A progressive regime that allows for a flexible, yet speedy restructuring is crucial for companies looking to restructure their indebtedness. With its stable and commerce-oriented market, well-functioning courts with the highest-caliber of common law judges, advanced digital landscape, and vast resources, including practical guides for corporate stakeholders, the Abu Dhabi Global Market (ADGM) has all the right attributes to become a preferred restructuring hub in the region.

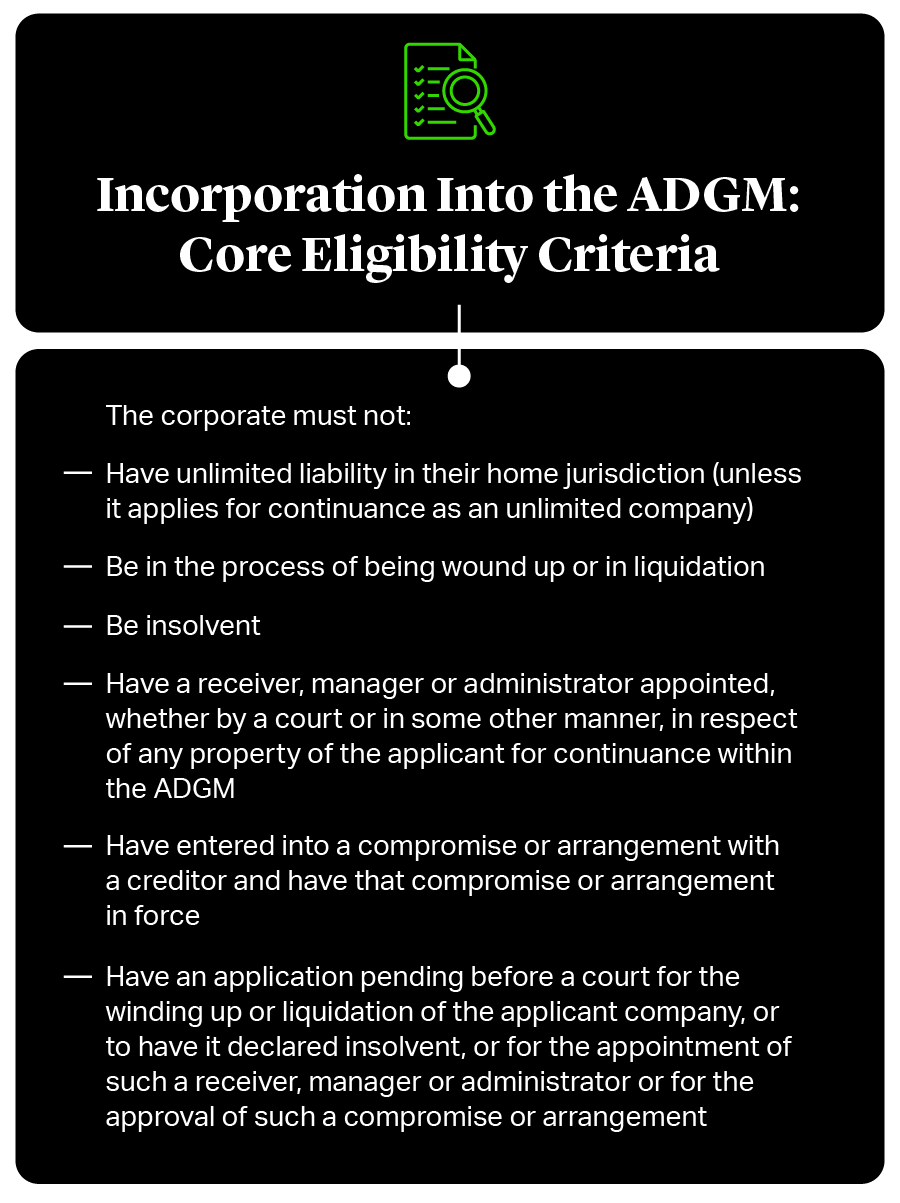

The ADGM restructuring regime is generally available to companies incorporated in the ADGM. The regime provides certain flexibility, albeit at the moment available primarily to solvent companies, allowing debtors to migrate into the ADGM1. To be eligible, the law of the original jurisdiction must permit continuance in other jurisdictions2. In order to migrate into the ADGM, certain customary information must be provided, including certified constitutional documents, a statement of solvency, and particulars of directors3. To facilitate redomiciliation, the ADGM has published a helpful continuance guidance as well as a checklist for prospective registrants.

An insolvent company, in general, would be unable currently to migrate into the ADGM. That said, the Registrar can disapply the requirement for the company to be solvent on public policy grounds (the amendment was introduced to allow NMC Health to take advantage of the ADGM administration regime and could potentially be available for other companies).

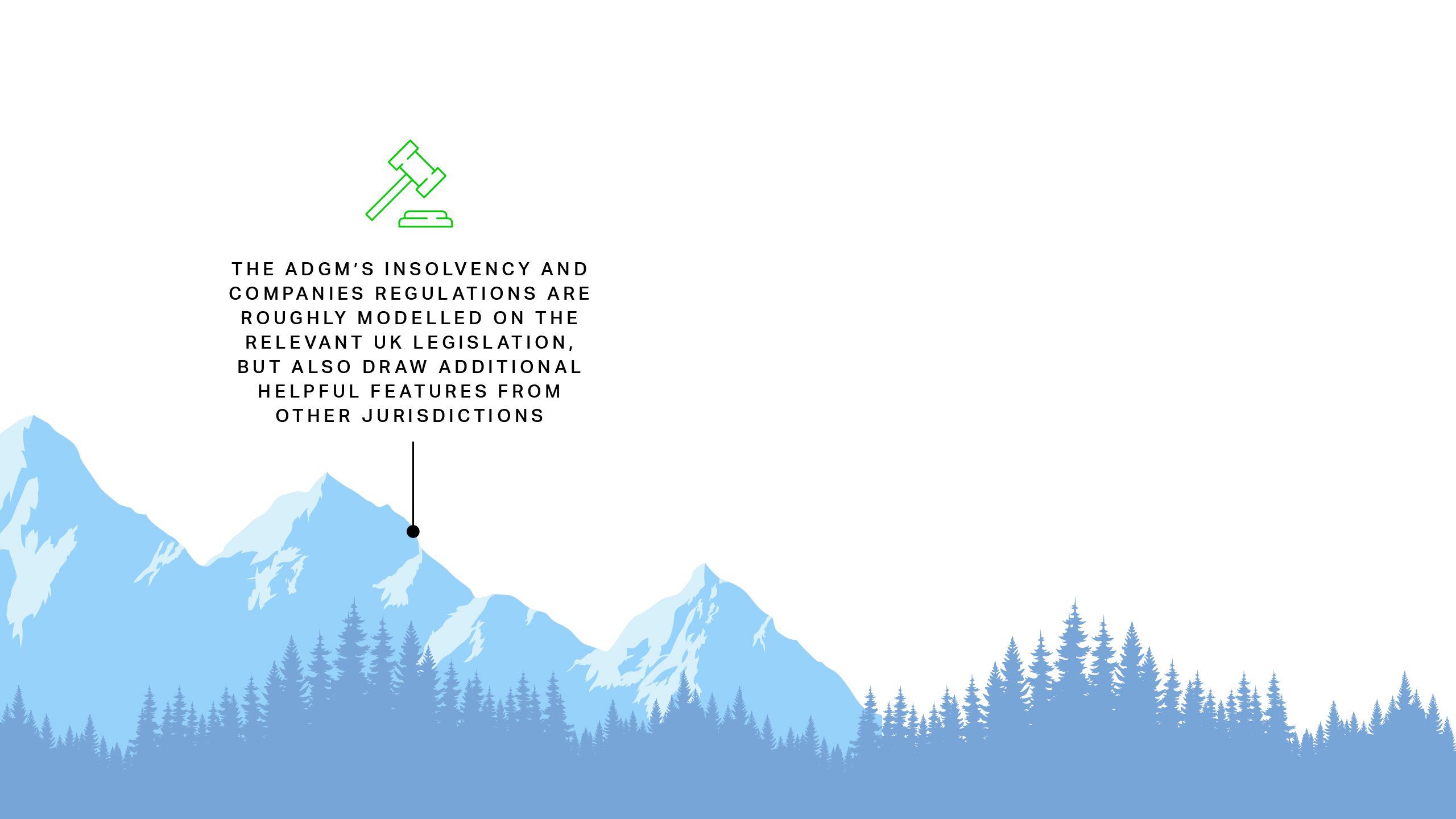

The ADGM restructuring regime is primarily embedded in the ADGM Insolvency Regulations 2022 (the Insolvency Regulations) and the ADGM Companies Regulations 2020 (as amended) (the Companies Regulations) and contemplate the following key restructuring options: administration, including DOCA, and schemes of arrangement. Liquidation/winding up is not separately analyzed given the focus on restructuring business as a going concern. Both pieces of regulation are roughly modelled on the relevant UK legislation, but also draw additional helpful features from other jurisdictions.

The ADGM restructuring regime is primarily embedded in the ADGM Insolvency Regulations 2022 (the Insolvency Regulations) and the ADGM Companies Regulations 2020 (as amended) (the Companies Regulations) and contemplate the following key restructuring options: administration, including DOCA, and schemes of arrangement. Liquidation/winding up is not separately analyzed given the focus on restructuring business as a going concern. Both pieces of regulation are roughly modelled on the relevant UK legislation, but also draw additional helpful features from other jurisdictions.

1. Administration

An administrator may be appointed to manage the affairs, business, and property of a distressed company. An administrator is appointed for the following objectives (in the following priority): (a) rescuing the company as a going concern; (b) achieving a better result for the creditors as a whole (compared to if the company was wound up); and (c) realizing property in order to make a distribution to one or more secured or preferential creditors. The administrator must perform its functions in the interests of the creditors as a whole. To be considered for appointment, an administrator must be registered as an insolvency practitioner with the ADGM.

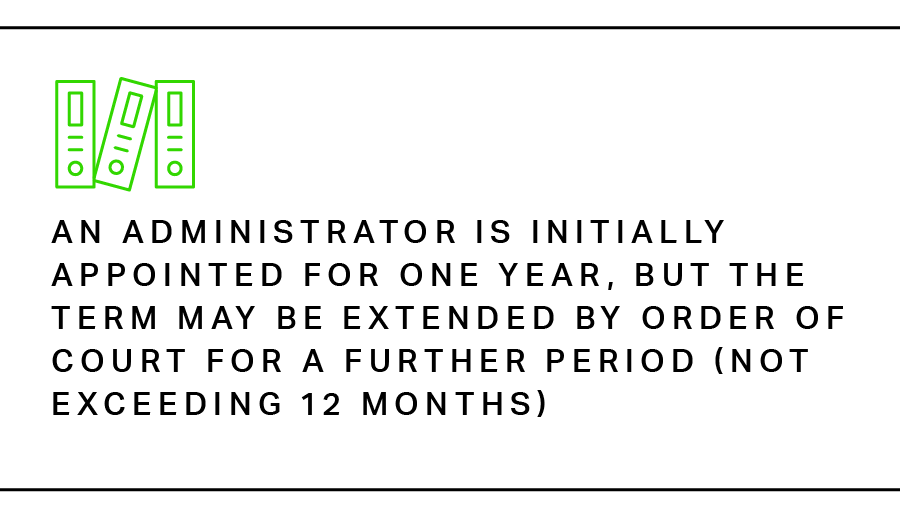

An administrator is initially appointed for one year, but the term may be extended by order of court for a further period (not exceeding 12 months). Following the making of an administration order, any petition for the winding-up of the company, as well as any previously appointed administrative receiver or other receiver (if the administrator so orders) shall be dismissed.

When the administration order takes effect, a moratorium will apply in respect of insolvency proceedings, as well as other legal processes involving the company. Any pending winding up petitions shall be dismissed, and administrative receivers shall vacate the office.

The administration process roughly follows its UK equivalent. However, it has certain additional features, e.g., DOCA (described in more detail below).

An administrator is initially appointed for one year, but the term may be extended by order of court for a further period (not exceeding 12 months). Following the making of an administration order, any petition for the winding-up of the company, as well as any previously appointed administrative receiver or other receiver (if the administrator so orders) shall be dismissed.

When the administration order takes effect, a moratorium will apply in respect of insolvency proceedings, as well as other legal processes involving the company. Any pending winding up petitions shall be dismissed, and administrative receivers shall vacate the office.

The administration process roughly follows its UK equivalent. However, it has certain additional features, e.g., DOCA (described in more detail below).

2. Dealing with Secured Property

The administrator can deal with certain charged property subject to the following considerations:

2. Dealing with Secured Property

The administrator can deal with certain charged property subject to the following considerations:

3. New Financing

Chapter 9A of the Insolvency Regulations allows the debtor to incur unsecured debt while administration is in place. Such credit or debt will be payable as an expense of the administration giving it priority in potential liquidation. Notably and in the absence of existing secured creditors’ consent or court approval, such debt can only be incurred on an unsecured basis.

An administrator may, however, apply to the court to incur such debt on a secured basis including secured on property that is already subject to a security interest with new security ranking pari passu or above existing security interest if it is unable to obtain such credit otherwise and there is “adequate protection” of the interest of the holder of existing security interest.

“Adequate protection” is deemed provided if the court is satisfied that (i) the provision of credit or debt would enable the administrator to achieve the first two objectives of the administration: rescue the company as a going concern or achieve a better result for the creditors as a whole (compared to if the company was wound up); and (ii) the grant of security is likely to achieve a better result for each creditor benefiting from an existing security.

4. Deed of Company Arrangement

The DOCA is a bespoke concept that has been introduced in the ADGM restructuring regime. DOCA provides for an agreed framework governing the debtor’s affairs with the approval of the requisite majority of creditors. The purpose of a DOCA is to maximize the chances of the company remaining in business and it may also result in a better return for creditors than a winding up of the company.

The process involves the administrator preparing an instrument setting out the terms of the arrangement to deal with the debtor’s outstanding debts. A resolution adopting the instrument needs to be passed by a simple majority of creditors (by value) voting at the relevant meeting. All creditors vote as a single class. The administrator of the company will typically act as the administrator of the DOCA, unless otherwise resolved at the creditors’ meeting.

All unsecured creditors are bound by the DOCA with respect to claims arising on or before the record date. A secured creditor/owner or lessor of property may realize or deal with secured property unless the DOCA (subject however to such secured creditor’s consent) or the court provides otherwise. The court may make an order for a secured creditor not to realize or otherwise deal with their security where such dealing or realization will have a material adverse effect on achieving the purpose of the DOCA, so long as the court is satisfied in light of the relevant circumstances that the creditor’s interests will be adequately protected.

The DOCA must contain a provision giving priority to preferential creditors, ensuring that preferential debts (such as employment costs and other contributions) would rank equally, or abate in equal proportions (in the event that the available assets are insufficient to satisfy the preferential debts owed). The terms of a DOCA may be varied at a creditors’ meeting. A DOCA will terminate on the first to occur of:

a) a court order, where: (i) any material false or misleading information was provided about the company’s business, property, affairs, or financial circumstances; (ii) there has been a material breach of the DOCA by a person bound by it, or a material omission in a report or statement issued by the company; (iii) effect cannot be given to the DOCA without injustice or unreasonable delay; or (iv) the DOCA will be oppressive, unfairly prejudicial, discriminatory, or contrary to the interest of creditors. Application for a court order may be made by a creditor, the company, the ADGM Financial Services Regulator, or any interested person;

b) pursuant to validly convened creditors’ meeting (in the event of a breach which has not been rectified). Creditors may also resolve at the meeting that the company be wound up;

c) occurrence of termination event(s) specified in the DOCA; or

d) execution of a notice of termination by the administrator where: (i) all the proceeds of the realization of assets have been paid to creditors; (ii) the administrator has paid the full amount outstanding, or such lesser sum as determined by creditors at a general meeting; or (iii) obligations under the DOCA have been fulfilled and creditors’ claims have been addressed. The administrator must lodge a notice of termination with the ADGM Registrar within 28 days.

Upon application by an interested person, the court may void or validate a DOCA where there is specific doubt regarding compliance of the DOCA with the provisions of the Insolvency Regulations. Nonetheless, the court may declare the DOCA (or a provision thereof) valid notwithstanding a breach, provided that the provision was substantially complied with, and such decision will not amount to injustice. Where a court declares a provision void, the court may vary the DOCA with the consent of the administrator. Termination or avoidance (whether partial or full) of the DOCA does not affect the previous operation of the DOCA5.

Upon application by an interested person, the court may void or validate a DOCA where there is specific doubt regarding compliance of the DOCA with the provisions of the Insolvency Regulations. Nonetheless, the court may declare the DOCA (or a provision thereof) valid notwithstanding a breach, provided that the provision was substantially complied with, and such decision will not amount to injustice. Where a court declares a provision void, the court may vary the DOCA with the consent of the administrator. Termination or avoidance (whether partial or full) of the DOCA does not affect the previous operation of the DOCA5.

5. Schemes of Arrangement

Modelled against the English law scheme of arrangement (SoA), this framework allows making of a compromise or arrangement between a company and its creditors or members. Following an application to the court by the company, any creditor or member of the company, liquidator, or administrator, the court may order a meeting of creditors or members (or a class of them). Similar to the English SoA, the debtor’s management will continue to run the company while the process is continuing. Equally, a moratorium will not automatically apply on launching of an SoA, unless the process is coupled with another insolvency procedure such as administration.

An arrangement must be approved by 75% in value of creditors present at the meeting and sanctioned by the court. Unlike English law SoA, there is no requirement for approval by a majority in number. Once sanctioned by the court, a scheme of arrangement shall be binding on the company and all creditors or class of creditors (as the case may be) subject to the scheme, irrespective of whether they participated in the meeting or voted in favor.

Unlike the English scheme of arrangement, the ADGM SoA is currently available primarily to ADGM-incorporated entities or redomiciled entities, with limited exceptions for non-ADGM companies. Where the arrangement relates to a non-ADGM company (i.e., companies that are not formed or registered under ADGM law), certain requirements must be satisfied before the court can sanction the arrangement, including making a statement of solvency, and obtaining all necessary authorizations as required by the laws of the jurisdiction of incorporation (or where the company is currently registered).

6. DOCA vs Scheme of Arrangement

There are a number of similarities between schemes and DOCAs and regimes are largely targeted at achieving the same outcome – compromising outstanding liabilities. Overall, both options are flexible instruments that can be adapted to the company’s needs.

DOCA can only be utilized after the company has entered administration, which would necessitate a relinquishment of control by the management of the company, and could create a negative perception of the company, potentially leading to a lower credit rating and loss in value. A scheme, on the other hand, can be implemented pre-insolvency, with the existing management remaining in control (notably a scheme can also be utilized in administration).

DOCA binds all the company’s unsecured creditors and assenting secured creditors to the contractual terms from the date administrators were appointed. A scheme, on the other hand, is only binding on a class/group of creditors expressly made subject to the scheme which, depending on the ultimate purpose of the arrangement, can be useful. That said, DOCA only requires a simple majority approval of all creditors (by value), unlike a scheme which requires the approval of 75% (by value) of creditors in each class. The choice between the tools may be driven by the likely support the company is hoping to obtain.

There are also certain limitations to take into account when dealing with secured creditors’ interests through DOCA, particularly because a DOCA has limited capacity to affect the rights of secured creditors or owners of leased property, unless these creditors or owners consent to the DOCA arrangement or the court exercises its discretion to bind secured creditors.

In accordance with the Insolvency Regulations, a DOCA can be amended by a resolution drawn up by creditors. A scheme, on the other hand, does not normally provide for an option to modify its terms, and a new scheme would likely be required.

NMC Health PLC (formerly listed on the London Stock Exchange) and its operating subsidiaries entered the UK administration in April 2020 following legal action brought by some of its creditors. Following their redomiciliation to the ADGM, 34 NMC operating companies subsequently filed for voluntary administration in the ADGM in September 2020.

Pursuant to a September 2020 ADGM decision, the ADGM courts ruled inter alia that the joint administrators (i) shall be at liberty to apply for recognition of the administrations outside the ADGM and (ii) may act as foreign representative on behalf of the NMC entities.

NMC Health PLC (formerly listed on the London Stock Exchange) and its operating subsidiaries entered the UK administration in April 2020 following legal action brought by some of its creditors. Following their redomiciliation to the ADGM, 34 NMC operating companies subsequently filed for voluntary administration in the ADGM in September 2020.

Pursuant to a September 2020 ADGM decision, the ADGM courts ruled inter alia that the joint administrators (i) shall be at liberty to apply for recognition of the administrations outside the ADGM and (ii) may act as foreign representative on behalf of the NMC entities.

In September 2021, NMC’s operating companies entered a DOCA (discussed above), with the aim of implementing a financial restructuring of the NMC group. The DOCA was executed in accordance with the Insolvency Regulations. 95% of eligible creditors voted in favor of the restructuring plan, while unsecured creditors settled claims on existing debt in exchange for certain exit instruments in a new facility. The joint administrators collaborated with the creditors during the restructuring process and implemented a three-year business plan. The companies became subsidiaries of a newly formed ADGM holding company, NMC OpCo Limited, in just under two years, following completion of the process in March 2022.

Among other things, the landmark restructuring of the 34 operating companies under the auspices of the “ADGM’s best-practice regulatory framework serve[d] as a precedent in the United Arab Emirates (UAE) for taking a complex business through a transparent, fair and timely process to establish a new capital structure”6, solved the challenge of non-recognition of foreign court orders by UAE courts and ultimately ensured the viability of the business.

In September 2021, NMC’s operating companies entered a DOCA (discussed above), with the aim of implementing a financial restructuring of the NMC group. The DOCA was executed in accordance with the Insolvency Regulations. 95% of eligible creditors voted in favor of the restructuring plan, while unsecured creditors settled claims on existing debt in exchange for certain exit instruments in a new facility. The joint administrators collaborated with the creditors during the restructuring process and implemented a three-year business plan. The companies became subsidiaries of a newly formed ADGM holding company, NMC OpCo Limited, in just under two years, following completion of the process in March 2022.

Among other things, the landmark restructuring of the 34 operating companies under the auspices of the “ADGM’s best-practice regulatory framework serve[d] as a precedent in the United Arab Emirates (UAE) for taking a complex business through a transparent, fair and timely process to establish a new capital structure”6, solved the challenge of non-recognition of foreign court orders by UAE courts and ultimately ensured the viability of the business.

Areas for Development

While the ADGM restructuring regime has been designed as a purpose-built tool to facilitate rescuing distressed companies and allowing the business to continue as a going concern, there remain a few areas for enhancement.

Eligibility

The administration process and scheme of arrangement generally are available to ADGM-incorporated entities or redomiciled companies, with limited exceptions for non-ADGM companies and (as noted above under the heading “schemes of arrangement”) subject to additional requirements. Additional flexibility allowing distressed companies to migrate and (in the schemes context) possibly expanding the notion of sufficient connection with ADGM could prove to be a useful feature, allowing a broader selection of MENA debtors to be able to benefit from the ADGM restructuring regime.

Recognition

One of the critical areas for further advancement will be to allow the recognition and enforceability of ADGM decisions in other jurisdictions without the need to initiate a new/parallel restructuring process. This is particularly important for other UAE jurisdictions in the first instance, and possibly other Gulf Cooperation Council (GCC) jurisdictions. In this regard, it is crucial to note that Article 170 of the ADGM Courts, Civil Evidence, Judgments, Enforcement and Judicial Appointments Regulations 2015 provides for an automatic application of treaties entered into by the UAE for the recognition and enforcement of judgements, to the ADGM courts.

Additionally, the ADGM courts have entered into various memoranda of understanding (MOUs) with the UAE Ministry of Justice, the Abu Dhabi Judicial Department, and the courts of the Emirate of Ras Al Khaimah, as well as other foreign jurisdictions (such as Singapore, Hong Kong, and Australia) in connection with reciprocal enforcements of judgments7. Whereas, pursuant to these MOUs, judgments (including arbitral awards and final orders) generally seem to be enforceable, there are however limited channels for the support of insolvency proceedings more broadly (other than in reliance on Model Law, to the extent it is adapted in the relevant jurisdiction, which may not always be the case). Even where Model Law is adopted (e.g., the Dubai International Financial Center (DIFC)) there may be practical difficulties in recognizing the ADGM proceedings in reliance on it (and, in the NMC Health case for instance, recognition was sought instead on the basis of common law and comity).