization/insolvency proceedings, and the protection of restructuring measures in a subsequent insolvency. However, as a less formal process, this will be entirely dependent on the willingness of the parties concerned to negotiate with debtors. As such, there is legitimate concern that preventive restructuring will be used by distressed companies merely as a means to delay inevitable insolvency proceedings, through a moratorium, rather than as a legitimate tool to avert them.

Václav Kment

Senior Associate, Kinstellar

Prague

T: +420 221 622 118

vaclav.kment@kinstellar.com

V-Card